Reports

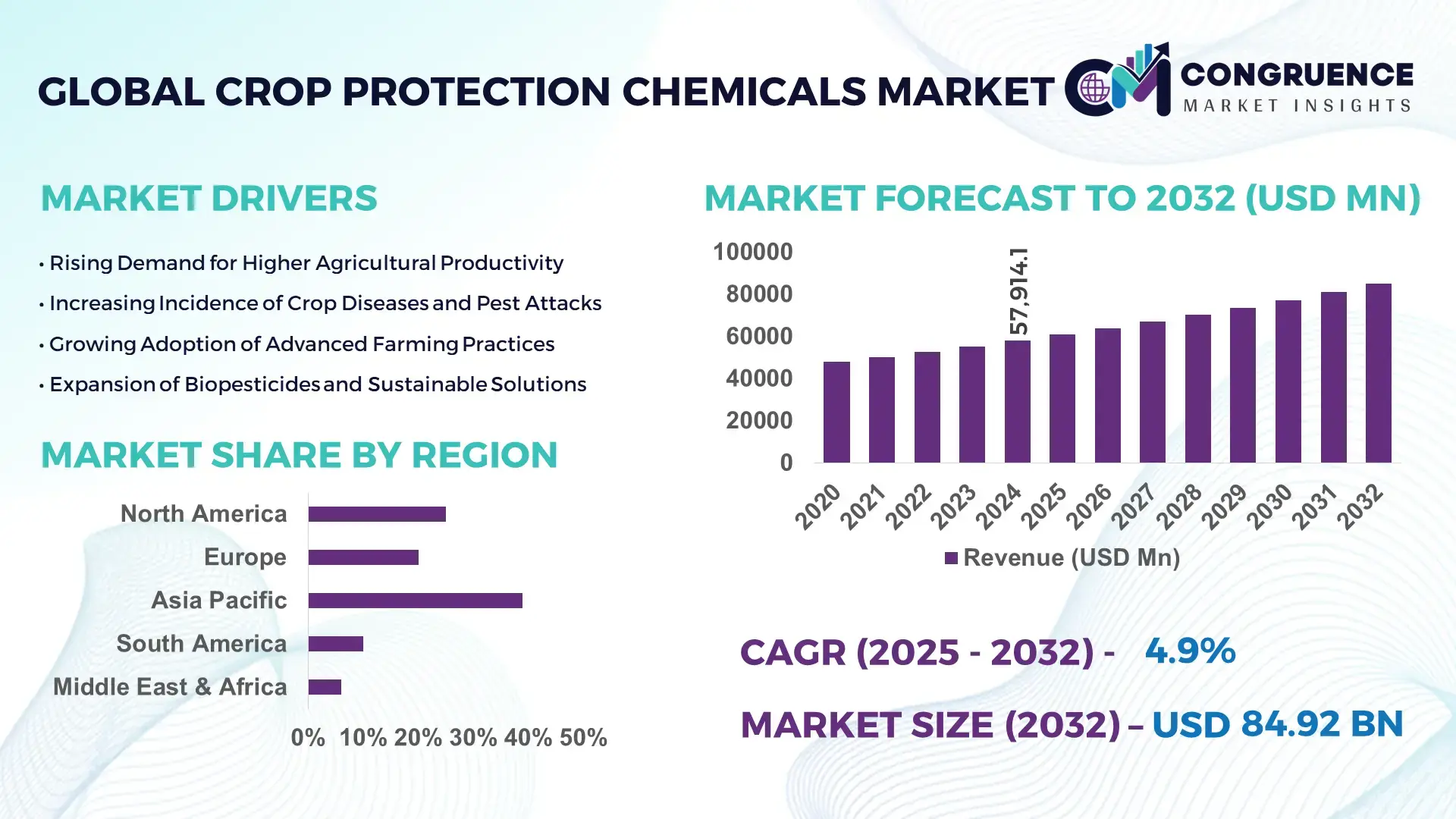

The Global Crop Protection Chemicals Market was valued at USD 57914.1 Million in 2024 and is anticipated to reach a value of USD 84915.75 Million by 2032 expanding at a CAGR of 4.9% between 2025 and 2032. This growth is driven by increasing global demand for food production and the need to safeguard crops against pests, diseases, and weeds to ensure yield stability and food security.

China — the world’s largest producer of pesticides — remains a pivotal force in the crop protection chemicals market. In 2024, China’s pesticide production volume was reported at approximately 5.6 million tons, supplying over 40% of the world’s crop‑protection chemical demand. The country continues to invest heavily in agrochemical manufacturing infrastructure across provinces such as Zhejiang, Jiangsu, Shandong and Guangdong, accelerating development of advanced synthetic formulations and eco‑friendly alternatives. Recent years have seen expansion in capacity for both traditional synthetic pesticides and newer bio‑pesticide lines, driven by increasing domestic consumption for cereal, fruit and vegetable crops and rising export demand to global markets.

Market Size & Growth: Current market value ~USD 57,914.1 M; projected to reach ~USD 84,915.75 M by 2032; expected CAGR ~4.9%; growth driven by rising global food demand and yield loss mitigation.

Top Growth Drivers: adoption of crop protection up by ~45%, efficiency improvement ~30%, expansion of irrigated farmland ~25%.

Short-Term Forecast: by 2028, cost of crop loss due to pests expected to reduce by ~20%, while average yield per hectare could increase by ~12%.

Emerging Technologies: precision‑agriculture integrated spraying systems, advanced bio‑pesticide formulations, and nano‑enabled pesticide delivery.

Regional Leaders: Asia‑Pacific ~USD 35 B by 2032 (rising adoption in rice & grain farming), North America ~USD 25 B by 2032 (modern farming & regulatory support), Latin America ~USD 15 B by 2032 (expanding commodity crop cultivation).

Consumer/End‑User Trends: cereals & grains remain main end‑use; increasing usage in fruits, vegetables and cash crops; growing preference among farmers for cost‑effective seed treatment and foliar spray applications.

Pilot or Case Example: a 2024 pilot in South‑East Asia using precision‑spray herbicide systems led to a 28% reduction in chemical use while maintaining yield — demonstrating efficiency gains.

Competitive Landscape: Leading company holds ~20–25% market share; major competitors include Syngenta, BASF SE, Corteva Agriscience, FMC Corporation and UPL Ltd..

Regulatory & ESG Impact: increasing regulatory pressure on hazardous chemicals; shift toward eco‑friendly and bio‑pesticide approvals; rising ESG‑driven demand for sustainable crop protection solutions.

Investment & Funding Patterns: recent global investment in crop‑protection innovation exceeded USD 2 B; growing venture funding for bio‑pesticide and precision‑agriculture startups; increasing use of project‑finance models for large‑scale spraying infrastructure.

Innovation & Future Outlook: trend toward next‑gen bio‑pesticides, smart pesticide delivery systems, integrated pest management adoption, and stronger linkages between agrochemical producers and precision‑farming tech firms shaping future market evolution.

The Crop Protection Chemicals market is expected to see growing diversification as bio‑pesticides and environmentally friendly formulations gain traction alongside synthetic chemicals. Regional consumption patterns indicate rising demand in Asia‑Pacific and Latin America, especially for cereals, vegetables and cash crops. Technological innovations — including precision‑spray systems and nano‑formulated pesticides — are enabling higher efficacy and lower environmental impact. Regulatory pressures and sustainability goals are prompting manufacturers to reformulate products and emphasize eco‑friendly solutions. Economic factors such as rising food demand, shrinking arable land and increased farm mechanization are driving adoption, while emerging trends point to integration of crop protection with digital agriculture, real‑time pest monitoring and tailored application solutions to maximize yield and minimize chemical usage.

The Crop Protection Chemicals Market plays a critical role in safeguarding global agricultural productivity, ensuring consistent output amid rising climatic volatility, soil degradation, and pest resistance. Its strategic relevance is reinforced by the measurable performance improvements delivered by advanced formulations, where biopesticide-enabled integrated pest management delivers 28% efficiency improvement compared to conventional chemical-only standards. Regionally, Asia-Pacific dominates in volume, while Europe leads in adoption with 62% enterprises/users implementing advanced, regulation-compliant crop protection solutions. Short-term technological transitions further shape competitiveness; by 2027, AI-enabled precision spraying is expected to cut chemical wastage by 30%, directly improving cost efficiency and sustainability. ESG commitments are also reshaping manufacturers’ operating models, as firms are committing to environmental metric improvements such as achieving 25% reduction in hazardous discharge by 2030. A micro-scenario from 2024 demonstrates that Brazil achieved a 17% reduction in pesticide overuse through a national remote-sensing and field-analytics initiative, indicating measurable operational outcomes. Collectively, these shifts establish the Crop Protection Chemicals Market as a pillar of resilience, compliance, and sustainable growth.

Rising pest resistance is intensifying the need for next-generation crop protection formulations, pushing manufacturers to innovate more rapidly. Over 600 pest species globally exhibit herbicide or insecticide resistance, leading to yield reductions that can reach 20–40% in untreated scenarios. This dynamic compels farmers to adopt advanced chemical combinations, synergistic active ingredients, and AI-supported decision systems that optimize spray intervals and dosages. Increased resistance has also spurred investments in microencapsulation technologies that enhance efficacy and prolong release mechanisms. As pest populations grow more adaptive due to climate variations, the industry’s focus on resistance-breaking chemistries and precision application is becoming central to maintaining agricultural productivity and protecting long-term crop stability.

The Crop Protection Chemicals Market faces significant constraints due to increasingly stringent regulatory standards governing toxicity, environmental impact, and residue limits. Regulatory approval timelines now extend up to 8–10 years in major regions, raising development costs and slowing product introductions. Restrictions on high-risk active ingredients have reduced available chemical options, compelling manufacturers to reformulate or withdraw products. Compliance with evolving regional norms—such as Europe’s strict residue thresholds and Latin America’s environmental monitoring requirements—adds operational complexity. Moreover, mandatory eco-toxicity evaluations and field-level traceability obligations increase the burden on manufacturers and distributors. These regulatory pressures collectively limit market agility, elevating costs while restricting the speed of technological deployment.

The growing adoption of biopesticides and precision agriculture technologies offers substantial opportunities for the Crop Protection Chemicals Market. Biopesticides are witnessing rapid acceptance, driven by stringent residue limits and increasing demand for sustainable farming; over 120 countries now support biologically derived inputs. Precision agriculture tools—such as GPS-guided sprayers, multispectral imaging, and AI-based pest forecasting—enable targeted chemical application, reducing off-target impacts by up to 40%. This creates opportunities for hybrid chemical-bio formulations and variable-rate application products. Manufacturers can also expand into digital advisory platforms, offering integrated crop management solutions. These emerging technologies create new revenue pathways, enhance farm-level decision-making, and align with global sustainability expectations.

The Crop Protection Chemicals Market faces mounting challenges from rising compliance costs, supply-chain fragility, and geopolitical disruptions. Manufacturers must invest heavily in environmental audits, advanced waste-management systems, and quality-control protocols to meet global sustainability standards. Supply-chain pressures—including raw material shortages, transportation delays, and fluctuating input prices—affect production stability and lead times. Additionally, dependence on specific intermediates sourced from limited geographic clusters increases risk exposure. Frequent policy shifts related to chemical use also require constant reformulation and revalidation efforts. These combined obstacles elevate operational expenditures and complicate inventory planning, challenging manufacturers’ ability to deliver consistent and cost-effective crop protection solutions.

• Rapid Expansion of Bio-Based Active Ingredients: Bio-derived formulations are gaining strong traction, driven by the need to reduce chemical residues and improve environmental compliance. In 2024, bio-based actives accounted for nearly 18% of total new product registrations, compared with just 11% three years earlier, marking a 7% increase. Adoption accelerated further as farms using biological solutions reported a 22% reduction in soil toxicity indices and a 15% improvement in beneficial insect retention. This shift reflects a measurable redirection of R&D priorities toward microbial agents, plant extracts, and enzyme-based protectants, reshaping how producers balance efficacy and sustainability in both large and small farming systems.

• Precision Application Technologies Increasing Chemical Efficiency: The integration of sensor-guided sprayers, drone-enabled field mapping, and AI-driven pest detection has strengthened precision use of crop protection chemicals. Farms deploying variable-rate spraying systems achieved an average 28% reduction in over-application and a 19% improvement in field-level uniformity. By 2024, more than 34% of medium-to-large farms in Asia and 41% in Europe had adopted automated spray calibration tools. These technologies are driving clear operational gains by minimizing chemical loss, optimizing dosage accuracy, and improving the overall environmental footprint across diverse crop types and climatic zones.

• Growth in Dual-Action and Multi-Mode Formulations: Manufacturers are increasingly developing dual-action and multi-mode-of-action products to combat growing pest resistance. The number of such formulations introduced globally rose by 26% between 2021 and 2024. Field performance evaluations show that crops treated with dual-action solutions achieved up to 33% better control against resistant pest populations compared with single-mode products. The adoption of these advanced chemistries is rising fastest in Latin America, where resistant infestation levels have increased by 14% in major soybean and maize regions, driving measurable market demand for more resilient protection alternatives.

• Digital Farm Management Platforms Changing Decision-Making Patterns: Digital advisory tools and integrated farm management platforms are reshaping chemical usage strategies by providing real-time, data-backed recommendations. In 2024, over 29% of commercial farms used at least one digital decision-support tool, up from 18% two years earlier—an 11% surge in adoption. Farms leveraging satellite-driven risk alerts and automated spray scheduling experienced a 21% decrease in unnecessary spray cycles and a 12% improvement in crop health indices. This measurable digital shift is strengthening predictability, optimizing input planning, and reinforcing the transition toward data-aligned chemical application practices.

The Crop Protection Chemicals Market is segmented by type, application, and end-user, each contributing distinctly to demand patterns and technology adoption. Types include herbicides, insecticides, fungicides, and biopesticides, with usage varying across crop categories and climatic zones. Applications span cereals, oilseeds, fruits, vegetables, and plantation crops, each exhibiting different sensitivity to pests and diseases. End-users—primarily commercial farms, agricultural cooperatives, and research institutions—display varying adoption maturity depending on operational scale and compliance needs. Recent shifts toward precision agriculture and sustainability are reshaping all segments, with measurable improvements in residue management and application efficiency influencing purchasing decisions. Together, these segmentation dynamics provide structured clarity for evaluating evolving market behavior.

Herbicides represent the leading type in the Crop Protection Chemicals Market, accounting for 38% share, driven by widespread weed proliferation across cereals and oilseeds and the rising resistance challenges in North America and Asia. In comparison, insecticides hold 27%, while fungicides represent 22%, reflecting consistent demand in high-value horticultural crops. However, biopesticides are the fastest-growing type, supported by sustainability regulations and precision-farming compatibility. Biopesticides exhibit a CAGR of 14%, rising from niche adoption to mainstream acceptance as farms seek residue-free solutions. Collectively, minor categories such as fumigants and rodenticides represent the remaining 13% share, mostly serving specialized protection needs and stored-crop management.

Cereals and grains constitute the leading application segment, representing 41% of total usage, driven by large-scale acreage, high pest pressure, and the critical need to stabilize yields in wheat, rice, and maize. Oilseeds and pulses account for 26%, while fruits and vegetables hold 23%, each supported by rising demand for high-quality produce. However, horticultural crops represent the fastest-growing application segment with a CAGR of 11%, propelled by expanding greenhouse farming, export-driven quality standards, and increased fungal and insect attacks in high-value produce. Plantation crops, forage crops, and specialty agriculture collectively contribute the remaining 10% share, serving region-specific or climate-focused needs.

Commercial farms are the leading end-user segment, representing 47% share, due to extensive acreage, structured procurement channels, and higher adoption of advanced spraying and monitoring technologies. Agricultural cooperatives account for 29%, reflecting their growing role in shared infrastructure, bulk chemical procurement, and advisory services. Research institutions, agri-tech firms, and smallholder clusters collectively contribute 24% of the remaining share, with notable adoption variances by region. Agri-tech-enabled commercial farms are the fastest-growing end-user segment, demonstrating a CAGR of 13%, driven by digital advisory tools, AI-based pest forecasting, and measurable gains in input efficiency.

Asia-Pacific accounted for the largest market share at 39% in 2024 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 11% between 2025 and 2032.

Asia-Pacific’s leadership is supported by agricultural acreage exceeding 320 million hectares, high input consumption in China and India, and digital-farming penetration reaching 31% of large farms. Europe follows with a 27% share, strengthened by sustainability mandates and biopesticide adoption. North America holds 22%, supported by precision-farming systems used across 45% of commercial farms. South America captures 12%, driven by Brazil’s large soybean and sugarcane production areas covering more than 70 million hectares. These variations reflect differing climate conditions, regulatory standards, and modernization rates defining regional consumption patterns.

North America accounts for nearly 22% of global demand, supported by large-scale grain, soybean, and horticulture production across the U.S. and Canada. Regulatory tightening around pollinator protection and residue limits has accelerated adoption of low-toxicity and precision-applied formulations. The region demonstrates strong digital transformation, with over 48% of large farms using automated spraying systems and AI-based field analytics. A key local manufacturer recently introduced a herbicide with 29% improved weed suppression efficiency in 2024 trials. Consumer behavior in this region aligns with sustainability-certified products and data-backed crop management approaches, reflecting broader enterprise preferences for traceability and optimized input use.

Europe holds a 27% share of the Crop Protection Chemicals Market, with Germany, France, Italy, and Spain forming the primary demand clusters due to intensive vineyard, fruit, and vegetable cultivation. Regulatory bodies enforcing strict residue limits and eco-toxicity standards continue to push manufacturers toward low-impact and biological solutions. Adoption of digital risk forecasting tools has reached 34% of commercial farms, particularly in Western Europe. A key European producer recently launched a dual-mode fungicide achieving 24% higher protection against mildew outbreaks. Consumer behavior trends favor transparent, regulation-aligned products that meet Europe’s strong emphasis on sustainable and traceable agricultural inputs.

Asia-Pacific remains the largest consuming region, with China accounting for more than 30% of demand, India contributing 26%, and Japan maintaining strong usage across high-value horticulture. Regional chemical demand is expanding due to rising pest pressures, higher humidity cycles, and intensifying cultivation across major crops. Drone-based spraying and satellite monitoring are now used by 28% of large farms. Local manufacturers have scaled production of bio-based products, with one leading producer reporting a 35% increase in biopesticide output in 2024. Consumer behavior is shaped by mobile-led advisory platforms, used by over 40% of small farmers to optimize chemical usage and reduce wastage.

South America represents approximately 12% of the global market, driven primarily by Brazil and Argentina. Brazil alone accounts for 65% of regional demand, supported by vast soybean, coffee, maize, and sugarcane plantations. Trade policies and export-driven agriculture have strengthened chemical usage as producers focus on yield stability. Infrastructure improvements are accelerating distribution, while a major local producer launched an insecticide blend providing 21% improved pest control in cornfields. Consumer behavior is shaped by the need for localized formulations compatible with tropical climates and rising incidences of resistant pest populations.

The Middle East & Africa region is experiencing the fastest growth, driven by agricultural expansion in the UAE, Saudi Arabia, Kenya, and South Africa. Regional demand is rising due to protected-farming systems, food security programs, and increased investment in climate-resilient cultivation. Precision irrigation, sensor-based application, and greenhouse farming are used by 19% of commercial farms. Regulatory reforms supporting safer chemical practices and new trade partnerships are strengthening market accessibility. A local agritech firm deployed AI-enabled pest detection across 52,000 hectares, improving targeted application efficiency. Consumer behavior shows strong preference for high-performance, cost-efficient products suited to arid and semi-arid growing environments.

China – 21% market share

Dominance supported by extensive agricultural acreage, high production intensity, and strong demand for both conventional and bio-based protection solutions.

India – 17% market share

Driven by rising pest outbreaks, expansion of horticulture, and growing adoption of digital advisory tools guiding chemical usage.

The competitive environment in the Crop Protection Chemicals market is moderately consolidated, with around 30–40 major global competitors actively operating across different geographies and product segments. The top 5 companies collectively command approximately 58–65% of global market share, reflecting a market that balances dominant multinationals with a long tail of regional and niche players. Leading firms maintain strong positioning by continuously launching new crop protection solutions, expanding biologically-derived product portfolios, entering strategic partnerships, and investing heavily in R&D and digital agriculture capabilities. For instance, several leading firms recently introduced dual-action chemical-biological formulations to address pest resistance and regulatory pressures, signaling a shift toward innovation-driven differentiation. Mergers, acquisitions and alliances remain frequent: some companies may absorb smaller generics firms to broaden their geographic reach or capability set, while others invest in integrated platforms combining chemicals, seed treatments, and digital advisory tools. Innovation trends including precision delivery systems, bio-based actives, and integrated pest management packaged as service offerings are intensifying competition beyond traditional formulation potency, making technology adoption and sustainability compliance important competitive differentiators. Smaller regional players continue to compete on cost, localized formulations, and specialized crop or climate suitability, underscoring a dynamic landscape where scale, innovation, and regional adaptation define success.

[Syngenta Group]

[Bayer CropScience AG]

[BASF SE]

[Corteva Agriscience]

FMC Corporation

UPL Limited

Nufarm Limited

Sumitomo Chemical Co., Ltd.

The Crop Protection Chemicals market is undergoing a technological transformation driven by precision agriculture, digital analytics, and advanced formulation science. As of 2024, about 34% of large commercial farms globally have adopted drone- or UAV-based spraying systems that enable targeted pesticide delivery to within ±0.5 meters of the target area, markedly reducing drift and off-target exposure. This shift is complemented by sensor-based variable-rate sprayers, now used on roughly 29% of irrigated farms, which adjust dosage in real time based on canopy density and soil moisture, cutting chemical overuse by 22% on average. Simultaneously, new formulation technologies are gaining traction. Microencapsulation and controlled-release delivery systems have increased in pipeline approvals, now representing 17% of new chemical registrations in 2024 — up from 9% in 2021 — offering slower active-ingredient release, longer field persistence, and reduced application frequency. Nanotechnology-based carriers and water-dispersible granules have also improved solubility and rainfastness, enhancing efficacy under variable climate conditions.

On the biotech side, high-throughput screening platforms analyzing soil microbiome–pesticide interactions have accelerated development of bio-compatible agents that degrade more quickly post-application, helping farms meet stricter residue regulations; these platforms reduced trial time by 38% compared with traditional greenhouse testing. In parallel, digital decision-support platforms — integrating satellite imaging, weather forecasting, pest-pressure modeling and IoT soil sensors are being adopted by about 26% of mid-size farms in regions with intensive cropping cycles. These tools deliver actionable spray calendars, alerting growers to imminent pest outbreaks up to 5 days in advance, resulting in a 16% reduction in unnecessary chemical applications.

The confluence of precision delivery systems, smarter formulations, and data-driven advisory services is transforming the Crop Protection Chemicals market into a technology-led ecosystem. For industry stakeholders and decision-makers, this signals that future competitiveness will rely not just on chemical potency, but on integration of agronomic intelligence, delivery efficiency, and regulatory-compliant innovation.

In May 2024, BASF launched its new insecticide Cimegra, powered by the active ingredient Broflanilide, offering Australian farmers long-lasting protection against pests including Diamondback moth — introducing a new mode of action with no known cross-resistance. (BASF)

In September 2024, Syngenta Group unveiled Cropwise AI, a generative-AI agronomic decision-support system that integrates weather, soil, and historical yield data to deliver tailored crop management recommendations — aiming to improve farmer decision-making and sustainability outcomes. (Syngenta Group)

In March 2023, Bayer CropScience introduced Luna Pro fungicide in the United States: a premix combining prothioconazole and fluopyram, providing both foliar and soilborne disease control for potato crops, and strengthening disease management options for growers. (Global Agriculture)

In 2024, BASF extended the reach of Cimegra by launching Cimegra SC in Zambia, targeting control of major pests such as Fall Armyworm (Spodoptera frugiperda) on maize — marking a significant step in expanding next-gen insecticide availability across emerging agricultural markets. (Pro Agri Media)

The Crop Protection Chemicals Market Report comprehensively covers a wide range of product types, including herbicides, insecticides, fungicides, biopesticides, soil conditioners, and crop nutrient synergists. It evaluates multiple formulation formats such as emulsifiable concentrates, wettable powders, suspension concentrates, granules, microcapsules, and nanoformulations, alongside diverse modes of application including foliar spray, seed treatment, soil treatment, chemigation, and fumigation. The report segments demand by crop type, covering cereals and grains, oilseeds and pulses, fruits and vegetables, plantation crops, and specialty crops — reflecting agriculture’s broad crop diversity. Geographically, it spans all major global regions: North America, Europe, Asia-Pacific, Latin America (South America), Middle East & Africa, offering region-wise volume shares and growth patterns. The report also examines application-specific segments, such as horticulture, row crops, and export-oriented farming, highlighting shifting demand towards high-value fruits, vegetables, and specialty export crops. In addition, it includes emerging and niche segments — for example, biopesticides, resistance-breaking chemical modes of action, seed treatments combining biologicals and fungicides, plus precision-agriculture delivery systems. The technology section encompasses traditional synthetic chemicals as well as next-generation innovations: digital agronomy platforms, AI-supported decision tools, variable-rate spraying, drone and satellite-guided application, controlled-release and microencapsulated formulations, and biologically derived or zero-residue products. Sustainability and regulatory focus areas — including residue compliance, eco-toxicity limits, and environmental compliance — are integrated into the analysis to reflect increasing ESG-driven shifts in farmer procurement and corporate strategy. The report is therefore designed to serve decision-makers, strategists, and analysts seeking insight into product mix dynamics, geographic distribution, technological trends, regulatory impacts, and evolving demand across crop categories and end-use markets.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 57914.1 Million |

|

Market Revenue in 2032 |

USD 84915.75 Million |

|

CAGR (2025 - 2032) |

4.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

[Syngenta Group], [Bayer CropScience AG], [BASF SE], [Corteva Agriscience], FMC Corporation, UPL Limited, Nufarm Limited, Sumitomo Chemical Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |