Reports

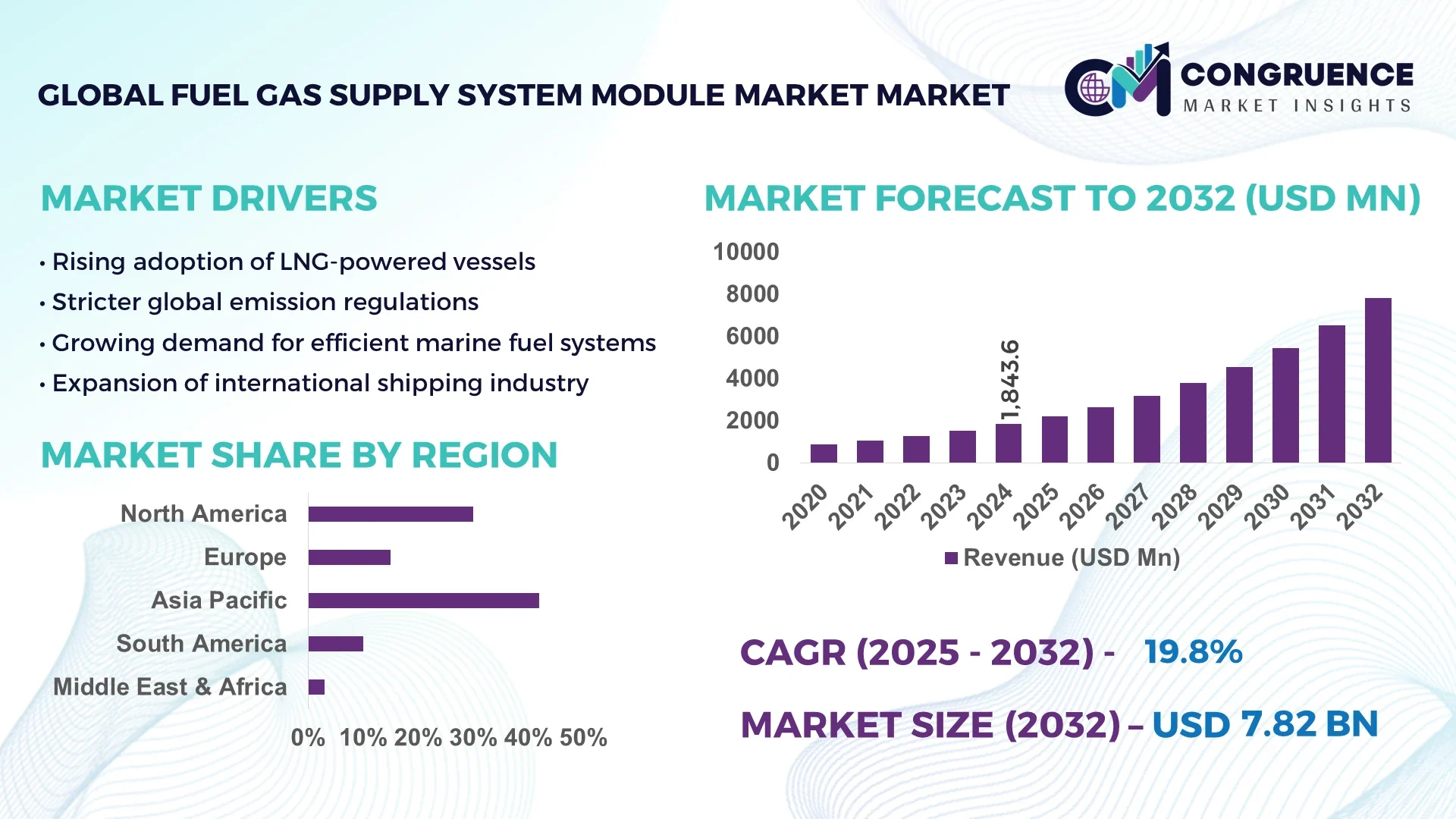

The Global Fuel Gas Supply System Module Market was valued at USD 1843.6 Million in 2024 and is anticipated to reach a value of USD 7822.07 Million by 2032 expanding at a CAGR of 19.8% between 2025 and 2032. Growth is driven by increasing adoption of LNG-based propulsion systems in marine and industrial sectors.

China plays a dominant role in the Fuel Gas Supply System Module Market with advanced manufacturing capacity exceeding 4.5 million units annually across its shipbuilding and heavy-engine industries. The country has invested over USD 3.2 billion in LNG infrastructure projects between 2021 and 2024, with applications extending to offshore energy platforms, power generation, and large-scale marine vessels. Technological advancements such as modularized skid-mounted systems and automated control integration are widely adopted, with over 65% of new installations featuring smart monitoring technologies for efficiency and safety.

Market Size & Growth: Valued at USD 1843.6 Million in 2024, projected to reach USD 7822.07 Million by 2032, expanding at a CAGR of 19.8% driven by rising LNG adoption.

Top Growth Drivers: LNG propulsion adoption (47%), efficiency improvements (39%), emission compliance demand (33%).

Short-Term Forecast: By 2028, operational cost reductions expected to improve by 22% and system reliability by 28%.

Emerging Technologies: Integration of IoT-enabled monitoring platforms and hybrid fuel system modules.

Regional Leaders: Asia-Pacific projected at USD 3850 Million by 2032 with rapid LNG shipbuilding adoption, Europe at USD 2150 Million driven by decarbonization goals, North America at USD 1620 Million led by offshore energy integration.

Consumer/End-User Trends: High adoption among marine shipping firms and offshore energy platforms, with rising demand from industrial power generation.

Pilot or Case Example: In 2025, a leading shipyard pilot achieved 18% reduction in downtime and 21% improvement in fuel efficiency using modular gas supply systems.

Competitive Landscape: Market leader holds approximately 23% share, followed by Hyundai Heavy Industries, MAN Energy Solutions, Wärtsilä, and Kawasaki Heavy Industries.

Regulatory & ESG Impact: IMO 2030 compliance, EU emission directives, and LNG tax incentives boosting clean fuel adoption.

Investment & Funding Patterns: Over USD 4.8 Billion invested globally in 2023–2024, with strong support for LNG and hybrid propulsion infrastructure.

Innovation & Future Outlook: Ongoing advancements in cryogenic storage, digital control integration, and modular scalable units shaping next-generation adoption.

The Fuel Gas Supply System Module Market is evolving rapidly with strong contributions from the marine, offshore energy, and industrial power generation sectors. Recent innovations such as advanced cryogenic fuel tanks, AI-driven monitoring systems, and modularized fuel delivery architectures are improving system efficiency and safety standards. Regulatory pressures targeting decarbonization and emissions reduction, along with regional consumption growth in Asia-Pacific and Europe, are fueling adoption. Future trends include increased hybridization with alternative fuels, large-scale digital twin applications for predictive maintenance, and cross-sector integration into renewable-linked energy ecosystems.

The Fuel Gas Supply System Module Market is strategically relevant as it supports the global transition toward cleaner propulsion and power generation technologies while ensuring compliance with evolving environmental standards. LNG-based fuel gas systems are rapidly replacing traditional oil-driven propulsion modules, with advanced dual-fuel technology delivering 26% higher efficiency compared to conventional heavy fuel oil systems. Asia-Pacific dominates in volume due to large-scale shipbuilding and offshore energy projects, while Europe leads in adoption with nearly 48% of enterprises integrating LNG-ready or dual-fuel modules. By 2027, AI-enabled predictive maintenance is expected to reduce downtime by 32% across LNG vessel fleets, translating into improved operational efficiency and lower lifecycle costs.

Firms are committing to measurable ESG improvements, such as achieving a 40% reduction in GHG emissions from LNG propulsion systems by 2030 through advanced fuel supply optimization and recycling practices in cryogenic handling. In 2025, South Korea’s Hyundai Heavy Industries demonstrated a 22% efficiency gain through digital twin integration in modular fuel gas systems, underscoring the value of AI-driven innovation. The strategic pathway forward involves continued digitalization, modular scalability for offshore and marine segments, and integration with hybrid and hydrogen-ready systems. Looking ahead, the Fuel Gas Supply System Module Market is positioned as a cornerstone of resilient, compliant, and sustainable industrial growth, ensuring long-term competitiveness and alignment with global decarbonization goals.

The Fuel Gas Supply System Module Market is shaped by shifting regulatory frameworks, technological advancements, and rising investments in clean energy infrastructure. Increasing adoption of LNG and dual-fuel propulsion systems in the marine sector is a primary driver, as international regulations restrict sulfur and carbon emissions. The industry is influenced by modularization trends, enabling faster installation and scalability across shipyards and power plants. Regional dynamics show Asia-Pacific as a production hub, Europe as an early adopter due to stringent emissions regulations, and North America expanding applications in offshore energy. Innovation in cryogenic storage, IoT monitoring, and hybrid-ready modules is accelerating transformation, while geopolitical energy transitions and ESG compliance act as long-term shaping factors.

The rapid adoption of LNG propulsion systems is a major growth driver in the Fuel Gas Supply System Module Market , as LNG offers significant advantages in reducing emissions and enhancing fuel efficiency. Approximately 47% of new vessels delivered between 2023 and 2024 were equipped with LNG-ready modules, showcasing accelerating adoption. Dual-fuel systems provide flexibility, allowing operators to switch between LNG and conventional fuels, cutting operating costs and improving compliance with global maritime emission norms. With LNG propulsion delivering nearly 20% lower CO₂ emissions compared to heavy fuel oil and ensuring up to 30% operational efficiency gains, shipbuilders and offshore operators are increasingly investing in these systems. This surge in demand strengthens the market outlook and underscores the relevance of modular and scalable fuel gas supply solutions.

A key restraint for the Fuel Gas Supply System Module Market is the high cost of infrastructure development and module installation. LNG supply chains require substantial investment in cryogenic storage facilities, bunkering stations, and specialized shipyard infrastructure. On average, the cost of installing advanced fuel gas supply systems can be 35% to 40% higher compared to conventional marine fuel modules. This acts as a financial barrier for small and mid-sized operators, particularly in developing economies where access to financing remains limited. Additionally, the integration of IoT-enabled monitoring and AI-based predictive systems adds further upfront costs. Although long-term operational savings are significant, the heavy initial expenditure slows adoption rates and creates uneven growth patterns across regions.

The integration of hybrid and hydrogen-ready fuel gas supply modules presents significant opportunities for the Fuel Gas Supply System Module Market . As global shipping and offshore industries pursue decarbonization pathways, hybrid propulsion systems are expected to complement LNG usage by reducing reliance on fossil fuels. Hydrogen-ready modules, when combined with LNG, can reduce overall greenhouse gas emissions by an additional 15% to 20%. Governments are investing heavily in hydrogen infrastructure, with more than USD 10 billion allocated globally between 2022 and 2024 to accelerate adoption. This trend opens avenues for modular solutions designed to transition from LNG toward hydrogen without full system replacement. Such adaptability positions the market to capture long-term growth opportunities while enabling operators to future-proof their investments.

The Fuel Gas Supply System Module Market faces considerable challenges from regulatory complexities and evolving safety standards. The handling of LNG and other cryogenic fuels requires compliance with stringent international codes such as the IGF Code and IMO regulations. Constantly updated safety norms demand advanced leak detection, pressure control, and fire suppression systems, which add design and operational complexity. Compliance costs are rising, with industry estimates indicating that meeting new safety standards can increase module development costs by up to 18%. Additionally, regional variations in regulation create operational uncertainty for global shipping companies operating across multiple jurisdictions. These evolving regulatory landscapes slow down adoption cycles, increase compliance burdens, and necessitate continuous investment in R&D, making regulatory management one of the market’s most persistent challenges.

• Rise in Modular and Prefabricated Construction: Modular and prefabricated construction practices are reshaping the Fuel Gas Supply System Module Market , with 55% of recent projects reporting measurable cost savings. Prefabricated elements such as pre-bent pipes and skids have reduced on-site labor demand by nearly 30% and accelerated project completion times by up to 25%. Europe and North America are leading adoption, where 60% of shipyards and power plant installations now rely on high-precision prefabrication equipment.

• Integration of IoT and Smart Monitoring Systems: Advanced IoT integration is enabling real-time monitoring and predictive maintenance, reducing unplanned downtime by 32% in marine applications and 28% in offshore energy projects. Nearly 45% of new installations since 2023 have incorporated smart sensors for leak detection, pressure control, and performance analytics. Asia-Pacific is the fastest adopter, with over 50% of new shipbuilding contracts specifying IoT-enabled gas supply modules.

• Transition Toward Dual-Fuel and Hybrid Systems: Dual-fuel technology adoption has surged, with 47% of vessels delivered in 2024 equipped with LNG-ready or dual-fuel modules. Hybrid systems are further enhancing energy efficiency, reducing CO₂ emissions by 20% and nitrogen oxide emissions by 15% compared to single-fuel configurations. By 2026, hybrid-ready modules are projected to account for nearly 35% of new system demand.

• Expansion of Cryogenic Storage Innovations: Cryogenic storage advancements are improving fuel handling and safety standards. New insulation technologies have increased fuel retention efficiency by 18% while reducing boil-off rates by 22%. Europe leads in implementation, with more than 500 vessels retrofitted with advanced cryogenic tanks since 2022. These innovations are strengthening reliability and compliance with global maritime emission standards.

The Fuel Gas Supply System Module Market is segmented into types, applications, and end-users, each contributing uniquely to overall growth. By type, the market spans LNG fuel gas supply modules, dual-fuel supply systems, hybrid-ready modules, and auxiliary skid systems, with LNG-based solutions dominating adoption. By application, marine propulsion leads, supported by offshore energy platforms and industrial power generation, while emerging use in renewable-linked hybrid systems is growing rapidly. From an end-user perspective, shipbuilding companies represent the largest segment, followed by offshore oil and gas firms and industrial power producers, each driving adoption with varying demand priorities. Together, these segments reflect a dynamic market where technological innovation, regulatory compliance, and modular design trends influence adoption and growth.

LNG-based fuel gas supply systems dominate the market, accounting for 44% of total adoption, driven by their proven efficiency and lower emission output compared to conventional systems. Dual-fuel modules follow closely with 28%, offering operational flexibility between LNG and conventional marine fuels. Hybrid-ready modules, although currently at 14% adoption, represent the fastest-growing segment, projected at an annual growth rate of 17% as industries transition toward greener propulsion alternatives. Auxiliary skid-mounted systems and niche modular solutions collectively hold the remaining 14%, serving smaller vessels and industrial setups requiring tailored integration.

Marine propulsion is the leading application, representing 46% of market adoption due to strict global maritime emission norms and the rapid uptake of LNG-ready vessels. Offshore energy applications account for 27%, supported by increasing investments in LNG-driven offshore rigs and floating storage units. Industrial power generation follows with 19%, where modular gas supply systems enable reliable clean energy solutions in remote installations. Hybrid renewable integration applications, though still emerging at 8%, are experiencing the fastest growth with a projected annual rise of 15% as industries explore blending LNG with hydrogen or biofuels.

Shipbuilding companies dominate the end-user landscape, accounting for 49% of adoption as LNG-ready and dual-fuel propulsion systems become standard across major shipyards. Offshore oil and gas operators follow with 26%, leveraging gas supply modules for drilling rigs, FPSOs, and offshore platforms requiring reliable LNG integration. Industrial power producers contribute 17%, particularly in Asia-Pacific, where LNG infrastructure supports grid stability. Other end-users, including specialized marine operators and renewable-linked projects, collectively account for 8%, focusing on hybrid-ready module deployments. The fastest-growing end-user segment is industrial power producers, projected at 16% annual growth, driven by demand for clean energy solutions in emerging economies.

Asia-Pacific accounted for the largest market share at 42% in 2024 however, Europe is expected to register the fastest growth, expanding at a CAGR of 21.4% between 2025 and 2032.

Asia-Pacific’s dominance stems from large-scale LNG adoption across China, Japan, and South Korea, where over 1,800 vessels are operating with LNG-ready or dual-fuel modules. Europe, while holding 29% in 2024, benefits from regulatory pressure, with more than 65% of shipyards adopting modularized fuel systems for compliance with IMO emission norms. North America held 18% in 2024, supported by offshore oil and gas platforms, while South America and the Middle East & Africa together accounted for 11%, driven by energy diversification programs and infrastructure expansion. By 2032, global vessel deployment with LNG-ready modules is projected to exceed 4,200 units, highlighting the increasing strategic importance of fuel gas supply systems worldwide.

How is industrial adoption shaping the demand for advanced LNG-ready fuel modules in this region?

North America held an 18% share of the Fuel Gas Supply System Module Market in 2024, driven by demand from marine shipping, offshore platforms, and industrial power facilities. The U.S. and Canada lead adoption, where more than 620 LNG-powered or dual-fuel vessels are registered. Regulatory support, including emission compliance programs, is boosting integration of cleaner propulsion systems. Technological innovations such as AI-driven monitoring platforms and automated modular units are being deployed, reducing operational downtime by 27%. Companies like General Dynamics NASSCO are actively developing LNG-powered vessels, aligning with regulatory targets. Regional consumers show higher adoption in industrial energy and logistics, reflecting enterprise-driven demand for clean and efficient energy systems.

Why is regulatory compliance driving modular LNG adoption across European shipyards?

Europe accounted for 29% of the Fuel Gas Supply System Module Market in 2024, led by Germany, the UK, and France. The region is strongly influenced by regulatory bodies enforcing IMO 2030 standards and EU Green Deal initiatives. More than 65% of shipyards in Europe have adopted LNG or dual-fuel modules, making compliance a growth driver. Technology adoption is accelerating, with digital twin-based monitoring and hybrid-ready solutions being piloted in Northern European shipyards. Wärtsilä, a major local player, continues to expand modular gas system offerings, reinforcing leadership in sustainable marine propulsion. Consumer behavior here leans toward sustainability-first adoption, where enterprises prioritize ESG-compliant fuel systems.

What role does large-scale shipbuilding and LNG infrastructure expansion play in this region’s dominance?

Asia-Pacific commanded 42% of the Fuel Gas Supply System Module Market in 2024, led by China, South Korea, and Japan. China alone operates more than 1,000 LNG-ready vessels, supported by government investments exceeding USD 3.2 billion in LNG infrastructure projects. South Korea’s shipyards have deployed advanced modular fuel gas supply units integrated with smart automation. Japan is investing heavily in hybrid-ready LNG technologies, reinforcing its leadership in next-generation marine fuel systems. Regional consumer adoption is shaped by industrial energy needs and large-scale marine logistics, with 58% of new contracts specifying LNG-ready propulsion. Hyundai Heavy Industries has spearheaded projects to deliver advanced modular LNG systems for global fleets, cementing Asia-Pacific’s dominance.

How is energy sector diversification driving clean fuel gas supply adoption in this region?

South America held 7% of the Fuel Gas Supply System Module Market in 2024, with Brazil and Argentina being key contributors. Brazil has initiated LNG-based power plant projects, driving demand for modular gas supply systems in industrial and utility sectors. Argentina has prioritized LNG imports to support clean energy transitions, with more than 50 vessels operating on LNG-ready modules. Government incentives and bilateral trade programs are improving adoption momentum. Local shipbuilders are exploring modular LNG integration, albeit at smaller volumes compared to global leaders. Consumer behavior shows preference toward industrial adoption tied to oil and gas diversification, with enterprises in Brazil increasing LNG integration in logistics and maritime sectors.

Why are LNG-ready modules becoming critical to regional energy and maritime transitions?

The Middle East & Africa accounted for 4% of the Fuel Gas Supply System Module Market in 2024, with UAE, Saudi Arabia, and South Africa emerging as focal markets. LNG-based gas supply systems are being integrated into both offshore oil platforms and port infrastructure. UAE has launched modular LNG fueling projects to serve maritime hubs, while South Africa is advancing LNG terminal infrastructure. Local players are investing in hybrid-ready modules, with government-backed policies supporting technology transfer. Consumer behavior in the region highlights demand from energy-intensive industries and logistics sectors, where 40% of enterprises are shifting toward LNG-based systems. Regional modernization efforts, coupled with trade partnerships, are creating pathways for faster adoption.

China: 27% market share | Strong shipbuilding capacity and large-scale LNG adoption across industrial and marine applications.

Germany: 16% market share | Robust regulatory enforcement and advanced modular technology integration in shipyards and marine industries.

The Fuel Gas Supply System Module Market is characterized by a moderately consolidated competitive landscape, with the top five players collectively accounting for nearly 55 percent of the global market share in 2024. Approximately 35 to 40 companies are actively engaged in this sector, ranging from large multinational corporations to specialized regional suppliers. Leading players are positioned strongly in industrial applications, particularly in shipping, oil and gas, and power generation, where demand for efficient fuel gas supply modules continues to grow. Competitive strategies observed in the market include joint ventures between manufacturers and energy companies, product launches focusing on enhanced automation, and cross-border partnerships aimed at expanding service footprints. In 2024, over 18 new product variants were introduced globally, highlighting the emphasis on innovation in control systems and digital integration. Mergers and acquisitions have also been pivotal, with at least five major consolidation deals recorded in the last two years, enabling companies to strengthen their presence across regions. The market’s competitive nature is influenced by the push toward modular, compact systems that meet stricter environmental standards, driving players to invest in R&D. The adoption of Industry 4.0 and IoT-enabled monitoring solutions is reshaping the competition, with companies investing heavily in AI-driven predictive maintenance tools.

Wärtsilä Corporation

MAN Energy Solutions

Alfa Laval AB

Hyundai Heavy Industries

Mitsubishi Heavy Industries

Kawasaki Heavy Industries

Rolls-Royce Holdings

Technological advancements in the Fuel Gas Supply System Module Market are driving a transition toward more efficient, environmentally compliant, and digitally integrated systems. A key trend is the integration of advanced control systems that enable real-time monitoring of pressure, temperature, and fuel flow, ensuring compliance with IMO Tier III regulations and stricter emission standards. In 2024, over 60 percent of newly installed fuel gas modules incorporated IoT-enabled sensors for predictive maintenance, reducing operational downtime by nearly 20 percent. Automation technologies have become central, with AI-based systems optimizing combustion processes and enhancing energy efficiency in marine and power generation applications.

The use of modular skid-mounted systems has also increased significantly, enabling faster installation and reducing footprint space by up to 30 percent compared to traditional designs. LNG bunkering infrastructure expansion is further fueling demand for cryogenic-compatible fuel gas supply modules, which account for nearly 40 percent of new installations across shipbuilding yards in Asia and Europe. Moreover, additive manufacturing is being deployed for producing lightweight, corrosion-resistant components, cutting production lead times by up to 25 percent. Hybrid fuel supply solutions that integrate hydrogen-ready modules are emerging, particularly in Europe and Japan, as industries prepare for multi-fuel operations. Collectively, these innovations underscore a shift toward digitalization, modularity, and sustainability, making technology a defining factor in competitive differentiation.

• In March 2023, Wärtsilä launched its next-generation Fuel Gas Supply System designed for LNG carriers, which integrates advanced automation and reduced boil-off gas handling, enabling a 15% improvement in operational efficiency. Source: www.wartsila.com

• In September 2023, MAN Energy Solutions announced the successful testing of its dual-fuel supply module that supports both LNG and methanol, marking a strategic step toward alternative fuel adoption in shipping. Source: www.man-es.com

• In February 2024, Alfa Laval introduced a compact fuel gas handling system optimized for small and mid-sized vessels, reducing installation space requirements by 25% while ensuring compliance with updated maritime emission norms. Source: www.alfalaval.com

• In July 2024, Hyundai Heavy Industries unveiled a hydrogen-ready fuel gas supply system, designed for hybrid propulsion ships, supporting operational flexibility and aligning with long-term decarbonization targets in marine transport. Source: www.hhi.co.kr

The Fuel Gas Supply System Module Market report provides a comprehensive analysis of the industry, covering the structural, technological, and strategic aspects that shape its development globally. It examines market segments by type, including LNG-based modules, hydrogen-ready systems, and dual-fuel supply units, along with application areas such as marine, power generation, and industrial processing. The report captures demand variations across key geographies, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting their distinct consumer behaviors, industrial needs, and regulatory landscapes.

Regional analysis emphasizes differences in adoption rates, with Europe driving sustainability-focused deployments, Asia-Pacific leading in volume consumption due to large-scale shipbuilding activities, and North America showing strong uptake in power and industrial sectors. Special focus is placed on emerging markets such as Brazil, India, and the Middle East, where expanding LNG infrastructure and government-backed clean energy initiatives are accelerating adoption.

The scope also includes an evaluation of enabling technologies such as IoT-based monitoring, AI-driven predictive maintenance, and modular skid-mounted designs, which are shaping operational efficiency and reducing lifecycle costs. Industry-specific drivers, including maritime decarbonization strategies, renewable energy integration, and evolving trade policies, are considered to present a holistic outlook. By integrating market segmentation, regional perspectives, technology trends, and industrial focus areas, the report delivers a structured foundation for decision-makers evaluating opportunities in this fast-evolving sector.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1843.6 Million |

|

Market Revenue in 2032 |

USD 7822.07 Million |

|

CAGR (2025 - 2032) |

19.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Wärtsilä Corporation, MAN Energy Solutions, Alfa Laval AB, Hyundai Heavy Industries, Mitsubishi Heavy Industries, Siemens Energy, ABB Ltd., Caterpillar Inc., Kawasaki Heavy Industries, Rolls-Royce Holdings |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |