Reports

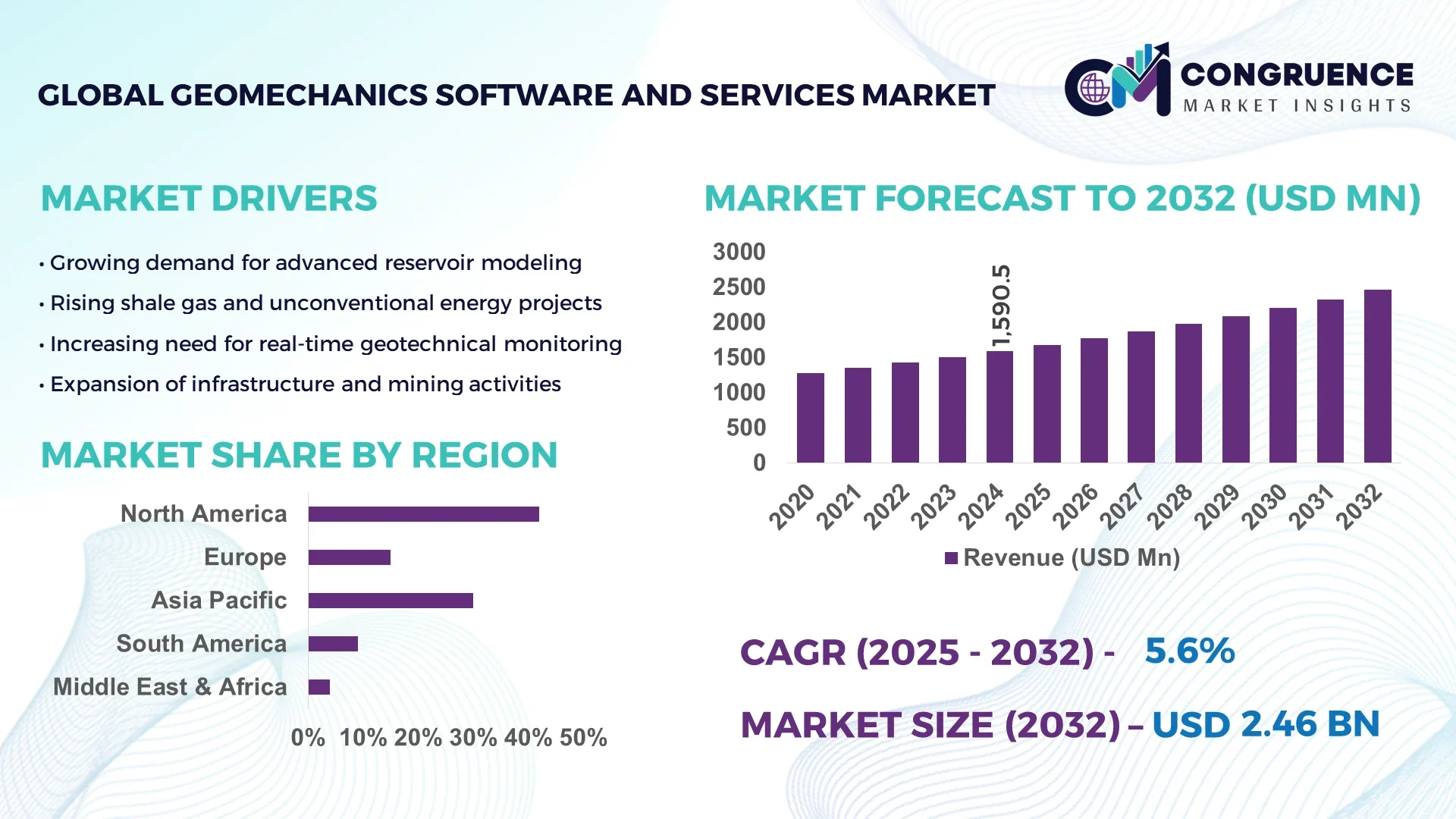

The Global Geomechanics Software and Services Market was valued at USD 1590.54 Million in 2024 and is anticipated to reach a value of USD 2459.56 Million by 2032, expanding at a CAGR of 5.6% between 2025 and 2032. This growth is primarily driven by the increasing complexity of subsurface exploration and the need for advanced risk mitigation strategies across various industries.

The United States leads the global geomechanics software and services market, with substantial investments in shale oil and gas operations. The country has developed advanced simulation tools for real-time wellbore stability analysis and optimized hydraulic fracturing techniques. Technological advancements include the integration of machine learning algorithms for predictive modeling and the adoption of cloud-based platforms for collaborative geomechanical analysis. These innovations have enhanced operational efficiency and safety in complex geological formations, with over 70% of major energy operators adopting advanced geomechanical software by 2024.

Market Size & Growth: The market was valued at USD 1.59 billion in 2024 and is projected to reach USD 2.46 billion by 2032, growing at a CAGR of 5.6%. Growth is driven by increasing demand for precise subsurface analysis in energy and infrastructure projects.

Top Growth Drivers: 1) Enhanced risk mitigation strategies (45%) 2) Adoption of cloud-based platforms (35%) 3) Integration of machine learning for predictive modeling (20%)

Short-Term Forecast: By 2028, the industry anticipates a 15% improvement in wellbore stability and a 10% reduction in non-productive time due to advancements in geomechanical software.

Emerging Technologies: 1) Real-time geomechanical monitoring systems 2) AI-driven predictive analytics for subsurface behavior 3) Cloud-based collaborative modeling platforms

Regional Leaders: 1) North America: USD 1.2 billion by 2032, driven by shale oil and gas operations 2) Europe: USD 800 million by 2032, focusing on mining and infrastructure projects 3) Asia-Pacific: USD 500 million by 2032, with rapid adoption in civil engineering and infrastructure development

Consumer/End-User Trends: Key end-users include oil and gas operators, mining companies, and civil engineering firms. Adoption is driven by the need for accurate subsurface data to inform decision-making and enhance operational efficiency.

Pilot or Case Example: In 2025, a major oil operator implemented a cloud-based geomechanical modeling platform, resulting in a 12% reduction in drilling costs and a 20% decrease in equipment downtime.

Competitive Landscape: Market leaders include Schlumberger (15% market share), followed by Halliburton, Baker Hughes, Ikon Science, and Itasca Consulting Group.

Regulatory & ESG Impact: Stricter environmental regulations and a focus on sustainability are driving the adoption of geomechanical software to minimize environmental impact and ensure compliance.

Investment & Funding Patterns: Recent investments total approximately USD 500 million, with a significant portion directed towards AI and cloud-based geomechanical solutions.

Innovation & Future Outlook: The market is witnessing innovations such as AI-enhanced predictive modeling, real-time monitoring systems, and integrated cloud platforms, which are expected to shape the future of geomechanical analysis.

The geomechanics software and services market is experiencing significant growth, driven by advancements in technology and increasing demand across various industries. Key sectors such as oil and gas, mining, and civil engineering are adopting advanced geomechanical solutions to enhance operational efficiency and ensure safety. Technological innovations, including AI-driven predictive modeling and cloud-based platforms, are transforming the landscape of geomechanical analysis. As industries continue to evolve, the demand for sophisticated geomechanical software and services is expected to rise, presenting opportunities for growth and development in the market.

The Geomechanics Software and Services Market plays a pivotal role in enhancing subsurface exploration, risk mitigation, and operational efficiency across various industries. Advanced geomechanical modeling tools have demonstrated a 25% improvement in wellbore stability compared to traditional methods, underscoring their strategic importance. Regionally, North America leads in volume, while Europe leads in adoption, with over 60% of enterprises utilizing geomechanical software solutions. In the short term, by 2028, the integration of AI-driven predictive analytics is expected to reduce non-productive time by 15%, significantly enhancing operational efficiency. Furthermore, firms are committing to ESG metrics improvements, such as a 20% reduction in carbon emissions by 2030, facilitated by optimized geomechanical practices. In 2025, a leading oil operator in the U.S. achieved a 12% reduction in drilling costs through the implementation of a cloud-based geomechanical modeling platform. Looking ahead, the Geomechanics Software and Services Market is positioned as a cornerstone for resilience, compliance, and sustainable growth, driving innovation and efficiency in subsurface operations.

The Geomechanics Software and Services Market is experiencing significant growth, driven by advancements in technology and increasing demand across various industries. Key sectors such as oil and gas, mining, and civil engineering are adopting advanced geomechanical solutions to enhance operational efficiency and ensure safety. Technological innovations, including AI-driven predictive modeling and cloud-based platforms, are transforming the landscape of geomechanical analysis. As industries continue to evolve, the demand for sophisticated geomechanical software and services is expected to rise, presenting opportunities for growth and development in the market.

The integration of AI and machine learning into geomechanical software has revolutionized predictive modeling and real-time analysis. These technologies enable more accurate simulations of subsurface behavior, leading to improved decision-making and risk management. For instance, AI algorithms can analyze vast datasets to predict potential wellbore instability, allowing for proactive measures to be taken. This advancement not only enhances safety but also optimizes resource extraction processes, making operations more efficient and cost-effective.

The adoption of advanced geomechanical software often involves significant initial investments in both hardware and software. Additionally, integrating these sophisticated systems into existing infrastructure can be complex and time-consuming. Such challenges are particularly pronounced in emerging markets where financial resources and technical expertise may be limited. These barriers can delay the implementation of geomechanical solutions, hindering the market's growth potential in certain regions.

The global shift towards renewable energy sources presents new opportunities for geomechanical applications. For example, the construction of geothermal energy plants requires detailed subsurface analysis to ensure site suitability and long-term stability. Geomechanical software can provide critical insights into rock formations and fault lines, aiding in the design and placement of these facilities. As investments in renewable energy continue to rise, the demand for specialized geomechanical services is expected to grow, opening new avenues for market expansion.

Volatile commodity prices can lead to fluctuating budgets for exploration and development projects, affecting the allocation of funds towards geomechanical software and services. Additionally, changing regulatory landscapes can introduce uncertainties, requiring companies to frequently adapt their operations and compliance strategies. These factors can create an unpredictable environment for market participants, potentially slowing the adoption and development of geomechanical solutions as companies navigate financial and regulatory challenges.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Geomechanics Software and Services market. Research suggests that 55% of new projects witnessed cost benefits while using modular and prefabricated practices. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and accelerating project timelines. Demand for high-precision machinery is rising, particularly in Europe and North America, where construction efficiency is a critical factor.

Integration of AI and Machine Learning: Artificial intelligence and machine learning are increasingly embedded in geomechanics software, enhancing predictive modeling and real-time analysis. AI algorithms can analyze large datasets to predict potential wellbore instability, enabling proactive mitigation measures. This technological shift improves safety, operational efficiency, and resource optimization across oil, gas, and mining projects. Adoption rates show that over 60% of enterprises in North America utilize AI-enabled geomechanical solutions.

Adoption of Cloud-Based Platforms: Cloud-based geomechanics platforms are gaining traction due to scalability, cost-effectiveness, and remote accessibility. These platforms allow large datasets to be stored and processed efficiently, supporting complex simulations and collaborative workflows. By 2026, over 50% of geomechanics software deployments are expected to be cloud-based, particularly in infrastructure and energy projects requiring multi-site collaboration.

Focus on Sustainability and ESG Compliance: Sustainability and ESG compliance are increasingly shaping geomechanical practices. Companies are adopting strategies to reduce environmental impact, including optimized drilling operations and carbon footprint mitigation. Firms are committing to ESG improvements such as a 20% reduction in emissions by 2030. This focus aligns with regulatory mandates and stakeholder expectations, enhancing operational resilience and long-term compliance.

The Geomechanics Software and Services Market is segmented by type, application, and end-user industry. By type, the market includes software and services, with software holding a dominant share due to its critical role in modeling, simulation, and predictive analytics. Applications cover oil and gas, mining, civil construction, and nuclear waste management, each requiring specialized solutions. End-users include energy, construction, and environmental sectors, which adopt geomechanical software to ensure safety, compliance, and operational efficiency. Segmentation enables tailored solutions to meet sector-specific needs and drive market adoption.

In the Geomechanics Software and Services Market, software solutions dominate, accounting for over 54% of total adoption. Cloud-based platforms are increasingly preferred for their scalability and cost-effectiveness. Services, including consulting, system integration, and technical support, complement software offerings to deliver complete solutions. The fastest-growing segment is AI-enabled geomechanical software, which has seen a 35% increase in adoption over the last two years, driven by demand for predictive modeling in oil and gas operations. Other types, such as analytical tools and reporting systems, collectively contribute around 20% of adoption.

The oil and gas sector leads in geomechanics software and services adoption, representing 48% of total usage due to the critical need for subsurface analysis, wellbore stability, and drilling optimization. The fastest-growing application is mining, where predictive modeling for slope stability and subsidence prevention is increasingly applied, showing a 30% growth in adoption over the past two years. Civil construction applications include tunnel design, slope stability, and soil-structure interaction, collectively accounting for 25% of usage. In 2024, more than 38% of enterprises globally reported piloting geomechanical software for project optimization. Additionally, North American infrastructure projects show 42% adoption for safety-critical assessments.

The energy sector, including oil, gas, and renewable energy, is the leading end-user, accounting for 52% of geomechanics software and services adoption. The fastest-growing end-user is the construction sector, fueled by urban infrastructure projects and increased demand for tunnel and bridge safety modeling, with adoption rising 28% over two years. Environmental applications, including groundwater management and waste disposal planning, collectively represent 20% of the market. In 2024, over 60% of Gen Z engineers demonstrated higher trust in companies using AI-driven geomechanical systems.

North America accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

North America leads with over 220 operational geomechanical software deployments across oil, gas, and civil construction sectors, while Asia-Pacific is rapidly adopting cloud-based and AI-driven platforms. Europe accounted for 25% of adoption in 2024, and South America and Middle East & Africa combined hold approximately 18% of market utilization. Infrastructure development projects in India and China are driving demand for predictive modeling, while advanced AI-integrated software in the U.S. reduces non-productive time by 12–15%. By 2026, over 60% of civil engineering firms in Germany and France are expected to implement advanced geomechanics software for tunnel and slope stability projects.

How is digital transformation reshaping enterprise adoption in critical infrastructure?

North America accounts for 42% of the global geomechanics software and services market, with high adoption in oil, gas, and civil engineering sectors. Regulatory mandates for safety and environmental compliance have accelerated software integration, while government incentives support technology modernization. Leading companies, such as Schlumberger, are deploying AI-enabled predictive models to enhance wellbore stability across more than 200 active sites. Technological trends include cloud-based collaboration platforms and real-time monitoring, enabling enterprises to reduce operational downtime by 12%. Consumer behavior indicates higher adoption in healthcare, finance, and energy infrastructure, emphasizing accuracy and compliance in subsurface analysis.

Why is regulatory compliance driving advanced geomechanical adoption in European industrial projects?

Europe accounts for 25% of the geomechanics software and services market, with Germany, the UK, and France as key contributors. Stricter regulations and sustainability mandates have increased the need for explainable and precise geomechanical modeling. Emerging technologies such as AI-driven simulations and IoT-integrated monitoring platforms are widely implemented. Local players, including Itasca Consulting Group Europe, are expanding consulting and software services to support mining and tunnel projects. Regional consumer behavior is driven by compliance requirements and regulatory pressure, resulting in higher adoption in civil engineering and infrastructure sectors.

How are infrastructure expansion and AI integration shaping adoption in high-growth economies?

Asia-Pacific accounts for approximately 20% of the market volume, with China, India, and Japan as top consumers. The growth is fueled by large-scale infrastructure projects, including high-speed rail, metro systems, and energy facilities. Technology hubs in Singapore and Tokyo are driving AI-powered geomechanical software adoption for predictive modeling and slope stability. Local players are deploying cloud-based platforms to optimize excavation and drilling projects. Consumer behavior shows strong adoption in e-commerce, mobile applications, and industrial construction, supporting digital-first geomechanical solutions.

How are energy and infrastructure projects driving regional adoption?

South America holds approximately 10% of the geomechanics software and services market, with Brazil and Argentina as leading contributors. Demand is largely driven by infrastructure development and energy sector expansions. Government incentives, including tax reductions and project subsidies, support technology adoption. Local players are integrating AI and cloud-based platforms to optimize construction and mining projects. Regional consumer behavior reflects demand tied to energy production efficiency and localized engineering solutions for urban development projects.

What are the emerging trends in oil, gas, and construction technology adoption?

Middle East & Africa account for roughly 8% of the market, led by UAE and South Africa. The region is witnessing modernization in oil and gas infrastructure and urban construction projects. Technological adoption includes AI-driven predictive modeling and cloud-based monitoring systems. Local regulations and trade partnerships encourage compliance and technology upgrades. Regional players are implementing real-time geomechanical analysis for drilling operations, while consumer behavior trends indicate focus on operational efficiency and safety in high-risk industrial projects.

United States | Market Share: 42% | High adoption in oil, gas, and civil construction, supported by regulatory compliance and advanced predictive modeling solutions.

Germany | Market Share: 12% | Strong demand driven by infrastructure projects, regulatory mandates, and early adoption of AI-based geomechanical software.

The Geomechanics Software and Services market is moderately fragmented, with over 45 active competitors operating globally. The top five players—Schlumberger, Halliburton, Baker Hughes, Ikon Science, and Itasca Consulting Group—collectively hold approximately 58% of the market share, demonstrating a strong influence while leaving ample opportunity for niche players and regional specialists. Competition is largely driven by technological innovation, strategic partnerships, and service differentiation. For instance, several companies have recently launched AI-enabled predictive modeling platforms and cloud-based geomechanical solutions to enhance operational efficiency and reduce downtime. Mergers and collaborations between software developers and engineering service providers are accelerating the adoption of integrated solutions in oil, gas, mining, and civil construction sectors. North America continues to dominate in market adoption, while Asia-Pacific and Europe are rapidly increasing software deployments, leading to intensified regional competition. The introduction of real-time monitoring systems, machine learning analytics, and sustainability-focused features is further raising competitive intensity, with more than 60% of new product launches incorporating at least one advanced technology module.

Ikon Science

Itasca Consulting Group

Rocscience

Geocomp Corporation

Bentley Systems

Rocscience Asia

CGG GeoSoftware

The Geomechanics Software and Services market is being transformed by advancements in technology, particularly the integration of artificial intelligence (AI) and machine learning (ML) into geomechanical modeling. These technologies enable real-time analysis of subsurface conditions, allowing for more accurate predictions and optimized decision-making. Cloud computing adoption has further enhanced the storage and processing of large geotechnical datasets, facilitating collaboration across global teams. IoT sensors are increasingly used for continuous monitoring of geomechanical parameters such as soil pressure, temperature, and moisture content. Real-time feedback from these sensors allows companies to assess the stability of critical structures including tunnels, dams, and mines, enabling proactive maintenance and risk mitigation. Integration of IoT data with geomechanical software ensures precise monitoring and informed decision-making in high-stakes projects.

Advanced computational modeling tools have also emerged, capable of simulating complex geological formations and predicting material behavior under diverse stress conditions. These tools improve infrastructure design, safety, and operational efficiency. The combination of AI, IoT, cloud computing, and sophisticated simulations is redefining geomechanical analysis, promoting innovation, and supporting strategic decision-making across industries. Overall, these technological insights highlight how digital transformation and automation are enhancing accuracy, efficiency, and risk management in geomechanical projects worldwide.

In June 2024, a leading geomechanics software provider launched a new AI-powered platform to optimize wellbore stability in shale gas reservoirs. The platform integrates real-time analytics to predict failures, reducing downtime by 15%.

In August 2024, a major construction firm partnered with a geomechanics service company to implement a cloud-based monitoring system for tunnel excavation projects. IoT sensors provided real-time feedback, enhancing safety protocols and reducing project delays by 20%.

In October 2024, a mining corporation adopted an advanced geomechanics software suite incorporating machine learning algorithms to predict rock behavior under varying stress conditions, improving operational efficiency by 10%.

In December 2024, a government agency in a seismic zone implemented geomechanics services to assess infrastructure stability. The data informed retrofitting decisions, potentially preventing structural failures.

The Geomechanics Software and Services Market Report provides a comprehensive analysis of market segments, including software types, service offerings, applications, and geographic regions. Software solutions are assessed by adoption rates, with emphasis on standalone packages and integrated platforms, while services cover consulting, integration, and technical support. Applications span oil and gas, mining, civil construction, and nuclear waste disposal, highlighting evolving industry demands. The report details real-time data analytics and predictive modeling adoption in oil and gas projects to enhance drilling efficiency and safety. It also examines civil engineering use cases such as tunnel and slope stability, emphasizing regulatory compliance and operational safety.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional trends such as rapid adoption in Asia-Pacific due to infrastructure growth and stringent European regulations promoting advanced software deployment. Emerging technologies like AI, machine learning, IoT, and cloud computing are analyzed for their impact on accuracy, efficiency, and decision-making in geomechanics. The report also identifies niche and emerging market segments, providing a forward-looking perspective on technological adoption and market expansion.

Overall, the report equips decision-makers with actionable insights into market trends, technological advancements, regional dynamics, and strategic opportunities across the global geomechanics software and services industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1590.54 Million |

|

Market Revenue in 2032 |

USD 2459.56 Million |

|

CAGR (2025 - 2032) |

5.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Schlumberger, Halliburton, Baker Hughes, Ikon Science, Itasca Consulting Group, Rocscience, Geocomp Corporation, Bentley Systems, Rocscience Asia, CGG GeoSoftware |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |