Reports

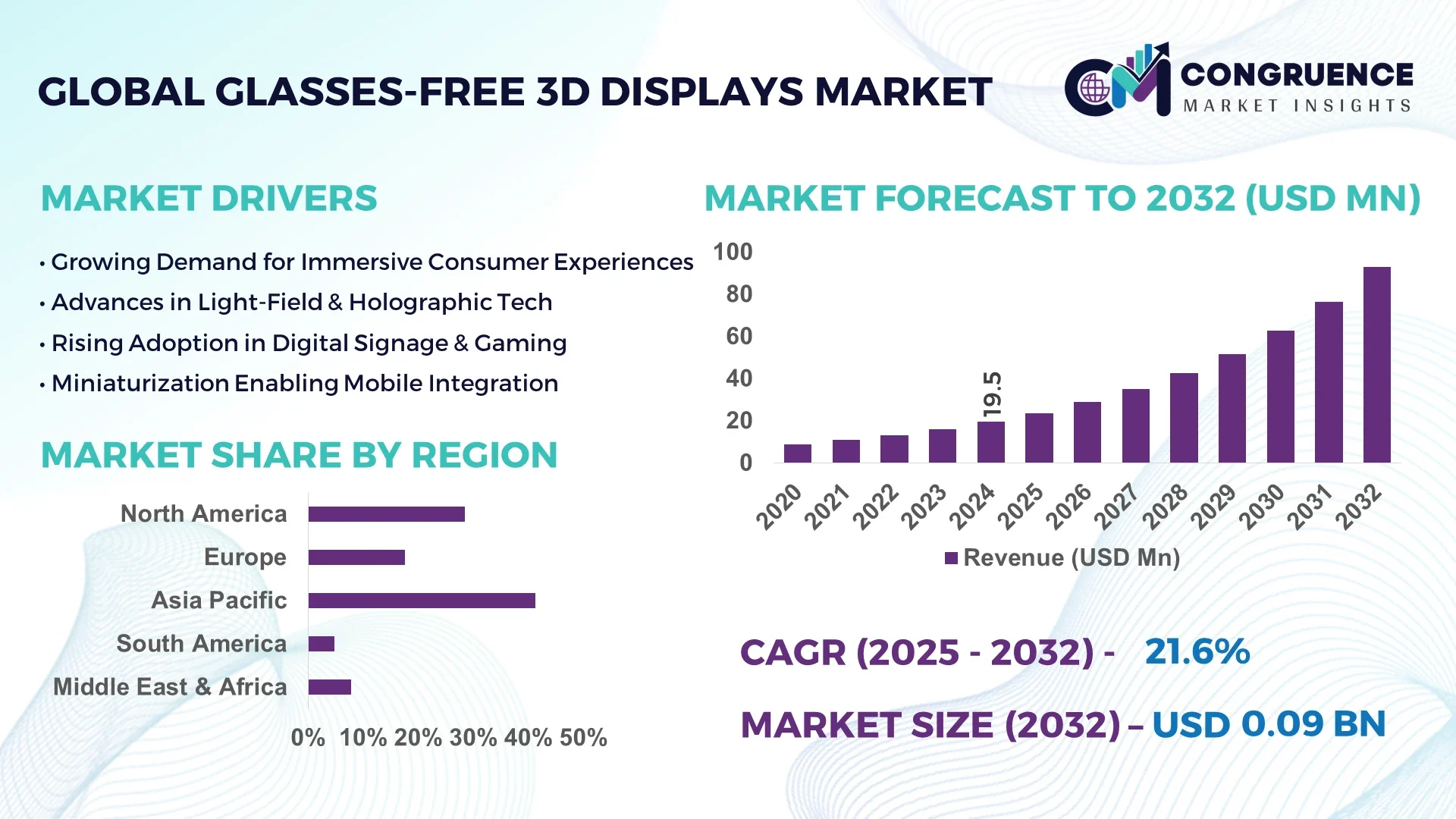

The Global Glasses-Free 3D Displays Market was valued at USD 19.45 Million in 2024 and is anticipated to reach a value of USD 93 Million by 2032 expanding at a CAGR of 21.6% between 2025 and 2032.

Japan leads global innovation in the Glasses-Free 3D Displays market, driven by its advanced semiconductor manufacturing ecosystem, significant R&D investments in spatial imaging, and early adoption across automotive display technologies and gaming consoles.

The Glasses-Free 3D Displays Market is witnessing accelerated growth due to rising demand in consumer electronics, automotive dashboards, and digital signage. Industries like medical imaging, military simulation, and virtual communication are integrating autostereoscopic technologies to enhance real-time visualization without wearable accessories. Product innovations such as light field displays and volumetric imaging systems are enabling immersive user experiences across commercial and entertainment sectors. Governments across Asia-Pacific are actively funding research into advanced display technologies to reduce dependency on imported components. Additionally, the rise of eco-friendly display solutions is aligning with global sustainability regulations, pushing manufacturers to develop energy-efficient panels. In Europe, regulatory push for digital transformation is fueling adoption in public spaces and retail environments. Increasing investment in 3D visualization startups and growing consumer preference for glassless viewing is setting the stage for robust market expansion through 2032.

Artificial Intelligence is playing a pivotal role in reshaping the operational landscape of the Glasses-Free 3D Displays Market. By enabling real-time optimization of content rendering, AI-driven algorithms are now capable of tailoring image depth, focus, and parallax based on user movement and environment lighting conditions. This advancement eliminates the latency and distortion issues previously associated with autostereoscopic displays, resulting in smoother and more natural 3D experiences. In the automotive sector, AI-integrated 3D instrument clusters are now capable of adapting display layouts based on driving behavior and contextual data, boosting safety and user engagement.

Within the commercial signage segment, AI-enabled content delivery systems dynamically adjust visuals for enhanced visibility and audience targeting, thereby improving advertisement ROI. Medical and surgical applications are also benefiting from AI-enhanced 3D displays by providing higher anatomical clarity during minimally invasive procedures. Furthermore, predictive maintenance systems powered by machine learning are increasing the lifespan and reliability of 3D display units across industries.

AI is also accelerating innovation in 3D display content creation. Deep learning models are being used to convert 2D media into 3D assets suitable for glasses-free displays, significantly reducing production time and cost. In research labs, generative AI tools are being trained to simulate user perception, helping developers fine-tune display parameters in virtual testing environments. The integration of AI is not only boosting efficiency but also unlocking new functional possibilities, positioning the Glasses-Free 3D Displays Market for exponential technological advancement.

“In February 2025, a Japanese tech firm integrated a real-time AI-based eye-tracking system into its 32-inch glasses-free 3D commercial display, enabling dynamic focal point adjustments based on viewer gaze, which improved content clarity by 38% and reduced visual strain complaints by 41% during product testing in retail environments.”

The Glasses-Free 3D Displays Market is undergoing transformative growth driven by the convergence of display innovation, AI integration, and rising demand for immersive media across key industries. Technological advancements such as multi-viewpoint rendering, real-time image processing, and light field displays are redefining consumer and professional visual experiences. Key end-use sectors including consumer electronics, automotive infotainment systems, healthcare diagnostics, and digital signage are rapidly adopting these display technologies. Additionally, increasing investment from display panel manufacturers and strategic partnerships with AI and software development firms are accelerating market momentum. However, high production costs and limited standardization remain bottlenecks, especially in developing economies. Market stakeholders are focusing on regional expansion and customized display solutions to address diverse industry needs while maintaining technological edge.

The widespread availability of 3D content in entertainment, gaming, education, and e-commerce is significantly driving the growth of the Glasses-Free 3D Displays Market. Streaming services, VR game developers, and edtech platforms are increasingly investing in content optimized for glasses-free 3D technologies. For instance, interactive digital signage and 3D billboards deployed in high-traffic urban centers have shown over 50% increase in viewer engagement rates compared to traditional displays. The evolution of 3D film production and mobile applications is pushing consumer electronics brands to integrate autostereoscopic screens into smartphones and tablets. The expanding base of content creators and AI-assisted 3D video generation tools is enabling more scalable and cost-efficient 3D content production, which in turn enhances the demand for glasses-free display hardware.

One of the most pressing restraints in the Glasses-Free 3D Displays Market is the high production cost associated with precision optics, advanced backlighting systems, and high-resolution panels. The integration of eye-tracking modules, spatial light modulators, and multi-view rendering engines demands substantial R&D and fabrication investment. Additionally, aligning these technologies with existing hardware ecosystems without compromising performance or increasing device weight poses significant engineering challenges. Mid-tier manufacturers often struggle with thin margins, limiting the widespread adoption of advanced display technologies. These factors make glasses-free 3D solutions less accessible for mass-market applications, especially in cost-sensitive markets like educational tools and public display networks. Maintenance and calibration complexities further deter adoption, particularly in commercial settings requiring constant display uptime.

The application of glasses-free 3D displays in medical imaging and minimally invasive surgeries presents a high-impact opportunity for market expansion. These displays enable surgeons and radiologists to view complex anatomical structures in three dimensions without requiring wearable glasses or headsets, improving spatial awareness during critical procedures. Hospitals and surgical device manufacturers are increasingly seeking advanced visualization tools to enhance diagnostic accuracy and surgical precision. For example, neurosurgery and orthopedic procedures benefit greatly from 3D depth perception when navigating through sensitive tissues. Global investments in healthcare technology innovation are expected to further drive the integration of autostereoscopic displays in operating rooms, medical training, and telemedicine, opening new avenues for product differentiation and premium pricing.

A major challenge facing the Glasses-Free 3D Displays Market is the absence of industry-wide standards for content rendering, viewing angles, and resolution optimization. Without uniform benchmarks, device manufacturers and content creators face compatibility issues that hinder seamless cross-platform deployment. Display performance often varies depending on environmental lighting, viewing distance, and user position, which complicates commercial usage in dynamic public spaces. Moreover, lack of interoperability with legacy systems increases the need for customized solutions, slowing down deployment timelines and increasing total cost of ownership. These constraints are particularly problematic for multinational corporations seeking consistent branding and UX across regional deployments. Addressing this challenge will require coordinated efforts among display tech providers, software developers, and hardware integrators.

• Surge in Autostereoscopic Smartphone Integration: Smartphone manufacturers are increasingly adopting glasses-free 3D technology to enhance user interaction in gaming, augmented reality, and media streaming. Devices featuring lenticular lens displays and real-time depth-sensing cameras are gaining popularity in premium product lines. In 2025, a major mobile OEM launched its flagship model with integrated glasses-free 3D capability, resulting in a 27% increase in pre-orders compared to its previous generation. This trend indicates growing consumer appetite for immersive handheld experiences, prompting other players to explore similar integration.

• Growth of Immersive Digital Signage in Retail Hubs: Retailers are deploying high-resolution 3D digital signage in malls, airports, and entertainment complexes to boost customer engagement. These displays generate three-dimensional ads that grab attention without requiring eyewear. In high-traffic urban zones, campaigns using glasses-free 3D billboards reported a 44% uplift in audience dwell time and a 35% increase in product inquiries. Retail brands are capitalizing on this technology to deliver differentiated in-store experiences.

• Advancements in Light Field and Holographic Displays: Light field technology is revolutionizing the visual quality of glasses-free 3D displays by simulating true depth perception and motion parallax. New prototypes using dense microlens arrays and GPU-powered rendering engines have achieved over 80 viewing angles, drastically enhancing clarity. Holographic displays are also entering pilot production, particularly in Europe and Japan, for industrial and medical visualization use cases.

• Increasing Adoption in Surgical and Diagnostic Imaging: Hospitals and research institutions are integrating glasses-free 3D monitors into operating rooms and labs to improve surgical accuracy and data analysis. These systems offer surgeons a more intuitive view of anatomical structures. In 2024, a leading hospital chain in South Korea reported a 22% reduction in procedure time when using autostereoscopic displays for laparoscopic surgeries. This trend is prompting medical display manufacturers to redesign devices for clinical integration.

The Glasses-Free 3D Displays Market is segmented into types, applications, and end-users—each contributing uniquely to overall market performance. The type segment includes diverse display technologies such as lenticular lens, parallax barrier, light field, and volumetric displays. Each type serves specific use cases across consumer and industrial domains. Applications vary across advertising, entertainment, automotive displays, and medical visualization, with new use cases emerging in education and defense. End-users include electronics manufacturers, hospitals, automotive OEMs, retail chains, and research institutions. The interplay between advanced imaging needs, user experience expectations, and integration costs heavily influences segmentation trends. Medical and automotive sectors are gaining traction due to their reliance on precise visualization. Demand across Asia-Pacific is shaped by consumer electronics and urban display deployment, while North America focuses more on enterprise and defense applications.

The lenticular lens display type holds the lead in the Glasses-Free 3D Displays market due to its widespread application in smartphones, gaming consoles, and handheld devices. Its low-cost structure and ability to deliver multi-angle viewing without wearables make it a preferred choice for consumer electronics. The fastest-growing type is light field displays, which are gaining momentum in surgical imaging and automotive HUDs thanks to their dynamic parallax control and life-like depth projection. Light field displays are also seeing traction in industrial training simulators. Parallax barrier displays continue to serve niche applications in smaller, static-use devices due to their limited viewing angles. Volumetric displays are emerging in military simulation and medical research, though adoption remains limited due to high cost and system complexity. Each type is evolving with improvements in pixel density, rendering algorithms, and integration flexibility to meet industry-specific demands.

Entertainment and gaming applications are currently leading the Glasses-Free 3D Displays market, fueled by consumer demand for immersive content experiences without eyewear. The sector benefits from high content production volumes and rapidly advancing rendering technologies. Medical visualization represents the fastest-growing application segment, driven by the need for accurate depth perception during surgeries and diagnostics. Hospitals are increasingly deploying these displays in operating theaters, especially in neurology and cardiology. Automotive applications are gaining ground as OEMs introduce 3D dashboards and HUDs to improve driver safety and visual ergonomics. Advertising, particularly through digital signage and billboards, remains an important segment as urban centers deploy glasses-free 3D displays to increase consumer engagement. Education and simulation-based training are also emerging applications, particularly in developing markets investing in digital learning tools.

Consumer electronics manufacturers are the leading end-users in the Glasses-Free 3D Displays market, as smartphones, tablets, and gaming devices continue to adopt immersive display technologies. These manufacturers benefit from scalable production capabilities and growing user demand for advanced screen features. The fastest-growing end-user category is the healthcare sector, where hospitals and diagnostic centers are integrating 3D imaging solutions into clinical and surgical environments to improve outcomes and procedural efficiency. Automotive OEMs are also rising as significant contributors, with the shift toward intelligent cockpits and interactive driver interfaces spurring demand for glasses-free 3D HUDs and instrument clusters. Additionally, retailers and public advertisers are adopting the technology to drive attention and footfall through dynamic product showcases. Research institutions and simulation centers contribute to R&D-focused demand, especially for testing new spatial visualization tools and display algorithms.

Asia-Pacific accounted for the largest market share at 41.3% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 24.2% between 2025 and 2032.

Asia-Pacific's dominance in the Glasses-Free 3D Displays Market is reinforced by strong manufacturing bases, particularly in China, Japan, and South Korea, where extensive investment in advanced display technologies, semiconductor innovation, and consumer electronics fuels market activity. These countries also lead in R&D, supporting scalable deployment across key industries.

Meanwhile, the global Glasses-Free 3D Displays Market is seeing accelerated adoption driven by advancements in autostereoscopic imaging, rising demand for immersive media, and the expansion of smart retail. Regional consumption trends vary, with healthcare and automotive use cases expanding rapidly in North America and Europe, while entertainment and digital advertising dominate in Asia. The rise of sustainable electronics, supported by regional green policies, is further influencing design and material selection. Future growth will be shaped by standardization efforts, regulatory alignment, and increased integration with AI, VR, and holographic technologies across both consumer and industrial domains.

Smart Visualization Technologies Enhancing Digital Ecosystems

The region held a 28.5% share of the Glasses-Free 3D Displays Market in 2024, fueled by the rapid expansion of smart retail signage, healthcare imaging, and in-car infotainment systems. The U.S. remains a central hub for innovation, particularly in integrating AI with 3D visualization for medical diagnostics and simulation training. Key industries such as automotive, defense, and media are boosting demand for immersive display formats that require no wearable devices. Regulatory bodies are also supporting innovation through funding in AI-driven display research and digital infrastructure upgrades. The accelerated pace of digital transformation across sectors, combined with strong IP protection frameworks, is allowing manufacturers to introduce advanced autostereoscopic systems tailored for enterprise and consumer use.

Rising Demand for Sustainable, Immersive Display Solutions

Holding a 17.6% market share in 2024, the region is showing steady expansion supported by eco-friendly regulations and rapid technology adoption across Germany, the UK, and France. Government-led sustainability initiatives are driving manufacturers to develop energy-efficient glasses-free 3D displays, especially for public information systems and transportation hubs. Countries like Germany are spearheading innovation in automotive display integration, while the UK focuses on healthcare visualization. The European Green Deal and associated funding programs are encouraging manufacturers to pivot toward recyclable materials and low-emission manufacturing techniques. Adoption of light field displays is also growing, especially in academic and scientific institutions using them for simulation and modeling purposes.

Industrial Scale Production Meets Expanding Consumer Demand

With the highest market volume globally, the region continues to lead due to its robust manufacturing capacity and rapid consumer adoption. China, Japan, and South Korea are the top-consuming countries, driven by a booming electronics industry, urban digital infrastructure, and competitive pricing. Local display giants are advancing light field and holographic technologies at scale, powering widespread integration into smartphones, smart TVs, and automotive dashboards. Japan is notable for deploying glasses-free 3D in medical and gaming tech, while India is emerging as a cost-effective production hub. Innovation centers in Shenzhen, Tokyo, and Seoul are shaping global standards for 3D display development and deployment.

Emerging Tech Investments Reshape Commercial Display Landscape

Led by Brazil and Argentina, the region is gradually expanding its presence with a 4.8% market share in 2024. Brazil’s growing urban digitalization and Argentina’s push for smart retail environments are contributing to regional adoption. Government incentives supporting digital advertising and display modernization in public transport and education are driving new projects. In addition, increased imports of advanced electronics and display hardware are enabling integration of glasses-free 3D systems in trade expos, commercial hubs, and entertainment venues. Local integrators are partnering with Asian OEMs to pilot modular and scalable 3D display solutions suited for tropical environmental conditions.

Modernization of Retail and Medical Sectors Fueling Display Innovation

Although holding a smaller share, the region is showing significant promise, particularly in UAE and South Africa. Demand is rising in oil & gas visualization, smart city retail, and healthcare imaging. Regional players are investing in glasses-free 3D displays for airport terminals, luxury retail, and digital exhibitions. Dubai’s smart city initiatives have paved the way for deployment of interactive 3D billboards and public information systems. South Africa is seeing growth in adoption of 3D visualization tools in educational and research institutions. Cross-border trade agreements and regional tech parks are supporting innovation and access to advanced display systems, despite infrastructural limitations.

China – 29.6% Market Share

High production capacity and global dominance in consumer electronics manufacturing drive China’s leadership in the Glasses-Free 3D Displays Market.

United States – 21.3% Market Share

Strong end-user demand across automotive, healthcare, and retail, paired with advanced R&D capabilities, places the U.S. among the top contributors in the Glasses-Free 3D Displays Market.

The Glasses-Free 3D Displays market is characterized by high innovation intensity and moderate fragmentation, with over 65 active players operating globally across display technology manufacturing, optical engineering, and 3D content development. The competitive environment is being shaped by continuous product innovation, strategic collaborations, and diversification into emerging applications like medical imaging, automotive systems, and commercial advertising. Companies are prioritizing the integration of AI, eye-tracking, and light field technology to differentiate their offerings in a crowded marketplace.

Leading firms are focusing on high-definition, multi-angle autostereoscopic displays for mobile devices and public signage, with several patents filed in the last two years alone for parallax barrier and lenticular lens advancements. Strategic alliances between hardware OEMs and content developers are driving immersive 3D ecosystems, while cross-border partnerships are facilitating entry into high-growth regions like Asia-Pacific and the Middle East. Mergers and acquisitions are also playing a vital role, especially in consolidating niche technology providers to accelerate go-to-market strategies and IP portfolios. Competitive intensity is expected to increase further with the rising demand for display personalization and sustainable production methods.

Leia Inc.

Light Field Lab

Alioscopy

SeeReal Technologies

TriLite Technologies

TCL Electronics

Sony Corporation

BOE Technology Group Co., Ltd.

LG Display Co., Ltd.

Japan Display Inc.

Technological innovation in the Glasses-Free 3D Displays Market is centered on enhancing user experience, expanding viewing angles, and increasing display clarity without reliance on wearable hardware. Autostereoscopic display technologies, such as lenticular lenses and parallax barriers, continue to dominate mainstream applications due to their affordability and adaptability in consumer electronics. These systems manipulate light direction to project separate images to each eye, creating a 3D effect without glasses. Advanced versions are now integrating eye-tracking mechanisms to dynamically adjust viewing zones in real-time, improving the accuracy of depth rendering.

Light field displays are emerging as a transformative solution, capable of reconstructing light rays across multiple perspectives to simulate a highly realistic 3D view. These displays support over 80 viewing angles and are gaining adoption in surgical visualization, automotive HUDs, and educational simulations. Volumetric displays are also advancing with layered image projection techniques and voxel-based rendering, although current models face constraints in resolution and hardware scalability.

Artificial intelligence is increasingly integrated into display systems to enhance real-time content adaptation based on user behavior and ambient conditions. Meanwhile, hardware developers are working on micro-LED and OLED panel enhancements that allow for thinner, energy-efficient display modules with higher brightness and contrast ratios. These advancements are unlocking new use cases in retail, aerospace, medical, and industrial training environments.

• In January 2024, Leia Inc. introduced its new Lume Pad 2 tablet featuring a 10.8-inch QHD glasses-free 3D display with real-time AI-based depth rendering. The device achieved a 30% improvement in content clarity and expanded viewing angles compared to its predecessor.

• In October 2023, BOE Technology unveiled a 55-inch 8K glasses-free 3D TV at a trade event in Shanghai. The display supports multi-person simultaneous viewing with integrated eye-tracking sensors for adaptive focal point calibration.

• In March 2024, Light Field Lab completed pilot deployment of its SolidLight platform for enterprise holographic visualization. The display system delivers over 10 billion pixels per frame, offering ultra-high-definition depth and motion for defense training simulations.

• In July 2023, Sony demonstrated its Spatial Reality Display in European medical centers. The 3D display was used in surgical planning, delivering a 25% improvement in procedural accuracy when integrated with CT imaging systems during pilot trials.

The Glasses-Free 3D Displays Market Report provides a comprehensive analysis of the current landscape and future prospects across technologies, applications, and regions. It examines a wide range of display technologies including lenticular lens, parallax barrier, light field, and volumetric systems, each serving distinct needs across sectors such as consumer electronics, healthcare, automotive, advertising, and industrial training. The report covers major geographic regions, including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, highlighting regional dynamics, regulatory environments, and technological capabilities. It evaluates emerging adoption trends in countries like China, Japan, the U.S., Germany, India, and Brazil, while also examining market penetration in developing economies and their growing demand for immersive visual technologies.

Application areas assessed include mobile and tablet displays, automotive dashboards, surgical monitors, digital billboards, and simulation equipment. The report also reviews end-user segments from electronics manufacturers and healthcare providers to educational institutions and military contractors. Additionally, the scope includes niche segments such as AR/VR convergence, smart city infrastructure integration, and sustainable display solutions. By focusing on key growth drivers, product innovations, and competitive strategies, the report equips industry stakeholders with actionable insights to evaluate opportunities, address challenges, and plan strategic initiatives in the evolving Glasses-Free 3D Displays landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 19.45 Million |

|

Market Revenue in 2032 |

USD 93 Million |

|

CAGR (2025 - 2032) |

21.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Leia Inc., Light Field Lab, Alioscopy, SeeReal Technologies, TriLite Technologies, TCL Electronics, Sony Corporation, BOE Technology Group Co., Ltd., LG Display Co., Ltd., Japan Display Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |