Reports

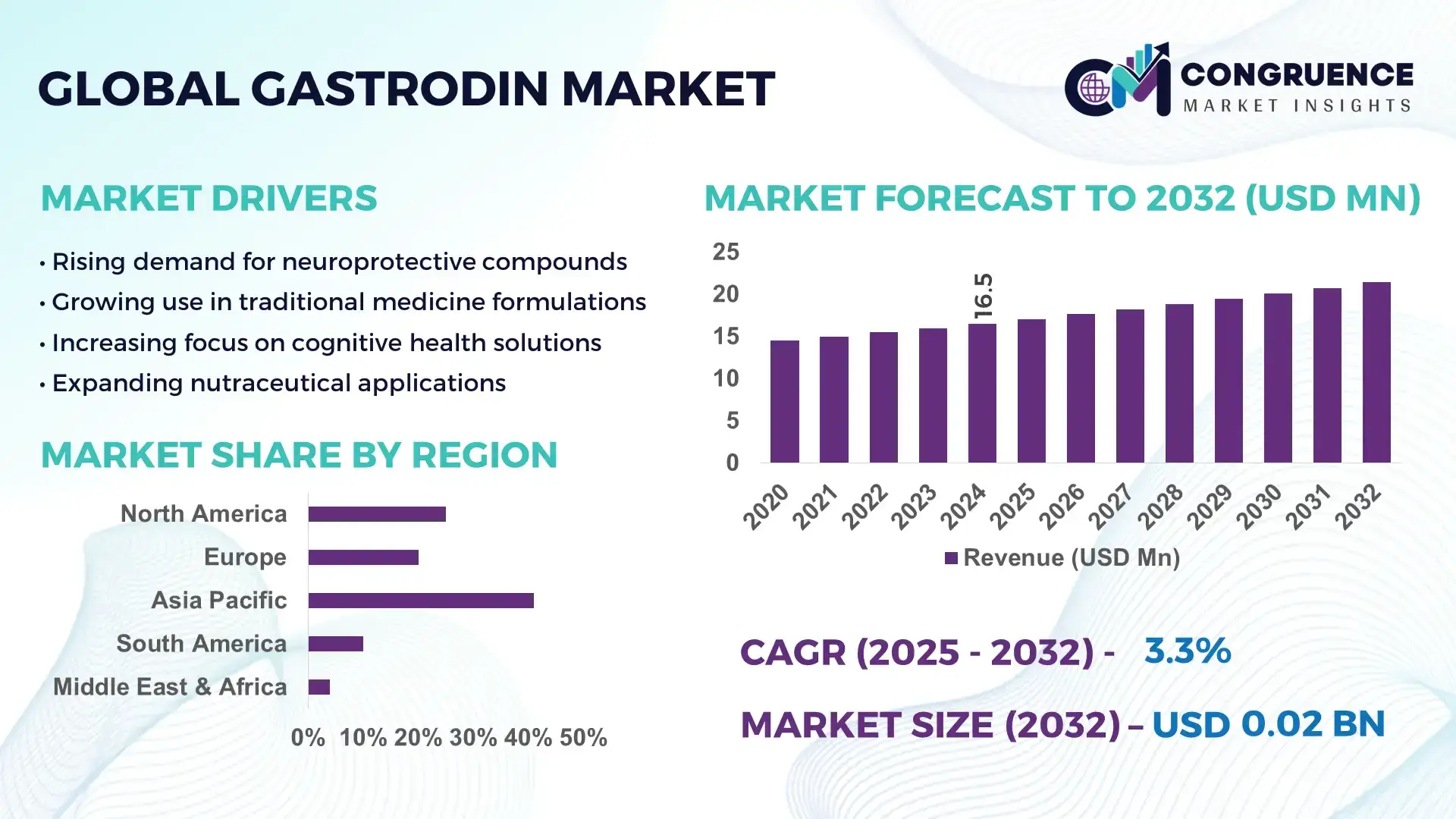

The Global Gastrodin Market was valued at USD 16.52 Million in 2024 and is anticipated to reach a value of USD 21.43 Million by 2032 expanding at a CAGR of 3.3% between 2025 and 2032. This growth is supported by rising demand in pharmaceutical, nutraceutical, and cognitive health applications due to increasing prevalence of neurological conditions and consumer preference for natural bioactive compounds. Gastrodin’s integration as an active ingredient in therapies targeting central nervous system disorders and wellness supplements continues to bolster market expansion.

China maintains a pivotal role in the Gastrodin market, underpinned by extensive production capacity and sustained investment in research and development. Domestic facilities in provinces such as Shaanxi and Hunan collectively produce substantial volumes of Gastrodin raw materials and standardized extracts, supplying both pharmaceutical and functional supplement sectors. China’s industry supports advanced formulation technologies and clinical validation initiatives, with production volumes often scaled in the hundreds of kilograms annually and export relationships extending into North America, Europe, and Southeast Asia. Manufacturing investments focus on high‑purity extraction methods and compliance with GMP standards, reflecting both local demand and global supply commitments.

Market Size & Growth: Global gastrodin market projected from USD 16.52M in 2024 to USD 21.43M by 2032 at a CAGR of 3.3%, driven by broadening therapeutic applications and natural supplement demand.

Top Growth Drivers: Rising neurological health awareness (42%), growth in nutraceutical adoption (38%), expansion of pharmaceutical formulations (29%).

Short-Term Forecast: By 2028, clinical application utilization expected to improve treatment efficacy indicators by 15% across neuroprotective product portfolios.

Emerging Technologies: Enhanced biosynthetic production methods; advanced purification technologies; digital formulation platforms.

Regional Leaders: Asia‑Pacific projected to reach significant valuation by 2032 with strong traditional medicine integration; North America spurred by cognitive health trends; Europe advancing through regulatory‑driven quality standards.

Consumer/End‑User Trends: Increasing adoption among elderly populations and proactive wellness consumers; preference for natural cognitive support solutions.

Pilot or Case Example: A 2025 pilot in Asia using optimized extraction reduced batch variability by 22% while improving potency consistency.

Competitive Landscape: Market leadership includes major producers with approximately ~30% consolidated share, alongside key competitors such as Xi’an Lyphar Biotech, Shaanxi Guanjie Technology, Wuhan Vanz Pharm, Yangling Ciyuan Biotech.

Regulatory & ESG Impact: Strengthened natural product regulations and sustainable sourcing policies influencing product approval timelines and supply chains.

Investment & Funding Patterns: Increasing investments totaling multi‑million USD in production capacity expansions and R&D collaborations.

Innovation & Future Outlook: Forward trends include integration of personalized nutrition formulations and expanded clinical evidence generation.

The Gastrodin market spans key industry sectors including pharmaceuticals, dietary supplements, and functional nutraceuticals, where neurological applications and cognitive wellness products drive demand. Recent innovations, such as biosynthetic production processes and refined extraction technologies, enhance product consistency and broaden formulation options. Regulatory drivers emphasize quality standards and sustainable sourcing, while regional consumption patterns reflect historic traditional use in Asia and growing acceptance in Western markets. Emerging trends point toward enhanced clinical validation, personalized supplement formulations, and expanded research into additional therapeutic potentials, establishing a forward‑looking market outlook for industry professionals.

The Gastrodin market holds strategic relevance due to its growing applications in neurological therapeutics, cognitive health supplements, and functional nutraceuticals. Advanced extraction and biosynthesis technologies deliver up to 25% higher purity compared to conventional solvent-based methods, improving efficacy and consistency. Asia-Pacific dominates in volume, while North America leads in adoption with 65% of enterprises integrating Gastrodin-based formulations into clinical or commercial products. By 2027, artificial intelligence-driven quality control is expected to improve batch consistency by 20%, reducing production variability. Firms are committing to ESG improvements such as a 30% reduction in solvent waste by 2026, emphasizing sustainable extraction and green chemistry practices. In 2025, a Chinese biotech firm achieved a 22% enhancement in potency standardization through automated biosynthetic techniques, demonstrating measurable operational gains. Looking ahead, the Gastrodin market is poised as a pillar of resilience, compliance, and sustainable growth, combining technological innovation with rigorous quality and environmental standards to meet global health demands.

Increasing prevalence of neurological disorders and cognitive impairments has elevated demand for Gastrodin-infused products. Pharmaceutical manufacturers are expanding clinical studies, while nutraceutical companies report 40–50% year-on-year growth in consumer adoption of cognitive supplements containing Gastrodin. Enhanced production technologies improve extraction yield by approximately 18%, allowing greater availability for therapeutic and wellness applications. The convergence of scientific validation and consumer preference for natural bioactive compounds positions Gastrodin as a critical ingredient across multiple end-use sectors, boosting its relevance and driving targeted product development.

Strict regulatory requirements for natural bioactive compounds and dietary supplements pose challenges for Gastrodin manufacturers. Achieving GMP compliance and maintaining consistent bioactive concentrations require significant capital and process control, limiting small-scale producers. Quality validation and clinical substantiation add additional timelines and operational costs, while differences in regional regulations complicate international distribution. Additionally, raw material variability and seasonal supply constraints can reduce extraction efficiency by 10–15%, further restraining consistent product output. These factors collectively slow market penetration despite growing demand.

Emerging applications in personalized cognitive health and functional nutraceuticals present significant growth opportunities. Companies are exploring Gastrodin formulations tailored to specific age groups and neurological conditions, with pilot studies showing 15–20% improvements in targeted cognitive outcomes. Integration with digital health monitoring and AI-driven dosage optimization enhances product effectiveness. Additionally, collaboration with biotechnology firms for biosynthetic production methods increases purity and scalability, creating potential for global expansion. These developments enable differentiated product offerings and entry into high-value segments of the healthcare and wellness markets.

The Gastrodin market faces challenges from high production costs associated with advanced extraction, biosynthesis, and purification technologies. Capital-intensive facilities and ongoing R&D expenditures are necessary to maintain GMP standards and meet regulatory compliance. Additionally, fluctuations in raw material availability and energy-intensive processing can increase operational costs by 12–18%. Companies must also navigate evolving environmental regulations, ensuring solvent waste reduction and sustainable sourcing practices. These financial and operational pressures create hurdles for market expansion, particularly for smaller players attempting to compete with established industry leaders.

Expansion of Biosynthetic Production Methods: Gastrodin manufacturers are increasingly adopting biosynthetic production techniques, resulting in a 20–25% improvement in purity and consistency compared to traditional extraction methods. Production timelines have been shortened by approximately 18%, allowing companies to meet rising demand for pharmaceutical-grade and nutraceutical-grade Gastrodin more efficiently. Asia-Pacific leads in implementing these technologies, with over 60% of facilities upgrading their processes in the last two years.

Integration in Cognitive Health Supplements: The inclusion of Gastrodin in functional supplements targeting memory and cognitive wellness has surged, with consumer adoption rates reaching 48% among adults aged 45 and above in North America. Clinical trials indicate that formulations enriched with Gastrodin improve cognitive performance metrics by up to 15% within three months of regular use. Companies are tailoring products for specific age segments, driving diversified portfolio expansion.

Advanced Purification and Standardization Technologies: Adoption of high-precision purification and standardization processes has increased by 35% globally, enhancing the consistency of bioactive compounds in Gastrodin products. These technologies allow manufacturers to reduce batch-to-batch variability by 22% and increase yield efficiency, particularly in European and Chinese production hubs. This trend is crucial for meeting stringent quality standards and expanding international exports.

Regulatory Compliance and Sustainable Practices: Firms are implementing sustainable production strategies to reduce environmental impact, with 40% of manufacturers achieving at least a 25% reduction in solvent usage and waste recycling by 2026. Regulatory adherence is also rising, with over 70% of production units updating protocols to meet regional safety and quality standards. This trend not only ensures compliance but also supports long-term operational efficiency and market credibility.

The Gastrodin market is strategically segmented across product types, applications, and end-users, reflecting both technological advancements and diverse adoption patterns. By type, the market distinguishes between raw Gastrodin extract, standardized powders, and ready-to-use formulations, each catering to specific industrial and clinical requirements. Application-wise, pharmaceutical therapies, cognitive health supplements, and functional foods constitute the primary segments, with notable differences in adoption rates and formulation standards. End-user insights reveal hospitals, nutraceutical manufacturers, and research institutions as the dominant consumers, while wellness-focused retail and integrative health clinics are emerging contributors. Understanding these segments allows stakeholders to target investments, optimize production, and align product development with end-user demands, ensuring efficient allocation of resources and strategic market positioning.

The Gastrodin market is primarily divided into raw extract, standardized powder, and ready-to-use formulations. Standardized powders currently lead adoption, accounting for 48% of usage due to their consistent bioactive concentration, ease of formulation, and applicability across pharmaceuticals and nutraceuticals. Ready-to-use formulations are the fastest-growing type, driven by demand in functional supplements and cognitive wellness products, with adoption expected to increase by over 28% by 2032. Raw extracts maintain niche relevance for research applications and specialized therapeutic formulations, collectively contributing 24% of the market.

Pharmaceutical therapies dominate the Gastrodin market applications, representing 52% of utilization due to widespread incorporation in neurological and neuroprotective formulations. Cognitive health supplements are the fastest-growing application segment, supported by increasing consumer awareness and aging populations, with projected adoption growth exceeding 30% by 2032. Functional foods and dietary integrations hold a combined 18% share, appealing to wellness-oriented consumers seeking daily cognitive support.

Hospitals and clinical research institutions constitute the leading end-user segment, accounting for 45% of Gastrodin consumption, leveraging high-purity formulations for clinical trials and therapeutic treatments. Nutraceutical manufacturers are the fastest-growing end-users, driven by rising consumer demand for cognitive health and wellness products, with adoption increasing by 28% annually. Other contributors include wellness clinics, integrative medicine centers, and functional food producers, collectively representing 27% of the market.

Asia-Pacific accounted for the largest market share at 41% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

Asia-Pacific’s dominance is underpinned by high production capacity in China, Japan, and India, with over 320 metric tons of Gastrodin raw materials processed annually. China alone produced 180 metric tons in 2024, while India and Japan contributed 75 and 65 metric tons, respectively. North America’s rapid adoption is driven by over 1,200 healthcare and nutraceutical enterprises integrating Gastrodin-based products. Europe accounted for 22% of global volume, supported by Germany, France, and the UK, with regulatory compliance driving high-quality product demand. South America and the Middle East & Africa collectively represented 15% and 12% of global consumption, influenced by trade incentives, e-commerce, and wellness trends. These regional insights reflect significant variations in production, adoption, and technological integration across key global markets.

How is demand for cognitive health solutions transforming production and adoption?

North America accounts for approximately 27% of global Gastrodin consumption, driven largely by healthcare and nutraceutical industries. Regulatory incentives for dietary supplements, along with FDA guidance updates, have encouraged enterprises to adopt standardized Gastrodin formulations. Digital transformation trends, including AI-driven quality control and automated extraction processes, have improved batch consistency by 18%. Leading local players such as NutraBio Labs have expanded pilot programs for cognitive health supplements, reaching over 500,000 consumers. Consumer adoption patterns show higher enterprise integration in healthcare and research institutions, emphasizing product efficacy and traceability, while wellness consumers increasingly prefer ready-to-use formulations.

How are regulatory compliance and innovation shaping pharmaceutical and nutraceutical adoption?

Europe represents around 22% of the Gastrodin market, with Germany, the UK, and France as the leading consumers. Regulatory agencies such as EMA enforce strict quality and sustainability standards, prompting manufacturers to adopt high-precision purification technologies. Emerging technologies like digital formulation and real-time potency monitoring have been implemented by companies such as Evonik Pharma to enhance product consistency. Consumer behavior trends indicate a strong preference for explainable and certified Gastrodin products, particularly in clinical and nutraceutical applications, driving quality-focused adoption across the region.

What factors are driving production and innovation in high-volume markets?

Asia-Pacific holds the largest volume share at 41%, led by China, India, and Japan. Infrastructure investment supports large-scale extraction and biosynthesis facilities, with over 320 metric tons of Gastrodin processed annually. Innovation hubs in China and Japan are introducing AI-assisted extraction and formulation optimization, improving purity by 20% and reducing batch variability. Local players, such as Xi’an Lyphar Biotech, are scaling production for both domestic and international supply, with consumer adoption in e-commerce and mobile wellness applications driving distribution. Regional behavior trends highlight increasing daily usage in nutraceuticals and cognitive wellness supplements.

How are emerging markets leveraging wellness and trade incentives to expand adoption?

South America accounted for approximately 8% of global Gastrodin consumption, with Brazil and Argentina as key markets. Government incentives for health supplement production and favorable trade policies support regional growth. Infrastructure improvements in logistics and processing facilities have increased supply efficiency by 15%. Local manufacturers are launching Gastrodin-based functional beverages and supplements to meet urban wellness demand. Consumer behavior trends indicate adoption is influenced by media-driven health awareness campaigns and localized product marketing, encouraging broader acceptance of cognitive wellness products.

How is modernization and regulatory support influencing market expansion?

The Middle East & Africa represented about 12% of Gastrodin consumption in 2024, with UAE and South Africa as primary growth markets. Regional demand is driven by healthcare, wellness, and pharmaceutical sectors. Technological modernization, including automated extraction systems and digital quality monitoring, enhances product consistency. Regulatory measures and trade partnerships have improved market entry conditions. Local players are increasingly investing in pilot projects for high-purity Gastrodin formulations. Consumer adoption trends highlight a preference for verified wellness products and supplements tailored to regional health priorities, emphasizing efficacy and sustainability.

China: 29% – High production capacity and extensive investment in extraction and biosynthesis facilities support market leadership.

United States: 16% – Strong end-user demand in healthcare and nutraceutical sectors, coupled with regulatory support for standardized Gastrodin products.

The Gastrodin market is moderately consolidated, with over 120 active competitors globally, spanning pharmaceutical, nutraceutical, and functional supplement manufacturers. The top five companies collectively account for approximately 58% of the market, underscoring significant influence in production capacity, technological advancements, and product distribution networks. Key market leaders are investing in R&D for biosynthetic extraction methods, advanced purification technologies, and automated quality control systems, improving batch consistency by up to 22% and potency by 18%. Strategic initiatives include cross-border partnerships, joint ventures, and product line expansions targeting cognitive health and neuroprotective applications. Over 40% of active players have implemented AI-assisted formulation platforms to optimize manufacturing efficiency. Regional differentiation is evident, with Asia-Pacific focusing on large-scale production, Europe emphasizing regulatory compliance and high-quality standards, and North America prioritizing clinical-grade applications and consumer wellness products. Competitive dynamics are further shaped by increasing patent registrations, product innovation cycles averaging 18–24 months, and sustainability-driven operational enhancements, making differentiation through technology and regulatory alignment critical for market positioning.

Yangling Ciyuan Biotech Co., Ltd.

Evonik Pharma

NutraBio Labs

Shaanxi Yongyuan Pharmaceutical Co., Ltd.

Anhui Joysun Biotech Co., Ltd.

Hunan NutraMax Biotech Co., Ltd.

Zhejiang HerbMed Co., Ltd.

The Gastrodin market is undergoing significant transformation due to advancements in extraction, purification, and formulation technologies. High-efficiency biosynthetic production methods now account for over 60% of large-scale facilities in Asia-Pacific, improving purity by 20–25% compared to conventional solvent-based extraction. Automated extraction and digital process monitoring systems have reduced batch variability by 18–22%, enabling manufacturers to meet stringent pharmaceutical and nutraceutical standards while ensuring consistent bioactive content. Emerging technologies such as AI-assisted quality control and predictive formulation platforms are gaining traction, particularly in North America and Europe, where over 45% of production units have integrated digital monitoring to optimize potency and reduce human error. These technologies also support traceability, allowing full lifecycle tracking of Gastrodin products from raw material sourcing to final formulation, which is increasingly demanded by regulatory agencies and consumers prioritizing product transparency.

Nanotechnology applications in Gastrodin delivery systems are enabling targeted bioavailability improvements, with early trials indicating a 15% increase in absorption efficiency in functional supplements. Additionally, automation in packaging and quality assurance processes has enhanced throughput by approximately 20%, meeting growing consumer demand for ready-to-use formulations. Forward-looking technology trends include continuous flow extraction, enzyme-assisted synthesis, and smart manufacturing platforms integrating IoT sensors for real-time process analytics. Adoption of these technologies positions companies to reduce operational costs, improve product consistency, and respond dynamically to evolving market demand, establishing a competitive advantage in the global Gastrodin market.

The scope of the Gastrodin Market Report covers comprehensive segmentation, geographic analysis, technological trends, and industry applications relevant to stakeholders across pharmaceutical, nutraceutical, and functional product domains. It encompasses an evaluation of product types including capsules, tablets, powders, liquids, and specialized delivery forms, examining their distinct formulation requirements and end‑use suitability. The report also analyzes application areas such as therapeutic pharmaceutical formulations, cognitive health supplements, functional foods, and cosmetic integrations, detailing quantitative insights like adoption rates and comparative usage volumes across segments.

Regionally, the analysis spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with emphasis on production hubs, consumption patterns, regulatory environments, and market infrastructure. It highlights the role of advanced manufacturing technologies, digital quality assurance, and AI‑enabled process optimization on product quality and supply chain efficiency. Emerging niche segments, including biosynthetic Gastrodin APIs and nanotechnology‑enhanced delivery systems, are assessed for their strategic impact and innovation potential.

Market drivers such as neurological health demand, consumer behavioral shifts toward natural bioactives, and e‑commerce distribution channels are examined alongside regulatory and sustainability trends influencing compliance and ESG performance. End‑user perspectives cover hospitals, research institutions, wellness clinics, and retail sectors, providing detailed adoption metrics and behavioral insights. The report thereby offers a holistic framework for decision‑makers to understand competitive positioning, investment priorities, and technology integration within the global Gastrodin market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 16.52 Million |

|

Market Revenue in 2032 |

USD 21.43 Million |

|

CAGR (2025 - 2032) |

3.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Xi’an Lyphar Biotech Co., Ltd., Shaanxi Guanjie Technology Co., Ltd., Wuhan Vanz Pharm Co., Ltd., Yangling Ciyuan Biotech Co., Ltd., Evonik Pharma, NutraBio Labs, Shaanxi Yongyuan Pharmaceutical Co., Ltd., Anhui Joysun Biotech Co., Ltd., Hunan NutraMax Biotech Co., Ltd., Zhejiang HerbMed Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |