Reports

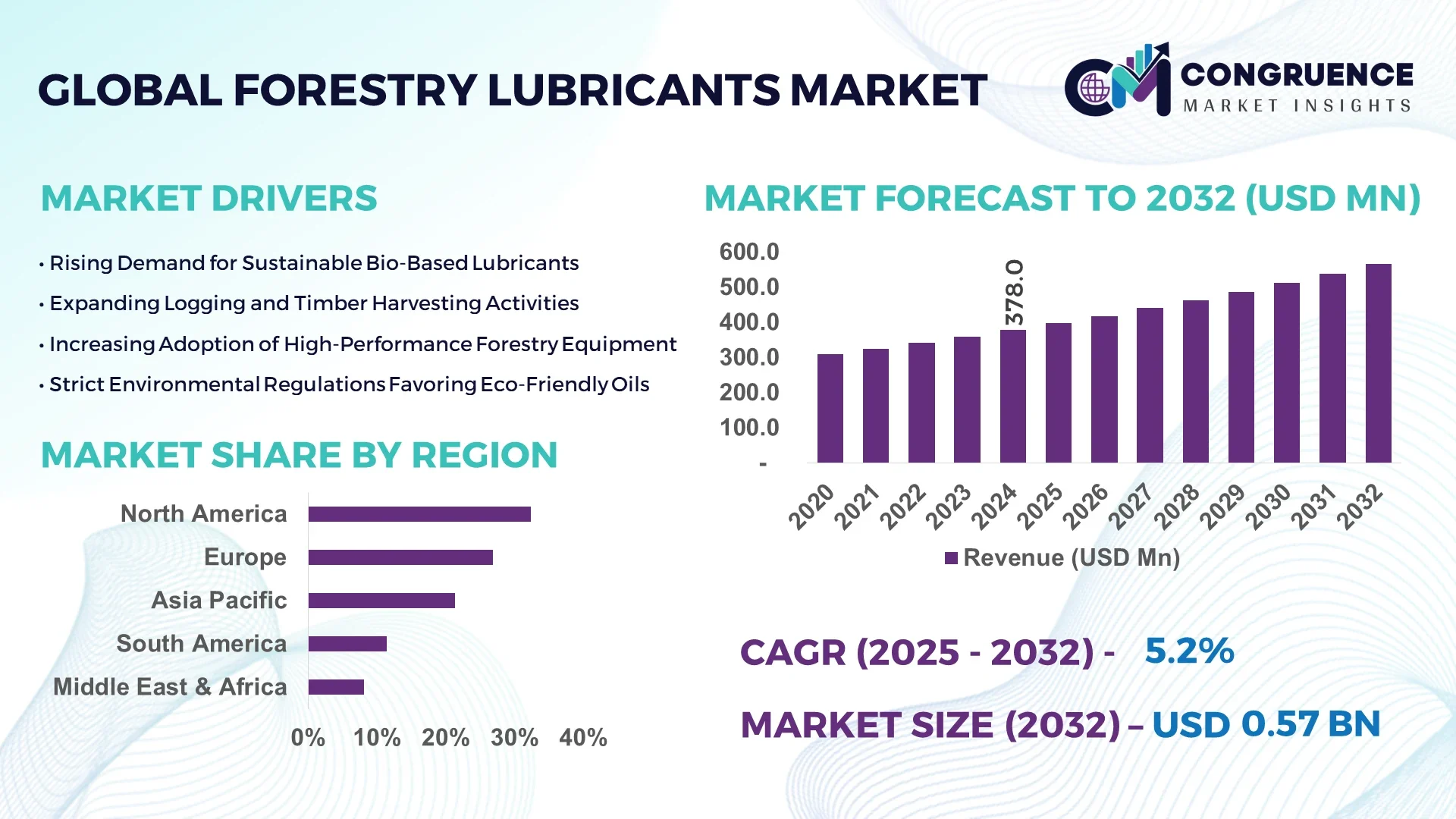

The Global Forestry Lubricants Market was valued at USD 378.0 Million in 2024 and is anticipated to reach a value of USD 567.0 Million by 2032 expanding at a CAGR of 5.2% between 2025 and 2032.

The United States holds a dominant position in the Forestry Lubricants Market, supported by its extensive manufacturing infrastructure, robust R&D investments exceeding USD 10 billion annually in bio-based lubricants, and advanced application in precision forestry machinery. The country also leads in deployment of high-performance biodegradable lubricants across timber harvesting and processing sectors, particularly in states like Oregon and Washington.

The Forestry Lubricants Market plays a critical role across multiple industry sectors including logging, timber transportation, sawmilling, and biomass production. Industrial applications account for over 65% of lubricant consumption, particularly in hydraulic systems, chainsaws, harvesters, and heavy-duty forestry equipment. The market is witnessing a strong shift towards environmentally acceptable lubricants (EALs) driven by increasingly stringent environmental regulations in Europe and North America. Technological advancements, such as nanotechnology-infused lubricants and synthetic ester formulations, are significantly improving machinery uptime and performance under harsh operating conditions. Furthermore, the rise in sustainable forest management practices and governmental mandates promoting low-toxicity, biodegradable alternatives are fostering product innovation. Consumption patterns indicate growing demand in emerging economies such as Brazil, Chile, and Indonesia, spurred by industrial-scale afforestation and forest product exports. Looking ahead, digital integration, predictive maintenance, and equipment-specific formulations are set to redefine competitive advantage in this evolving landscape.

Artificial intelligence (AI) is rapidly transforming the operational dynamics of the Forestry Lubricants Market by enhancing predictive maintenance, real-time monitoring, and automated diagnostics across forestry machinery. These AI-powered solutions help decision-makers optimize lubricant selection, reduce equipment downtime, and extend service intervals in harsh forestry environments. AI-enabled sensors integrated within forestry equipment collect data on pressure, temperature, and lubricant viscosity to enable intelligent lubricant dosing, thereby improving machine lifespan and environmental compliance.

Advanced machine learning algorithms now process historical equipment data to predict component wear, allowing operators to schedule maintenance based on lubricant degradation patterns rather than fixed intervals. This shift reduces lubricant waste by up to 30% while enhancing equipment reliability. AI platforms are also helping lubricant manufacturers develop next-generation formulations tailored to specific operating environments through simulation-based product testing and accelerated R&D cycles. In addition, robotics-driven lubrication systems powered by AI have improved operational accuracy in automated sawmills, resulting in up to 15% improved operational efficiency.

By embedding AI across the lubricant lifecycle—from formulation to application—stakeholders in the Forestry Lubricants Market are achieving improved sustainability, cost efficiency, and operational agility, especially in regions with volatile environmental conditions and stringent regulatory frameworks.

“In April 2025, a leading forestry machinery OEM deployed an AI-powered lubrication management system across 2,000 logging units in Scandinavia. The rollout resulted in a 22% reduction in unscheduled maintenance events and a 17% improvement in lubricant usage efficiency within six months of implementation.”

The Forestry Lubricants Market is influenced by a complex interplay of environmental, technological, and industrial dynamics. Global emphasis on sustainable forestry practices has increased the demand for biodegradable and low-toxicity lubricants in environmentally sensitive areas. Innovations in synthetic base oils and additive technologies have significantly expanded product durability and resistance to temperature fluctuations, which is critical in forestry operations. Regional policy frameworks promoting eco-compliance, particularly in the EU and Canada, are accelerating the adoption of Environmentally Acceptable Lubricants (EALs). Meanwhile, increased mechanization in forestry operations, especially in Latin America and Asia-Pacific, is driving the volume demand for high-performance lubricant formulations optimized for chainsaws, harvesters, skidders, and forwarders.

The adoption of biodegradable forestry lubricants is rapidly expanding due to global regulatory mandates and end-user demand for environmentally responsible solutions. Bio-based lubricants, derived from vegetable oils and synthetic esters, reduce ecological risks in case of leakage or spillage in forest environments. For example, Sweden and Finland have enforced national forestry codes that require the use of biodegradable lubricants in protected zones. In the U.S., federal and state-level forestry procurement policies now favor eco-labeled lubricants certified under OECD 301 guidelines. As a result, major lubricant manufacturers are investing in bio-refinery capacities and green chemistry to address these regulatory and sustainability requirements. This shift is fostering innovation and increasing the availability of high-performance EALs that perform comparably to conventional mineral oil-based products.

Despite environmental advantages, bio-based forestry lubricants often face limitations in terms of oxidation stability, pour point, and long-term thermal resistance. Forestry operations in extreme climates—such as northern Canada and Russia—require lubricants that maintain performance under sub-zero temperatures and high mechanical loads. Many biodegradable formulations degrade faster and are susceptible to microbial contamination, especially in high-moisture conditions prevalent in logging sites. This performance gap makes operators hesitant to transition fully from mineral-based to eco-friendly alternatives. Additionally, bio-based lubricants generally have higher production costs due to raw material sourcing and formulation complexity, posing an adoption barrier for cost-sensitive segments in emerging markets.

The integration of precision forestry technologies presents a significant opportunity for the Forestry Lubricants Market. Digital mapping, telemetry, and sensor-based control systems used in modern forestry machinery require lubrication systems that can adapt dynamically to workload and environmental conditions. Manufacturers are introducing digitally optimized lubricants compatible with predictive maintenance systems and smart machinery. For instance, digital lubrication management platforms now track lubricant health in real time, alerting operators before critical failure occurs. The increased adoption of autonomous and semi-autonomous forestry equipment in countries like Germany, Canada, and Japan is expected to drive demand for intelligent lubricant solutions with embedded diagnostics and usage analytics. This convergence of digitalization and lubrication science is unlocking new growth avenues across OEMs and aftermarket services.

Navigating the regulatory landscape is a growing challenge for players in the Forestry Lubricants Market. Compliance with international environmental and performance standards such as EU Ecolabel, USDA BioPreferred, and ISO 15380 requires rigorous testing, documentation, and certification processes. These frameworks often differ by region, adding complexity to product approval and market entry strategies. Smaller manufacturers, in particular, face difficulties in meeting these evolving compliance benchmarks due to limited technical expertise and high testing costs. Moreover, increased scrutiny over carbon footprints and lifecycle assessments has placed additional pressure on companies to invest in sustainable sourcing and manufacturing. The need for continuous regulatory alignment and documentation is not only resource-intensive but also limits time-to-market for new product launches.

Surge in Demand for Biodegradable Hydraulic Fluids: The Forestry Lubricants Market is witnessing a sharp increase in demand for biodegradable hydraulic fluids used in logging equipment and forwarders. In 2025, usage of these fluids grew by over 35% in forest zones near water bodies due to regulatory bans on mineral oils. Countries including Austria and Norway now mandate the exclusive use of EALs in environmentally sensitive logging regions, pushing suppliers to ramp up bio-based production capabilities.

Growth of Custom Formulations for Harsh Climates: Lubricant producers are investing in R&D to create custom formulations capable of operating in extreme temperatures and high-moisture environments. In 2025, at least 18 new lubricant variants were launched globally for cold-climate operations, particularly suited for Scandinavian and North American forestry machinery. These products are specifically engineered to retain viscosity and reduce freeze-thaw degradation during sub-zero deployments.

Integration of Lubricant Monitoring IoT Systems: Smart IoT-enabled lubricant monitoring systems are being deployed in heavy forestry equipment to track real-time lubricant condition. By mid-2025, over 14% of new harvester models sold in Europe featured factory-installed sensors for lubricant temperature, viscosity, and contamination level tracking. This development supports predictive maintenance and reduces downtime, enhancing operational efficiency across forest operations.

OEM Collaboration in Sustainable Product Development: Leading OEMs are partnering with lubricant manufacturers to co-develop eco-compliant products tailored to next-gen forestry machinery. In 2024–2025, over six joint development agreements were signed between equipment manufacturers and lubricant formulators. These collaborations are producing synergistic solutions that enhance lubrication efficiency, reduce emissions, and improve compatibility with emission-reducing engine technologies.

The Forestry Lubricants Market is segmented by type, application, and end-user, with each segment contributing uniquely to the market's structure and growth dynamics. On the basis of type, the market includes bio-based, synthetic, and mineral-based lubricants, each tailored to specific operational and environmental requirements. Applications span a broad range of forestry machinery and components, including engines, hydraulics, chainsaws, and bearings, with hydraulic systems accounting for a substantial portion of the demand. From an end-user perspective, the market is influenced by logging companies, timber processing units, government forest management agencies, and equipment manufacturers. Growth is particularly strong among technologically advanced forestry operators who are prioritizing sustainability and machine efficiency. Increasing emphasis on preventive maintenance and environmental compliance across end-user segments is accelerating the adoption of specialty lubricants, while innovation in product development is enabling better alignment with end-use demands and working conditions.

The Forestry Lubricants Market comprises bio-based lubricants, synthetic lubricants, and mineral oil-based lubricants. Among these, synthetic lubricants lead the segment due to their superior performance under extreme temperatures, oxidation resistance, and extended service intervals. They are preferred in high-performance forestry machinery, especially in regions like North America and Scandinavia, where operations face harsh climate variability and continuous-duty cycles.

Bio-based lubricants represent the fastest-growing category, driven by increasing regulatory mandates on environmental safety and biodegradable material use. Their popularity is further supported by expanding reforestation efforts and eco-sensitive logging practices. Advancements in formulation technologies have also enhanced the thermal stability and shelf life of bio-based variants, making them more viable for commercial use.

Mineral-based lubricants, while still widely used in emerging markets due to cost advantages, are gradually losing share in favor of more sustainable options. However, they remain relevant in low-intensity applications and in geographies with limited environmental regulations. Niche formulations are also being developed to improve their environmental profile, keeping them competitive in selected markets.

Forestry lubricants are applied across a range of systems and machinery components including hydraulic systems, engines, saw chains, transmission systems, bearings, and gearboxes. Hydraulic systems dominate the application segment due to the extensive use of hydraulics in forestry equipment such as harvesters, skidders, and forwarders. These systems require constant lubrication to handle heavy loads, high pressure, and variable speed conditions, making them critical consumers of high-performance fluids.

Chainsaw lubrication is emerging as the fastest-growing application area, driven by increased mechanization in small- to mid-scale forestry operations and rising global chainsaw sales. Specialized chain oils with tackifiers and bio-based additives are gaining traction to reduce fling-off and minimize environmental impact during wood cutting and processing.

Other applications such as gear and transmission systems contribute to operational reliability and performance in large-scale mechanized forestry. Lubricants used in bearings and slideways are tailored to handle shock loads and prevent corrosion in outdoor, moisture-heavy environments, further highlighting the diversified lubrication needs across forestry machinery.

In the end-user landscape, commercial logging companies represent the leading segment, as they operate large fleets of machinery requiring constant maintenance and high-performance lubricants. These companies prioritize uptime, equipment longevity, and environmental compliance, thus driving demand for advanced lubricant solutions across harvesting, forwarding, and transportation equipment.

Timber processing units and sawmills form the fastest-growing end-user group. Their growth is supported by expanding global wood product demand and increasing automation in sawing and processing operations. The need for lubricants that can withstand high temperatures, reduce wear, and operate in continuous-duty cycles is pushing innovation in this segment.

Other notable end-users include government forestry departments and reforestation contractors, who increasingly specify biodegradable lubricants in procurement contracts to comply with environmental protection standards. Additionally, OEMs (original equipment manufacturers) are forming partnerships with lubricant producers to pre-specify compatible fluids in new machinery, contributing to aftermarket lubricant consumption and brand loyalty.

North America accounted for the largest market share at 32.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

The Forestry Lubricants Market shows varying dynamics across regions due to differences in industrial forestry practices, environmental regulations, and technology adoption. North America’s leadership stems from its robust logging infrastructure, high equipment mechanization, and strict bio-lubricant usage mandates. Meanwhile, Asia-Pacific’s growth is fueled by rising demand in emerging economies, expanding forestry operations, and increased investment in automated machinery. Europe follows closely behind, driven by sustainability directives and mature forestry sectors. South America and the Middle East & Africa contribute moderately, with potential growth tied to timber exports, energy sector collaboration, and infrastructure development.

North America held 32.4% of the global Forestry Lubricants Market in 2024, supported by extensive commercial logging operations in the U.S. and Canada. Key industries driving demand include timber harvesting, paper manufacturing, and biomass energy. The implementation of stringent EPA and EAL-compliance regulations has led to widespread adoption of bio-based and synthetic lubricants. Additionally, government support for forest sustainability, such as U.S. Forest Service initiatives, has promoted environmentally responsible lubrication practices. Technological transformation is evident with increasing deployment of AI-integrated lubrication monitoring systems and IoT-based predictive maintenance across forestry machinery fleets. Equipment manufacturers in the region are also collaborating with lubricant producers to offer pre-approved, eco-compliant products that reduce downtime and extend operational lifespan.

Europe accounted for 26.8% of the Forestry Lubricants Market in 2024, with major contributions from Germany, Sweden, and Finland. These countries lead the way in implementing sustainable forestry practices, reinforced by policies under the EU Ecolabel and Green Public Procurement frameworks. Forestry operations in this region are highly mechanized, requiring premium lubricant solutions for chainsaws, skidders, and feller bunchers. The EU’s push toward reducing carbon emissions and environmental impact has accelerated demand for biodegradable lubricants. Technological innovation is strong, with German OEMs pioneering AI-enabled lubrication systems for forestry applications. Adoption of low-viscosity synthetic lubricants has also gained traction in cold-weather forestry equipment, particularly in Nordic countries.

Asia-Pacific ranked first in growth potential and contributed 21.3% of the market volume in 2024. China, India, and Indonesia are top consumers, driven by growing construction timber demand, reforestation programs, and increasing use of automated harvesting equipment. Infrastructure expansion, particularly in Southeast Asia, is propelling demand for forestry lubricants in sawmilling and timber processing operations. The region is also witnessing growth in domestic lubricant manufacturing hubs, especially in China, where advancements in synthetic formulations are gaining market traction. Emerging tech adoption, including sensor-driven maintenance and smart lubrication systems, is evident in Japanese and South Korean forestry machinery markets. Regional governments are also incentivizing the use of eco-friendly products, aiding market maturity.

South America accounted for approximately 11.4% of the global Forestry Lubricants Market in 2024, with Brazil and Chile leading in both consumption and production. The continent’s expanding timber export sector, supported by growing demand from North America and Europe, has driven increased usage of lubricants in harvesting and processing equipment. Governments are promoting sustainable forestry certifications, which encourage the adoption of environmentally acceptable lubricants. In Brazil, forestry equipment fleets are being modernized with hydraulic and high-performance lubricant systems to ensure compliance with both domestic and international operational standards. Although infrastructure challenges persist in rural areas, increased private investments are fostering better lubricant distribution networks.

The Middle East & Africa region represented 8.1% of the Forestry Lubricants Market in 2024. Countries like South Africa and the United Arab Emirates are key contributors, with demand supported by diversified forestry, construction, and energy industries. In South Africa, eucalyptus plantations and wood-based manufacturing drive lubricant needs, particularly in chainsaws and hydraulic machinery. The UAE is investing in sustainable construction and landscaping sectors that indirectly boost lubricant demand. Technology modernization is gaining pace through adoption of predictive analytics in machinery maintenance. Meanwhile, trade partnerships and policy support under frameworks like the African Continental Free Trade Agreement are creating new entry points for international lubricant brands targeting eco-friendly forestry applications.

United States – 21.9% Market Share

Strong end-user demand, advanced logging fleet infrastructure, and high adoption of synthetic lubricants support the U.S. dominance in the Forestry Lubricants Market.

China – 16.7% Market Share

High production capacity and expanding forestry equipment manufacturing capabilities make China a leading country in the Forestry Lubricants Market.

The Forestry Lubricants Market is characterized by a competitive landscape consisting of over 60 active global and regional players. Competition is primarily driven by product innovation, eco-compliance, performance differentiation, and strategic geographic expansion. Key players are focusing on developing bio-based and synthetic lubricants that offer enhanced thermal stability and biodegradability, aligning with increasingly strict environmental regulations across Europe and North America.

Companies are engaging in strategic partnerships with OEMs, enabling them to supply factory-approved lubricants tailored to next-generation forestry machinery. Between 2023 and 2024, the market witnessed multiple product launches targeting high-performance applications, particularly in hydraulic systems and chainsaw lubrication. Mergers and acquisitions are also shaping the competitive dynamics, especially as larger players seek to strengthen their presence in fast-growing markets like Asia-Pacific and South America.

Innovation is a key competitive lever, with firms investing in AI-integrated lubrication systems, nanotechnology-based additives, and sensor-compatible formulations. Moreover, companies are prioritizing sustainability certifications and lifecycle assessments to differentiate themselves in government and institutional procurement channels. Overall, the Forestry Lubricants Market is becoming increasingly technology- and compliance-driven, with competition intensifying around product lifecycle performance, environmental impact, and operational efficiency.

FUCHS Petrolub SE

ExxonMobil Corporation

TotalEnergies SE

Klüber Lubrication

Chevron Corporation

Shell plc

Petro-Canada Lubricants Inc.

BP Castrol

Schaeffer Manufacturing Co.

Quaker Houghton

RSC Bio Solutions

Valvoline Inc.

Panolin AG

Technological advancements are playing a central role in redefining product development and application efficiency in the Forestry Lubricants Market. AI-powered lubrication management systems are now widely used to monitor lubricant condition in real time, enabling predictive maintenance that reduces machinery downtime. These systems utilize embedded sensors to track parameters such as viscosity, temperature, and contamination, which can then be analyzed through cloud-based platforms.

Biodegradable formulations, particularly those based on synthetic esters and vegetable oils, have improved significantly in terms of thermal stability and oxidation resistance. This allows them to function effectively under high mechanical stress and in extreme temperatures, addressing one of the key limitations previously faced by eco-friendly products. New additive technologies—such as friction modifiers and anti-wear agents—are being incorporated to enhance load-carrying capacity and reduce wear in high-demand components like hydraulic pistons and saw chains.

In 2024, nanotechnology-based lubricant additives entered commercial forestry applications, offering improved surface protection and extended re-lubrication intervals. Smart lubrication systems are being embedded into OEM forestry machinery, allowing automated lubricant distribution based on workload and environmental conditions. Furthermore, digital twins and simulation tools are being used in lubricant formulation to model lubricant behavior under various operating conditions before field deployment. These technological developments are not only elevating product performance but also enhancing cost-efficiency and compliance across forestry operations globally.

• In March 2024, FUCHS launched a new line of biodegradable hydraulic oils specifically for forestry applications, engineered to maintain performance across extreme temperature swings. Field trials reported a 28% extension in maintenance intervals for skidder and harvester equipment.

• In September 2023, Shell introduced its AI-integrated lubrication management platform across forestry equipment fleets in Canada. Initial results showed a 19% reduction in lubricant waste and a 14% improvement in operational uptime within six months of implementation.

• In January 2024, Klüber Lubrication expanded its production facility in Germany to meet rising demand for high-performance forestry lubricants. The expansion increased production capacity by 25%, targeting supply in European and Nordic markets.

• In December 2023, Petro-Canada Lubricants unveiled a new synthetic chain oil optimized for chainsaw operations in cold climates. The product demonstrated a 35% reduction in fling-off and a 22% decrease in equipment wear during high-frequency cutting operations.

The Forestry Lubricants Market Report provides a comprehensive analysis covering product types, applications, end-users, technology trends, and regional performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report encompasses major lubricant categories including synthetic, bio-based, and mineral-based formulations, with in-depth insights into their usage in key systems such as hydraulics, engines, chainsaws, and gearboxes.

End-user segments analyzed include commercial logging firms, timber processors, government forestry agencies, and OEMs, offering granular detail on procurement behavior and adoption patterns. The study examines recent innovations such as AI-driven lubrication monitoring, biodegradable formulations, sensor integration, and nanotechnology-enhanced lubricants, highlighting their impact on operational efficiency and environmental performance.

Geographically, the report explores both mature and emerging markets, identifying region-specific regulatory frameworks, infrastructure readiness, and consumption patterns. Additionally, it addresses niche market segments like smart sawmill operations and remote forestry services that are increasingly influencing demand dynamics. The scope also includes competitive intelligence with a focus on market structure, key participants, product launches, strategic collaborations, and production expansions. This report serves as a strategic resource for decision-makers seeking to capitalize on market opportunities and navigate technological and regulatory developments shaping the future of forestry lubrication.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 378.0 Million |

| Market Revenue (2032) | USD 567.0 Million |

| CAGR (2025–2032) | 5.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | FUCHS Petrolub SE, ExxonMobil Corporation, TotalEnergies SE, Klüber Lubrication, Chevron Corporation, Shell plc, Petro-Canada Lubricants Inc., BP Castrol, Schaeffer Manufacturing Co., Quaker Houghton, RSC Bio Solutions, Valvoline Inc., Panolin AG |

| Customization & Pricing | Available on Request (10% Customization is Free) |