Reports

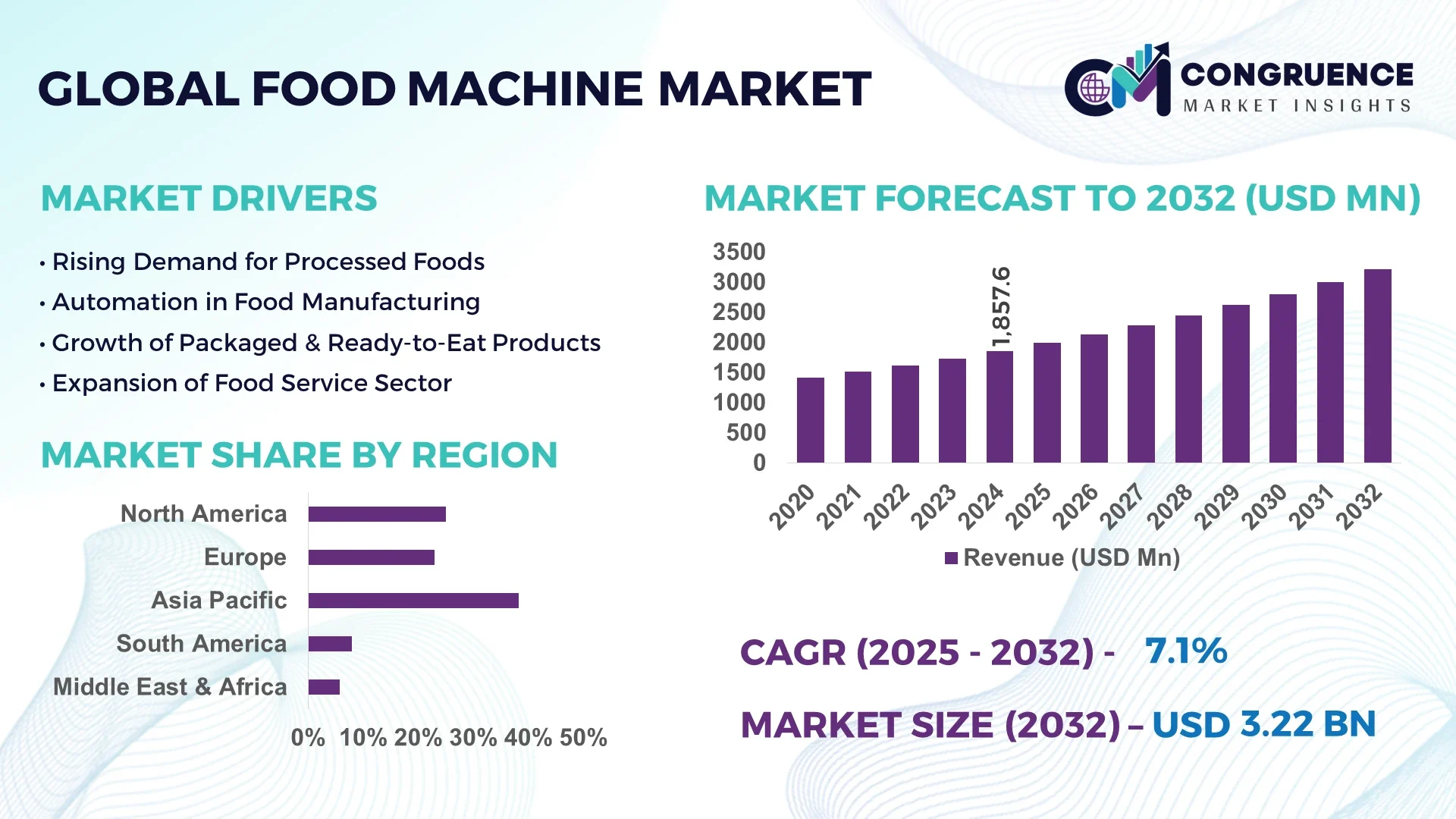

The Global Food Machine Market was valued at USD 1857.63 Million in 2024 and is anticipated to reach a value of USD 3215.7 Million by 2032 expanding at a CAGR of 7.1% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

The United States stands as a pivotal player in the Food Machine market, boasting significant production capacity and high levels of investment in automated and smart food processing equipment. Its industries benefit from advanced robotics integration, particularly in sectors like bakery, meat processing, and dairy production, supported by cutting-edge technological advancements in automation and precision machinery.

The Food Machine Market spans various key industry sectors including packaging, food processing, and ingredient handling, each contributing substantially to overall market growth. Recent innovations focus on enhancing machine versatility, energy efficiency, and hygiene standards, driven by increasing regulatory requirements and consumer demand for safer, higher-quality food products. Environmental factors such as waste reduction and sustainability are shaping product development strategies. Regional consumption patterns highlight robust demand in North America and Asia-Pacific, fueled by expanding food manufacturing sectors and urbanization. Emerging trends include integration of IoT-enabled devices and predictive maintenance technologies, which are expected to further optimize production processes and reduce operational downtime. This dynamic market outlook encourages manufacturers and stakeholders to prioritize innovation and regulatory compliance to maintain competitive advantage.

Artificial intelligence (AI) is revolutionizing the Food Machine Market by significantly enhancing operational efficiency and production accuracy across food processing and packaging lines. Advanced AI-driven sensors and machine learning algorithms enable real-time monitoring and predictive maintenance of food machinery, reducing unplanned downtime and increasing throughput. AI-powered quality control systems can detect product defects and contamination faster than traditional methods, ensuring consistent food safety and reducing waste.

In the Food Machine Market, AI facilitates automation in complex processes such as sorting, cutting, and packaging, where precision and speed are critical. These intelligent machines adapt to variations in raw materials and adjust settings autonomously, improving flexibility in food production. Moreover, AI integration supports data analytics platforms that optimize supply chain management by forecasting demand and managing inventory more effectively. This transformation leads to cost savings and improved resource utilization for food manufacturers. By incorporating AI, the Food Machine Market is evolving towards smart factories where interconnected systems enhance transparency and enable rapid decision-making. Such innovations not only boost productivity but also support sustainability initiatives by minimizing energy consumption and reducing material waste.

“In 2024, a leading food machinery manufacturer launched an AI-enabled predictive maintenance system that reduced equipment failure rates by 30% and extended machine lifecycle by 15%, demonstrating measurable operational improvements within commercial food production environments.”

Automation in the Food Machine Market significantly boosts production efficiency by reducing manual labor and minimizing human error. The growing demand for ready-to-eat and packaged food products globally necessitates faster processing times and improved consistency, which automated food machines effectively provide. Advanced robotics and intelligent sensors integrated into food machines enhance precision in cutting, sorting, and packaging processes. Furthermore, automation helps manufacturers comply with strict hygiene and safety regulations by minimizing direct human contact with food products. This trend has resulted in increased capital investment by food processors seeking to improve throughput and product quality while lowering operational costs.

One major restraint in the Food Machine Market is the high upfront cost associated with acquiring advanced food machinery, including automation and AI-enabled equipment. Many small and medium-sized enterprises (SMEs) face budget constraints that limit their ability to invest in the latest technology. Additionally, maintenance expenses for complex machines require skilled technicians and specialized parts, increasing the total cost of ownership. Frequent equipment downtime due to maintenance needs can disrupt production schedules, impacting profitability. These financial barriers slow down the adoption of innovative food machinery, especially in developing regions where cost sensitivity is higher.

The rising popularity of plant-based and alternative food products creates significant opportunities within the Food Machine Market. Manufacturers require specialized machines capable of processing novel raw materials such as legumes, algae, and protein isolates. This emerging sector demands customized food machines that support texture modification, extrusion, and precision packaging, allowing producers to meet consumer preferences for sustainable and health-conscious foods. Investment in research and development of machinery tailored for alternative food production enables companies to tap into this growing niche. Additionally, expanding vegan and vegetarian consumer bases in North America, Europe, and Asia-Pacific regions further enhance market prospects.

Navigating complex food safety regulations and certification requirements poses a significant challenge for the Food Machine Market. Manufacturers must ensure their equipment complies with multiple regional standards related to hygiene, contamination prevention, and traceability. Failure to meet these regulations can result in costly recalls, legal penalties, and reputational damage. The process of certification often involves rigorous testing and documentation, extending product development cycles. Furthermore, rapid regulatory changes require continuous machine upgrades and operator training, increasing operational burdens. These challenges hinder market players, particularly smaller companies, from swiftly adapting to evolving compliance demands.

Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction methods is transforming production requirements within the Food Machine market. Manufacturers are increasingly investing in automated systems capable of fabricating pre-bent and cut components off-site, which streamlines installation and significantly reduces labor dependency. In Europe and North America, where construction timelines and compliance with hygiene standards are paramount, the demand for high-precision, pre-assembly food machines has increased by over 25% in the past two years. This shift supports lean manufacturing initiatives and enables faster plant expansions and retrofits in the food processing sector.

Surge in Demand for Multi-Functional Equipment: Multi-functional food machines that handle multiple operations—such as mixing, cooking, and packaging—are gaining traction among manufacturers looking to maximize space and efficiency. These machines reduce equipment footprint while improving operational flexibility. In 2024, industry surveys indicated a 40% increase in procurement of modular multifunctional units among mid-sized food producers. This trend reflects the growing preference for compact, scalable systems that adapt quickly to new product lines and small-batch production needs.

Integration of Smart Sensors for Predictive Maintenance: Smart sensor technology is becoming integral in the Food Machine market, enabling predictive maintenance strategies that reduce downtime and improve machine reliability. Machines equipped with AI-driven diagnostics have shown up to a 35% reduction in unexpected mechanical failures. This evolution enhances operational transparency and ensures food safety compliance by preventing contamination risks linked to equipment breakdown. Predictive maintenance adoption is especially strong in Asia-Pacific, where demand for continuous production systems is surging.

Emphasis on Eco-Friendly and Energy-Efficient Systems: Environmental sustainability is now a critical purchasing criterion in the Food Machine market. Manufacturers are increasingly opting for machines that operate with lower energy consumption and incorporate recyclable materials. Recent advancements in heat recovery systems and low-energy conveyors have led to energy reductions of up to 30% in high-capacity food processing facilities. With regulatory pressure mounting and consumer preferences shifting toward eco-conscious brands, energy-efficient machines are rapidly becoming industry standard across both established and emerging markets.

The Food Machine market is segmented into three primary categories: by type, by application, and by end-user. Each segment reflects the market’s evolving nature and technological adaptation. In terms of type, the market includes processing machines, packaging machines, and slicing and cutting machines, with processing equipment dominating due to its broad applicability in various food production stages. Application-wise, food machines are utilized across sectors such as bakery, meat processing, dairy, beverages, and confectionery. Meat processing holds a strong position, while plant-based food production is expanding rapidly. End-user segmentation includes food manufacturing companies, commercial kitchens, institutional facilities, and catering services. Among these, large-scale food manufacturers lead usage, driven by high-volume production demands. Meanwhile, the commercial kitchen segment is gaining momentum due to growing demand for quick-service restaurants and automated cooking solutions. These segmentation insights reveal dynamic usage trends and offer critical understanding for stakeholders optimizing equipment investments across the food processing value chain.

Processing machines represent the leading product type in the Food Machine market, owing to their indispensable role in food production, from initial ingredient preparation to thermal processing. Their broad applicability across multiple food categories—such as dairy, meat, and bakery—positions them as essential infrastructure for manufacturers targeting high-output efficiency. The use of intelligent automation in these machines has further solidified their dominance. Packaging machines are currently the fastest-growing product type, driven by escalating demand for hygienic, shelf-stable, and eco-friendly packaging solutions. With global concerns around food contamination and waste reduction, companies are investing in automated, vacuum-sealing, and modified-atmosphere packaging systems to meet evolving regulatory and consumer requirements. Slicing and cutting machines, while more niche, play a critical role in meat and bakery processing, offering precision and consistency that manual operations cannot match. Additionally, specialized machines such as forming, filling, and mixing systems contribute to niche segments like confectionery and pet food manufacturing, adding diversity to the overall equipment landscape.

Meat processing is the leading application area in the Food Machine market, driven by the global consumption of processed meats such as sausages, nuggets, and deli products. Food machines in this segment support essential functions such as deboning, marinating, and portioning with high efficiency and hygiene compliance. Automation in meat processing lines has drastically improved product consistency and throughput. The fastest-growing application is plant-based food processing. The rise of alternative proteins and vegan diets has pushed manufacturers to innovate in texture modification, extrusion, and blending. The need for machines that replicate meat-like consistency using legumes, soy, and mycoprotein is becoming crucial in this space. Bakery and confectionery also account for significant application share, where precision baking, dough mixing, and chocolate tempering require technologically advanced systems. Dairy and beverage processing continue to utilize large-scale homogenizers, pasteurizers, and fermenters, especially in markets expanding into functional foods and probiotic beverages. Together, these segments form a complex and diverse machinery demand landscape.

Food manufacturing companies remain the dominant end-user segment in the Food Machine market, primarily due to their large-scale, continuous production needs. These companies depend heavily on automated processing lines, robotic packaging systems, and predictive maintenance tools to ensure consistency, efficiency, and regulatory compliance. Their capital investment capabilities allow for early adoption of new machinery technologies, reinforcing their market leadership. Commercial kitchens are the fastest-growing end-user segment, especially with the rapid rise of quick-service restaurants and dark kitchens. These settings prioritize compact, multi-functional, and energy-efficient machines to manage high-turnover meal preparation within limited space and labor resources. Institutional facilities, such as hospitals, universities, and defense services, represent a steady contributor to the market. Their demand is driven by the need for hygienic, bulk food preparation with strict nutritional compliance. Catering services, although smaller in market size, are showing increasing adoption of semi-automated solutions to boost productivity in events and mass food delivery services, contributing to the market's diversification.

Asia-Pacific accounted for the largest market share at 38.2% in 2024, however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.7% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

Asia-Pacific’s dominance stems from the strong food manufacturing infrastructure in China, India, and Japan, as well as growing domestic consumption and export potential. In contrast, the Middle East & Africa region is witnessing rapid investment in food processing technology, driven by food security initiatives and a shift toward localized production. Europe held a 27.5% market share in 2024, supported by automation trends and strict regulatory compliance in food safety. North America, with a 22.3% market share, continues to benefit from strong technological adoption and innovation in packaging and processing machines. South America accounted for approximately 7.8% of the market, fueled by demand from Brazil and Argentina’s expanding agro-processing sector. Regional performance is strongly linked to government incentives, trade liberalization, and demand for precision food manufacturing equipment.

Automation and Compliance Driving Equipment Modernization

North America captured 22.3% of the global Food Machine market in 2024, supported by advanced food processing infrastructure and consistent demand across meat, dairy, and beverage sectors. The U.S. and Canada continue to lead adoption due to early integration of Industry 4.0 technologies such as IoT-enabled packaging systems and predictive maintenance tools. Government bodies such as the FDA have enforced tighter food safety regulations, pushing food manufacturers to invest in compliant, automated machinery. In addition, the growth of the convenience food segment and ready-to-eat meals has fueled demand for slicing, packaging, and thermal processing equipment. Large food brands are adopting modular and smart machines to reduce labor dependency while enhancing operational efficiency. Sustainability concerns have also driven machine upgrades focused on energy efficiency and waste reduction, especially in the frozen food and beverage bottling sectors.

Smart Manufacturing Fuels Sustainable Food Equipment Growth

Europe held a 27.5% market share in the Food Machine industry in 2024, anchored by strong demand from Germany, France, and the United Kingdom. The region is a leader in adopting sustainable practices, with regulatory bodies like the European Food Safety Authority (EFSA) advocating cleaner and more efficient machinery. Germany’s precision engineering and strong export capabilities drive continuous innovations in food processing equipment. France and Italy have invested heavily in bakery and confectionery machinery, while the UK has become a center for robotic food packing lines. EU-wide green initiatives have resulted in increased demand for eco-friendly machines with lower carbon footprints. Advanced technologies like digital twin simulations, AI-driven process optimization, and hygienic machine designs are gaining traction. As sustainability and automation converge, European food manufacturers are proactively updating legacy systems to remain compliant and competitive.

Manufacturing Boom and Consumption Demand Accelerate Equipment Uptake

Asia-Pacific held the largest market share at 38.2% in 2024, making it the global leader in the Food Machine market. China dominates this segment due to its extensive food manufacturing ecosystem and export-oriented production. India follows closely with its rapidly growing packaged food and dairy processing sectors, while Japan contributes significantly through technological innovation and precision equipment demand. Regional demand is driven by a growing middle class, urbanization, and shifting dietary patterns. Food manufacturing clusters in cities like Shenzhen, Pune, and Osaka are rapidly automating to meet both domestic and international standards. Increasing public-private investments in smart factories and digital integration are transforming production lines. Equipment such as vacuum packagers, retort machines, and automated mixing systems are experiencing steep adoption, particularly in frozen foods and nutraceuticals.

Agro-Industrial Development Enhances Machinery Demand

South America represented 7.8% of the Food Machine market share in 2024, with Brazil and Argentina emerging as the two most significant contributors. Brazil's robust agro-processing industry and government support for food exports continue to bolster investment in automated slicing, canning, and packaging machinery. Argentina is investing in dairy and meat processing plants to cater to both local and export markets. Trade policies favoring domestic manufacturing of food products and tax incentives on imported machinery are aiding industry modernization. Infrastructure development projects focused on rural food processing zones are increasing demand for portable and decentralized food machines. Energy sector trends—such as the availability of biogas and biomass—are also pushing manufacturers to adopt machines compatible with alternative fuels. These developments are enabling small- to medium-scale producers to scale operations while complying with safety and hygiene standards.

Diversification and Food Security Propel Equipment Upgrades

The Middle East & Africa is expected to be the fastest-growing region, supported by strong government initiatives focused on food security and industrial diversification. Countries such as the UAE and South Africa are investing in localized food production facilities to reduce import reliance, driving demand for state-of-the-art food machines. The regional focus on long-term sustainability and water-efficient processing systems is encouraging the adoption of energy-saving technologies. Growth in the hospitality and tourism sectors is pushing demand for compact, multi-functional kitchen food machines in hotels and institutional kitchens. Saudi Arabia’s Vision 2030 and South Africa’s agro-processing investment policies are fostering increased uptake of intelligent equipment like robotic packagers and hygienic slicers. Cross-border trade partnerships are also enabling machinery upgrades in emerging markets like Kenya and Egypt, further boosting modernization across the region.

China – 24.6% market share

High production capacity and robust domestic demand for processed food continue to drive China’s leadership in the Food Machine market.

Germany – 17.2% market share

Dominance in precision engineering and consistent export of food machinery solidifies Germany’s position as a global equipment manufacturing hub.

The Food Machine market is highly competitive, with over 450 active players operating globally across various segments, including processing, packaging, handling, and automation. The competitive landscape is characterized by a mix of well-established multinational corporations and regional manufacturers specializing in niche equipment. Leading companies continue to focus on strategic partnerships, particularly with food processing firms and automation technology providers, to broaden their solution portfolios and gain a competitive edge.

Product innovation and modular design are emerging as critical differentiators, with players integrating features like AI-enabled control systems, hygienic machine structures, and energy-efficient operations. Recent trends show a surge in mergers and acquisitions, especially in Asia-Pacific and Europe, where companies aim to strengthen regional footprints and expand manufacturing capabilities. Additionally, geographic expansion into developing regions, particularly in the Middle East & Africa, is driving competition among global players seeking first-mover advantage. The rise of customized and compact food machines for SMEs is also reshaping the competitive dynamics, pushing manufacturers to diversify their product lines. Overall, the market is shifting toward smart, sustainable, and scalable solutions, positioning innovation as a primary driver of competitive success.

GEA Group AG

JBT Corporation

Tetra Laval International S.A.

Marel HF

Buhler Group

Middleby Corporation

Alfa Laval AB

Heat and Control Inc.

SPX FLOW, Inc.

Krones AG

Technological advancements are playing a transformative role in shaping the Food Machine market, with automation, digital control systems, and sustainable engineering becoming essential across all equipment categories. One of the most significant shifts involves the integration of Industry 4.0 technologies, such as Internet of Things (IoT), machine learning, and real-time data analytics. These innovations are enhancing process efficiency, predictive maintenance, and remote monitoring capabilities across both large-scale and small-scale food production setups.

Smart sensors are being increasingly embedded in mixers, conveyors, and packaging machines to ensure precise temperature control, humidity monitoring, and contamination detection. Meanwhile, robotics is gaining momentum in high-speed food packaging and sorting lines, improving hygiene, labor efficiency, and output accuracy. For instance, robotic arms with vision guidance systems are now capable of handling delicate items like fruits and baked goods with minimal damage.

Energy efficiency has also become a core focus, prompting manufacturers to design machines with reduced power consumption, enhanced insulation, and waste-heat recovery mechanisms. 3D printing is being explored for custom components and rapid prototyping in machinery development, cutting down lead times. Furthermore, modular design approaches allow businesses to scale production with minimal machine downtime. These technological upgrades are not just improving operational performance but also aligning with global sustainability and food safety regulations.

• In February 2024, Bühler launched a new high-efficiency pasta production line equipped with intelligent drying and real-time quality sensors. The system increases throughput by 30% while reducing energy consumption by 15%, aligning with the industry's demand for sustainable and cost-effective solutions.

• In September 2023, Marel introduced a robotic cutting platform for fish and poultry that integrates machine learning algorithms for real-time decision-making. The solution enhances yield by 12% and minimizes waste, addressing growing industry concerns around processing efficiency.

• In April 2024, GEA Group AG unveiled its next-generation homogenizers designed for dairy applications. These machines feature smart diagnostics and automatic adjustment modules, leading to 25% less maintenance downtime and improved consistency in high-volume food production.

• In November 2023, JBT Corporation expanded its READYGo™ Clean-in-Place (CIP) system, optimizing sanitation cycles across beverage processing lines. The upgrade allows for a 40% reduction in water usage and a 20% cut in chemical consumption, meeting stricter hygiene and sustainability standards.

The Food Machine Market Report offers a comprehensive analysis of the global landscape, covering a wide array of machinery used in food processing, preparation, packaging, and preservation. It encompasses insights across primary product categories such as mixing machines, cutting and slicing units, sealing and packaging equipment, sterilization and pasteurization systems, as well as advanced robotic and automation tools designed for high-volume food production. The study evaluates both legacy technologies and emerging innovations that support operational efficiency, hygiene compliance, and energy conservation in food manufacturing environments.

Geographically, the report examines key regional markets including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It identifies top-performing countries such as the United States, Germany, China, Brazil, and the UAE, highlighting local market dynamics, industrial growth, and evolving regulatory environments. Each region is analyzed for its unique infrastructure readiness, technological adoption rate, and demand volume across commercial and industrial segments.

From an application standpoint, the scope extends to bakery and confectionery, dairy, meat and seafood, beverages, and ready-to-eat food sectors. Furthermore, the report profiles demand trends among key end-users such as food manufacturers, catering services, retail chains, and institutional food providers. Also covered are niche markets like plant-based food production and allergen-free processing. This report serves as a valuable tool for business leaders evaluating investment, product development, and expansion opportunities across the global food machinery ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1857.63 Million |

|

Market Revenue in 2032 |

USD 3215.7 Million |

|

CAGR (2025 - 2032) |

7.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

GEA Group AG, JBT Corporation, Tetra Laval International S.A., Marel HF, Buhler Group, Middleby Corporation, Alfa Laval AB, Heat and Control Inc., SPX FLOW, Inc., Krones AG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |