Reports

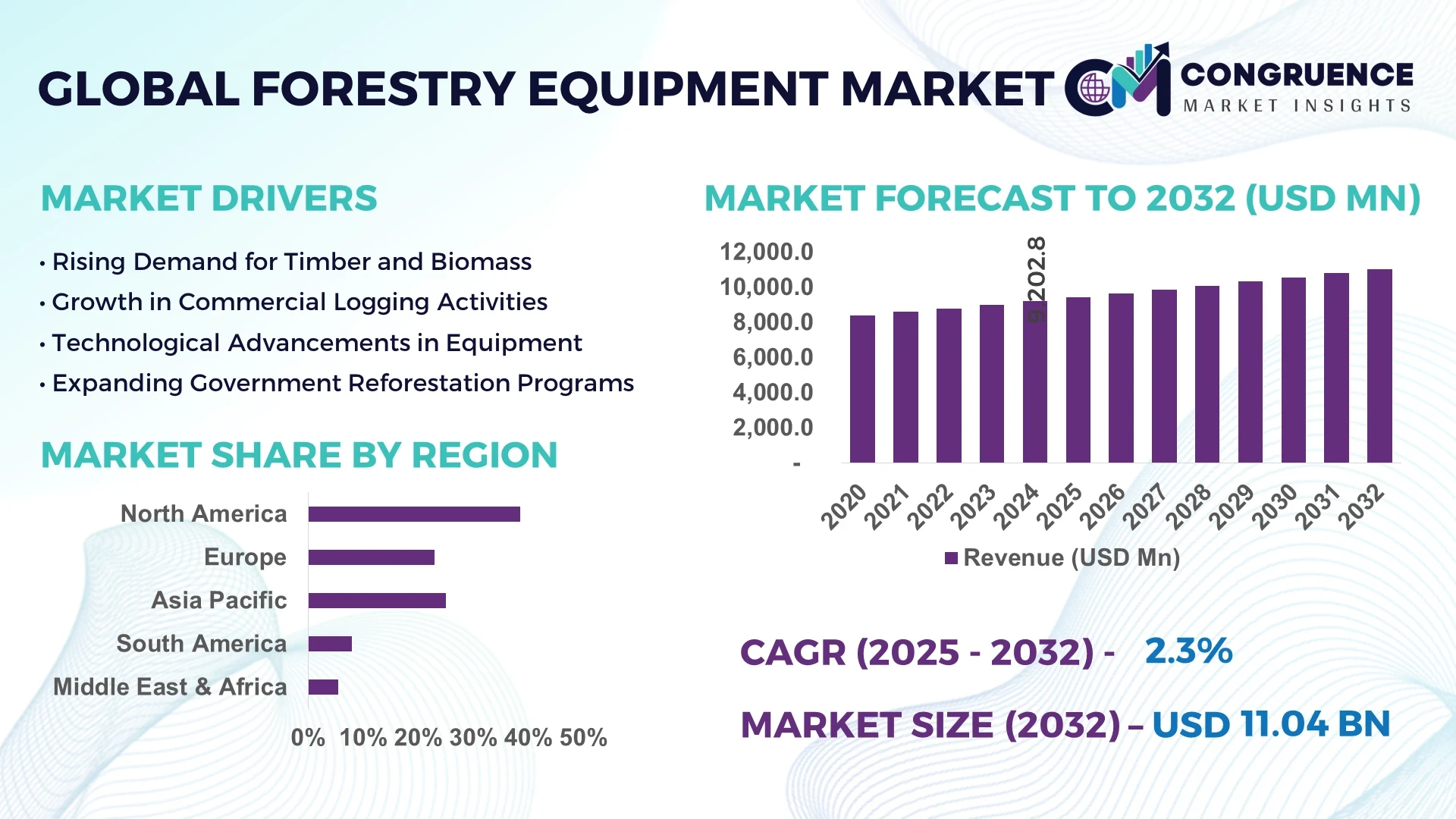

The Global Forestry Equipment Market was valued at USD 9,202.75 Million in 2024 and is anticipated to reach a value of USD 11,038.82 Million by 2032 expanding at a CAGR of 2.3% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

Germany plays a pivotal role in the forestry equipment ecosystem, with advanced engineering facilities, robust R&D investments, and high-volume production capacity in harvesting machinery and logging systems integrated with precision hydraulic control technologies.

The Forestry Equipment Market is experiencing progressive transformation across multiple segments, including logging, site preparation, and silviculture. High adoption rates in the timber harvesting and biomass collection industries have driven significant growth, especially in North America, Europe, and Asia-Pacific. Recent product innovations, such as hybrid-forwarders and low-emission chainsaws, reflect increasing regulatory pressures to meet environmental sustainability standards. Governments are also promoting mechanized solutions in reforestation and afforestation initiatives, intensifying demand for specialized equipment like feller bunchers and skidders. Enhanced connectivity, via IoT sensors, has improved machine utilization tracking and predictive maintenance, driving operational efficiency across forestry applications. Regional consumption patterns reflect a surge in Southeast Asia and Latin America, driven by infrastructure expansion and furniture export industries. Additionally, ongoing climate change mitigation policies and forest conservation programs are influencing equipment modernization. As digitalization deepens across forestry operations, the market is poised for greater demand for technologically integrated, eco-efficient machinery through 2032.

Artificial Intelligence (AI) is reshaping the Forestry Equipment Market by enabling intelligent, precision-based decision-making and automated machinery operations. Through the integration of AI-powered analytics and machine learning algorithms, forestry operators are now optimizing logging patterns, terrain navigation, and equipment performance in real time. This shift is significantly reducing fuel consumption and mechanical wear, especially in remote and rugged forest zones. AI-enhanced forestry equipment, such as autonomous harvesters and vision-based feller bunchers, enables real-time obstacle detection and adaptive maneuverability, minimizing accidents and enhancing workforce safety.

In the modern Forestry Equipment Market, AI facilitates predictive maintenance by monitoring component wear through embedded IoT sensors and forecasting part failures before they result in costly downtime. This contributes to reduced lifecycle costs and improved return on investment for forestry operators. Furthermore, AI algorithms are being leveraged for forest mapping using drone-enabled LiDAR imaging, which offers highly accurate vegetation assessments, tree density evaluations, and yield predictions. These capabilities support more sustainable harvesting cycles and ecosystem preservation strategies. In addition, machine learning supports intelligent log sorting and grading systems that automate wood quality assessment at logging sites, reducing dependency on manual inspection. As digital forestry advances, AI adoption will become a core differentiator for equipment manufacturers aiming to lead in productivity and environmental compliance within the evolving Forestry Equipment Market.

“In 2024, a Scandinavian forestry equipment manufacturer launched an AI-powered harvester system integrated with LiDAR sensors and neural-network processing, which increased wood extraction efficiency by 18% while reducing operational fuel use by 12% across trial sites in Finland’s dense boreal forests.”

Rising mechanization across global timber-producing regions is significantly propelling the Forestry Equipment Market forward. As manual logging becomes less viable due to labor shortages and safety concerns, the adoption of mechanized solutions like feller bunchers, harvesters, and skidders is surging. Countries such as Canada, Sweden, and the United States are leading this transformation by deploying technologically advanced forestry machines equipped with real-time control systems and low-emission engines. In India and China, mechanized tools are being introduced to boost efficiency in state-led afforestation drives. According to industry insights, mechanized harvesting improves productivity by up to 40% while minimizing environmental disruption. Forestry businesses are also investing in all-terrain and remote-control-enabled equipment, which accelerates logging in difficult terrains. This growing reliance on mechanization enhances operational scalability, reduces human risk, and meets sustainability requirements, strengthening the foundation for sustained market growth.

A major challenge in the Forestry Equipment Market is the substantial upfront cost linked to acquiring and maintaining advanced forestry machinery. Modern harvesters, skidders, and forwarders come equipped with high-tech features like GPS mapping, AI-enabled diagnostics, and precision hydraulics, which significantly increase their purchase price. Small and medium-scale forestry operators, especially in developing countries, often struggle to justify the return on investment due to limited operational budgets. Furthermore, maintenance and training costs associated with these complex systems add to the financial burden. In regions where access to financing or leasing models is limited, potential buyers delay upgrades, opting instead for manual or semi-mechanized alternatives. Additionally, replacement parts and technical servicing for branded, high-spec machines remain expensive and localized, hampering long-term equipment utilization. This financial restraint slows technological adoption and can affect productivity, especially in price-sensitive markets.

Government-backed initiatives targeting reforestation, carbon offsetting, and biodiversity conservation are unlocking new growth avenues within the Forestry Equipment Market. Countries including Brazil, Indonesia, and Kenya have launched large-scale afforestation programs supported by international climate finance and public-private partnerships. These initiatives require robust site preparation, planting, and maintenance machinery, creating high demand for specialized equipment like mulchers, brush cutters, and tree planters. In Europe, the EU’s Green Deal is encouraging mechanized reforestation as part of its climate targets, further stimulating market demand. In North America, forest fire prevention programs have led to increased investment in vegetation management equipment. Additionally, sustainable certification programs such as FSC and PEFC are pushing companies toward using advanced logging systems that reduce environmental impact. These policy frameworks and incentives are driving a positive shift toward equipment modernization, presenting lucrative opportunities for manufacturers and distributors in the forestry sector.

One of the pressing challenges in the Forestry Equipment Market is the underdeveloped infrastructure and limited logistics support in emerging forestry zones, particularly in parts of Africa, Southeast Asia, and Latin America. Remote forest sites often lack access roads, machine servicing facilities, and fuel distribution networks, which hinders the efficient operation and maintenance of heavy equipment. Transporting machinery to and from these areas is costly and time-consuming, reducing operational feasibility. Moreover, inconsistent electricity supply and weak communication networks obstruct the implementation of IoT-based monitoring and real-time diagnostics systems. Equipment breakdowns in such isolated locations lead to extended downtime, impacting profitability. Manufacturers and contractors are forced to depend on local, less efficient alternatives or delay deployment, affecting forest management programs and resource extraction timelines. Addressing this challenge requires coordinated investments in rural connectivity, logistics, and localized equipment support systems.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction techniques is driving notable shifts in the Forestry Equipment market. As timber-based structures become more common in commercial and residential sectors, the demand for accurately processed wood products is surging. High-precision equipment such as computerized sawmills and CNC-controlled harvesters are now essential to meet exact dimensional tolerances required in pre-cut and pre-finished components. Europe and North America have witnessed a 22% increase in demand for such advanced machinery due to the rapid scale-up of modular housing and industrial wood-framed buildings. This trend is pushing manufacturers to develop equipment with improved cutting speed, load-handling accuracy, and digital connectivity.

• Expansion of Electrified Forestry Equipment: There is a strong push toward electrification in the Forestry Equipment market, with a growing number of manufacturers introducing battery-electric and hybrid models. These machines offer reduced noise levels, lower maintenance requirements, and zero on-site emissions—making them suitable for use in environmentally sensitive or urban-adjacent forests. In 2024 alone, over 130 electric forestry units were deployed in Scandinavian logging operations. Lithium-ion battery systems are increasingly being paired with lightweight materials and regenerative braking to optimize energy efficiency and extend machine runtimes.

• Integration of Remote Diagnostics and Telematics: Telematics and remote diagnostic systems are becoming standard in modern forestry equipment, enabling real-time monitoring of machine health, fuel usage, and operator performance. These digital tools allow fleet managers to respond proactively to potential failures, significantly reducing equipment downtime. Between 2023 and 2024, adoption of telematics-equipped forestry machinery grew by 28% in large-scale forestry operations. The shift toward connected machinery is also streamlining compliance reporting and improving asset utilization across multinational logging projects.

• Increasing Demand for Multi-Functional Forestry Equipment: The Forestry Equipment market is seeing rising interest in multi-functional machinery that can perform various tasks—such as felling, delimbing, and stacking—within a single operating cycle. This is particularly prominent in emerging markets where budget constraints necessitate maximizing machinery ROI. Multi-head harvesters with modular attachments have seen a 17% increase in demand over the past year, driven by their versatility and reduced operational costs. Manufacturers are responding with equipment designs that allow for rapid tool interchangeability and optimized hydraulic control, supporting efficiency gains in mixed-species and uneven-terrain forests.

The Forestry Equipment Market is segmented into types, applications, and end-user categories, each playing a distinct role in shaping market performance and growth trajectories. In terms of equipment type, core categories include harvesters, forwarders, skidders, feller bunchers, loaders, and others, with evolving preferences driven by terrain, automation levels, and operational scale. Application-wise, the market is primarily driven by logging, site preparation, and forest thinning, while emerging uses in fire management and afforestation are gaining attention. End-user segmentation includes logging contractors, forest management agencies, sawmills, and timber product manufacturers. Each segment reflects varied equipment demands based on functionality, ownership models, and sustainability goals. Increasing mechanization, regulatory compliance needs, and the push for digital forestry practices are significantly influencing purchase behavior across segments. A growing preference for eco-efficient, multi-functional, and connected machinery is noticeable among large-scale operators, while entry-level automation remains a priority for small and medium forestry enterprises, especially in Asia-Pacific and Latin America.

Product segmentation in the Forestry Equipment Market includes harvesters, forwarders, skidders, feller bunchers, loaders, and other specialized tools such as delimbers and mulchers. Harvesters currently lead the market due to their ability to execute felling, delimbing, and bucking in a single operation, making them indispensable in high-volume commercial logging. Their popularity is further fueled by operator safety, precision cutting capabilities, and integration with digital forest planning systems. Forwarders are the fastest-growing type, as demand intensifies for equipment that can transport felled logs with minimal ground disturbance. Their rubber-tired design, fuel efficiency, and increasing automation in load balancing and navigation are making them favorable, especially in forest-sensitive areas of Europe and North America. Skidders maintain relevance in regions with rugged terrain, while feller bunchers are frequently used in controlled harvesting zones due to their speed and handling of clustered trees. Loaders and other attachments continue to find utility in smaller-scale operations and support functions, especially where flexibility is prioritized over specialization.

Within the Forestry Equipment Market, logging operations represent the most dominant application area. The constant global demand for timber in the construction, packaging, and furniture industries is sustaining the requirement for robust, high-capacity equipment suited for felling, processing, and transporting logs efficiently. Logging also requires varied machinery adapted to different forest types, enhancing equipment diversity within this segment. The fastest-growing application is site preparation, driven by increased investments in reforestation, afforestation, and biomass energy projects. Site clearing and terrain preparation are essential for both sustainable forestry and plantation development, leading to growing demand for mulchers, brush cutters, and bulldozers with advanced hydraulic and maneuverability features. Other applications such as forest thinning, fire prevention, and conservation activities are also gaining attention. Equipment used in controlled thinning and underbrush removal is critical for reducing wildfire risks and maintaining ecosystem balance. As sustainability becomes central to forestry strategy, application diversity is expected to expand further in the coming years.

Logging contractors represent the leading end-user segment in the Forestry Equipment Market. These businesses require high-volume, multi-functional machines for intensive harvesting operations, especially in North America and Scandinavia. Their preference for advanced equipment with integrated GPS, telematics, and automation systems is shaping equipment innovation and driving demand for durability and precision in forest operations. Government and forest management agencies are emerging as the fastest-growing end-users. Rising involvement in reforestation, afforestation, and wildfire prevention programs is prompting agencies to procure eco-efficient, specialized machinery for land clearing, vegetation control, and forest restoration. Public funding initiatives and global climate commitments are supporting this growth, especially in Europe, Brazil, and Southeast Asia. Other contributors include timber product manufacturers, who often own or lease forestry equipment to ensure raw material consistency and supply chain control. Sawmills and biomass plants also play a vital role, investing in equipment tailored for log intake, sorting, and processing logistics. This diverse end-user base ensures sustained demand for both entry-level and high-tech forestry machinery across global regions.

North America accounted for the largest market share at 38.5% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 3.2% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

The North American Forestry Equipment Market continues to thrive due to expansive commercial logging operations, well-established infrastructure, and widespread adoption of precision forestry technologies. Meanwhile, Asia-Pacific is emerging as a global growth hub due to increasing afforestation projects, forest conservation programs, and rising demand for timber in rapidly developing economies. Overall, regional shifts are being shaped by government support, ecological regulations, and increasing digital integration across forestry operations.

The Forestry Equipment Market is also benefiting from ongoing electrification, automation, and the growing demand for multi-functional machinery tailored to region-specific needs. As countries focus on sustainable timber harvesting and forest management, there's a significant uptick in demand for environmentally compliant equipment. Innovations in hybrid machines, GPS tracking systems, and telematics-enabled solutions are influencing purchasing behavior across major markets. Additionally, global deforestation policies, bioenergy expansion, and urban development have further amplified the demand for efficient, eco-friendly, and high-performance forestry tools. With countries aligning toward carbon neutrality and sustainable development goals, the Forestry Equipment Market is witnessing dynamic regional expansion and specialization.

Strong Digital Integration Elevates Regional Equipment Demand

North America held the highest regional market share in 2024 at 38.5%, bolstered by the presence of large-scale logging firms and advanced forest management systems. The U.S. and Canada dominate equipment consumption due to their vast commercial forestry operations and high investment in technologically advanced harvesters and forwarders. Government incentives such as cost-sharing programs for equipment modernization and sustainable land management practices have also boosted market activity. The introduction of digital logging platforms, fleet telematics, and real-time tracking tools has significantly enhanced operational efficiency across forest zones. Regulatory frameworks emphasizing carbon capture and sustainable forestry are further accelerating the adoption of eco-efficient forestry equipment.

Advanced Sustainability Measures Driving Equipment Upgrades

Europe accounted for approximately 29.3% of the global Forestry Equipment Market in 2024, with Germany, Finland, and Sweden leading the charge. The region has seen a steady uptick in investment towards electric and hybrid forestry equipment, supported by EU sustainability mandates and national green transition programs. Regulatory bodies such as the European Forest Institute and initiatives like Natura 2000 are shaping policy frameworks that promote mechanized yet environmentally friendly forestry practices. Germany's industrial base is actively adopting AI-integrated harvesters and precision forestry tools, while France and the UK are expanding reforestation and biomass production projects. Technology adoption, especially of IoT-based monitoring systems, is playing a critical role in equipment procurement decisions.

Rapid Urbanization Spurs Demand for High-Capacity Machines

Asia-Pacific is witnessing accelerating momentum in the Forestry Equipment Market, with China, India, and Japan emerging as key growth drivers. The region's market volume expanded significantly in 2024, supported by rising domestic timber demand and infrastructure investments. China has prioritized mechanized logging to reduce labor dependency and increase output in managed forests, while India’s afforestation initiatives under government-led sustainability programs are boosting equipment acquisition. Japan’s adoption of automated thinning machinery and compact harvesters is reshaping small-scale forest operations. Regional technology hubs in China and South Korea are also developing smart forestry solutions, integrating machine vision, and real-time diagnostics into equipment for improved operational control and performance.

Timber Production and Bioenergy Projects Propel Equipment Sales

In South America, Brazil and Argentina are the central players in the Forestry Equipment Market. Brazil alone accounted for approximately 6.9% of global market share in 2024, fueled by its expansive eucalyptus plantations and the booming demand for pulp and bioenergy. Argentina is ramping up sustainable forestry initiatives supported by government subsidies and land-use reforms, encouraging mechanization. Trade agreements within Mercosur and improved infrastructure in logging regions have further supported cross-border equipment deployment. The region is also benefiting from increasing foreign investment and public-private collaborations aimed at enhancing forestry logistics and reducing manual labor dependency through technological modernization.

Strategic Modernization Efforts Reshape the Regional Landscape

The Middle East & Africa region is steadily integrating into the global Forestry Equipment Market, particularly through initiatives in the UAE, South Africa, and Kenya. Local governments are emphasizing reforestation, carbon offsetting, and land rehabilitation, resulting in rising equipment demand for thinning, site preparation, and mulching operations. South Africa remains the region's major contributor, driven by strong construction wood demand and established timber production zones. UAE is investing in digitized forestry programs linked to carbon neutrality goals, creating demand for advanced harvesting and monitoring machinery. Regional demand is further supported by updated trade policies, partnerships with international equipment manufacturers, and the shift toward renewable material sourcing.

United States – 27.4% market share

High production capacity and widespread adoption of smart logging systems support dominance in the Forestry Equipment Market.

China – 16.1% market share

Strong end-user demand from expanding infrastructure and timber industries drives equipment sales across both public and private sectors.

The Forestry Equipment Market is characterized by a moderately consolidated competitive landscape, featuring approximately 30 to 40 globally active manufacturers and a larger base of regional players catering to niche demands. Major companies are competing on the basis of product durability, technological integration, environmental compliance, and operational efficiency. Global leaders are leveraging strategic mergers, long-term supply contracts, and distribution partnerships to solidify their presence in emerging markets such as Southeast Asia and Latin America.

Product innovation remains central to competitive differentiation. Several players have launched electric and hybrid-powered harvesters, forwarders, and skidders in response to rising demand for low-emission forestry machinery. Additionally, firms are integrating advanced telematics, autonomous navigation systems, and AI-powered diagnostic tools to enhance equipment uptime and operator productivity. European manufacturers are increasingly focusing on compact, lightweight designs optimized for plantation thinning, while North American players continue to develop heavy-duty machines tailored to industrial-scale logging operations. The competitive environment is further intensified by growing investments in R&D, sustainability certifications, and aftersales service enhancements, all of which are shaping long-term positioning strategies across global and regional markets.

John Deere Forestry

Komatsu Forest

Ponsse Plc

Tigercat Industries Inc.

Doosan Infracore

Kesla Oyj

Caterpillar Inc.

Eco Log Sweden AB

Husqvarna Group

Sennebogen Maschinenfabrik GmbH

The Forestry Equipment Market is undergoing a significant technological transformation, driven by the integration of precision forestry solutions, automation, and environmentally conscious innovations. Telematics and GPS-enabled tracking systems are now standard features in many modern harvesters and skidders, allowing real-time data monitoring, route optimization, and enhanced operational control. These digital tools enable forestry operators to minimize downtime and optimize fuel usage, significantly improving cost-efficiency in logging operations. Hybrid and electric-powered forestry machines are also gaining traction, particularly in regions with stringent emission regulations. For example, electric harvesters have demonstrated a 20–30% reduction in fuel consumption compared to traditional diesel models. Moreover, battery-powered chainsaws and brush cutters are becoming more popular among smaller-scale operators due to their lower noise levels, reduced maintenance needs, and zero-emission performance.

Artificial Intelligence and machine learning algorithms are being implemented in equipment to support autonomous operations such as obstacle detection, tree species identification, and real-time logging analytics. These smart systems not only enhance safety in remote logging areas but also improve productivity by optimizing harvesting sequences and load distribution. 3D vision systems, LiDAR-based mapping tools, and automated blade control technologies are helping operators conduct selective logging and thinning with higher accuracy. This shift towards precision forestry reflects a broader industry trend toward sustainability, digitalization, and operational excellence.

• In March 2023, Komatsu Forest launched the all-new Komatsu 951XC harvester, a powerful 8-wheel machine designed for steep terrain. The model integrates an advanced hydraulic system that improves fuel efficiency and offers enhanced traction control for challenging forest environments.

• In September 2023, John Deere unveiled its latest JDLink™ connectivity upgrade, enabling real-time data sharing between forestry machines and central operations. This upgrade facilitates predictive maintenance scheduling and improves remote diagnostics, boosting uptime across logging fleets.

• In February 2024, Ponsse introduced a next-gen electric forwarder prototype designed for silent and emission-free operation in urban and conservation-sensitive areas. The machine has completed successful pilot testing in Nordic countries, achieving up to 40% energy savings compared to diesel counterparts.

• In May 2024, Tigercat Industries launched a new H-series feller buncher equipped with advanced boom control technology and a reinforced undercarriage system. This model targets high-volume logging operations and enhances operator comfort with a redesigned, vibration-dampened cabin.

The Forestry Equipment Market Report offers a comprehensive examination of the industry across multiple dimensions, including equipment type, application segments, end-user industries, and geographic regions. The report covers a wide range of machinery used for felling, extraction, processing, and transportation of timber and biomass, including harvesters, forwarders, skidders, feller bunchers, loaders, mulchers, and chainsaws. It also assesses both traditional diesel-powered equipment and emerging electric or hybrid alternatives, with detailed insights into their operational efficiency, design evolution, and environmental adaptability. The scope of analysis extends across key application areas such as logging, biomass harvesting, land clearing, and wildfire management, identifying demand trends among commercial forestry operators, municipal services, and private landowners. It further delves into technological integrations like telematics, automation, AI-based diagnostics, and sustainable engineering solutions being adopted globally.

Regionally, the report evaluates the Forestry Equipment Market across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with country-level detail highlighting consumption patterns, infrastructure growth, and regulatory influences. Niche market segments, including compact forestry equipment and smart-enabled portable tools, are also assessed to capture innovation-led demand pockets. Overall, the report serves as a strategic decision-making tool by mapping the competitive landscape, technology roadmaps, and demand forecasts across a wide range of industrial use-cases and regional dynamics.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 9,202.75 Million |

|

Market Revenue in 2032 |

USD 11,038.82 Million |

|

CAGR (2025 - 2032) |

2.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End‑User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Dutch Plantin Coir India Pvt. Ltd., Riococo Lanka Pvt. Ltd., Jiffy Products International B.V., Kumaran Coirs, Coco Veda India Pvt. Ltd., Fibredust LLC, Samarasinghe Brothers (Pvt) Ltd., Benlion Coir Industries, Lignocel (Pvt) Ltd., Pelemix Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |