Reports

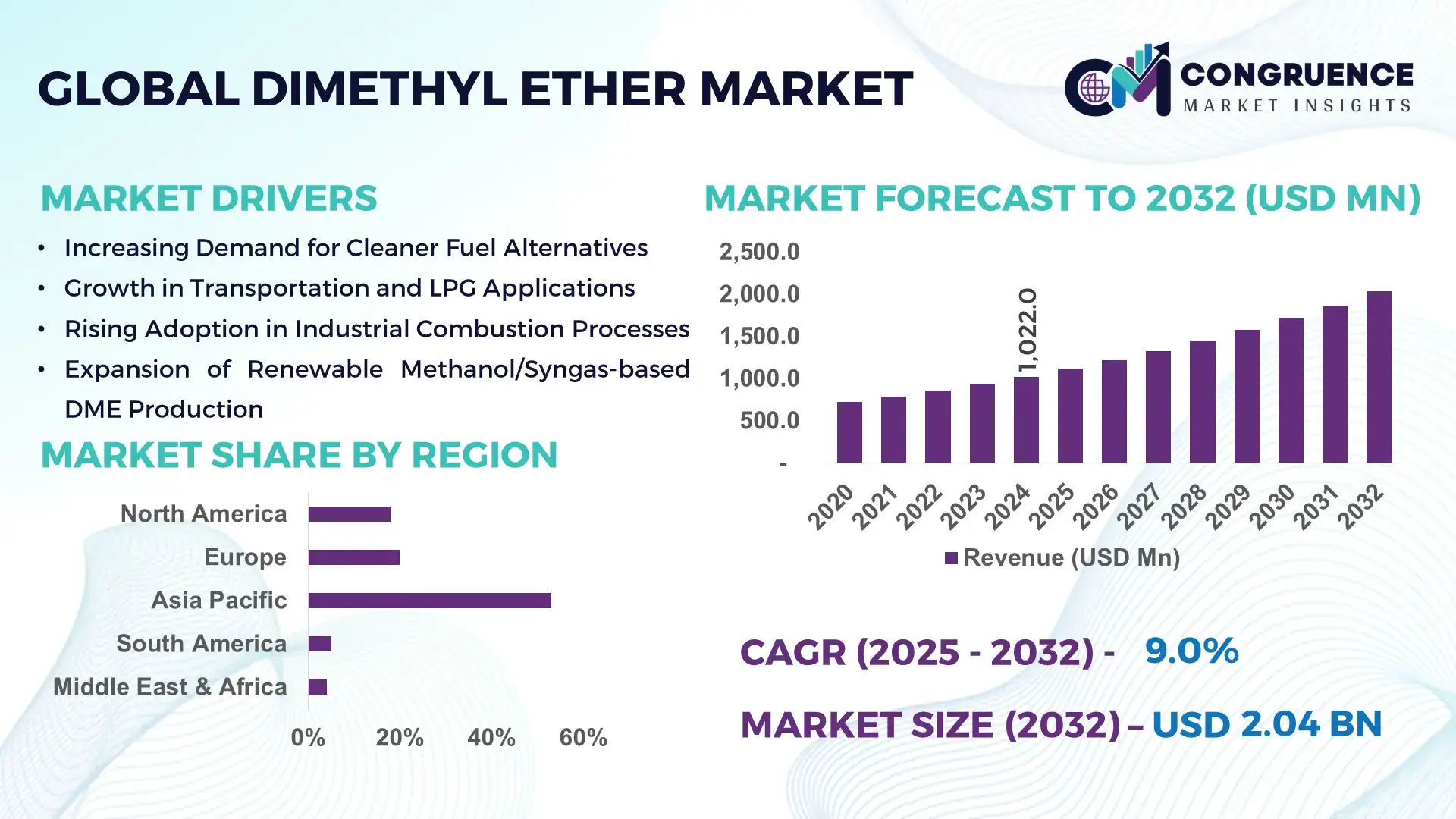

The Global Dimethyl Ether Market was valued at USD 1,022.0 Million in 2024 and is anticipated to reach USD 2,036.4 Million by 2032, expanding at a CAGR of 9.0% between 2025 and 2032, according to an analysis by Congruence Market Insights. Growth is primarily fueled by rising adoption of cleaner-burning fuel substitutes across industrial and commercial applications.

China continues to play a central role in shaping the global Dimethyl Ether landscape due to its exceptionally large production capacity, exceeding 4.5 million tons annually, backed by substantial national investments into coal-to-chemical infrastructure exceeding USD 12 billion over the past decade. The country has integrated DME into emerging energy-transition frameworks, utilizing it in domestic LPG blending, industrial combustion systems, and pilot renewable DME projects. Advanced catalytic technologies, supported by more than 30 operational high-efficiency DME plants, are enabling higher conversion rates and improved product quality, establishing China as a technical and industrial backbone of global DME development.

Market Size & Growth: Valued at USD 1,022.0 Million in 2024 and projected to reach USD 2,036.4 Million by 2032 at a CAGR of 9.0%, driven primarily by increasing preference for clean-burning fuels and rapid expansion of alternative energy applications.

Top Growth Drivers: Industrial fuel substitution (up to 32% adoption), efficiency improvements in DME-based combustion systems (17%), and expanding use in LPG blending (24% adoption across emerging economies).

Short-Term Forecast: By 2028, process optimization technologies are projected to reduce DME production costs by nearly 14% while improving catalytic conversion efficiency by 11%.

Emerging Technologies: Bio-DME synthesis, CO₂-to-DME catalytic pathways, and high-selectivity dehydration reactors are enabling cleaner, scalable fuel alternatives with measurable efficiency gains.

Regional Leaders: Asia-Pacific expected to reach USD 1,348 Million by 2032 with strong industrial adoption; Europe projected at USD 342 Million with rising clean-fuel standards; North America estimated at USD 201 Million driven by renewable fuel integration.

Consumer/End-User Trends: Strong uptake across LPG distributors, automotive users adopting DME-compatible engines, and industrial operators shifting from conventional fuels to cost-efficient DME blends.

Pilot or Case Example: In 2026, a large-scale bio-DME pilot in Japan achieved a 22% reduction in carbon intensity across transport fuels through advanced catalytic conversion.

Competitive Landscape: The market leader holds approximately 18% share, followed by 3–5 prominent players specializing in coal-based, natural-gas-based, and renewable DME technologies.

Regulatory & ESG Impact: Governments are accelerating adoption with clean-fuel incentives and emissions standards requiring up to 35% lifecycle carbon reduction by 2030.

Investment & Funding Patterns: Recent investment exceeded USD 1.1 Billion, with increasing project financing in CO₂-derived DME and renewable energy-linked production.

Innovation & Future Outlook: Advancements in low-carbon feedstock utilization, emerging DME engine platforms, and circular-carbon pathways will shape the next decade of market development.

The Dimethyl Ether Market continues to advance through innovation in catalytic systems, broader industrial adoption, improved combustion efficiency, and supportive environmental regulations, with growing interest in renewable and bio-based DME technologies accelerating long-term progress.

The Dimethyl Ether Market holds significant strategic importance as economies transition toward low-carbon energy systems. Its clean combustion profile, adaptability across industrial, residential, and transportation sectors, and compatibility with circular-carbon technologies strengthen its long-term relevance. Modern DME synthesis technologies enable more efficient production, where next-generation catalytic systems deliver 18% improvement compared to earlier dehydration standards. This technological advantage accelerates industry interest in scalable and economically viable DME pathways.

Regional dynamics reinforce this strategic positioning. Asia-Pacific dominates in volume, supported by large feedstock availability and production infrastructure, while Europe leads in adoption, with over 41% of enterprises integrating DME-based blends into clean fuel frameworks. These adoption disparities reflect policy differences, industrial needs, and transition agendas across regions. Short-term projections indicate that by 2027, AI-enabled plant automation and real-time process control are expected to improve plant efficiency by 16%, reducing downtime and feedstock losses across DME facilities.

Compliance-driven transformations are accelerating investment. Firms are committing to ESG improvements such as 30% lifecycle emission reductions by 2030, supported by regulatory mandates and carbon-intensity performance benchmarks. These commitments enhance DME’s strategic viability as a clean-fuel alternative in both emerging and advanced markets. In 2026, a large-scale Chinese energy company achieved 21% efficiency improvement through digital plant optimization, showcasing the measurable potential of technology-driven pathways.

Collectively, these indicators position the Dimethyl Ether Market as a pillar of resilience, compliance, and sustainable growth, well-aligned with global decarbonization strategies and long-term industrial modernization efforts.

The Dimethyl Ether Market is shaped by evolving energy policies, technological advancements in chemical synthesis, and rising adoption of clean-burning fuel alternatives. Demand is influenced by its role as a substitute for traditional fuels across industrial combustion, transportation, and LPG blending applications. Growing interest in renewable energy production is further promoting pathways for bio-DME and CO₂-to-DME technologies, fostering new investments. Advancements in catalytic dehydration and process integration are improving energy efficiency and operational performance. Regional consumption is expanding as industries seek cost-effective, lower-emission fuels, while infrastructure development and feedstock availability continue to define competitive landscapes.

Growing emphasis on cleaner energy sources is significantly influencing the expansion of the Dimethyl Ether Market. DME’s ultra-clean combustion characteristics—virtually eliminating particulate emissions and reducing NOₓ levels by up to 25%—make it an attractive replacement for diesel and other conventional fuels. Industries are increasingly adopting DME for industrial heating and power-generation applications due to its high cetane number and stable performance. In transportation, pilot programs for DME-powered engines demonstrate operational efficiency improvements of 8–12%, reinforcing DME's suitability for low-emission mobility solutions. Additionally, LPG distributors in emerging economies are incorporating DME blends at rates exceeding 20%, driven by lower toxicity and improved burning efficiency. This broadening application spectrum, combined with policy measures supporting clean-fuel adoption, continues to accelerate DME market penetration.

Infrastructure constraints remain a key limitation in the expansion of the Dimethyl Ether Market. DME requires dedicated storage, transport, and blending systems due to its distinct physical properties, limiting compatibility with existing fuel infrastructure. Many regions lack specialized distribution networks, increasing capital requirements for new installations. Industrial users face additional challenges in retrofitting combustion systems for DME compatibility, often involving equipment modifications and technical upgrades that elevate operational costs. Feedstock availability also varies significantly, with limited access to methanol and syngas supply chains in certain geographies, impacting production continuity. Moreover, regulatory complexities associated with classifying and transporting DME add compliance costs that further hinder adoption. These limitations collectively contribute to slower expansion in regions with underdeveloped energy infrastructure.

Increasing focus on renewable energy production presents a substantial opportunity for the Dimethyl Ether Market. Emerging pathways such as bio-DME production from biomass, agricultural residues, and waste-derived feedstocks offer significant environmental advantages. CO₂-to-DME catalytic conversion technologies show promising efficiencies, enabling carbon circularity and reducing lifecycle emissions by up to 45%. These innovations align with global decarbonization policies, promoting investment in low-carbon fuels. Government incentives supporting renewable fuel development are encouraging companies to establish pilot-scale and commercial facilities utilizing green methanol and syngas. Additionally, the rising demand for sustainable transportation fuels is creating new avenues for DME adoption in heavy-duty vehicles and maritime applications. As renewable feedstock availability expands and technology costs decline, the market is well-positioned to benefit from emerging green energy pathways.

Regulatory compliance obligations and feedstock price volatility pose significant challenges for the Dimethyl Ether Market. Producers must adhere to stringent safety, environmental, and transportation standards governing DME, which increase operational and certification costs. Variations in methanol and syngas prices—driven by global energy market fluctuations—impact production economics, causing uncertainties for manufacturers. Moreover, regional disparities in emissions policies complicate cross-border distribution and adoption strategies. Companies operating in regions with high compliance burdens face additional costs for emissions monitoring and low-carbon certification. Technical challenges associated with scaling new catalytic systems and integrating renewable feedstocks further add to operational complexity. These combined factors create a challenging environment for both new entrants and existing producers, slowing broader market expansion.

Acceleration of Renewable DME Production Technologies: The shift toward low-carbon energy is stimulating investments in renewable DME pathways, including biomass and CO₂-derived production. Pilot plants in Asia and Europe achieved efficiency gains of 14–18%, with emission reductions exceeding 30%. Over 20 new renewable DME facilities are under planning or construction globally, signaling a significant shift toward sustainable fuel synthesis.

Rapid Expansion of DME Blending in LPG Applications: Adoption of DME–LPG blends is accelerating, with blending ratios rising to 20–25% across major emerging economies. Regulators in multiple regions are targeting reductions of up to 28% in carbon emissions from residential and commercial LPG applications, stimulating demand for DME-enhanced fuel distribution. These transitions are driving new investments in blending infrastructure and storage systems.

Advancements in Engine and Combustion Technologies: Engine manufacturers are introducing DME-compatible platforms capable of achieving 10–12% higher thermal efficiency while reducing particulate emissions by nearly 100%. Over 15 commercial pilot trials since 2025 demonstrate strong potential for DME adoption in heavy-duty transport, particularly in fleets requiring low-emission fuel alternatives. This trend is accelerating OEM interest in DME-based fuel systems.

Growth of Digitalized and Automated Production Processes: Automation technologies are transforming DME production, with AI-enabled plant control systems delivering 16% reduction in operational downtime and 11% improvement in energy utilization. More than 40% of new DME facilities planned for 2026–2028 include integrated digital monitoring platforms, supporting predictive maintenance, process optimization, and enhanced catalytic performance.

The segmentation of the Dimethyl Ether Market reflects a structured distribution across types, applications, and end-user categories, each shaped by evolving energy demands and clean-fuel adoption patterns. Type-based segmentation highlights the differing roles of fossil-based, bio-based, and synthetic production routes, each offering distinct benefits related to feedstock availability and emission performance. Application segmentation underscores the growing shift toward cleaner combustion solutions, LPG blending practices, and industrial heating systems, supported by measurable improvements in burning efficiency and reduced pollutant output. End-user segmentation shows diverse uptake across residential consumers, industrial operators, transportation fleets, and commercial establishments, all seeking alternatives to traditional fuels amid tightening environmental regulations. Collectively, these segments reveal a market transitioning steadily toward cleaner, more efficient fuel pathways, with emerging technologies widening the scope of future demand.

Type-wise, the Dimethyl Ether Market includes fossil-based DME, bio-DME, and synthetic DME derived from CO₂ or renewable feedstocks. Among these, fossil-based DME currently leads the market with approximately 63% share, driven by established production infrastructure, abundant coal and natural gas feedstock availability, and mature catalytic dehydration technologies. Bio-DME, while presently accounting for a smaller share, represents the fastest-growing type with an estimated growth rate of about 11%, supported by rising investments in low-carbon fuel production, improved biomass-to-DME conversion efficiencies, and strong policy incentives promoting renewable fuels. Synthetic CO₂-derived DME and power-to-DME variants hold a combined 12% share, serving niche markets focused on circular-carbon applications and advanced pilot projects in Europe and East Asia. Broader industry movement toward decarbonization continues to enhance the relevance of emerging DME types. For instance, recent pilot demonstrations achieved over 40% reduction in lifecycle emissions by integrating carbon capture with methanol-to-DME pathways, illustrating the role of newer DME types in long-term sustainability transitions.

DME serves several critical applications, including LPG blending, aerosol propellants, industrial fuel, transportation fuel, and chemical intermediates. LPG blending leads the market with approximately 47% share, driven by the need to reduce carbon intensity in residential and commercial LPG usage. Industrial fuel applications follow with 28% adoption, while aerosol propellants account for 17%, supported by DME’s non-toxic profile and superior vapor pressure characteristics. However, transportation fuel applications are expanding the fastest with a growth rate of about 10%, driven by increased testing of DME-compatible engines and the need for cleaner diesel alternatives. Chemical intermediate applications and other specialized uses hold a combined 8% share, serving targeted industrial processes requiring specific purity and reactivity characteristics. Consumer adoption trends also support market expansion. In 2024, more than 39% of industrial enterprises globally reported adopting cleaner fuel substitutes in high-temperature operations, demonstrating a clear shift in energy management strategies. Additionally, 52% of LPG distributors in emerging economies reported integrating alternative blends to meet evolving emissions standards.

End-user segmentation in the Dimethyl Ether Market spans residential consumers, industrial users, commercial establishments, and transportation fleets. Residential and commercial LPG users represent the largest end-user segment with approximately 49% share, supported by increasing use of DME-blended LPG for cooking, heating, and small-scale energy applications. Industrial end-users account for 33% adoption, relying on DME for combustion systems, material processing, and applications requiring clean, soot-free burning. Transportation fleets, though currently at 10% share, are the fastest-growing segment with an estimated growth rate of 12%, driven by expanding pilot programs for DME-powered trucks and logistic networks under pressure to reduce particulate and NOₓ emissions. Remaining end-users, including chemical producers and energy-tech developers, contribute a combined 8% and reinforce innovation and diversification within the market. Broader adoption trends indicate rising acceptance of cleaner fuel alternatives. In 2024, over 41% of logistics companies globally reported evaluating low-emission fuel options for fleet modernization, signaling strong potential for DME integration. Similarly, 36% of manufacturing facilities in Asia adopted hybrid fuel systems incorporating DME to reduce operational emissions.

Asia Pacific accounted for the largest market share at 53% in 2024; also it is expected to register the fastest growth, expanding at a CAGR of 10% between 2025 and 2032.

The region maintains a dominant position due to extensive manufacturing capacity, strong LPG substitution programs, and the rapid expansion of chemical and fuel-blending applications. China, India, and Japan collectively contribute more than 70% of regional consumption, supported by increasing deployment of clean fuel initiatives and rising industrial output. Meanwhile, accelerated adoption in transportation fuels, aerosol propellants, and hybrid energy systems is expected to drive faster growth through 2032, particularly as governments push alternative fuel standards and large-scale petrochemical projects expand across emerging Asian economies.

North America held approximately 18% of the global dimethyl ether market in 2024, supported by strong demand from the automotive, power generation, and chemical processing industries. Growth is influenced by rising interest in low-emission fuel substitutes and the expansion of bio-based DME production from waste, agricultural residue, and renewable methanol. Government support for clean energy pathways, including updated emissions standards and tax credits for alternative fuels, is strengthening adoption across the U.S. and Canada. The region is also experiencing increased digital transformation in fuel blending systems and industrial combustion technologies. A notable example includes a U.S.-based energy company advancing pilot-scale DME integration in diesel engine retrofits. Consumer behavior in North America shows higher enterprise adoption in sectors such as healthcare and finance, reflecting a broader shift toward low-carbon operational models.

Europe represented nearly 20% of global dimethyl ether demand in 2024, driven by leading markets such as Germany, the U.K., France, and the Netherlands. Strong emphasis on decarbonization policies, circular economy targets, and clean energy mandates supports consistent adoption across industrial and transportation applications. Regulatory bodies in Europe are accelerating sustainability frameworks that encourage the replacement of high-emission fuels with low-carbon alternatives such as DME. The region is witnessing faster adoption of emerging technologies, including renewable methanol-derived DME and advanced combustion systems. A major European fuel producer has begun enhancing DME–LPG blending capabilities to reduce emissions in commercial heating applications. Consumer behavior is shaped largely by regulatory pressure, which increases demand for transparent and environmentally compliant solutions.

Asia Pacific remains the largest and fastest-growing regional market, driven by increasing production volumes, large consumer bases, and continuous infrastructure expansion. China retains over 60% of regional DME consumption, supported by extensive coal-to-chemical facilities and strong LPG replacement activity. India and Japan contribute significantly owing to growing investments in petrochemicals, transportation fuels, and renewable alternatives. The region benefits from advanced manufacturing ecosystems, low-cost raw materials, and expanding industrial clusters. A major Chinese producer has recently expanded DME capacity to support hybrid fuel applications in both urban and semi-urban areas. Consumer behavior trends show rapid adoption fueled by e-commerce growth and mobile platforms, as digital integration accelerates industrial procurement and distribution.

South America accounted for nearly 5% of global DME demand in 2024, led primarily by Brazil, Argentina, and Chile. Growth is supported by rising industrial activity, expanding automotive fuel diversification programs, and the modernization of energy infrastructure. Governments in the region are offering incentives for clean fuel imports and local production, enhancing industrial adoption of DME for combustion, transportation, and aerosol applications. A notable local example includes a Brazilian chemical distributor integrating DME into its specialty gas portfolio for industrial clients. Consumer behavior leans toward increased demand for media localization, industrial digitalization, and language-adapted solutions, indirectly supporting technology-driven end-user verticals that benefit from DME-related applications.

The Middle East & Africa captured close to 4% of global DME consumption in 2024, backed by strong activity in oil & gas, construction, and heavy industries. The UAE, Saudi Arabia, and South Africa lead the region’s adoption, supported by increasing interest in fuel diversification and chemical feedstock alternatives. Infrastructure modernization, petrochemical expansions, and new refinery integration projects are driving higher DME utilization. A regional energy firm has begun exploring DME–diesel blending to support reduced-emission industrial operations. Consumer behavior shows rising interest in hybrid fuel solutions aligned with national sustainability initiatives and industrial energy transition strategies.

China – 42% Market Share: Dominance driven by large-scale production capacity, extensive coal-to-DME infrastructure, and strong domestic consumption.

India – 11% Market Share: Growth supported by rapid industrial expansion, clean fuel mandates, and increasing demand across transportation and chemical sectors.

The global Dimethyl Ether (DME) market is moderately consolidated, with a core group of around 10–15 major active competitors globally shaping more than half of the industry’s output and direction. The top 5 companies together command approximately 56–62% combined share of global DME production and distribution. Key market players have established diversified strategies — including expansion of production capacity, transition toward renewable or bio-based DME, strategic partnerships, and investment in advanced synthesis technologies — to differentiate themselves and address evolving demand for cleaner fuels.

Strategic initiatives in 2023–2024 highlight the competitive intensity: some firms expanded renewable-DME output by over 30%, while others launched improved catalyst platforms to boost conversion efficiency and reduce emissions. New product formats — such as high-purity aerosol-grade DME and low-carbon fuel variants — are being introduced to capture niche markets in aerosol propellants, LPG blending, and transportation fuel segments. Several companies are forming cross-region alliances with chemical, automotive, and energy firms to accelerate adoption and distribution globally.

Innovation trends — including developments in CO₂-to-DME synthesis, catalytic distillation, renewable methanol feedstocks, and improved process automation — are reshaping competition, pushing firms to invest in R&D and differentiate through sustainability credentials. Overall, the DME market reflects a competitive yet dynamic environment where economic scale, feedstock flexibility, technological sophistication, and regulatory compliance determine leadership.

Royal Dutch Shell plc

Mitsubishi Corporation

Korea Gas Corporation

Akzo Nobel N.V.

Lummus Technology

Dimeta

DCC Energy

The technological evolution of the Dimethyl Ether Market is currently driven by advances in both production and application technologies. On the production side, firms increasingly adopt renewable-feedstock pathways, such as converting biomethanol, biogas, or CO₂-derived syngas into DME, enabling more sustainable and lower-carbon fuel alternatives. Innovative catalytic conversion technologies — including catalytic distillation and optimized methanol-to-DME dehydration catalysts — are improving conversion yield and energy efficiency, reducing waste and lowering emissions associated with traditional coal or natural-gas based DME production.

Parallel to feedstock diversification, there is growing integration of digital automation and process control systems in DME plants. Advanced process monitoring and control enable tighter regulation of reaction parameters, reducing energy consumption and increasing output consistency. Some producers are piloting modular, scalable micro-reactor units for decentralized DME production, supporting faster deployment in distributed industrial or remote settings.

On the application front, new combustion engine and fuel-blending technologies optimized for DME are being developed. Engine manufacturers are adapting combustion chambers and fuel delivery systems to maximize DME’s high cetane number and cleaner burn profile, enabling reductions in particulate and NOₓ emissions compared to traditional diesel. In aerosol propellants and chemical feedstock applications, high-purity DME grades — enabled by refined distillation and purification technologies — are expanding the range of safe, low-VOC products.

Overall, the technology trajectory for DME is pointing toward sustainable feedstock conversion, process intensification, digital automation, and application-specific adaptations — positioning DME as a competitive clean-fuel and industrial-feedstock solution in a decarbonizing energy landscape.

29 Mar 2023 — DCC Energy & Oberon Fuels: partnership to deploy renewable DME production in Europe. DCC Energy signed an offtake and partnership agreement with Oberon Fuels to advance the design, construction and operation of multiple renewable-DME production plants in Europe; DCC committed to offtake volumes once plants are operational and to retail renewable DME to its LPG customers. Source: www.dcc.ie

25 Jul 2023 — Dimeta (SHV Energy JV) & Enerkem: collaboration on large-scale waste-to-DME projects. Dimeta and Enerkem announced feasibility studies and collaboration to develop large-scale renewable and recycled-carbon DME projects in Europe and the U.S., aiming to convert mixed residual waste into renewable methanol/DME and target collective annual production capacity in the low-hundreds of kilotonnes. Source: www.enerkem.com

30 May 2024 — Lummus Technology: commercial launch of renewable-DME production technology (CDDME). Lummus publicly launched a commercially available renewable-DME technology that processes various methanol feedstocks (including low-carbon and renewable methanol) using catalytic-distillation approaches, marketed to lower CAPEX/OPEX and enable flexible feedstock use for renewable DME production. Source: www.lummustechnology.com

2024 (Jul–Sep 2024 notices) — GRILLO (GRILLO-Werke AG): product & site updates for GRILLO-one DME. GRILLO published corporate updates showing REDcert² biomass-balanced certification activity for its DME product “GRILLO-one” (noting improved sustainability credentials), announced product positioning as a high-purity aerosol DME grade, and updated site status notices related to production site repairs/force-majeure resolutions. These are published on GRILLO’s company news pages and sustainability report. Source: www.grillo.de

This Dimethyl Ether Market Report covers a broad scope across multiple dimensions: it segments the market by raw material type (fossil-based, bio-based, natural gas–derived, renewable methanol/syngas-based), application area (LPG blending, aerosol propellants, transportation fuel, industrial combustion, chemical feedstock, others), and end-user segments including residential LPG users, industrial operations, transportation fleets, and commercial applications. The geographic scope spans North America, Europe, Asia-Pacific, Latin America (South America), and Middle East & Africa, capturing both established and emerging markets globally.

Technological focus areas include conventional coal and natural-gas based DME synthesis, bio-DME using biomass or biogas, CO₂-to-DME / renewable-methanol-to-DME conversion pathways, and advanced catalytic and distillation technologies. The report also analyses application-specific technological adaptations, such as engine retrofits for DME fuel, LPG-DME blending systems, aerosol-grade purification processes, and modular production units for decentralized deployment.

In addition, the report assesses industry dynamics including competitive positioning, strategic investments, partnerships, regulatory and environmental compliance trends, and adoption behavior across regions and sectors. It highlights both mature segments (e.g., LPG blending and industrial fuel) and emerging niches (transportation fuel, bio-based DME, chemical feedstock) — offering a comprehensive overview intended for decision-makers, investors, and industry stakeholders evaluating market entry, expansion, or technology deployment.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,022.0 Million |

| Market Revenue (2032) | USD 2,036.4 Million |

| CAGR (2025–2032) | 9.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory & ESG Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Oberon Fuels, Inc., China Energy Investment Corporation, Grillo‑Werke AG, Royal Dutch Shell plc, Mitsubishi Corporation, Korea Gas Corporation, Akzo Nobel N.V., Lummus Technology, Dimeta, DCC Energy |

| Customization & Pricing | Available on Request (10% Customization Free) |