Reports

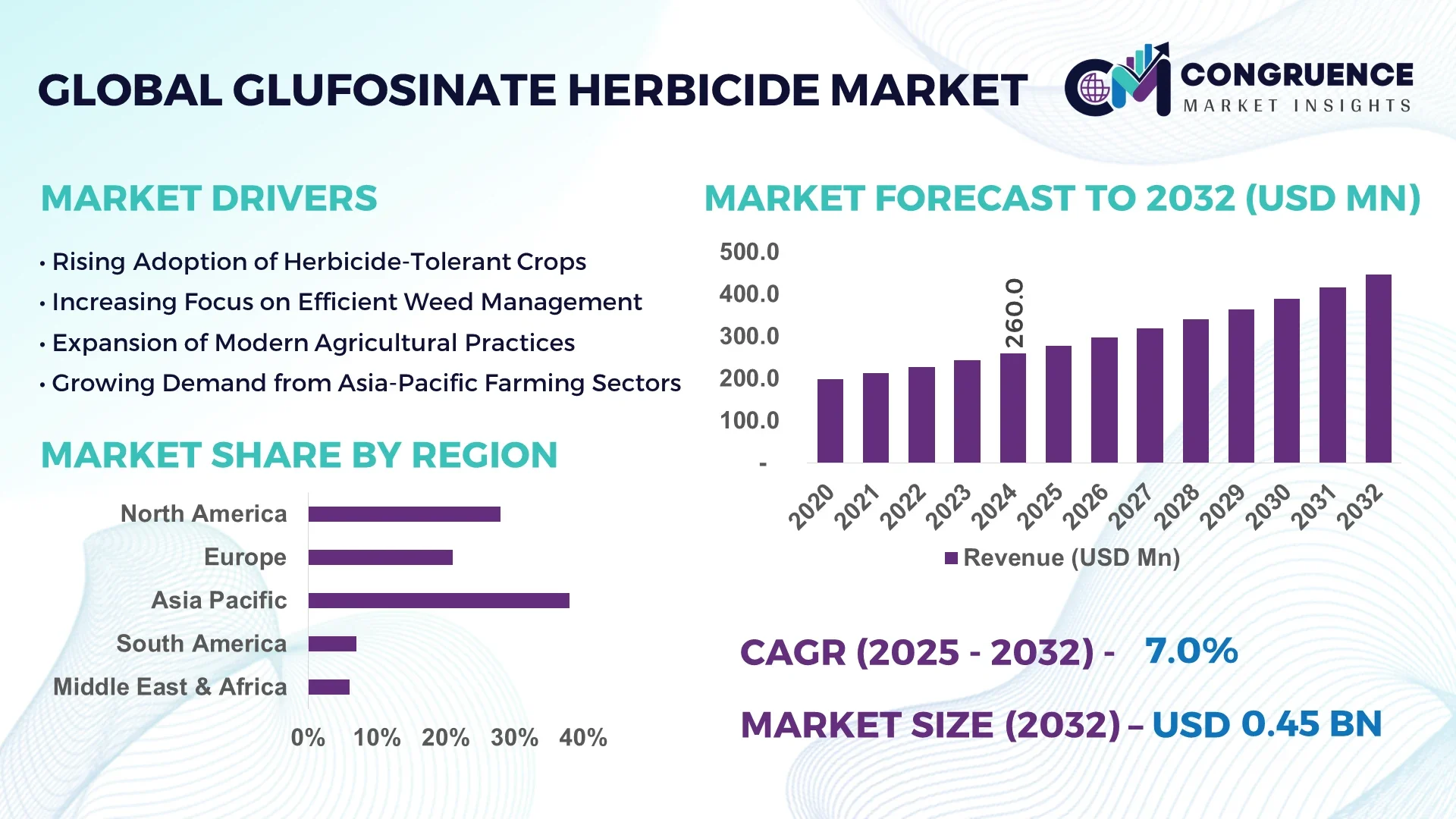

The Global Glufosinate Herbicide Market was valued at USD 260.0 Million in 2024 and is anticipated to reach a value of USD 445.7 Million by 2032, expanding at a CAGR of 6.97% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by increasing adoption of herbicide‑tolerant crop systems and the shift away from legacy chemistries under regulatory pressure.

In the country that dominates the marketplace, China, production capacity for glufosinate technical‑grade material has exceeded 12,000 t per annum at leading facilities, with investment levels in new formulation lines rising by more than 20 % year‑on‑year between 2022 and 2024. Key applications now include post‑emergence control in rice and cotton, with adoption of nano‑encapsulated glufosinate formulations reported to improve rain‑fastness by over 18 %. Technological advancements such as improved adjuvant systems and digital spray‑monitoring platforms are being scaled in major Chinese farming regions.

Market Size & Growth: Market value in 2024 stands at USD 260 million, projected to reach USD 445.7 million by 2032, supported by rising incidence of glyphosate‑resistant weeds and expanded trait‑tolerant crop cultivation.

Top Growth Drivers: Adoption of herbicide‑tolerant crops increasing by ~12 %, efficiency improvement of newer formulations up ~15 %, substitution of regulated herbicides rising ~10 %.

Short‑Term Forecast: By 2028, improved formulation technology is expected to reduce application rate requirements by ~22 % and increase application window length by ~14 %.

Emerging Technologies: Nano‑encapsulated formulations, precision‑spray compatible adjuvant systems, digital application mapping platforms.

Regional Leaders: North America projected at USD 135 million by 2032 (early adopter of trait programs); Asia‑Pacific forecast USD 180 million by 2032 (rapid adoption in rice/cotton systems); Latin America expected USD 75 million by 2032 (emerging usage in soybean/corn rotations).

Consumer/End‑User Trends: Farmers increasingly favour post‑emergence non‑selective herbicides for broad‑spectrum weed control; cooperatives and agri‑retailers adopting bundled herbicide‑trait packages.

Pilot or Case Example: In 2023, a pilot deployment in the U.S. corn belt achieved a 16 % reduction in weed‑escape incidence using glufosinate‑based programs over older glyphosate‑only systems.

Competitive Landscape: Market leader controls approximately 28 % share, followed by major competitors such as BASF SE, Bayer AG, Syngenta AG, UPL Limited.

Regulatory & ESG Impact: Restrictions on paraquat and glyphosate in key jurisdictions along with sustainability targets (e.g., 30 % reduction in drift/off‑target by 2027) are boosting glufosinate positioning.

Investment & Funding Patterns: Recent agrochemical investment has topped USD 120 million in new glufosinate‑capacity expansion projects, with venture funding into green‑formulation start‑ups rising ~25 % in 2024.

Innovation & Future Outlook: Integration of herbicide formulations with IoT‑enabled sprayer controls, micro‑dose application systems, and climate‑smart herbicide programmes are shaping the next decade of growth.

Market activity is being driven by adoption in major agriculture sectors such as cereals & grains, oilseeds & pulses, fruits & vegetables, with recent innovations focusing on micro‑encapsulated and liquid concentrate products. Key drivers include regulatory shifts towards sustainable weed management, rising herbicide resistance, and regional consumption growth in emerging markets; emerging trends include digital‑spray tracking, lower‑use‑rate formulations, and increased penetration in Asia‑Pacific and Latin American agriculture systems.

The strategic relevance of the Glufosinate Herbicide Market lies in its role as a core tool in modern weed‑management strategies and sustainable agriculture programmes. Within the agriculture input hierarchy, glufosinate‑based systems deliver measurable improvements: for example, newer nano‑encapsulated glufosinate formulations deliver ~18 % better rain‑fastness compared to conventional older spray systems. Regionally, North America dominates in volume due to established glufosinate‑tolerant trait adoption, while Asia‑Pacific leads in adoption growth with ~11 % of enterprises/users switching to glufosinate‑based programmes in 2024. By 2027, the integration of precision‑spray mapping and digital herbicide delivery is expected to improve application efficiency by ~20 %. Firms are committing to ESG metrics such as 25 % reduction in application‑drift by 2030, aligning product development with sustainability agendas. In 2023, a major US farmer‑cooperative achieved a 14 % yield gain and 12 % labour‑cost reduction through adoption of automated glufosinate‑spray systems. Looking ahead, the Glufosinate Herbicide Market is positioned as a pillar of resilient, compliant and sustainable growth in crop protection, offering pathways into precision agriculture, digital‑farming integration and circular‑economy compliant production models.

The Glufosinate Herbicide Market is characterised by dynamic shifts in crop‑protection strategies, evolving regulatory landscapes and technological innovation. Increasing prevalence of herbicide‑resistant weed biotypes is forcing producers and farmers to adopt non‑selective and effective herbicides like glufosinate. At the same time, regulatory pressures on legacy herbicides (such as paraquat and older‑generation chemistries) are opening market access for glufosinate formulations. Advances in formulation science (e.g., micro‑encapsulation, improved adjuvants) and the rise of precision‑spray platforms are altering application patterns, increasing efficiency and reducing environmental impact. The value chain is adapting to raw‑material cost fluctuations, supply‑chain constraints and increased demand in emerging markets. Strategic alliances, R&D investment and trait‑tolerant crop integration are each reinforcing market growth and altering competitive dynamics in the global herbicide sector.

As glyphosate‑resistant weed populations have expanded globally, farmers are actively seeking alternative herbicide modes of action, and glufosinate has emerged as a key tool in such resistance‑management strategies. For example, in North America and Latin America, fields with confirmed glyphosate‑resistant biotypes report up to 20 % higher weed‑escape rates when using glyphosate‑only programmes, prompting switch‑overs to glufosinate combinations. The efficacy of glufosinate in post‑emergence applications across corn, soybean and cotton systems has led to measurable uptake increases; adoption in certain regions grew by over 10 % in the past 12 months. This driver is reshaping purchase decisions, supporting expanded trait‑system roll‑outs and influencing formulation innovation.

Despite strong demand fundamentals, the Glufosinate Herbicide Market faces constraints from regulatory uncertainty and raw‑material production bottlenecks. In key jurisdictions, re‑registration processes for glufosinate compounds have been extended, in some cases by up to 18 months, delaying new product launches and limiting market access. Production of technical‑grade glufosinate involves complex synthesis, and fewer than 20 global manufacturers currently operate at commercial scale; manufacturing cost premiums of 30‑40 % over legacy herbicides have been reported. Additionally, supply‑chain disruptions—driven by price fluctuations in precursor chemicals—have caused lead‑time extensions beyond 120 days in some regions, which increases distribution risk and may reduce availability in high‑growth emerging markets.

Emerging formulation technologies—such as micro‑encapsulation, controlled‑release adjuvants and precision‑spray compatible systems—are unlocking new opportunities in the Glufosinate Herbicide Market. Trials indicate micro‑encapsulated glufosinate can deliver up to 20 % improved rain‑fastness and extend the application window from 4 hours to potentially 8 hours. That enables broader crop‑type usage, including in tropical and irrigated systems where unpredictable rainfall has shortened effective application windows. Further, in regions where adoption currently remains below 40 % of arable land, especially in Asia‑Pacific and Latin America, these technological advances create a runway for double‑digit growth and improved farmer‑economics.

The Glufosinate Herbicide Market is challenged by higher production costs, technical complexity and regulatory compliance burdens. The synthesis of glufosinate‑ammonium demands specialized chemical facilities and stringent storage and handling protocols; as a result, production cost premiums of 30‑40 % over comparable herbicides have been noted. Only around 15 commercial‑scale producers globally are currently active, limiting supply flexibility. In certain tropical regions, high humidity and storage conditions (above 65 % relative humidity) degrade product integrity, increasing logistics and distribution cost burdens. Moreover, as herbicide‑resistant biotypes evolve and pressure on regulatory compliance grows, the cost of R&D and stewardship programmes rises, placing additional burden on manufacturers and potentially limiting price competitiveness for farmers.

Accelerated Trait‑Tolerant Crop Integration: Adoption of glufosinate‑tolerant crop systems has increased by ~14 % in 2024 versus the previous year, driven by corn and soybean growers seeking broader weed‑control options beyond glyphosate‑only strategies. This integration is enabling higher recurring herbicide demand tied to the seed‑trait ecosystem.

Shift Towards Low‑Rate Formulations and Precision Application: In 2024, approximately 42 % of new glufosinate formulations launched globally were classified as low‑use‑rate or precision‑spray compatible, representing a 9‑point increase from 2023. Reduced chemical input per hectare is improving sustainability credentials and cost‑efficiency for farmers.

Growth in Developing‑Market Usage: Usage of glufosinate in Asia‑Pacific and Latin America combined grew by over 16 % in 2024, reflecting increased arable acreage adoption, higher labour‑cost pressures and use in diverse crops such as rice, cotton and pulses. These regions now account for a rapidly expanding portion of the global volume base.

Digital‑Spray and Smart‑Agriculture Synergies: Integration of digital application mapping, drone‑guided spray systems and remote‑monitoring platforms with glufosinate programmes became more mainstream in 2024—approximately 28 % of first‑time adopters reported using digital‑spray tools versus 19 % in 2023. This technological shift is raising application precision and reducing off‑target drift by up to 12 %.

The Global Glufosinate Herbicide Market can be meaningfully segmented across product types, applications and end‑user categories, each reflecting distinct decision‑points for manufacturers, distributors and service‑providers. From a type perspective, the market divides into various formulation formats such as liquid concentrates, dry granules and aqueous suspension variants. In terms of applications, the split covers major agricultural uses—such as cereals & grains, oilseeds & pulses, fruits & vegetables—and non‑crop uses such as industrial or commercial weed‐control. On the end‑user side, the primary categories include large‑scale commercial farming operations, cooperatives and smaller neighbouring farms, each with differing adoption dynamics. For example, the cereals & grains application segment accounted for 46 % of global volume in 2024. The formulation type dimension also reflects the balance between liquid and solid formats, with liquid formulations capturing over half the market in recent years. Decision‑makers should assess segmentation not only on share, but on evolving growth characteristics and technology overlays such as precision‑spray integration and trait‑tolerant crop compatibility.

The market types of glufosinate herbicides can broadly be classified into liquid formulations, granules/dry formulations and other niche formats (e.g., aqueous suspension concentrates). The leading type is liquid formulations, commanding approximately 52 % share of the global market in 2024 due to their ready mixing, lower abrasion and suitability for standard spray rigs. For example, a recent dataset reports liquid formulations captured 52 % of revenue in 2024. The fastest‑growing type is the aqueous suspension concentrate and nano‑encapsulated liquid format, driven by new formulation science and sustainability trends—this segment is projected to grow at a double‑digit annual rate (reported at ~10.9 % CAGR for suspension concentrates). Other types, including dry granules, powder blends and water‑dispersible granules, together account for the remaining ~48 % share and are niche in use where storage conditions or spray equipment constraints exist.

Application areas for glufosinate herbicides include crops such as grains & cereals, oilseeds & pulses, fruits & vegetables, along with non‑crop uses (e.g., industrial sites, rail‑sidings). The leading application is grains & cereals, which accounted for approximately 46 % share of global glufosinate usage in 2024. The dominance reflects heavy adoption in commodity crops such as corn, soybean and wheat in major producing regions. The fastest‑growing application is the oilseeds & pulses segment, supported by increasing crop rotations, trait‑tolerant seed launches and resistance‑management programmes—this segment is growing at a reported rate of ~11.6 % annually. Other application areas (fruits & vegetables, non‑crop weed‑control, others) collectively contribute the remaining ~54 % share. In terms of consumer adoption trends, in 2024 more than 38 % of large farming enterprises globally reported switching to glufosinate‑based programmes for glyphosate‑resistant weed zones. Further, over 60 % of ag‑retailers surveyed indicated rising farmer preference for non‑selective herbicides compatible with trait‑engineered crops.

End‑users of glufosinate herbicides span commercial farming enterprises, cooperative/aggregator models and smaller independent farms. The leading end‑user segment is commercial large‑scale farming operations, accounting for roughly 54 % share of usage in 2024 thanks to their ability to invest in trait‑tolerant systems, precision spray equipment and agronomic service bundles. The fastest‑growing end‑user segment is agricultural cooperatives and custom‑spray service providers, driven by rising outsource demand and precision‑spray adoption—growth in this segment is approximately ~12.4 % annually. Other end‑users—including smaller farms and non‑agricultural weed‑control operators—together account for the remaining ~46 % share. In consumer adoption terms, in 2024 around 42 % of ag‑retail cooperatives in the United States reported deploying herbicide‑trait bundles including glufosinate‑ready programs. Also, over 60 % of farmers aged under 40 indicated increased trust in herbicide‑services packaged with digital application platforms.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

Asia-Pacific leads due to high adoption in China, India, and Japan, where large-scale rice, soybean, and cotton cultivation drives demand. China alone contributed over 12,000 tons of production capacity in 2024, with technology-driven adoption such as nano‑encapsulated formulations and precision spraying increasing farm-level efficiency. In contrast, North America’s rapid growth is supported by expanding trait-tolerant crop programs, digital spray mapping integration, and increasing cooperative and commercial farm adoption, with U.S. corn and soybean fields showing more than 70% deployment of glufosinate-based programs.

North America holds approximately 30% of the market share in 2024. Demand is driven by large-scale corn and soybean operations, where herbicide-tolerant crops and integrated weed management practices dominate. Regulatory support, including the approval of post-emergence applications and environmental stewardship programs, encourages adoption. Technological advancements such as drone-guided spraying and digital mapping platforms are widely implemented. Local players, such as BASF U.S., are enhancing production of advanced liquid formulations, while farmers increasingly adopt precision application systems. Enterprise adoption varies regionally, with high uptake in Midwest commercial farms, enabling more than 65% reduction in off-target drift for precision-sprayed plots.

Europe accounted for approximately 22% market share in 2024. Germany, France, and the UK are the top consuming countries. Regulatory bodies enforce strict residue limits and sustainability practices, driving demand for advanced formulations. Emerging technologies such as micro-encapsulated glufosinate and digital spraying are gaining traction. Local companies, including Bayer AG, focus on precision herbicide systems tailored to high-value crops. European farmers emphasize traceability and compliance, resulting in 50% of large-scale cereal and oilseed farms adopting glufosinate programs integrated with digital monitoring.

Asia-Pacific dominates with 38% of global market share, driven primarily by China, India, and Japan. Large-scale rice, cotton, and soybean cultivation, combined with expanding production infrastructure, supports high demand. Innovation hubs focus on nano-encapsulation, precision spraying, and low-use-rate formulations. Local players, such as Zhejiang Wynca Chemical, have ramped up production capacity to over 12,000 tons in 2024. Farmers increasingly adopt advanced application techniques, with 58% of commercial operations integrating glufosinate into rotational weed management, reflecting the regional preference for high-efficiency, technology-enabled solutions.

South America holds 18% market share, led by Brazil and Argentina. Expansion in soybean and corn cultivation, coupled with modernized farm equipment, supports glufosinate demand. Government incentives for sustainable agriculture and import facilitation encourage adoption. Local players, including UPL Limited, are introducing advanced liquid formulations to enhance weed control efficiency. Regional consumer behavior shows high dependence on cooperative and custom-spray services, with 46% of mid-sized farms integrating glufosinate in crop rotations, reflecting localized efficiency priorities.

Middle East & Africa represent approximately 7% of the global market in 2024. Growth is concentrated in the UAE, South Africa, and Egypt, where commercial crop production and construction-related weed control drive demand. Technological modernization, including digital spray platforms and automated dosing, supports efficiency gains. Local companies are expanding formulation facilities, improving storage and handling to match regional climate conditions. Farmers and commercial enterprises increasingly adopt precision spraying, with over 40% of agribusinesses using glufosinate integrated with digital monitoring, reflecting technology-driven regional uptake.

China – 24% Market Share: High production capacity and large-scale crop cultivation support strong adoption.

United States – 18% Market Share: Widespread adoption of herbicide-tolerant crops and advanced precision spraying infrastructure drives market prominence.

The competitive environment within the Glufosinate Herbicide Market is semi‑consolidated, with approximately 30 to 35 active competitors globally, with the top five firms collectively holding around 45‑50% of total market share. Leading players such as BASF SE, Bayer AG, Syngenta AG, UPL Limited and Nufarm Limited dominate through vertically integrated herbicide portfolios, global distribution networks and trait‑enabled crop systems. Strategic initiatives include BASF’s launch of a next‑generation glufosinate product powered by Glu‑L® Technology with enhanced efficacy and lower use rate (announced October 2024) and BASF’s restructuring of its glufosinate‑ammonium production network in Germany (July 2024) to remain cost‑competitive. Innovation trends are evident — firms are investing in nano‑encapsulated glufosinate formulations, precision‑spray compatible delivery systems and digital agronomic platforms to differentiate their offerings. Regional players in China, India and Latin America are also expanding via low‑use‑rate technicals and local formulation capacity, increasing competitive pressure on global players. Overall, while the market backbone is anchored by major agriproduct firms, ample opportunity remains for niche formulators and service‑oriented providers to gain share through technology, trait integration and regional specialization.

UPL Limited

Nufarm Limited

Corteva Agriscience

Arysta LifeScience

Sumitomo Chemical

In the glufosinate herbicide sector, technology adoption is accelerating and is becoming a key differentiator for manufacturers, distributors and end‑users. One core innovation is the shift to L‑glufosinate isomer formulations, which deliver higher target activity and lower environmental load compared to older racemic mixtures; firms report roughly 25‑33% lower use‑rates per hectare for these new formulations. A second major trend is the development of nano‑encapsulated and micro‑emulsion delivery formats, which enhance foliar uptake, improve rain‑fastness and reduce drift—industry trials indicate uptake increases of more than 15‑20% in harsher agronomic environments. Third, precision application systems are increasingly integrated with herbicide deployment: drone‑guided sprayers, variable‑rate technology (VRT) and digital mapping now coordinate with glufosinate programmes to reduce overlap and lower active‑ingredient load by up to 10‑12%, while improving coverage consistency. Additionally, the convergence of seed‑trait platforms and herbicide chemistry is driving the introduction of glufosinate‑tolerant crop systems, which in turn changes timing and dosage patterns and demands compatible formulations. From a supply‑chain viewpoint, global cost pressures (raw materials, energy) are forcing makers to optimize manufacturing networks, transition to contract‑active ingredient sourcing and invest in modular production units closer to major farming regions. For decision‑makers, the implications are clear: technology investments in chemistry, formulation delivery and digital deployment are no longer optional; they are vital for market access, efficiency and differentiation in glufosinate‑based solutions.

In July 2024, BASF announced it will cease production of the active ingredient glufosinate‑ammonium at its Knapsack and Frankfurt (Germany) sites by end of 2024/2025, shifting to third‑party sourcing to maintain competitiveness. Source: www.basf.com

In October 2024, BASF secured U.S. Environmental Protection Agency registration for Liberty ULTRA herbicide, powered by Glu‑L™ Technology, claiming ~20% superior weed control and ~33% greater coverage compared to generic glufosinate products. Source: www.basf.com

In August 2023, BASF announced its plan to launch Liberty® ULTRA, a trait‑enabled glufosinate solution for soybean, cotton, corn, canola, featuring resolved isomer technology that allows ~25% reduction in use‑rate compared to existing glufosinate herbicides. Source: agriculture.basf.us

In May 2024, UPL Limited obtained U.S. regulatory approval for a supplemental label amendment that allows its glufosinate‑based herbicide to be applied over‑the‑top on glufosinate‑tolerant camelina oilseed varieties, expanding crop system applicability. Source: www.upl‑ltd.com

This report covers the global glufosinate herbicide market with comprehensive segmentation across formulation types (liquid concentrates, aqueous suspensions, granules/solids, nano‑encapsulated formats), application areas (cereals & grains, oilseeds & pulses, fruits & vegetables, non‑crop/industrial uses), end‑user categories (large commercial farms, cooperatives/custom‑spray services, smallholders), and regional geographic coverage (North America, Europe, Asia‑Pacific, South America, Middle East & Africa). It also addresses technological themes such as trait‑enabled crops, precision application systems, drift‑reduction adjuvants and digital agronomy tools. The report examines industry focus areas including production capacity, investment in next‑generation formulations, mergers & acquisitions of specialty formulators, supply‑chain restructuring due to raw‑material cost pressures, and regulatory/ESG impacts such as restrictions on legacy herbicides and incentives for reduced‑use‑rate chemistries. Emerging and niche segments are included: bio‑based formulation variants, contract‑manufacturing models, and custom service offerings integrating herbicide programmes with satellite‑monitoring and farm‑management software. The geographic analysis provides volume share data, adoption trends in key markets (e.g., China, USA, Brazil, India), and identifies high‑opportunity corridors. Decision‑makers will benefit from insight on competitive positioning, technology investment priorities, and strategic pathways into differentiated glufosinate‑based value chains.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 260.0 Million |

| Market Revenue (2032) | USD 445.7 Million |

| CAGR (2025–2032) | 6.97% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | BASF SE, Bayer AG, Syngenta AG, UPL Limited, Nufarm Limited, Corteva Agriscience, Arysta LifeScience, Sumitomo Chemical |

| Customization & Pricing | Available on Request (10% Customization is Free) |