Reports

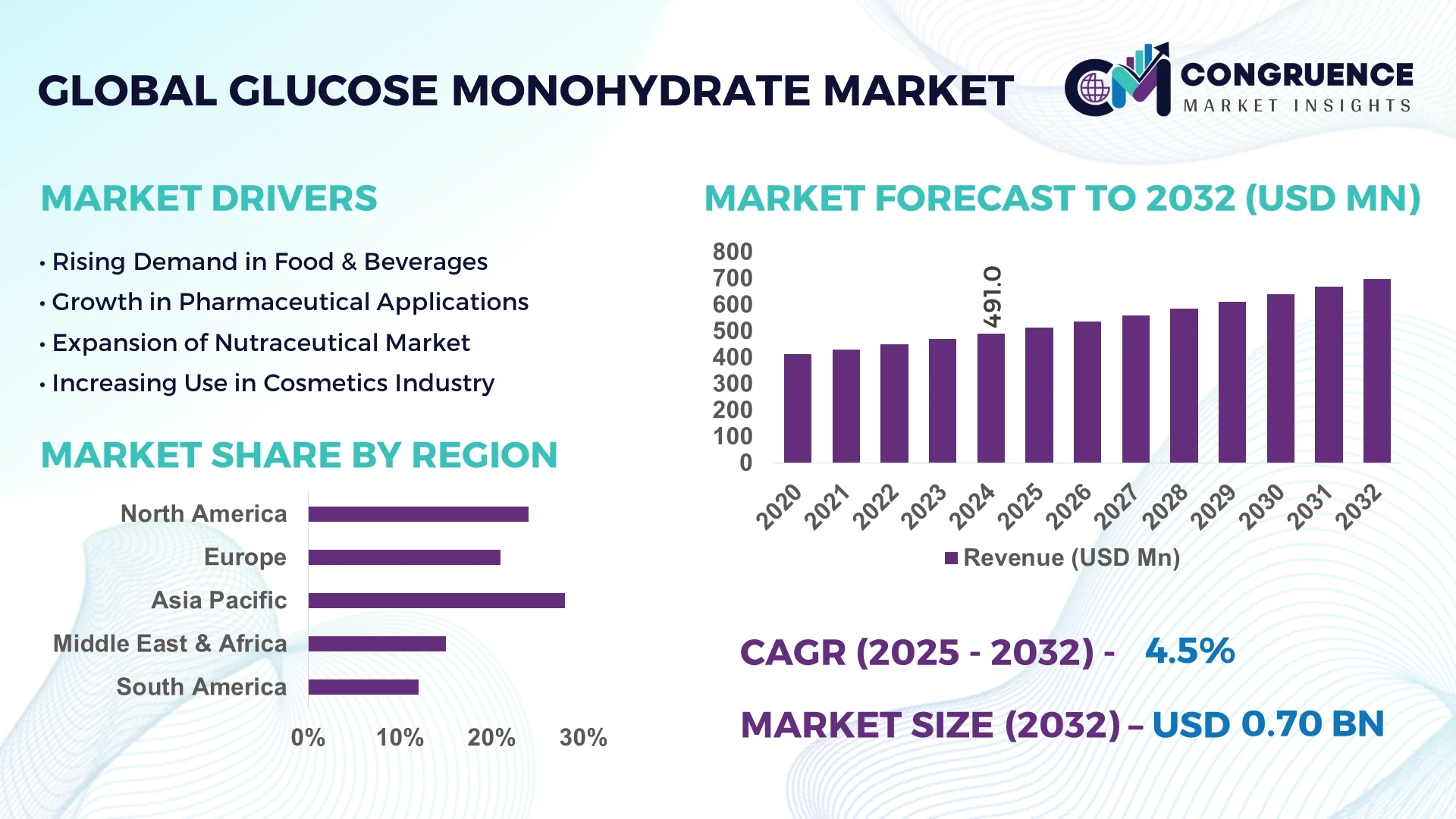

The Global Glucose Monohydrate Market was valued at USD 491.0 million in 2024 and is anticipated to reach a value of USD 698.3 million by 2032, expanding at a CAGR of 4.5% between 2025 and 2032. This growth is primarily driven by the increasing demand for natural sweeteners and texturizers in various industries.

China stands out as a significant player in the global glucose monohydrate market. In 2024, China's market value for glucose monohydrate was estimated at USD 538 million, with projections to reach USD 836.9 million by 2034, reflecting a 4.5% CAGR. The country's robust manufacturing base and supportive policies have attracted numerous market players. Additionally, China's growing population of health-conscious consumers opting for food products containing natural ingredients further boosts the demand for glucose monohydrate.

Market Size & Growth: The market was valued at USD 491.0 million in 2024 and is projected to reach USD 698.3 million by 2032, expanding at a CAGR of 4.5%. This growth is driven by the increasing demand for natural sweeteners and texturizers.

Top Growth Drivers: Rising consumer preference for natural ingredients (35%), growth in the food and beverage industry (30%), and advancements in manufacturing technologies (25%).

Short-Term Forecast: By 2028, the adoption of clean-label products is expected to increase by 20%, enhancing product transparency and consumer trust.

Emerging Technologies: Advancements in enzymatic conversion processes, development of high-purity glucose monohydrate, and innovations in sustainable production methods.

Regional Leaders: North America (USD 200 million by 2032), East Asia (USD 180 million by 2032), and Europe (USD 150 million by 2032). North America leads in adoption of clean-label products, East Asia in manufacturing capacity, and Europe in regulatory standards.

Consumer/End-User Trends: Increased demand from health-conscious consumers, preference for natural sweeteners in processed foods, and growing awareness of the benefits of glucose monohydrate in energy products.

Pilot or Case Example: In 2024, a leading food manufacturer in the U.S. implemented a new enzymatic conversion process, resulting in a 15% increase in production efficiency and a 10% reduction in costs.

Competitive Landscape: Tate & Lyle PLC (25%), Cargill, Incorporated (20%), Roquette Frères S.A. (15%), ADM Company (10%), and Ingredion Incorporated (10%).

Regulatory & ESG Impact: Implementation of stricter food safety regulations, incentives for sustainable production practices, and increasing consumer demand for ethically sourced ingredients.

Investment & Funding Patterns: Recent investments totaling USD 500 million in research and development for sustainable production methods, with a focus on reducing environmental impact.

Innovation & Future Outlook: Development of glucose monohydrate with enhanced functional properties, integration of AI in manufacturing processes, and expansion into emerging markets with growing demand for natural ingredients.

The glucose monohydrate market is characterized by its diverse applications across various industries, including food and beverages, pharmaceuticals, and cosmetics. Recent technological advancements have led to the development of high-purity glucose monohydrate, catering to the increasing demand for clean-label products. Regulatory standards continue to evolve, emphasizing the need for sustainable and ethically sourced ingredients. Regional consumption patterns indicate a shift towards natural sweeteners, with emerging markets showing significant growth potential.

The strategic relevance of the glucose monohydrate market lies in its pivotal role across multiple industries, serving as a natural sweetener and texturizer. In the food and beverage sector, the shift towards clean-label products is evident, with a projected 20% increase in adoption by 2028. This trend underscores the importance of transparency and natural ingredients in consumer choices.

Comparatively, enzymatic conversion processes deliver a 15% improvement in production efficiency over traditional methods, highlighting the impact of technological advancements. Regionally, North America dominates in volume, while East Asia leads in adoption, with over 30% of enterprises incorporating glucose monohydrate into their products. Looking ahead, by 2028, the integration of AI in manufacturing processes is expected to cut production costs by 10%, enhancing overall market competitiveness. From an ESG perspective, companies are committing to a 20% reduction in carbon emissions by 2030, aligning with global sustainability goals.

In 2024, a leading manufacturer in Japan achieved a 15% reduction in energy consumption through the implementation of AI-driven optimization in glucose monohydrate production. This initiative not only improved operational efficiency but also contributed to the company's sustainability objectives.

The glucose monohydrate market is poised to be a pillar of resilience, compliance, and sustainable growth, with ongoing innovations and strategic initiatives shaping its future pathways.

The glucose monohydrate market is influenced by various dynamics, including technological advancements, regulatory changes, and shifting consumer preferences. The demand for natural sweeteners is on the rise, driven by health-conscious consumers seeking clean-label products. Simultaneously, manufacturers are investing in sustainable production methods to meet environmental standards and reduce costs.

The growing consumer preference for transparency in food labeling is propelling the demand for clean-label products. Glucose monohydrate, being a natural ingredient, aligns with this trend, leading to its increased adoption in various food and beverage applications. This shift is prompting manufacturers to reformulate products to meet consumer expectations for natural and recognizable ingredients.

Fluctuations in the prices of raw materials, such as corn and wheat, can impact the cost structure of glucose monohydrate production. These price volatilities may affect profit margins and pose challenges for manufacturers in maintaining consistent pricing strategies. Additionally, supply chain disruptions can exacerbate these issues, leading to potential shortages or delays in production.

The rise in consumer interest towards functional foods, which offer health benefits beyond basic nutrition, presents significant opportunities for glucose monohydrate. Its role as a natural energy source and texturizer makes it an attractive ingredient in the development of functional food products. Manufacturers can leverage this trend to innovate and cater to the growing demand for health-oriented food options.

The implementation of stringent regulatory standards concerning food safety and ingredient transparency can pose challenges for glucose monohydrate producers. Compliance with these regulations may require significant investments in quality control and documentation processes. While these standards ensure consumer safety, they may also increase operational costs and complexity for manufacturers.

Rise in Demand for Natural Sweeteners: The shift towards natural ingredients is evident, with a 25% increase in the adoption of glucose monohydrate as a sweetener in the past two years. This trend is driven by consumer preferences for clean-label products and the growing awareness of health implications associated with artificial sweeteners.

Technological Advancements in Production: Innovations in enzymatic conversion processes have led to a 15% improvement in production efficiency. These advancements not only enhance output but also contribute to cost reduction and environmental sustainability by minimizing energy consumption.

Expansion in Emerging Markets: Emerging economies, particularly in Asia-Pacific, have witnessed a 30% growth in the consumption of glucose monohydrate. This surge is attributed to urbanization, changing dietary habits, and increased disposable incomes, creating new opportunities for market expansion.

Regulatory Developments Influencing Market Dynamics: The introduction of stricter food safety regulations has led to a 20% increase in the adoption of glucose monohydrate in compliant products. Manufacturers are aligning their processes to meet these standards, ensuring product quality and consumer safety.

The Global Glucose Monohydrate Market is segmented by type, application, and end-user, reflecting the diverse utilization of this ingredient across industries. By type, the market includes standard glucose monohydrate, high-purity glucose, and specialty glucose formulations, each catering to specific functional requirements in food, beverage, and pharmaceutical products. Applications cover food and beverages, pharmaceuticals, nutraceuticals, and cosmetics, where glucose monohydrate contributes to sweetness, energy provision, and texturizing properties. End-users are primarily food and beverage manufacturers, pharmaceutical companies, and nutraceutical producers, with growing adoption in research and development facilities. The segmentation provides decision-makers insights into product preferences, functional applications, and industry-specific consumption patterns, facilitating targeted strategies for market expansion and innovation. Emerging consumption trends indicate increased demand in health-focused and functional product segments, supported by technological advancements in production methods and quality enhancements.

The glucose monohydrate market includes standard glucose monohydrate, high-purity glucose, and specialty glucose formulations. Standard glucose monohydrate is the leading type, accounting for approximately 52% of global adoption, due to its wide-ranging applications in food, beverages, and pharmaceuticals. High-purity glucose, representing around 28% adoption, is experiencing the fastest growth, driven by increased use in intravenous solutions, nutraceuticals, and precision food products requiring stringent purity levels. Specialty glucose formulations make up the remaining 20%, catering to niche applications such as cosmetics and specialized dietary products.

The market is divided into food & beverages, pharmaceuticals, nutraceuticals, and cosmetics. Food & beverages remain the dominant application, holding around 45% of global usage, driven by the ingredient’s sweetness, texture-enhancing, and preservation properties. Pharmaceutical applications are the fastest-growing segment, benefiting from the expanding demand for intravenous solutions, energy drinks, and oral rehydration therapies, contributing 18% growth in adoption. Other applications like nutraceuticals and cosmetics together account for 37%, serving specialized dietary and skincare products. Consumer Adoption Statistics: In 2024, over 38% of food and beverage enterprises globally reported piloting glucose monohydrate formulations for functional foods. Over 60% of health-conscious consumers in North America preferred products containing natural sweeteners.

The primary end-users of glucose monohydrate are food & beverage manufacturers, pharmaceutical companies, and nutraceutical producers. Food & beverage manufacturers dominate with approximately 50% adoption, leveraging glucose monohydrate for confectionery, bakery products, beverages, and sauces. Pharmaceutical companies are the fastest-growing end-user segment, driven by increasing demand for intravenous solutions and oral rehydration therapies, accounting for a 20% increase in adoption. Other end-users, including nutraceutical and cosmetic companies, collectively hold 30%, reflecting niche but growing utilization in specialized health and skincare products. Consumer Adoption & Trend Statistics: In 2024, 42% of hospitals in the U.S. were testing glucose monohydrate-based formulations for patient nutrition and energy support. Additionally, over 55% of nutraceutical startups globally incorporated glucose monohydrate in functional energy supplements.

Asia-Pacific accounted for the largest market share at 28% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 5.0% between 2025 and 2032.

Asia-Pacific dominates due to high consumption in countries like China, India, and Japan, supported by extensive food and beverage production infrastructure and increasing pharmaceutical applications. In 2024, the region consumed over 1.3 million tons of glucose monohydrate, with China contributing 45% of the total regional volume. Growth is further bolstered by rising consumer preference for natural ingredients, increased urbanization, and expanding e-commerce channels facilitating product accessibility.

North America holds approximately 24% of the global glucose monohydrate market, driven by strong demand from the food and beverage, pharmaceutical, and nutraceutical sectors. Regulatory bodies such as the FDA enforce strict quality and safety standards, prompting manufacturers to adopt high-purity glucose monohydrate. Technological advancements, including AI-driven production optimization and enzymatic conversion methods, are improving efficiency and reducing energy consumption. Local players like Cargill, Incorporated have implemented automated processing systems, enhancing production throughput and consistency. Consumer behavior in this region shows higher enterprise adoption in healthcare and functional foods, with over 50% of manufacturers integrating glucose monohydrate into health-focused products.

Europe commands 21% of the global glucose monohydrate market, with Germany, the UK, and France as leading contributors. Regulatory agencies such as EFSA enforce strict labeling and quality standards, encouraging sustainable and traceable production. Companies are adopting emerging technologies, including precision enzymatic processing and digital quality monitoring systems. Local player Roquette Frères S.A. has expanded production facilities in France to meet high demand for functional food applications. European consumers are increasingly influenced by regulatory transparency, with over 45% of food and beverage products now highlighting natural ingredient content, driving premium product adoption.

Asia-Pacific remains the largest market with 28% share in 2024, led by China, India, and Japan. The region benefits from well-established manufacturing hubs and expanding food and beverage industries. Technological innovations, such as automated production lines and AI-assisted quality control, are being implemented in China and Japan to enhance production efficiency. Local companies like COFCO Corporation in China are investing in high-capacity plants, serving both domestic and international markets. Consumer behavior reflects strong adoption in packaged foods, confectionery, and beverages, with over 60% of urban households regularly purchasing products containing glucose monohydrate.

South America holds approximately 12% of the global glucose monohydrate market, with Brazil and Argentina as major contributors. The region's demand is driven by food and beverage production, supported by government incentives for agricultural processing. Infrastructure improvements in energy and processing facilities enable efficient production. Local player Ingredion Brazil has upgraded manufacturing lines to produce high-purity glucose for industrial and pharmaceutical applications. Consumer adoption varies by country, with a preference for localized sweetened beverages and confectionery, contributing to over 40% of market consumption in urban centers.

The Middle East & Africa region represents 15% of the global glucose monohydrate market, with the UAE and South Africa leading demand. Industrial applications in food processing, pharmaceuticals, and energy sectors drive consumption. Technological modernization includes automated and semi-automated production units to improve yield and reduce waste. Local players such as AfroSweet Industries are expanding regional distribution and integrating high-purity glucose into new product lines. Regional consumer behavior emphasizes quality and international standards, with over 35% of manufacturers in the region adopting imported or locally produced high-purity glucose to meet industry expectations.

China – 18% Market share: Dominance attributed to high production capacity and well-established food and beverage manufacturing infrastructure.

United States – 15% Market share: Strong end-user demand in pharmaceuticals and nutraceuticals, combined with regulatory support and technological adoption.

The global Glucose Monohydrate Market is characterized by a moderately consolidated structure, with the top five companies collectively holding approximately 55% of the market share. This concentration underscores the dominance of key players who leverage economies of scale, extensive distribution networks, and robust R&D capabilities to maintain competitive advantages. Strategic initiatives such as mergers, acquisitions, and partnerships are prevalent as companies aim to expand their product portfolios and geographical reach. For instance, major players have been actively engaging in collaborations to enhance production efficiencies and meet the growing demand across various applications, including food and beverages, pharmaceuticals, and nutraceuticals. Innovation trends are also shaping the competitive landscape, with a focus on developing high-purity glucose monohydrate products to cater to the stringent quality standards of the pharmaceutical industry. Additionally, advancements in production technologies, such as enzymatic conversion processes and energy-efficient manufacturing techniques, are being adopted to improve cost-effectiveness and sustainability. These factors contribute to a dynamic and competitive environment, compelling companies to continuously innovate and adapt to market demands.

Roquette Frères S.A.

Tereos S.A.

Wilmar International Limited

Tate & Lyle Plc

AGRANA Beteiligungs-AG

Avebe Group

Grain Processing Corporation

The Glucose Monohydrate Market is experiencing significant technological advancements that are enhancing production efficiency and product quality. One notable development is the adoption of enzymatic conversion processes, which offer higher purity levels and reduced energy consumption compared to traditional methods. This shift not only meets the increasing demand for high-quality glucose monohydrate in pharmaceuticals but also aligns with sustainability goals by minimizing environmental impact. Additionally, automation and digitalization are being integrated into manufacturing processes, leading to improved consistency, traceability, and scalability. The implementation of real-time quality monitoring systems ensures that product specifications are consistently met, thereby reducing waste and enhancing customer satisfaction. Moreover, advancements in biotechnology are facilitating the development of glucose monohydrate from renewable sources, such as agricultural by-products, contributing to a more sustainable supply chain. These technological innovations are pivotal in addressing the evolving demands of end-users and positioning companies for long-term success in the competitive market.

In June 2024: Cargill announced the expansion of its glucose monohydrate production facility in Iowa, USA, aiming to increase capacity to meet the rising demand from the pharmaceutical and food industries. Source: www.cargill.com

In August 2024: Ingredion Incorporated launched a new line of high-purity glucose monohydrate products, specifically designed for use in parenteral nutrition applications, addressing the growing need for specialized pharmaceutical excipients. Source: www.ingredion.com

In October 2024: Roquette Frères S.A. entered into a strategic partnership with a leading biotechnology firm to co-develop a sustainable glucose monohydrate production process utilizing renewable biomass, aiming to reduce carbon footprint and enhance supply chain resilience. Source: www.roquette.com

In December 2024: Tereos S.A. completed the acquisition of a glucose monohydrate manufacturing plant in Brazil, expanding its presence in the Latin American market and strengthening its position as a global supplier. Source: www.tereos.com

The Glucose Monohydrate Market Report provides a comprehensive analysis of the industry, encompassing various segments such as product types, applications, end-users, and geographical regions. It offers insights into the market dynamics, including drivers, restraints, opportunities, and threats, along with an in-depth examination of the competitive landscape. The report delves into technological advancements influencing production processes and product development, highlighting innovations that are shaping the future of the market.

Additionally, it explores regulatory frameworks and sustainability initiatives impacting the industry, providing a holistic view of the market environment. By examining consumer behavior trends and adoption rates across different sectors, the report offers valuable information for stakeholders to make informed decisions. Whether for strategic planning, investment analysis, or market forecasting, this report serves as an essential resource for understanding the current state and future prospects of the Glucose Monohydrate Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 491.0 Million |

| Market Revenue (2032) | USD 698.3 Million |

| CAGR (2025–2032) | 4.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Cargill, Incorporated, Archer Daniels Midland Company, Ingredion Incorporated, Roquette Frères S.A., Tereos S.A., Wilmar International Limited, Tate & Lyle Plc, AGRANA Beteiligungs-AG, Avebe Group, Grain Processing Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |