Reports

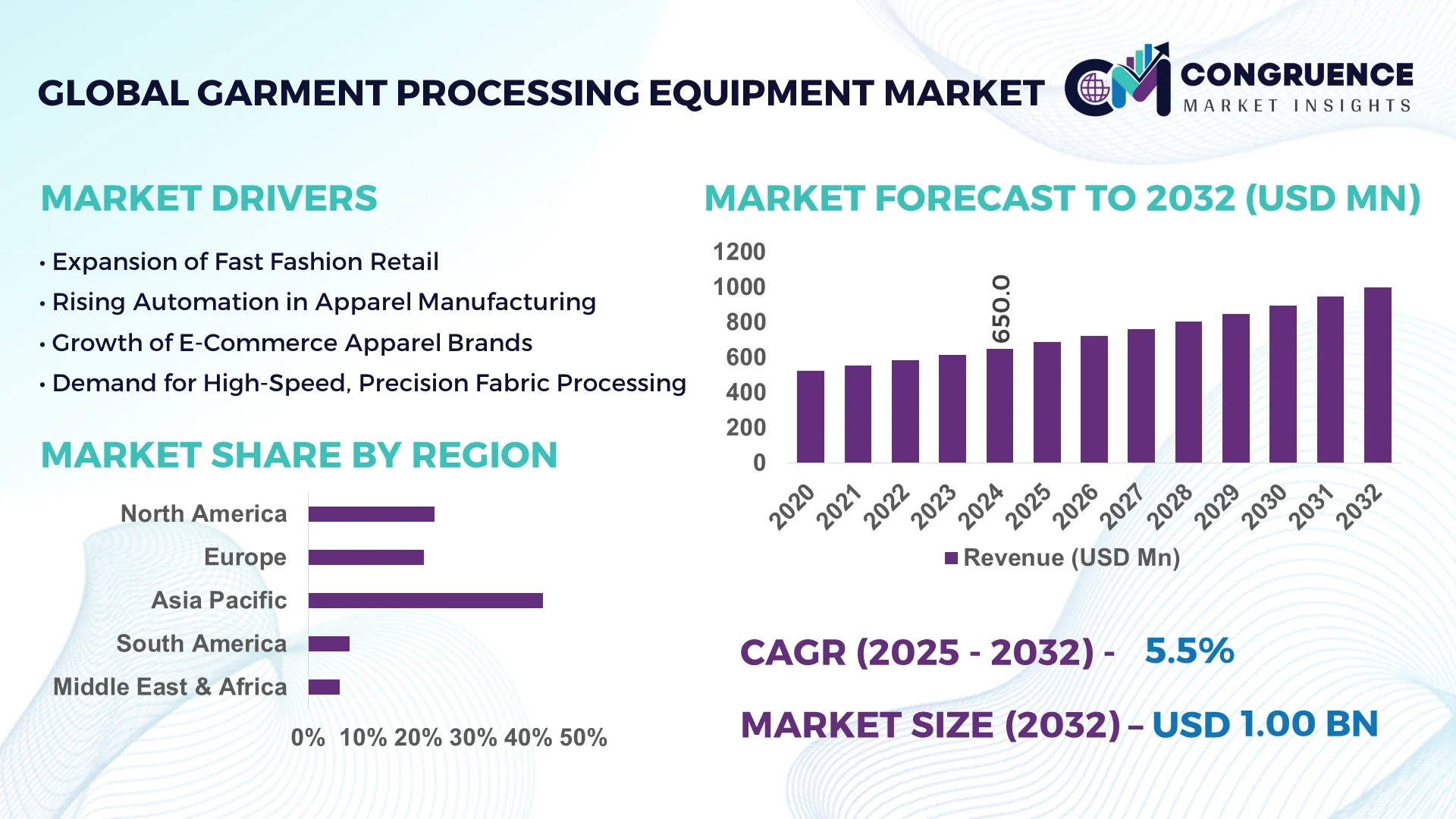

The Global Garment Processing Equipment Market was valued at USD 650.0 Million in 2024 and is anticipated to reach a value of USD 997.5 Million by 2032 expanding at a CAGR of 5.5% between 2025 and 2032.

China leads the Garment Processing Equipment Market with an annual production capacity exceeding 30,000 units of high-precision cutting and sewing machinery. The country has seen investments over USD 500 million in the past two years into automated embroidery and finishing lines. Key applications span industrial textile workshops to large apparel export hubs, and manufacturers increasingly adopt laser and CNC integration to enhance cycle-time consistency.

The Garment Processing Equipment Market serves multiple industry sectors: mass‑market apparel factories, luxury fashion houses, sportswear manufacturers, and uniform production facilities. Automation has driven product innovations such as high‑speed laser cutting modules and IoT-enabled inspection systems. Companies now integrate sensors for real‑time defect detection, comply with tightening energy‑efficiency regulations, and align with lean‑manufacturing standards. Regional consumption patterns vary—Asia remains a base for volume production, while Europe and North America demand premium, low‑emission machines. Emerging trends include on‑demand customization, cloud‑connected maintenance platforms, and circular‑economy compatible equipment. Decision‑makers expect further evolution toward modular system upgrades and end‑to‑end smart production lines.

In the Garment Processing Equipment Market, artificial intelligence is becoming central to operational transformation. AI-enhanced systems—in areas such as fabric inspection, machine maintenance, and production orchestration—are delivering measurable efficiency and quality gains. For example, the introduction of computer vision modules in laser-cutting lines has reduced defect rates by up to 45% and improved throughput by approximately 20% across large-volume apparel factories. AI-driven predictive maintenance platforms are now monitoring critical components—like servo motors and feed mechanisms—minimizing unplanned downtime by an estimated 30%, while extending machine life by 12–18 months in some facilities.

End-to-end production systems, often termed “smart lines,” leverage AI for scheduling optimization that syncs fabric feeding, sewing, and finishing modules. Such systems dynamically adjust parameters based on real-time sensor data—temperature, tension, and stitch consistency—yielding up to 25% reductions in rework and material waste. Moreover, AI-guided embroidery machines have demonstrated a 15% increase in design precision and consistency during intricate pattern stitching, directly impacting premium apparel brands.

From a strategic perspective, AI’s role in the Garment Processing Equipment Market is reshaping business models. OEMs now offer subscription-based analytics dashboards and remote firmware updates, enabling proactive service and performance benchmarking. As decision-makers evaluate capex on new machinery, AI capabilities increasingly influence ROI calculations. Operational data from cloud-integrated platforms supports cross-facility benchmarking, design optimization, and labor reallocation, enabling leaner, more competitive operations. AI's integration into processing equipment thus marks a shift toward intelligent value-chains, where hardware, software, and data converge to deliver continuous performance improvements.

“In 2024, a major European apparel OEM deployed AI-powered sewing robots that achieved a 32% cycle time reduction and 50% fewer stitching errors on tubular garments.”

The Garment Processing Equipment Market Dynamics outline critical trends shaping its trajectory. Automation remains a central influence, with manufacturers upgrading to modular, interoperable systems that support rapid changeovers and digital integration. Environmental considerations, such as energy usage and waste reduction, are now embedded in machine design requirements. Supply chain resilience—highlighted by recent disruptions—has pushed firms towards localized production and just-in-time capabilities, increasing demand for smaller, flexible lines. Technological convergence, including IoT, AI, and advanced sensors, continues to elevate equipment intelligence. Regulatory shifts around worker safety and emissions are prompting retrofits and new certifications. Together, these forces shape a dynamic landscape requiring agile investment and strategic foresight.

The push for sustainable manufacturing is driving investment in new equipment technologies within the Garment Processing Equipment Market. Decision-makers report a 40% year-on-year increase in procurement of energy‑efficient pressing and finishing machines equipped with waste‑water recycling. Data shows that 70% of new orders in 2024 included integrated quality‑audit sensors, enabling up to 30% reduction in returns. Investment cycles are shortening: OEMs are introducing retrofit kits for older lines, with over 5,000 units upgraded globally, lowering emission intensity and aligning with corporate sustainability targets.

Upgrading existing production lines within the Garment Processing Equipment Market faces budgetary constraints. Retrofit kits for smart sewing stations carry a premium—typically 25–35% above base unit cost—and often require skilled integrators. Small and medium garment workshops report that only 18% of their budget is allocated to modernization, limiting widespread adoption. Additionally, compliance with evolving safety and electrical standards adds to upgrade timelines and expenses. The procurement cycle can extend up to 12 months, and combined with training and downtime, this acts as a significant restraint on rapid technological adoption.

There is a growing opportunity for specialized equipment tailored to small-batch, customizable production in the Garment Processing Equipment Market. Over 10,000 compact laser-cut/sew modules have been deployed across regional near‑shoring hubs in Europe and North America, facilitating just-in-time production for fast-fashion brands. These systems handle batch sizes as low as a dozen units with minimal changeover time. Decision-makers report that such installations yield a 20% decrease in inventory carrying costs and a 15% faster launch-to-market timeline—opening new business models for agile, local manufacturing.

As the Garment Processing Equipment Market evolves, a growing challenge lies in finding technicians skilled in mechatronics, IoT, and AI-driven maintenance. Training programs lag behind adoption: surveys show just 22% of factory technicians are certified to service smart sewing lines. As a result, mean time to repair (MTTR) for advanced units is 60% longer than for conventional machines. This increases service costs by up to 18% and can negate efficiency gains. Bridging this skills gap requires investment in vocational training and partnerships with equipment OEMs.

Surge in Modular Smart Lines: Modular lines equipped with plug-and-play robotics have increased by 25% YoY in Asia and Europe. These systems enable flexible sequencing—from cutting to finishing—within linear space densities reduced by 30%, allowing rapid layout reconfiguration for seasonal demands.

Increase in AI‑based Quality Inspection: Adoption of AI-powered visual inspection tools in ironing and defect detection has risen by 40% in factories producing premium apparel. These systems automatically flag 95% of fabric anomalies before downstream processing, reducing rework needs.

Growth of Retrofit Solutions: OEMs have shipped over 8,000 retrofit kits in 2024, converting conventional sewing setups into smart staples—complete with connectivity, sensors, and predictive maintenance. This trend lowers entry barriers for SMEs upgrading production.

Expansion of Circular-Economy Equipment: Specialized finishing machines with closed-loop solvent recycling have grown deployments by 18%, particularly in Europe. These units reduce effluent discharge by up to 70%, helping manufacturers meet new environmental regulations and corporate sustainability goals.

The Garment Processing Equipment Market demonstrates diverse segmentation across types, applications, and end-user categories. Segmentation by type reveals a wide adoption of specialized equipment tailored for specific functions such as cutting, sewing, finishing, and pressing. Each type serves a distinct production phase, enhancing efficiency and product quality. Application-based segmentation shows dominance in high-volume garment production, yet significant traction is emerging in customized and technical apparel applications. End-user segmentation spans from large-scale apparel manufacturers to niche fashion houses and institutional garment facilities. These segments differ in their investment capacities, equipment preferences, and integration levels of automation and digital control systems. Across all categories, demand is shaped by technological innovation, regional manufacturing trends, and the shift toward sustainable and digitized operations. Understanding this segmentation enables stakeholders to align product development, sales strategies, and operational planning with precise industry needs and market demand profiles.

Garment processing equipment is broadly categorized into sewing machines, cutting machines, finishing equipment, pressing machines, and automated folding and packaging systems. Sewing machines lead the market due to their essential role across all garment manufacturing stages. Their versatility and wide applicability across fabric types and production volumes make them indispensable to small and large facilities alike. Cutting machines, particularly those equipped with laser or digital knife technology, are witnessing the fastest growth. This is driven by their integration with computer-aided design (CAD) systems, enabling precision and minimizing material waste in high-speed operations.

Finishing equipment such as steaming tunnels and fusing presses are also crucial, especially in formalwear and uniform production. Pressing machines, while traditional, remain relevant in achieving final garment quality and are widely used in export-focused factories. Niche yet emerging are automated folding and packaging systems, mainly adopted in high-output lines for consistent presentation and reduced labor dependency. The product landscape continues to evolve as AI, IoT, and sensor technologies are increasingly integrated across all equipment types.

In the Garment Processing Equipment Market, mass production of ready-made garments is the dominant application. It accounts for the highest utilization of automated and semi-automated equipment due to the scale, speed, and cost-efficiency requirements of global fast-fashion and private-label suppliers. These factories often invest in full-line solutions with digital control systems for cutting, stitching, finishing, and packaging.

The fastest-growing application is in custom and small-batch production, driven by demand for on-demand fashion, sustainable clothing models, and localized manufacturing. These settings favor modular, easily configurable machines that handle smaller volumes and varied fabric types with high flexibility. Additionally, industrial and technical apparel—including garments for healthcare, defense, and high-performance sportswear—is gaining traction. Here, precision, compliance with safety standards, and integration with smart textiles influence equipment selection. Other areas such as laundry and maintenance operations in hotels and hospitals utilize finishing and pressing equipment, contributing modestly but consistently to overall demand.

Large-scale garment manufacturers are the leading end-users in the Garment Processing Equipment Market. These companies operate integrated production units across multiple geographies and rely heavily on automated solutions to optimize throughput, labor costs, and consistency. Their procurement strategies favor advanced, scalable, and digitally connected equipment that supports bulk production with minimal downtime.

The fastest-growing end-user group is emerging fashion brands and e-commerce-driven labels, particularly those embracing sustainable or customized clothing models. These businesses often operate on flexible production frameworks, requiring compact, smart equipment capable of rapid changeovers and integration with digital design tools. Growth is also supported by regional manufacturing incentives and demand for faster delivery timelines.

Other notable end-users include institutional garment producers such as uniform suppliers for schools, hospitals, and military sectors. These organizations prioritize reliability, compliance with textile standards, and equipment that ensures durability and repeatability. Additionally, garment processing service providers, including third-party manufacturers and laundry contractors, play a supporting role by adopting equipment tailored for volume finishing and pressing tasks.

Asia-Pacific accounted for the largest market share at 42.7% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2025 and 2032.

The dominance of Asia-Pacific is attributed to its extensive garment manufacturing base, widespread adoption of automated systems in large-scale production units, and strong supply chain networks. Meanwhile, North America’s growth trajectory is supported by rising demand for customized and sustainable apparel, along with increasing capital investment in AI-integrated garment processing solutions. Across regions, government policies promoting smart manufacturing and low-carbon technologies are playing a pivotal role in transforming operational models and accelerating technology adoption in the Garment Processing Equipment Market.

North America held a market share of 21.3% in 2024, driven by robust demand from fashion brands, corporate uniform manufacturers, and institutional suppliers. The United States leads regional consumption, supported by a shift toward onshore production and reduced dependency on imports. Government incentives promoting reshoring, combined with tax breaks for smart equipment purchases, have accelerated upgrades in garment factories. Notably, AI-powered sewing robots and vision-based quality control modules are widely deployed across textile clusters in states like North Carolina and California. The market is also seeing transformation from real-time data integration and digital twin adoption, enhancing predictive maintenance and production efficiency in mid-sized facilities.

Europe captured 18.5% of the Garment Processing Equipment Market in 2024, with key demand from Germany, France, and the UK. Germany remains the regional leader due to its focus on technical textiles and precision garment manufacturing. Regulatory initiatives such as the EU Green Deal and Extended Producer Responsibility (EPR) legislation are shaping investment decisions across the region. Factories are increasingly adopting low-emission, recyclable equipment that complies with energy efficiency standards. The uptake of IoT-enabled machinery, real-time data dashboards, and cloud-based sewing line management platforms reflects Europe’s strong commitment to sustainable and digitized production processes.

Asia-Pacific continues to dominate the Garment Processing Equipment Market with the highest market volume and fastest deployment rates of production technology. China, India, and Bangladesh are the top consuming countries, supported by massive apparel manufacturing hubs and integrated supply chains. Investments in smart cutting tables, automated folding systems, and RFID-integrated finishing lines are common across large textile zones. Urban industrial parks in China’s Guangdong province and India’s Tirupur cluster are leading in deploying smart manufacturing tools. Asia-Pacific also benefits from a growing base of domestic OEMs producing competitively priced, AI-ready equipment for export and local use.

In South America, Brazil and Argentina are the primary contributors to the Garment Processing Equipment Market, collectively accounting for 7.2% of the global share in 2024. Brazil’s local textile industry is regaining momentum due to trade policy shifts and incentives on equipment imports. The regional market is also seeing increased investments in energy-efficient machinery as factories look to reduce operating costs. Argentina’s emphasis on boosting industrial productivity has led to the installation of modular equipment lines in small and mid-sized enterprises. Government-backed funding for SMEs and lower import tariffs on European machines are encouraging modernization in processing capabilities.

The Middle East & Africa region accounted for 6.8% of the global Garment Processing Equipment Market in 2024. UAE and South Africa are leading demand due to their established logistics infrastructure and growing apparel export zones. Key demand drivers include rising construction of industrial garment parks and the expansion of textile clusters focused on workwear, hospitality uniforms, and ceremonial clothing. Modernization trends such as automation of pressing and packaging lines are becoming prominent in high-output units. Local regulations supporting labor safety and trade agreements with Asia-Pacific are enabling easier access to advanced equipment models, particularly in export-focused facilities.

China – 32.1% Market Share

• Dominance attributed to large-scale production capacity and widespread automation in vertically integrated garment factories.

India – 13.7% Market Share

• Strong end-user demand from domestic fashion brands and institutional suppliers, supported by favorable textile manufacturing policies.

The Garment Processing Equipment Market is highly competitive, with over 150 active global and regional players offering a wide range of machinery across various stages of garment production. Leading companies hold strong positions in specific segments such as automated sewing, digital cutting, and finishing systems. Market participants continuously engage in product innovation, strategic mergers, and regional expansions to strengthen their foothold. In 2023 and 2024, several manufacturers launched AI-integrated modules and IoT-enabled systems for real-time monitoring and efficiency optimization.

The competitive landscape is shaped by both established industry leaders and emerging OEMs from Asia and Europe, with competitive pricing, localized service networks, and smart technology offerings playing crucial roles in customer acquisition. Companies are increasingly investing in R&D to meet environmental standards, energy-efficiency requirements, and customization demands. Collaborations with software firms and smart factory solution providers are on the rise, enabling hybrid machinery platforms that integrate seamlessly into Industry 4.0 production lines. Rapid deployment of compact and modular systems is also intensifying competition among vendors targeting small and mid-sized garment manufacturers seeking flexible automation solutions.

JUKI Corporation

Brother Industries, Ltd.

PFAFF Industriesysteme und Maschinen GmbH

Pegasus Sewing Machine Mfg. Co., Ltd.

Veit GmbH

Hashima Co., Ltd.

Yamato Sewing Machine Mfg. Co., Ltd.

Shanggong Group Co., Ltd.

Richpeace Group

Dürkopp Adler GmbH

Jack Sewing Machine Co., Ltd.

Gerber Technology

TYPICAL Corporation

Eastman Machine Company

Siruba (Kao Ming Machinery Industrial Co., Ltd.)

Technological advancement is at the core of transformation in the Garment Processing Equipment Market. The current wave of innovation is marked by the integration of AI, IoT, and robotics to enhance equipment functionality, efficiency, and flexibility. Intelligent machines with embedded sensors now enable predictive maintenance, reducing downtime by up to 30% in high-throughput factories. AI-powered cutting systems use real-time vision and machine learning to identify fabric defects and adjust cutting paths dynamically, improving material yield by 15–20%.

Sewing robots equipped with force feedback and machine vision have become increasingly precise, performing intricate stitching with reduced human oversight. Automation in folding and packaging is gaining ground, with compact units now capable of handling over 1,000 garments per hour. RFID tagging systems integrated into finishing lines allow tracking and quality assurance throughout the production cycle. In addition, smart ironing and fusing systems with programmable pressure and temperature control ensure consistency across different garment types and materials.

Software interoperability is also expanding, with machines now compatible with cloud-based production planning systems, CAD tools, and ERP platforms. This enables centralized control of distributed manufacturing setups. As the industry shifts toward lean manufacturing and sustainability, newer machines emphasize low energy consumption, closed-loop processing, and modular upgrades that reduce the need for complete replacement. These innovations collectively enable scalable, smart, and sustainable garment processing operations.

• In January 2024, Jack Sewing Machine Co., Ltd. launched an AI-enabled overlock sewing machine capable of real-time defect detection and adaptive stitch control, improving production line efficiency by 28% in pilot factories across Southeast Asia.

• In May 2023, JUKI Corporation introduced a collaborative robot arm for sewing lines that integrates with smart conveyors, reducing manual handling tasks by 40% and supporting 24/7 lights-out manufacturing.

• In March 2024, Veit GmbH unveiled an energy-efficient ironing tunnel with 25% lower power consumption and an intelligent steam distribution system designed for large-scale shirt manufacturing units in Europe.

• In October 2023, Eastman Machine Company upgraded its digital cutting tables with AI-vision calibration software, enabling automatic fabric alignment correction and enhancing precision cutting for stretch and patterned textiles.

The Garment Processing Equipment Market Report provides an in-depth evaluation of the global market across various segments, regions, applications, and technologies. It covers detailed insights on primary product types including sewing machines, cutting systems, finishing equipment, pressing systems, and automated folding/packaging units. Each category is analyzed with respect to technology adoption, end-use applicability, and integration capabilities within smart manufacturing frameworks.

Geographically, the report spans major markets including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with individual country-level insights for key contributors such as China, India, the U.S., Germany, Brazil, and the UAE. The application scope of the report covers mass garment manufacturing, custom apparel production, institutional garment processing (uniforms, workwear), and technical textile applications.

The study also evaluates technological innovations such as AI integration, IoT connectivity, energy-efficient retrofits, and cloud-based process automation. The report outlines demand trends among key end-users ranging from large garment factories to SMEs, e-commerce apparel brands, and public sector institutions. It further identifies growth in niche segments like circular economy-driven equipment, RFID tagging solutions, and on-demand garment processing technologies, enabling stakeholders to identify high-potential investment opportunities across the evolving garment processing ecosystem.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 650.0 Million |

| Market Revenue (2032) | USD 997.5 Million |

| CAGR (2025–2032) | 5.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | JUKI Corporation, Brother Industries, Ltd., PFAFF Industriesysteme und Maschinen GmbH, Pegasus Sewing Machine Mfg. Co., Ltd., Veit GmbH, Hashima Co., Ltd., Yamato Sewing Machine Mfg. Co., Ltd., Shanggong Group Co., Ltd., Richpeace Group, Dürkopp Adler GmbH, Jack Sewing Machine Co., Ltd., Gerber Technology, TYPICAL Corporation, Eastman Machine Company, Siruba (Kao Ming Machinery Industrial Co., Ltd.) |

| Customization & Pricing | Available on Request (10% Customization is Free) |