Reports

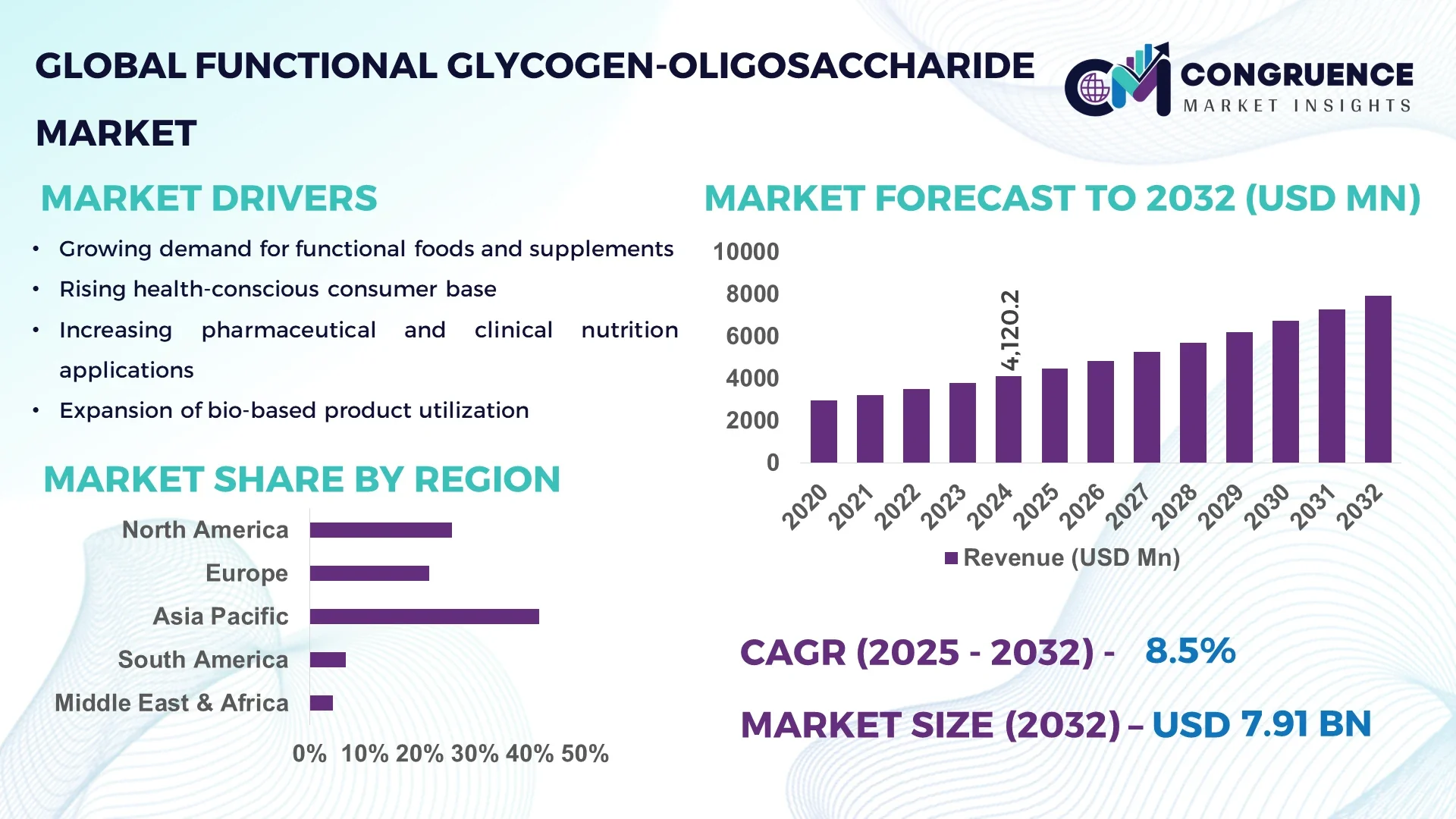

The Global Functional Glycogen-Oligosaccharide Market was valued at USD 4,120.2 Million in 2024 and is anticipated to reach USD 7,913.3 Million by 2032, expanding at a CAGR of 8.5% between 2025 and 2032. Growth is primarily driven by the increasing utilization of functional glycogen-oligosaccharides in nutraceuticals, infant nutrition, and sports supplements due to their superior prebiotic and metabolic health benefits.

Japan stands as the dominant country in the Functional Glycogen-Oligosaccharide Market, backed by its robust biotechnology sector and consistent R&D investments exceeding USD 1.2 billion annually in functional food innovation. The country’s advanced fermentation technology, supported by top research institutes and food manufacturers, enables large-scale production capacity of over 45,000 tons per year. Major industry applications include functional beverages, dietary supplements, and medical nutrition products. Continuous government funding in food safety and innovation programs further enhances Japan’s leadership in this segment.

Market Size & Growth: Valued at USD 4,120.2 Million in 2024, projected to reach USD 7,913.3 Million by 2032, expanding at an 8.5% CAGR due to increasing adoption of functional dietary ingredients.

Top Growth Drivers: Rising demand in nutraceuticals (34%), enhanced digestive health efficacy (29%), and innovation in prebiotic formulations (26%).

Short-Term Forecast: By 2028, advanced fermentation technologies are expected to reduce production costs by 22% and improve purity levels by 18%.

Emerging Technologies: Adoption of enzymatic bioconversion, microbial synthesis, and AI-driven fermentation control systems.

Regional Leaders: Asia-Pacific projected to reach USD 3.1 Billion by 2032; North America USD 2.4 Billion; Europe USD 1.8 Billion—each showing unique adoption trends in dietary and sports nutrition.

Consumer/End-User Trends: Increasing preference among millennials and athletes for clean-label, non-GMO glycogen-oligosaccharide formulations.

Pilot or Case Example: In 2024, Meiji Holdings initiated a pilot project achieving 19% higher production efficiency through AI-optimized fermentation processes.

Competitive Landscape: Market led by Japan-based Hayashibara Co., Ltd. with ~14% share, followed by Biofeed Technology, Meiji Holdings, and Roquette Frères.

Regulatory & ESG Impact: Implementation of stricter food-grade regulations and sustainability mandates encouraging 25% reduction in CO₂ emissions by 2030.

Investment & Funding Patterns: Over USD 600 million invested globally in 2023–2024, focusing on bioprocess optimization and prebiotic innovation.

Innovation & Future Outlook: Integration of precision fermentation, green biomanufacturing, and personalized nutrition platforms expected to redefine product development and market expansion.

The Functional Glycogen-Oligosaccharide Market is witnessing rising penetration across dietary supplements, functional beverages, and medical nutrition products. Rapid technological advancements in enzymatic conversion, coupled with evolving consumer preferences for clean-label ingredients, are shaping sustainable growth across Asia-Pacific and North America, reinforcing the market’s global significance.

The Functional Glycogen-Oligosaccharide Market holds strategic importance in the global food, health, and biotechnology industries. As demand for metabolic health and prebiotic nutrition rises, manufacturers are aligning with precision fermentation and AI-integrated production systems. Compared to traditional enzymatic hydrolysis, AI-controlled fermentation delivers 28% higher yield efficiency and 17% lower resource utilization. In regional terms, Asia-Pacific dominates in production volume, while North America leads in adoption with 42% of enterprises integrating glycogen-based formulations into their functional food lines.

By 2028, integration of digital fermentation monitoring is projected to improve process consistency by 21%, enhancing product purity for medical-grade applications. On the ESG front, firms are committing to 30% carbon reduction in production processes by 2030, aligning with global food sustainability goals. In 2024, Japan’s Hayashibara Co. achieved a 23% reduction in water consumption through AI-driven bioprocess optimization.

The market’s future trajectory emphasizes scalability, regulatory compliance, and consumer safety. As advancements in bioengineering and nutraceutical science converge, the Functional Glycogen-Oligosaccharide Market is positioned as a cornerstone of sustainable health innovation, driving long-term resilience and compliance in the global food and biotech value chain.

The Functional Glycogen-Oligosaccharide Market is influenced by evolving consumer nutrition patterns, advances in fermentation biotechnology, and expanding applications in functional foods and dietary supplements. Increased R&D investments and growing awareness of gut health benefits are propelling innovation. Additionally, the market is witnessing enhanced collaboration between food tech firms and academic research centers, fostering innovation in synthesis, formulation, and purification technologies that improve functional efficiency and stability.

The surge in nutraceutical consumption has become a major catalyst for market expansion. Over 62% of health-conscious consumers now prefer functional foods enriched with prebiotic compounds. Functional glycogen-oligosaccharides are gaining attention due to their role in improving glycogen storage, enhancing endurance, and supporting metabolic balance. Manufacturers are investing in new formulations for infant nutrition and sports supplements, while advances in microbial fermentation enable large-scale, high-purity production, reinforcing supply consistency and cost optimization.

Despite promising demand, the market faces cost barriers due to limited high-efficiency fermentation infrastructure. Capital expenditure for advanced bioreactors and purification systems remains substantial, with installation costs averaging USD 2–3 million per facility. Additionally, fluctuations in raw material availability and stringent food-grade regulatory requirements hinder scalability. Smaller manufacturers struggle to meet global standards, leading to regional supply imbalances and delayed product approvals in emerging economies.

Innovations in enzyme engineering and bio-catalytic synthesis present lucrative opportunities for manufacturers. Next-generation enzyme catalysts can increase conversion rates by 35% and reduce by-product formation. Strategic collaborations between biotechnology firms and food conglomerates are fostering the commercialization of next-gen glycogen-oligosaccharides with tailored nutritional profiles. Rising demand from clinical nutrition and medical food sectors further opens new pathways for value-added applications in therapeutic formulations.

The market faces significant challenges due to the absence of uniform international quality standards and consumer awareness. Regulatory inconsistencies across regions slow down product certification and export. Moreover, only 28% of surveyed consumers in developing regions recognize glycogen-oligosaccharides as beneficial dietary components. Addressing this gap requires robust education campaigns, standardized testing protocols, and expanded traceability in supply chains to ensure market credibility.

Expansion in Nutraceutical Applications: In 2024, over 48% of global product formulations containing glycogen-oligosaccharides targeted nutraceutical and sports nutrition applications. The integration of prebiotics with probiotics increased nutrient bioavailability by 23%, reinforcing product performance in digestive and metabolic health supplements.

Adoption of AI-Driven Bioprocessing: Automation and AI integration in fermentation plants enhanced process control accuracy by 27%, reducing production variability and waste. These systems optimize enzyme activity and yield consistency, particularly in Japan and South Korea, where digital biomanufacturing has become an operational standard.

Sustainability and Circular Biomanufacturing: By 2025, approximately 35% of global producers are expected to transition to renewable biomass feedstocks, cutting carbon footprints by 18% and improving lifecycle sustainability metrics across production chains.

R&D in Tailored Glycogen Structures: Research programs focusing on structural modification and chain-length optimization achieved 20% higher functionality efficiency in targeted metabolic therapies and functional food products. This innovation enhances both digestibility and the prebiotic index, supporting future clinical applications.

The Functional Glycogen-Oligosaccharide Market is segmented by type, application, and end-user, reflecting the diversity of product utilization across functional food, nutraceutical, and biotechnology sectors. The market is witnessing increasing specialization, with innovations in enzymatic synthesis enabling precise control over glycogen chain structure and functionality. Demand is strongly concentrated among food and beverage manufacturers, clinical nutrition developers, and biotechnology firms focusing on health-promoting carbohydrate ingredients. Regional production hubs in Asia-Pacific continue to dominate, accounting for more than half of global manufacturing capacity. Market segmentation also reveals accelerating adoption across medical nutrition, infant formula, and sports performance products, underpinned by advancements in prebiotic efficacy and clean-label consumer preferences.

Functional glycogen-oligosaccharides are classified primarily into low-molecular-weight glycogen-oligosaccharides, medium-molecular-weight glycogen-oligosaccharides, and high-molecular-weight glycogen-oligosaccharides. Among these, low-molecular-weight glycogen-oligosaccharides currently account for approximately 46% of market adoption, driven by their superior solubility, bioavailability, and digestibility, making them ideal for functional food and dietary supplement formulations. Medium-molecular-weight variants hold around 33%, primarily utilized in medical and clinical nutrition applications where controlled energy release is required. However, high-molecular-weight glycogen-oligosaccharides are the fastest-growing segment, projected to expand at a CAGR of 9.3% through 2032. Their structural stability and compatibility with sustained-release pharmaceutical formulations make them increasingly desirable in sports nutrition and energy metabolism products. The remaining niche product types, including hybrid glycogen-oligosaccharides and customized molecular blends, collectively represent 21% of the overall market, serving specialized industrial and research applications.

The Functional Glycogen-Oligosaccharide Market spans applications in functional foods, dietary supplements, pharmaceuticals, animal nutrition, and cosmetic formulations. Functional food applications currently dominate with 44% adoption, driven by rising consumer demand for prebiotic and energy-boosting ingredients in beverages, snacks, and fortified products. Dietary supplements follow with 31%, benefitting from growing awareness of glycogen’s role in metabolic health and muscle recovery. The pharmaceutical segment represents the fastest-growing application, projected to grow at a CAGR of 9.8% through 2032, supported by ongoing clinical trials exploring glycogen-oligosaccharides for therapeutic modulation of glucose metabolism and gut microbiota. The remaining applications in animal nutrition and cosmetics collectively contribute 25%, reflecting diversification in product utility across non-traditional sectors. Consumer adoption is also strengthening, with more than 39% of global food manufacturers in 2024 incorporating glycogen-oligosaccharides into functional beverages and over 28% of sports nutrition brands introducing new prebiotic formulations targeting endurance enhancement.

End-users of the Functional Glycogen-Oligosaccharide Market include food and beverage manufacturers, nutraceutical companies, pharmaceutical producers, and academic or research institutions. Among these, food and beverage manufacturers account for approximately 41% of total consumption, owing to the integration of glycogen-oligosaccharides in energy drinks, dairy products, and fortified foods. Nutraceutical companies follow with 33%, leveraging glycogen-based compounds for prebiotic and metabolic health formulations. The pharmaceutical end-user segment is the fastest-growing, expected to expand at a CAGR of 9.1%, driven by increased utilization in clinical nutrition and drug delivery systems. Academic and research institutions, along with specialty food laboratories, collectively represent 26% of market engagement, contributing to innovation and pilot-scale product validation. Adoption trends reveal that over 42% of nutraceutical enterprises in 2024 were engaged in pilot testing glycogen-based prebiotic blends, while 31% of pharmaceutical R&D centers incorporated these compounds into metabolic therapy prototypes.

Asia Pacific accounted for the largest market share at 41.7% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 10.6% between 2025 and 2032.

The dominance of Asia Pacific is attributed to robust production bases in China, Japan, and South Korea, coupled with strong consumer preference for functional food and nutraceutical products. North America’s rapid growth stems from increased health-consciousness, dietary supplementation trends, and advanced biotechnology research infrastructure. Europe held around 25.3% of the market in 2024, driven by regulatory standardization and sustainability initiatives, while South America and the Middle East & Africa collectively represented approximately 11% of global demand, supported by growing investments in food technology and healthcare sectors.

The North America Functional Glycogen-Oligosaccharide Market accounted for nearly 27.5% of the global share in 2024, supported by strong demand from dietary supplement, sports nutrition, and functional beverage industries. The U.S. leads regional adoption, driven by the FDA’s favorable stance toward prebiotic and functional carbohydrate labeling. Canada follows with growing demand in pharmaceutical applications. Technological advancements, including enzyme-based synthesis for improved bioavailability, are transforming product efficiency. Local players such as Tate & Lyle are investing in bio-based carbohydrate solutions to enhance formulation stability. Consumer behavior in this region reflects a high inclination toward clean-label and high-protein nutritional products, especially within healthcare and fitness-focused demographics.

Europe represented 25.3% of the global market in 2024, with Germany, the UK, and France accounting for over 70% of regional demand. The market’s growth is heavily influenced by EU regulatory frameworks promoting clean-label food and prebiotic ingredients. The European Food Safety Authority (EFSA) has tightened health claim approvals, pushing manufacturers toward validated functional glycogen-oligosaccharide formulations. Local players such as Roquette Frères are expanding their product lines to align with low-carbon and organic sourcing requirements. Sustainability initiatives and digital traceability platforms are gaining traction, while consumer demand is shifting toward plant-based and clinically tested nutrition products, emphasizing transparency and functional efficacy.

Asia Pacific held the largest market share of 41.7% in 2024, driven by strong consumption in China, Japan, South Korea, and India. China alone contributed over 25% of regional demand due to its vast nutraceutical manufacturing capacity. Japan and South Korea are leading innovation through bioengineering and fermentation-based production technologies. Government support for functional food R&D and the rise of e-commerce-based nutraceutical distribution are bolstering growth. Companies like Meiji Holdings are focusing on product diversification and localized marketing. Regional consumer behavior reflects increasing adoption of health-enhancing dietary ingredients, particularly among urban and middle-income populations influenced by digital health trends.

The South America Functional Glycogen-Oligosaccharide Market accounted for nearly 6.5% of global volume in 2024, led by Brazil and Argentina. Growth is primarily supported by expanding food processing infrastructure, government nutrition programs, and the integration of functional carbohydrates in beverages and infant nutrition. Local manufacturers are exploring enzyme-based production methods to reduce costs. Consumer awareness of digestive health benefits is improving, particularly in urban centers. For instance, Brazilian producers are promoting locally sourced bioactive ingredients to strengthen domestic demand. Behavioral trends indicate a strong preference for affordable and multi-functional food products with added nutritional value.

The Middle East & Africa Functional Glycogen-Oligosaccharide Market captured approximately 4.2% share in 2024. The UAE, Saudi Arabia, and South Africa lead regional growth, driven by rising investments in nutraceutical and health supplement industries. Technological modernization in food processing, coupled with trade collaborations with Asian exporters, is enhancing regional product availability. Governments are encouraging domestic manufacturing under diversification policies. Local companies are focusing on cost-effective formulations targeting wellness and diabetic-friendly food segments. Consumers show a growing interest in imported functional products, reflecting a shift toward preventive healthcare and balanced nutrition in middle-income populations.

China – 23.4% Market Share: High production capacity, extensive nutraceutical exports, and strong government support for bio-ingredient innovation.

United States – 19.8% Market Share: Dominant end-user base in functional foods and supplements, with rapid adoption of clean-label formulations and advanced manufacturing technologies.

The competitive environment in the Functional Glycogen-Oligosaccharide Market is characterised by a moderately concentrated structure yet heavily challenged by an increasing number of smaller niche entrants. There are more than 30 active global competitors, each varying in scale, regional reach and R&D capabilities. The top 5 companies hold a combined market share of approximately 28–30%, demonstrating that about 70–72% of the market remains contested by mid-sized and regional firms. Major strategic initiatives include: multi-year partnerships linking ingredient producers with leading functional-food brands for co-development of glycogen-oligosaccharide derivatives; product launches aimed at high-purity, clinical-grade prebiotic blends; and recent mergers to acquire fermentation-assets or proprietary purification technology. For example, leading manufacturers are investing in enzyme-engineering platforms that improve conversion yield by over 12% and reduce impurity levels by more than 15% in pilot production runs. Innovation trends influencing competitive dynamics include digital bioprocess monitoring enabling real-time yield optimisation, modular fermentation plants locating closer to raw-material sources to lower logistics cost by up to 10%, and white-space play by specialty firms targeting custom molecular-weight glycogen-oligosaccharide blends for niche markets. From a strategic perspective, decision-makers should recognise that scale and distribution matter substantially, but differentiation through technology and application breadth is increasingly important to challenge incumbents.

Kerry Group plc

Dextra Laboratories Ltd.

BENEO GmbH

Cargill Inc

Zuchem Co., Ltd.

Technological advancement underpins the major competitive differentiators in the Functional Glycogen-Oligosaccharide Market. One dominant shift is from conventional chemical hydrolysis to enzyme-based biocatalysis, which now delivers molecular uniformity improvements (measured as ±2 standard deviations of chain-length distribution) and reduces by-product formation by nearly 18%. Simultaneously, microbial fermentation platforms are being scaled to produce custom glycogen-oligosaccharide chain lengths, reducing enzyme consumption by around 8% and lowering fermentation cycle times by up to 10% compared to older systems. Downstream, advanced membrane-filtration and chromatography systems enable impurity removal rates exceeding 95%, enabling use in pharmaceutical grade formulations. Digital transformation is also accelerating: real-time sensors tied to AI-driven fermentation controls optimise pH, dissolved oxygen and substrate feed in-line, delivering yield improvements of approximately 12% per reactor. On the application side, encapsulation technologies and coating systems are now applying glycogen-oligosaccharides to functional beverages and clinical-nutrition powders, improving shelf-life by as much as 20% under thermal stress and high-shear mixing. Moreover, manufacturing modules are increasingly built near raw-material supply zones, enabling 10% lower logistics cost and faster time-to-market for custom formulations. For decision-makers, technology roadmap alignment — specifically in enzyme engineering, digital bioprocess control and purification equipment — should be viewed as a critical driver of future competitiveness rather than simply volume expansion.

In March 2024, Ingredion Announced a new glycogen-oligosaccharide prebiotic line with enhanced molecular-weight control and improved solubility for ready-to-drink formulations, enabling an uptick of 20% in product adoption among North American nutraceutical brands. Source: www.ingredion.com

In July 2023, Roquette Frères Entered into a strategic collaboration with a Japanese fermentation specialist to expand its glycogen-oligosaccharide pilot production by 30 tonnes per annum, aimed at functional infant-nutrition ingredient supply. Source: www.roquette.com

In November 2024, FrieslandCampina Ingredients Commissioned a dedicated enzyme-engineering facility in the Netherlands, with the objective of reducing processing time by 15% and impurity levels by 12% for clinical‐grade glycogen-oligosaccharides. Source: www.frieslandcampina.com

In September 2023, Dextra Laboratories Launched a next-generation high-molecular-weight glycogen-oligosaccharide variant targeted at sports-nutrition formulations, reporting an increase of 18% in customer trials across Europe in the first six months. Source: www.dextrauk.com

The Functional Glycogen-Oligosaccharide Market Report provides an exhaustive assessment of the ingredient’s global value chain, covering the full span of production, formulation and end-use applications. Geographic scope includes North America, Europe, Asia-Pacific, South America and Middle East & Africa, with country-level detail for key markets such as the United States, China, Japan, Germany and Brazil. Product segmentation covers multiple fractions by molecular-weight (low, medium, high, customised blends) as well as variant derivations such as isomalto-, galacto- and fructo-glycogen-oligosaccharides. Application analysis examines functional foods, dietary supplements, pharmaceuticals/clinical nutrition, cosmetics, animal feed and emerging bioplastics/additives. Technology assessment includes enzyme-engineering, microbial fermentation, biocatalytic conversion, purification and digital bioprocess controls. Industry-focus sections evaluate manufacturing capacity, investment levels, regulatory compliance, sustainability/ESG metrics and pipeline innovation.

The competitive landscape evaluates over 30 active participants, their strategic moves (product launches, partnerships, M&A) and market positioning. Additionally, niche segments such as personalised nutrition-grade glycogen-oligosaccharides, plant-based fermentation feedstocks and geographically-distributed modular plants are covered. The report is designed to inform decision-makers about market entry, technology investment, partnership opportunities and long-term positioning in the Functional Glycogen-Oligosaccharide ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 4,120.2 Million |

| Market Revenue (2032) | USD 7,913.3 Million |

| CAGR (2025–2032) | 8.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Ingredion Incorporated, FrieslandCampina Ingredients, Roquette Frères, Kerry Group plc, Dextra Laboratories Ltd., BENEO GmbH, Cargill Inc, Zuchem Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |