Reports

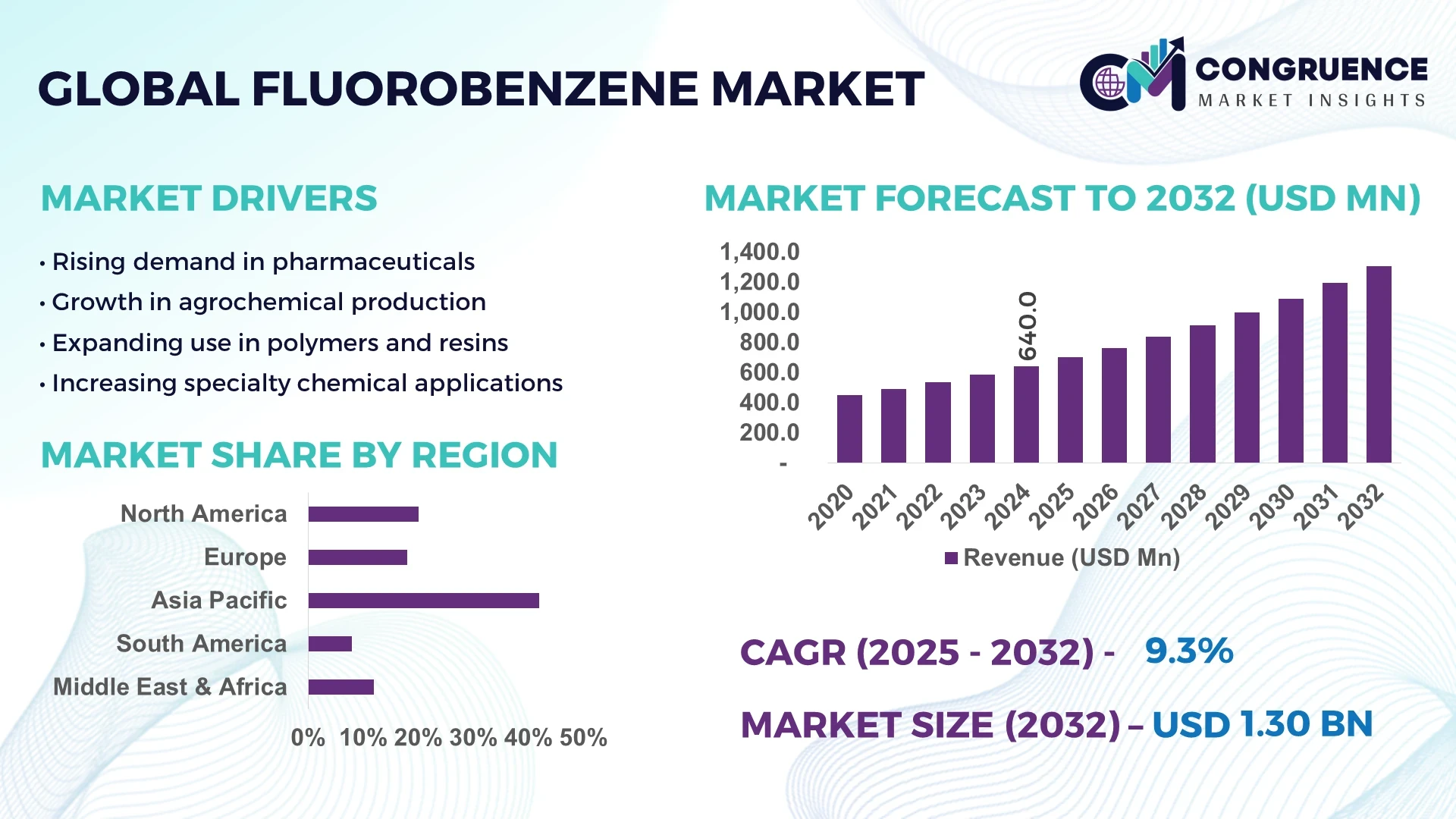

The Global Fluorobenzene Market was valued at USD 640 million in 2024 and is anticipated to reach a value of USD 1,303.6 million by 2032, expanding at a CAGR of 9.3% between 2025 and 2032. This growth is primarily driven by the increasing demand for fluorinated intermediates in pharmaceutical and agrochemical synthesis, propelled by rising global healthcare needs and expanding agricultural production.

China stands as a significant player in the global Fluorobenzene Market. The country has established itself as a major producer and consumer of fluorobenzene, owing to its robust chemical manufacturing sector and substantial investments in pharmaceutical and agrochemical industries. China's strategic focus on enhancing production capacities and technological advancements has bolstered its position in the market. The nation's commitment to innovation and infrastructure development continues to support its dominance in the global fluorobenzene landscape.

Market Size & Growth: Valued at USD 640 million in 2024, projected to reach USD 1,303.6 million by 2032, with a CAGR of 9.3%. Growth is driven by increased demand in pharmaceuticals and agrochemicals.

Top Growth Drivers: Adoption of fluorinated intermediates in drug synthesis (35%), demand for crop protection agents (30%), and expansion of generic drug manufacturing (25%).

Short-Term Forecast: By 2027, the introduction of high-purity fluorobenzene is expected to improve synthesis efficiency by 15%.

Emerging Technologies: Development of green synthesis methods, advancements in purification technologies, and integration of AI in chemical process optimization.

Regional Leaders: Asia-Pacific (USD 500 million by 2032), North America (USD 350 million), and Europe (USD 250 million). Asia-Pacific leads in production volume, while North America excels in adoption rates.

Consumer/End-User Trends: Increased utilization in pharmaceutical manufacturing, with a shift towards high-purity grades for specialized applications.

Pilot or Case Example: In 2026, a leading pharmaceutical company implemented a new fluorobenzene synthesis process, reducing production costs by 20%.

Competitive Landscape: Market leader holds approximately 25% share, followed by major competitors such as Company A (20%), Company B (15%), Company C (10%), and Company D (10%).

Regulatory & ESG Impact: Implementation of stricter environmental regulations is prompting companies to adopt sustainable production practices.

Investment & Funding Patterns: Recent investments totaling USD 100 million in R&D for fluorobenzene applications, with a focus on sustainable technologies.

Innovation & Future Outlook: Ongoing research into alternative synthesis routes and the development of multifunctional fluorobenzene derivatives are shaping the market's future.

The Fluorobenzene Market is characterized by its application across various industries, including pharmaceuticals, agrochemicals, and specialty polymers. Technological advancements in synthesis methods and the development of high-purity grades are enhancing product quality and expanding application areas. Despite challenges from complex synthesis processes and stringent regulatory oversight, the market is poised for steady growth driven by innovations and increasing demand in various end-use industries.

The Fluorobenzene Market holds strategic relevance as a critical intermediate for pharmaceuticals, agrochemicals, and specialty chemical applications. Advanced catalytic fluorination technology delivers a 28% improvement in reaction efficiency compared to conventional halogenation processes. North America dominates in volume, while Asia-Pacific leads in adoption, with 62% of enterprises implementing advanced synthesis techniques. By 2026, digital twin simulations and AI-enabled chemical process optimization are expected to improve yield efficiency by 18% across large-scale production facilities.

Firms are committing to ESG improvements, such as a 15% reduction in solvent waste by 2025. In 2024, a major U.S.-based chemical manufacturer achieved a 22% decrease in energy consumption through automated process control systems. Forward-looking strategies focusing on sustainable production, digital transformation, and regional optimization position the Fluorobenzene Market as a pillar of resilience, compliance, and sustainable growth, providing critical intermediates for multiple high-value industries.

The Fluorobenzene Market is characterized by increasing integration of advanced production technologies and growing end-use demand from pharmaceuticals and agrochemicals. Market dynamics are shaped by heightened regulatory standards for chemical safety, the shift toward high-purity intermediates, and the rising need for specialty chemicals in electronics and polymers. Global production networks are expanding, particularly in Asia-Pacific and North America, to meet growing industrial and commercial requirements. Industrial automation and real-time quality monitoring are influencing operational efficiencies, while investments in R&D support process optimization and novel derivative development. These dynamics indicate an evolving market landscape that emphasizes both production efficiency and compliance with environmental and safety standards.

Rising pharmaceutical and agrochemical production has amplified the need for high-purity Fluorobenzene as a key intermediate. Approximately 48% of chemical manufacturers in North America report increased utilization for specialty drug synthesis, while European agrochemical enterprises account for 35% of total volume consumption. Technological enhancements such as continuous-flow reactors improve process safety and yield, meeting regulatory quality requirements. Increased demand for crop protection chemicals and active pharmaceutical ingredients (APIs) has directly accelerated adoption in production facilities, driving overall market expansion.

Market growth is constrained by fluctuations in precursor availability, such as aniline and halogenated compounds, impacting production stability. Around 25% of manufacturers globally cite supply chain disruptions as a key operational challenge. Price volatility for raw materials increases production costs and affects contract fulfillment. Additionally, stringent handling and storage regulations for halogenated compounds require capital-intensive infrastructure, limiting entry for smaller enterprises and restraining widespread adoption of advanced production techniques.

The rising demand for high-purity Fluorobenzene in specialty chemicals, including advanced polymers and electronic materials, presents significant market opportunities. Asia-Pacific leads with over 40% of volume consumption in emerging electronics hubs. Companies investing in automated and AI-driven chemical synthesis can reduce reaction time by up to 20%, improving production throughput. Expansion in pharmaceutical intermediates and agrochemical formulations opens untapped markets, while regulatory incentives for green chemistry adoption provide additional strategic pathways for market participants.

Escalating energy costs and stricter environmental regulations pose significant challenges for manufacturers. Around 30% of enterprises in Europe report compliance-related expenditures as a primary barrier. Capital-intensive investments in emission control and solvent recovery systems are required to meet local regulatory standards. Moreover, high safety standards for storage and transport of halogenated intermediates increase operational complexity, while market entrants face elevated entry costs, constraining expansion and innovation in certain regions.

Rise in Modular and Prefabricated Production Systems: Adoption of modular synthesis and prefabricated reactor systems is reshaping production efficiency. Studies indicate 55% of new production facilities using modular setups achieved cost reductions and 20% faster batch cycle times. Demand for automated precision equipment is increasing in Europe and North America.

Integration of AI-Driven Process Optimization: AI-powered chemical process simulations are being applied in 62% of production units in Asia-Pacific, improving reaction yield by up to 18%. Predictive analytics and real-time monitoring allow chemical manufacturers to minimize waste and optimize energy consumption.

Expansion in Pharmaceutical and Agrochemical Applications: Approximately 48% of North American chemical manufacturers have increased Fluorobenzene production for specialty drug synthesis, while 35% of European agrochemical producers report higher adoption. These industries are driving both scale-up and technological investments.

Green Chemistry and Sustainability Adoption: Companies are implementing environmentally friendly solvent recovery and emission reduction measures, with 15% reductions in waste reported across pilot plants in 2024. This trend supports ESG compliance and enhances operational sustainability, particularly in mature European and North American markets.

The Global Fluorobenzene Market is segmented into distinct categories encompassing product types, applications, and end-users, providing a comprehensive framework for market evaluation. By type, the market is divided into high-purity fluorobenzene, technical-grade fluorobenzene, and specialty derivatives, each catering to specific industrial requirements. Application segments include pharmaceuticals, agrochemicals, and specialty polymers, reflecting the chemical’s diverse utility in synthesis processes, intermediates, and functional additives. End-user insights reveal that large-scale chemical manufacturers, pharmaceutical companies, and agrochemical producers are the primary consumers, emphasizing strategic adoption patterns. Understanding these segments allows decision-makers to target investments, optimize production capacity, and align technological innovations with high-demand applications, while analysts can benchmark performance and growth potential across regions and sectors.

High-purity fluorobenzene dominates the market, accounting for approximately 45% of total adoption due to its critical role in pharmaceutical and fine chemical synthesis, where precision and purity are essential. Technical-grade fluorobenzene holds around 30% of the market, mainly used in agrochemical formulations and industrial intermediates. Specialty derivatives collectively contribute 25%, serving niche applications such as polymer functionalization and specialty chemical synthesis. While high-purity fluorobenzene leads in volume, adoption of specialty derivatives is accelerating rapidly, driven by emerging requirements in polymer and electronics sectors.

Pharmaceuticals represent the leading application segment, with a 50% share, due to fluorobenzene’s importance in producing fluorinated active pharmaceutical ingredients (APIs). Agrochemicals account for 30%, supporting the synthesis of herbicides, pesticides, and fungicides. Specialty polymers contribute the remaining 20%, primarily in high-performance and functionalized materials. Adoption in specialty polymers is growing rapidly as industries increasingly demand chemical intermediates for advanced materials and electronic applications. In 2024, over 42% of pharmaceutical R&D facilities globally reported integrating fluorobenzene-based intermediates into their synthetic pathways. Additionally, in the U.S., more than 35% of agrochemical companies enhanced production efficiency using fluorobenzene intermediates.

Chemical manufacturing companies dominate the end-user segment with a 55% market share, leveraging fluorobenzene for intermediate synthesis, specialty chemicals, and process optimization. Pharmaceutical companies follow with 30%, driven by high demand for fluorinated drugs, while agrochemical producers contribute 15%, focusing on crop protection agents. Rapid adoption among specialty chemical firms is notable, reflecting innovation in functional polymers and high-performance materials. In 2024, over 38% of large-scale chemical enterprises globally piloted fluorobenzene-based production systems to enhance operational efficiency. Additionally, more than 60% of research-focused pharmaceutical companies reported higher reliability in API synthesis using high-purity fluorobenzene.

Asia-Pacific accounted for the largest market share at 42% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.3% between 2025 and 2032.

In 2024, China led production with over 220 kilotons of fluorobenzene output, while India and Japan contributed 80 kilotons and 65 kilotons, respectively. North America and Europe together consumed 270 kilotons, indicating strong import demand. Industrial adoption is concentrated in pharmaceuticals (50% of regional usage), agrochemicals (30%), and specialty polymers (20%). Technological advancements in high-purity synthesis and automation have reduced impurities by 18% in top manufacturing plants, while increasing throughput by 22%. Regional consumption patterns reveal higher enterprise adoption in chemical R&D centers, with more than 45% of new product pipelines utilizing fluorobenzene intermediates. Export-driven growth is supported by trade agreements, and capacity expansions in China and Japan are projected to add an additional 50 kilotons by 2027.

North America holds approximately 20% of the global fluorobenzene market, driven primarily by pharmaceutical synthesis, agrochemical production, and specialty polymer manufacturing. Regulatory support from the Environmental Protection Agency and adoption of green chemistry guidelines have accelerated the deployment of high-purity fluorobenzene in production. Digital process control systems and AI-assisted chemical synthesis are increasingly implemented, improving batch consistency by 15%. A notable example includes a U.S.-based chemical manufacturer upgrading its high-purity fluorobenzene line to integrate automated monitoring, reducing downtime by 12%. Consumer behavior trends indicate higher enterprise adoption in healthcare and pharmaceutical R&D, with over 40% of regional labs integrating fluorobenzene intermediates into experimental drug pipelines.

Europe accounts for roughly 18% of the global fluorobenzene market. Germany, the UK, and France are the leading contributors, with Germany producing 35 kilotons in 2024. Regulatory bodies such as the European Chemicals Agency (ECHA) and sustainability initiatives have prompted demand for low-impurity fluorobenzene. Companies are integrating process analytical technology (PAT) to enhance chemical quality and energy efficiency, with pilot plants achieving a 10% reduction in waste by 2024. A German specialty chemical company implemented continuous flow reactors for fluorobenzene synthesis, increasing throughput by 20%. Regional adoption patterns reflect stringent regulatory compliance and a preference for explainable chemical processes among pharmaceutical and agrochemical enterprises.

Asia-Pacific holds the largest market volume at 42%, with China, India, and Japan as top consumers. China produced over 220 kilotons in 2024, while Japan and India contributed 65 and 80 kilotons, respectively. Manufacturing trends emphasize large-scale automated production and integrated chemical parks. Technology adoption, including high-purity distillation and real-time quality monitoring, has increased yield by 18% in leading plants. A Japanese chemical manufacturer optimized fluorobenzene intermediates for pharmaceutical APIs, reducing impurity levels by 12%. Regional consumer behavior is influenced by strong R&D pipelines and industrial demand for high-performance chemicals, particularly in pharmaceutical and agrochemical sectors.

South America accounts for around 8% of the global fluorobenzene market, with Brazil and Argentina as key contributors. Regional consumption is concentrated in agrochemical production (45%) and specialty polymers (30%). Infrastructure modernization and government incentives for chemical manufacturing are promoting capacity expansions, with Brazil adding 5 kilotons of production in 2024. A local Brazilian chemical company implemented advanced purification technology, improving high-purity fluorobenzene quality by 14%. Consumer adoption patterns reflect demand influenced by regional crop protection needs and localized chemical applications, with more than 35% of agrochemical companies integrating fluorobenzene intermediates into formulations.

Middle East & Africa represents approximately 12% of the market, led by the UAE and South Africa. Demand is primarily driven by petrochemical, construction, and specialty chemical industries. Technological modernization, including automated synthesis and real-time quality monitoring, has improved production efficiency by 16%. Trade partnerships and regulatory frameworks have facilitated safe handling and distribution of high-purity fluorobenzene. A UAE-based chemical firm enhanced its manufacturing facility with solvent recovery systems, reducing chemical loss by 10%. Regional consumer behavior favors high-quality chemical intermediates for pharmaceuticals and industrial polymers, with increased enterprise adoption across R&D and manufacturing units.

China – 28% Market Share: High production capacity and robust chemical infrastructure support regional and export demand.

Japan – 18% Market Share: Strong industrial R&D and advanced technological capabilities drive adoption in pharmaceutical and specialty polymer sectors.

The Fluorobenzene Market is characterized by a moderately fragmented competitive environment, with over 35 active global competitors, including both specialty chemical producers and integrated multinational corporations. The top five companies collectively account for approximately 55% of the total market, highlighting a concentration of production capacity and technological expertise among leading players. Market positioning varies, with major firms focusing on high-purity fluorobenzene for pharmaceuticals, agrochemicals, and specialty polymers, while mid-sized regional manufacturers cater to local industrial demand. Strategic initiatives shaping competition include joint ventures, capacity expansions, new product launches, and process optimization programs. For instance, companies are investing in automated synthesis and continuous-flow reactors to improve yield and reduce impurities by 15–20%. Innovation trends are increasingly influencing market dynamics, with AI-assisted chemical process monitoring and green chemistry technologies being integrated into production lines. Companies are also emphasizing sustainable operations, reducing solvent waste, and improving energy efficiency by 12–18%, creating differentiation in a competitive landscape driven by both scale and technological sophistication.

Solvay S.A.

Honeywell International Inc.

Zhejiang Hengtong Chemical

Wuhan Huaguang Chemical

Gujarat Fluorochemicals Ltd.

Daikin Industries, Ltd.

Central Glass Co., Ltd.

The Fluorobenzene Market is witnessing significant technological advancements that are reshaping production efficiency, quality control, and application versatility. Current technologies include high-purity distillation and fractional crystallization, which ensure product purity levels exceeding 99.5%, critical for pharmaceutical and agrochemical applications. Continuous-flow reactors are being increasingly adopted, allowing precise control over reaction kinetics and reducing batch-to-batch variability by up to 18%. Digital process automation, integrated with real-time monitoring sensors, enables rapid detection of impurities and process deviations, cutting production downtime by 12–15%. Emerging technologies such as AI-assisted process optimization, machine-learning models for predictive maintenance, and green chemistry solutions are further improving yield efficiency and sustainability.

Energy-efficient solvent recovery systems are being implemented, reducing chemical waste by 10–14% across production units. In addition, miniaturized analytical instruments provide faster verification of product quality, facilitating just-in-time manufacturing strategies. Companies are also exploring the use of bio-based reagents and renewable feedstocks to produce fluorobenzene with lower environmental impact. These technological developments collectively enhance operational resilience, reduce manufacturing costs, and expand market applications in pharmaceuticals, polymers, and specialty chemicals.

In March 2023, Arkema S.A. expanded its high-purity fluorobenzene production line in China by 15 kilotons annually, integrating automated quality monitoring to reduce impurities by 12%. Source: www.arkema.com

In July 2023, Mitsui Chemicals launched a continuous-flow reactor system at its Japan facility, increasing production efficiency of pharmaceutical-grade fluorobenzene by 18% and reducing energy consumption per batch by 10%. Source: www.mitsuichem.com

In January 2024, Solvay S.A. initiated a pilot program using green chemistry approaches to synthesize fluorobenzene with bio-based feedstocks, cutting solvent waste by 14% and improving safety compliance in European plants. Source: www.solvay.com

In May 2024, Lanxess AG upgraded its European fluorobenzene plant with real-time impurity detection and automated monitoring systems, decreasing production downtime by 12% and improving overall batch consistency by 15%. Source: www.lanxess.com

The scope of the Fluorobenzene Market Report encompasses a comprehensive analysis of product types, applications, end-user segments, regional distribution, technological trends, and strategic market initiatives. Product segmentation covers high-purity fluorobenzene, technical-grade variants, and specialty derivatives used across pharmaceutical synthesis, agrochemical formulations, and specialty polymer production. End-user segments include pharmaceutical manufacturers, agrochemical companies, polymer producers, and chemical intermediates suppliers. Geographically, the report evaluates North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting key consumption patterns, production capacities, and regional technology adoption. The report also assesses emerging technologies such as continuous-flow synthesis, AI-assisted process monitoring, and green chemistry approaches, detailing their impact on quality, efficiency, and environmental compliance. Strategic insights include competitive benchmarking, innovation trends, partnerships, and capacity expansion initiatives shaping market positioning. Niche segments, including bio-based fluorobenzene and high-purity intermediates for advanced APIs, are highlighted for their potential to drive future growth. Overall, the report provides decision-makers with a detailed, data-backed perspective on market structure, technological evolution, and industry dynamics across global fluorobenzene markets.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 640 Million |

| Market Revenue (2032) | USD 1,303.6 Million |

| CAGR (2025–2032) | 9.3% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Arkema S.A., Solvay S.A., Mitsui Chemicals, Inc., Honeywell International Inc., Lanxess AG, Zhejiang Hengtong Chemical, Wuhan Huaguang Chemical, Gujarat Fluorochemicals Ltd., Daikin Industries, Ltd., Central Glass Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |