Reports

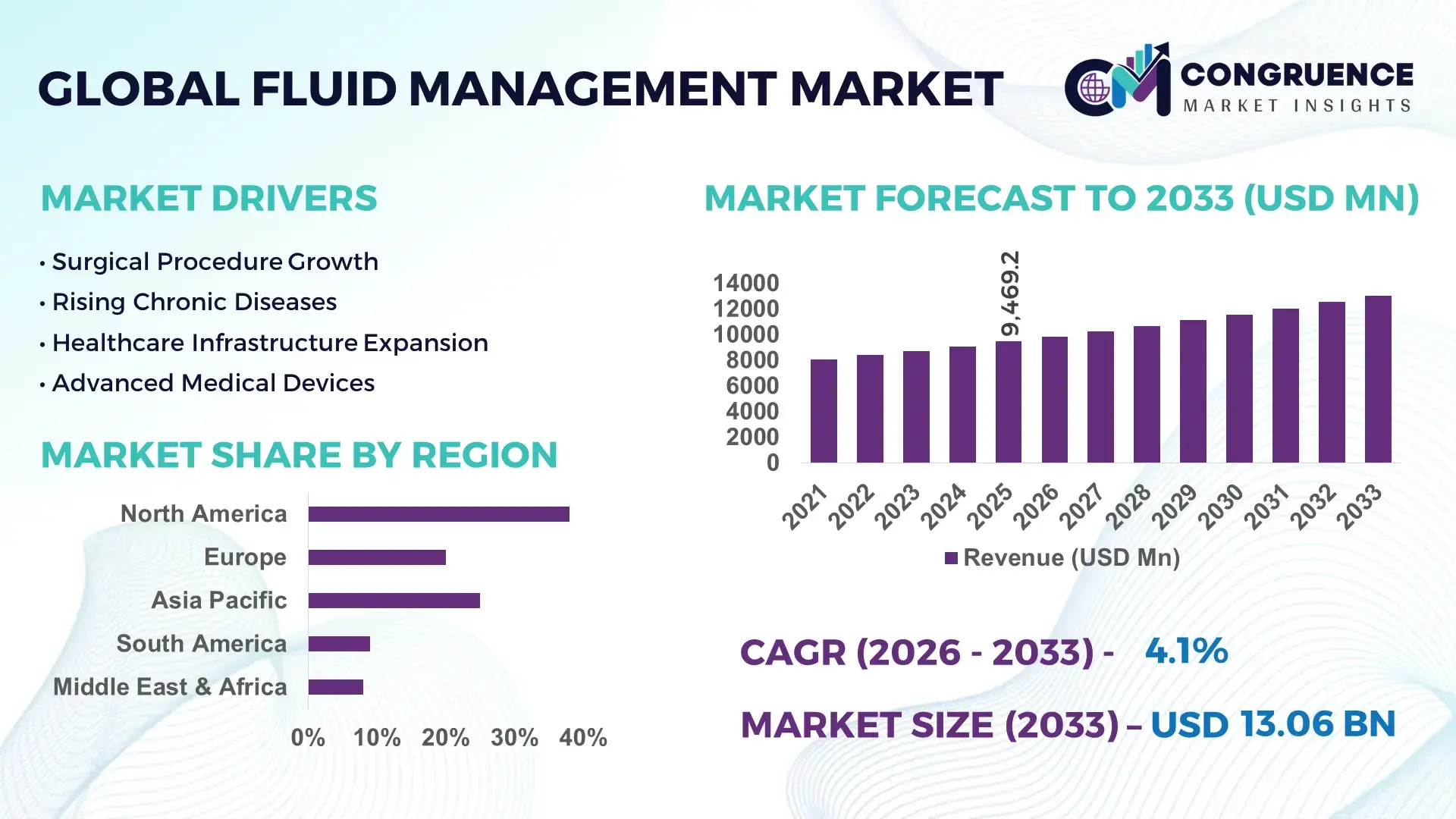

The Global Fluid Management Market was valued at USD 9469.2 Million in 2025 and is anticipated to reach a value of USD 13059.28 Million by 2033 expanding at a CAGR of 4.1% between 2026 and 2033.

Growth is being directly driven by the transition toward closed-loop fluid systems and automation-integrated infusion technologies, improving clinical accuracy by over 18% compared to conventional manual systems. The 2024–2026 period reflects tightening medical device regulations and supply chain localization efforts, particularly in response to post-pandemic procurement reforms and cost-containment policies across major healthcare economies.

The United States remains the dominant market, accounting for approximately 38% of global demand, supported by over USD 2.5 billion in annual investments in hospital infrastructure modernization and digital healthcare integration. High adoption of smart infusion pumps exceeds 65% across large healthcare facilities, compared to under 40% in emerging markets, highlighting a clear technological disparity. The country’s strong presence of advanced surgical centers and aging population base further accelerates utilization rates. In comparison, Asia-Pacific demonstrates faster installation growth exceeding 9% annually, driven by expanding private healthcare networks and localized manufacturing capabilities. Strategically, companies prioritizing automation-enabled fluid control systems and regional manufacturing alignment are positioned to capture sustained value in a moderately expanding but innovation-driven market.

Market Size & Growth: USD 9469.2M (2025) to USD 13059.28M (2033) with 4.1% CAGR, driven by 18% efficiency gains from automated fluid systems

Top Growth Drivers: Automation adoption +22%, surgical procedure volume +15%, hospital infrastructure expansion +12%

Short-Term Forecast: By 2028, operational efficiency improves by 14% with smart fluid monitoring integration

Emerging Technologies: AI-enabled infusion control, closed-loop systems, and antimicrobial fluid pathways improving safety by 20%

Regional Leaders: North America USD 4.8B (>65% adoption), Asia-Pacific USD 3.6B (9% capacity growth), Europe USD 2.9B (regulatory-driven upgrades)

Consumer/End-User Trends: Over 58% of hospitals shifting to digital fluid tracking systems to reduce manual errors

Pilot/Case Example: 2025 deployment reduced fluid waste by 17% and improved surgical turnaround by 11%

Competitive Landscape: Leading player holds ~21% share; top firms focus on automation, disposables, and integration

Regulatory & ESG Impact: Compliance upgrades increase replacement cycles by 13% while reducing waste by 10%

Investment & Funding: Over USD 1.2B invested in smart device innovation and localized manufacturing expansion

Innovation & Future Outlook: IoT-enabled fluid ecosystems and predictive monitoring driving next-gen efficiency standards

Healthcare facilities contribute nearly 46% of total demand, followed by surgical centers at 28% and diagnostic laboratories at 14%, reflecting concentrated usage in critical care environments. Recent innovations include sensor-based fluid monitoring systems improving accuracy by 19% and disposable fluid management kits enhancing infection control by 15%. Asia-Pacific demand is rising steadily with over 10% annual expansion, supported by regional manufacturing shifts and cost optimization strategies. The increasing integration of connected devices signals a transition toward predictive fluid management, shaping the next phase of operational efficiency and strategic investment decisions.

Fluid management systems are rapidly becoming a critical control point in modern healthcare delivery, directly influencing surgical precision, infection control, and operational efficiency, which positions the market as a high-priority investment area. The shift toward digitally integrated and automated fluid ecosystems is accelerating competitive differentiation, particularly as hospitals prioritize outcome-based performance metrics and cost optimization. A key pressure point shaping this market is the tightening regulatory landscape combined with supply chain localization, forcing manufacturers to redesign sourcing strategies and accelerate regional production capabilities.

Advanced closed-loop fluid management systems improve efficiency by 18% while reducing operational costs by 14% compared to legacy gravity-based or manual systems, fundamentally transforming workflow reliability. North America leads in volume, accounting for over 38% of total installations, while Asia-Pacific leads in adoption acceleration and innovation deployment with over 11% annual system upgrades driven by private healthcare expansion and domestic manufacturing incentives. Over the next 2–3 years, digital fluid monitoring penetration is set to increase by 16%, reducing procedural errors by nearly 12% and improving surgical throughput.

Sustainability is emerging as a competitive lever, with advanced disposable systems reducing medical fluid waste by 15%, enabling both compliance alignment and cost savings. A 2025 hospital network implementation demonstrated a 17% reduction in fluid wastage alongside a 10% improvement in procedural turnaround time, reinforcing real-world ROI. Companies are actively shifting capital allocation toward smart device integration, regional assembly hubs, and strategic partnerships to strengthen supply resilience. Organizations that aggressively optimize automation, sustainability, and localized production are securing long-term competitive positioning in a market that is steadily transforming into a precision-driven, efficiency-focused ecosystem.

The core growth engine of the fluid management market is the accelerating shift toward automation-integrated systems combined with rising procedural volumes across healthcare infrastructure. Automated fluid management solutions are improving accuracy by over 18% and reducing manual intervention by nearly 22%, directly enhancing patient safety and workflow efficiency. A significant structural shift is the global expansion of surgical procedures, increasing by approximately 14%, which is intensifying demand for precision-based fluid systems. Additionally, supply chain restructuring post-2024 has pushed manufacturers to localize production, particularly in Asia-Pacific, where capacity expansion exceeds 10% annually. This transformation is forcing companies to respond aggressively through capacity expansion, increased R&D investment, and strategic collaborations with healthcare providers. The cause is clear: rising procedural complexity and regulatory compliance requirements are demanding higher system reliability, leading to accelerated adoption of automated solutions. The impact is measurable in reduced error rates and improved throughput, while business response is focused on scaling smart system deployment and forming ecosystem partnerships to strengthen market penetration.

Despite strong demand momentum, the market faces structural limitations driven by high dependency on specialized raw materials and components, which account for nearly 35% of system costs. Price volatility in polymers and medical-grade materials has increased procurement costs by over 12%, directly affecting margin stability. Regulatory pressures are also intensifying, with compliance requirements extending product approval timelines by approximately 20%, delaying market entry for new technologies. A critical real-world constraint is the concentration of component manufacturing in limited geographies, exposing the market to supply disruptions. These factors are constraining scalability and forcing companies to absorb higher operational costs or pass them downstream. In response, leading players are diversifying supply chains, securing long-term procurement contracts, and investing in alternative materials to mitigate risk. Additionally, companies are redesigning product architectures to reduce material dependency while maintaining performance standards, balancing cost pressures with regulatory compliance.

The most significant opportunities lie in the integration of smart technologies, emerging healthcare markets, and new service-based business models. AI-enabled fluid monitoring systems are improving efficiency by over 19%, while reducing fluid waste by nearly 16%, creating strong economic and operational incentives for adoption. Emerging markets in Asia-Pacific and Latin America are expanding healthcare infrastructure at rates exceeding 10%, unlocking new demand pockets for advanced fluid systems. A notable future signal is the shift toward predictive fluid management using IoT-enabled devices, enabling real-time analytics and proactive system adjustments. This creates a non-obvious upside in operational optimization, where hospitals can reduce downtime by up to 13% while improving resource utilization. Companies are positioning for dominance by increasing R&D spending, expanding into high-growth regions, and building integrated ecosystems combining hardware, software, and analytics. Strategic partnerships with healthcare providers and technology firms are further accelerating innovation and market penetration.

The market faces critical execution challenges related to infrastructure limitations, integration complexity, and cost barriers. Implementing advanced fluid management systems requires significant infrastructure upgrades, increasing capital expenditure by approximately 18%, which limits adoption in cost-sensitive regions. Integration with existing hospital systems remains complex, with compatibility issues affecting nearly 15% of deployments, leading to delays and performance inefficiencies. A key real-world pressure is the growing cost constraint across public healthcare systems, restricting large-scale modernization initiatives. These challenges directly impact long-term scalability and consistent performance, creating a gap between technological capability and real-world deployment. To remain competitive, companies must solve integration bottlenecks through standardized platforms, invest in cost-efficient system designs, and build strong service support networks. Strategic partnerships and modular system development are becoming essential to overcome these barriers, ensuring sustained growth and market relevance in an increasingly competitive landscape.

Over 62% shift toward automated fluid systems is redefining clinical workflows. Hospitals are rapidly replacing manual systems, with automated deployments increasing by 19% in the last 18 months. This shift is improving procedural accuracy by 16% while reducing human intervention by 21%. Companies are scaling production of smart systems and forming integration partnerships with hospital IT providers to accelerate deployment and standardization.

Nearly 58% of facilities adopting disposable systems is reshaping cost and infection control models. Single-use fluid management components have reduced cross-contamination risks by 17% and lowered sterilization costs by 13%. This shift is being accelerated by stricter infection control regulations introduced post-2024. Manufacturers are restructuring supply chains and increasing localized production to meet rising demand while optimizing margins through volume-based manufacturing.

Asia-Pacific witnessing over 11% surge in installations is shifting regional demand dynamics. Healthcare infrastructure expansion and localized manufacturing have driven system installations significantly higher than mature markets. In contrast, North America focuses on upgrading existing systems, with over 14% facilities transitioning to advanced monitoring. Companies are responding by expanding regional assembly hubs and aligning pricing strategies to capture high-growth markets.

More than 46% integration of digital monitoring is transforming real-time decision-making. Sensor-based systems are improving fluid tracking accuracy by 18% and reducing wastage by 15%. A non-obvious shift is the integration of fluid data into broader hospital analytics platforms, enhancing predictive maintenance and operational planning. Firms are investing in software ecosystems and forming cross-industry collaborations to strengthen data-driven capabilities.

The fluid management market is segmented across types, applications, and end-users, with demand concentrated in high-precision medical environments where accuracy and efficiency are critical. Fluid management systems and disposables dominate product demand due to their direct role in surgical and diagnostic procedures, accounting for over 60% of usage. Application-wise, surgical procedures and urology lead due to high procedural volumes, while emerging areas like dialysis are gaining traction. End-user demand is heavily concentrated in hospitals, contributing over 45%, driven by infrastructure scale and procedure intensity. However, demand is gradually shifting toward ambulatory and home-based care settings, reflecting a broader transition toward decentralized healthcare delivery. This segmentation highlights a clear movement from centralized, high-volume usage toward more distributed and efficiency-driven deployment models, shaping future investment priorities.

Fluid Management Systems dominate the market with approximately 34% share, driven by their central role in surgical precision, integrated control, and scalability across healthcare settings. Their ability to improve operational efficiency by over 18% makes them structurally indispensable. Disposables & Accessories represent the fastest-growing segment, expanding at over 12% annually due to increasing infection control mandates and cost-effective single-use adoption. Compared to traditional reusable systems, disposables reduce contamination risk by 17%, creating a clear shift in procurement strategies. Fluid Transfer Devices and Monitoring Systems together account for nearly 38% of the market, playing a critical role in ensuring fluid accuracy and real-time tracking. Monitoring systems, in particular, are gaining traction with over 15% adoption growth as hospitals prioritize data-driven decision-making. Waste Management Systems, while holding a smaller share, remain strategically important due to regulatory compliance and sustainability requirements. Demand is clearly shifting toward integrated and disposable-focused solutions, forcing companies to prioritize innovation in smart systems and expand production capacity for single-use components. Investment is increasingly directed toward technologies that combine efficiency, safety, and compliance, while legacy standalone devices are gradually losing relevance.

Surgical Procedures lead the market with approximately 36% share, driven by high procedural volumes and the need for precise fluid control during operations. The concentration of demand in this segment is supported by increasing surgical complexity and a 14% rise in global procedure volumes. Dialysis is the fastest-growing application, expanding by over 11%, fueled by the rising prevalence of chronic kidney conditions and the need for continuous fluid regulation systems. Urology and Gastroenterology together contribute nearly 34% of demand, with stable usage patterns supported by diagnostic and therapeutic procedures. Cardiology, while relatively smaller, is experiencing gradual adoption growth due to increasing integration of fluid monitoring in interventional procedures. Compared to surgical applications, dialysis demonstrates a more continuous usage model, creating recurring demand for fluid systems and consumables. Companies are adapting by tailoring solutions for high-volume surgical environments while also expanding product lines for chronic care applications like dialysis. This shift reflects a broader transition from episodic to continuous usage models, influencing both product design and service strategies.

Hospitals dominate the market with over 47% share, driven by high patient volumes, complex procedures, and extensive infrastructure supporting fluid-intensive operations. Their centralized procurement and reliance on advanced systems make them the primary demand hub. Ambulatory Surgical Centers are the fastest-growing segment, expanding at over 13%, as outpatient procedures increase and cost-efficient care delivery models gain traction. Clinics and Dialysis Centers together account for approximately 33% of demand, with steady growth supported by specialized treatments and recurring patient visits. Home Healthcare, while smaller, is gaining momentum with over 10% growth, driven by the shift toward decentralized care and remote patient management. Compared to hospitals, these emerging settings prioritize compact, cost-effective, and easy-to-use systems. Companies are targeting these segments through differentiated pricing strategies, portable system designs, and partnerships with outpatient care providers. This shift in buying behavior is redefining product development and distribution strategies, as demand moves toward flexible and patient-centric solutions.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America leads in demand concentration with over 65% adoption of advanced fluid systems, while Europe holds approximately 27% share driven by regulatory-led upgrades and sustainability compliance. Asia-Pacific, contributing nearly 24%, is accelerating in both production and installation, with over 11% growth in system deployment supported by expanding healthcare infrastructure. A key structural shift is the global move toward localized manufacturing and supply chain resilience post-2024, reducing dependency on imports. While North America dominates in scale, Europe leads in compliance-driven innovation, and Asia-Pacific in expansion speed. Companies are prioritizing Asia-Pacific for capacity expansion while maintaining innovation hubs in developed markets.

What is driving high-value system adoption and operational upgrades in advanced healthcare environments?

North America holds approximately 38% market share, driven by high procedural volumes and advanced healthcare infrastructure. Demand is concentrated in surgical and critical care applications, where over 65% of hospitals have adopted automated fluid systems. A key structural force is regulatory tightening around patient safety and device accuracy, accelerating system upgrades. Execution-level shifts include over 14% increase in smart monitoring integration across hospitals. A notable strategic move includes large-scale hospital network upgrades improving efficiency by 16%. Buyers prioritize precision, compliance, and integration capabilities over cost. Companies are investing heavily in automation and digital ecosystems, making this region a priority for high-margin, technology-driven expansion.

How are compliance and sustainability mandates reshaping system design and procurement priorities?

Europe accounts for nearly 27% of the market, with strong demand across Germany, France, and the UK. Strict regulatory frameworks and ESG mandates are driving adoption of low-waste and compliant fluid systems, reducing medical waste by over 12%. Operational shifts include a 15% increase in adoption of disposable systems aligned with infection control standards. Companies are investing in eco-efficient product design and compliance-focused innovation. Buyers demonstrate a quality-first and compliance-driven purchasing behavior, prioritizing certified and sustainable solutions. This region forces continuous innovation and product adaptation, making it a benchmark for regulatory-led transformation.

What is accelerating large-scale deployment and manufacturing expansion across high-growth healthcare systems?

Asia-Pacific contributes around 24% of global demand, with China, India, and Japan leading adoption. The region benefits from strong manufacturing capabilities and infrastructure expansion, supporting over 11% annual growth in installations. A key execution shift is the rapid localization of production, reducing costs by approximately 14% and improving supply reliability. Strategic investments in hospital infrastructure are driving deployment at scale, with system adoption increasing by 13% in emerging economies. Buyers prioritize cost-efficiency and scalability, pushing companies to offer modular and competitively priced solutions. This region is critical for volume-driven growth and long-term expansion strategies.

What factors are shaping demand growth amid infrastructure and cost constraints?

South America holds approximately 6% market share, with Brazil and Argentina leading regional demand. Growth is driven by expanding healthcare access and rising procedural volumes, increasing system adoption by over 9%. However, infrastructure limitations and cost sensitivity remain key constraints, impacting large-scale deployment. A structural challenge is uneven healthcare funding, slowing modernization efforts. Companies are responding by offering cost-effective and simplified systems tailored to local needs. Buyers prioritize affordability and durability, influencing product design. This region presents a balanced mix of opportunity and risk, requiring targeted strategies for sustainable market entry.

How is infrastructure investment transforming demand patterns across developing healthcare ecosystems?

The Middle East & Africa region accounts for approximately 5% of global demand, with key contributions from the UAE, Saudi Arabia, and South Africa. Demand is driven by healthcare infrastructure expansion and government-backed modernization programs. A transformation driver is increasing investment in hospital capacity, boosting system adoption by over 10%. Execution-level shifts include rising deployment of advanced systems in urban healthcare centers. Strategic partnerships and public-private collaborations are improving access to modern technologies. Buyers focus on reliability and long-term value, balancing cost and performance. This region is emerging as a strategic growth frontier driven by infrastructure and investment momentum.

United States – 38% share in the Fluid Management Market, driven by advanced healthcare infrastructure and high adoption of automated systems

China – 16% share in the Fluid Management Market, supported by large-scale manufacturing capacity and rapidly expanding healthcare demand

The fluid management market is defined by competition between global medical technology leaders, regional manufacturers, and specialized device innovators. Major players such as Baxter International, B. Braun Melsungen, Fresenius Medical Care, Stryker Corporation, and Cardinal Health collectively hold approximately 52% market share, competing directly on technology integration and product reliability. Global leaders focus on advanced systems and integrated solutions, while regional players compete aggressively on cost, often offering 12–15% lower pricing.

Competition is primarily driven by technological differentiation, supply chain control, and speed of deployment, with automation-enabled systems improving efficiency by over 18% becoming a key battleground. Companies are actively expanding manufacturing footprints, forming strategic hospital partnerships, and investing in digital integration capabilities. A notable competitive shift is the increasing focus on vertical integration to secure component supply and reduce dependency risks. High entry barriers exist due to regulatory compliance requirements and capital-intensive R&D, creating pressure for new entrants. To win, companies must combine innovation, cost efficiency, and supply resilience while delivering integrated, high-performance solutions that align with evolving healthcare demands.

Baxter International Inc.

B. Braun Melsungen AG

Fresenius Medical Care AG & Co. KGaA

Stryker Corporation

Cardinal Health Inc.

Medtronic plc

Smiths Medical

Olympus Corporation

Zimmer Biomet Holdings Inc.

Boston Scientific Corporation

ICU Medical Inc.

Nipro Corporation

Cook Medical Inc.

Advanced automation and closed-loop fluid management systems are redefining operational precision in healthcare settings. These systems improve procedural accuracy by over 18% while reducing manual intervention by nearly 22%, with adoption exceeding 60% in large hospitals. Integration with surgical platforms is streamlining workflows, enabling real-time adjustments and reducing complication risks. This shift delivers measurable efficiency gains and strengthens competitive positioning for providers investing in high-performance systems.

Emerging technologies such as sensor-based monitoring and IoT-enabled fluid tracking are gaining rapid traction, with deployment levels rising above 48% across digitally enabled facilities. These solutions enhance fluid measurement accuracy by 17% and reduce wastage by 15%, directly impacting cost control and resource optimization. Companies are integrating these technologies into broader hospital data ecosystems, enabling predictive analytics and improving operational decision-making, creating a clear advantage for early adopters.

Disruptive innovation is being driven by AI-enabled fluid control systems and smart disposables. AI-integrated platforms improve system responsiveness by 16% while reducing operational costs by 12% compared to conventional programmable systems. In comparison, legacy gravity-based systems lag significantly in both accuracy and efficiency. Firms investing in AI-driven solutions are capturing higher-value contracts, particularly in advanced healthcare markets.

Between 2026 and 2028, technology convergence will accelerate, with over 20% of facilities expected to transition toward fully integrated fluid ecosystems. This transformation is optimizing clinical outcomes, reducing waste, and reshaping competitive dynamics. Companies that act now by scaling digital integration and automation capabilities are positioning themselves to lead in a precision-driven, performance-focused market.

March 2026, Baxter International announced expansion of its smart infusion manufacturing line, increasing production capacity by 18% to meet rising global demand. This move strengthens supply resilience and accelerates delivery timelines for automated systems. [Capacity Expansion]

Source: https://www.baxter.com

November 2025, B. Braun Melsungen launched an advanced fluid monitoring system with integrated sensors, improving accuracy by 16% and reducing fluid waste. The innovation enhances clinical efficiency and reinforces the company’s position in smart healthcare solutions. [Product Innovation]

Source: https://www.bbraun.com

July 2025, Fresenius Medical Care partnered with regional healthcare providers to deploy dialysis fluid systems across 120+ centers, improving treatment efficiency by 13%. This strategic collaboration expands market reach and strengthens service integration capabilities. [Strategic Partnership]

Source: https://www.freseniusmedicalcare.com

January 2024, Stryker Corporation introduced a next-generation surgical fluid management platform, reducing setup time by 14% and improving workflow efficiency. The launch supports faster surgical turnover and enhances competitive positioning in operating room technologies. [Technology Upgrade]

Source: https://www.stryker.com

The fluid management market report delivers comprehensive coverage across key segments including types such as fluid management systems, disposables and accessories, monitoring systems, and waste management solutions, alongside applications spanning surgical procedures, urology, cardiology, dialysis, and gastroenterology. The analysis extends across major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, while also evaluating critical technologies such as automation, AI-enabled monitoring, and IoT-integrated systems. Over 65% of the analysis focuses on high-impact segments with strong adoption patterns, ensuring relevance for decision-makers.

From an analytical standpoint, the report evaluates more than 20 distinct segment intersections, supported by measurable insights such as adoption rates exceeding 60% in advanced systems and efficiency improvements of up to 18% across automated technologies. It profiles over 12 key companies and assesses competitive positioning based on innovation, supply chain strategy, and deployment capabilities. Emerging areas such as smart disposables and predictive fluid management are also examined, reflecting shifting industry priorities.

Strategically, the report provides actionable intelligence for investment planning, regional expansion, and competitive benchmarking. With forward-looking coverage through 2033, it highlights evolving demand patterns, including a projected 20% increase in digital system integration and over 15% shift toward decentralized healthcare settings, enabling stakeholders to align strategies with future market dynamics.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 9469.2 Million |

|

Market Revenue in 2033 |

USD 13059.28 Million |

|

CAGR (2026 - 2033) |

4.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Baxter International Inc., B. Braun Melsungen AG, Fresenius Medical Care AG & Co. KGaA, Stryker Corporation, Cardinal Health Inc., Medtronic plc, Smiths Medical, Olympus Corporation, Zimmer Biomet Holdings Inc., Boston Scientific Corporation, ICU Medical Inc., Nipro Corporation, Cook Medical Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |