Reports

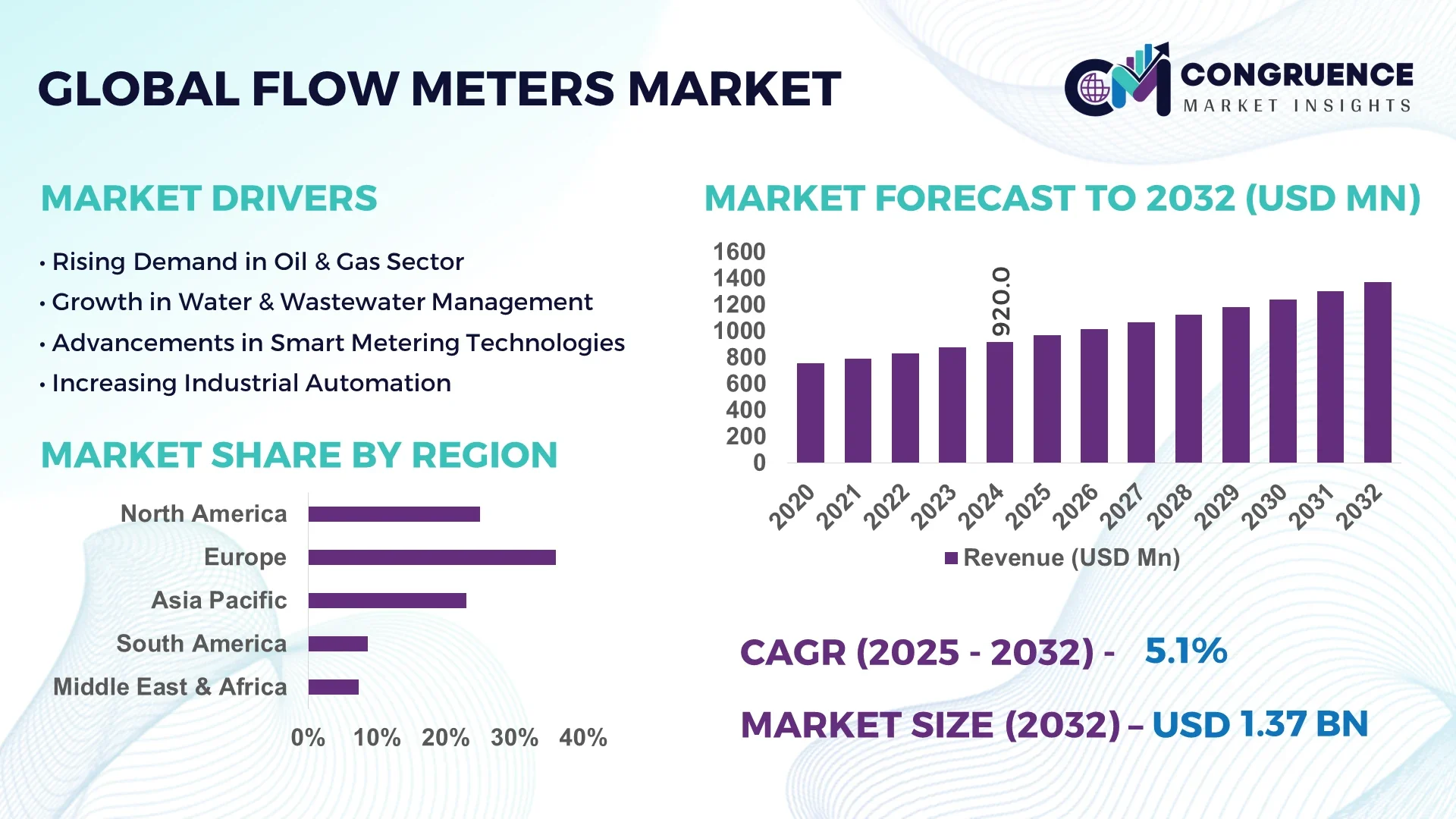

The Global Flow Meters Market was valued at USD 920.0 Million in 2024 and is anticipated to reach a value of USD 1,373.8 Million by 2032 expanding at a CAGR of 5.14% between 2025 and 2032.

Asia-Pacific dominates the global flow meters market, driven by robust industrial development, water infrastructure upgrades, and stringent environmental monitoring regulations. Countries like China, Japan, and India have significantly increased investments in industrial automation and smart water management systems, which has led to rising installations of advanced flow meters across sectors like manufacturing, chemical processing, and utilities.

Flow meters are critical for monitoring and controlling liquid and gas flows in diverse applications such as oil and gas exploration, water treatment, and power generation. As demand for high precision and operational efficiency rises, flow meters are being increasingly integrated with digital technologies such as IoT and AI. The adoption of smart flow meters has grown due to their capability to transmit real-time data, minimize system downtimes, and facilitate predictive maintenance strategies, especially in large-scale industrial environments.

Artificial Intelligence (AI) is playing a pivotal role in modernizing the flow meters market by enabling smarter and more responsive flow measurement solutions. With AI integration, flow meters can now interpret real-time data, learn from usage patterns, and trigger intelligent alerts for maintenance or abnormalities, reducing downtime and operational inefficiencies.

AI-driven flow meters are contributing to improved operational visibility across industries like utilities, oil & gas, and chemicals. These smart devices leverage machine learning algorithms to continuously analyze flow dynamics, detect leaks, or unusual flow behaviors, and optimize operational parameters without manual intervention. AI applications are also enhancing diagnostic capabilities, enabling operators to identify and resolve issues before they escalate into costly failures.

Moreover, cloud connectivity supported by AI allows for centralized monitoring of flow meter networks across multiple facilities. This has proven highly beneficial in distributed systems such as municipal water networks or offshore oil platforms, where real-time insights improve decision-making and ensure compliance with safety and environmental regulations.

"In January 2024, the Aljezur Municipal Council in Portugal installed 1,500 AI-powered smart water meters in Vale da Telha to reduce water loss. These meters provide real-time data and automatically detect anomalies, enabling faster response to leaks and inefficient usage patterns."

The rising need for precise flow monitoring across industries such as oil & gas, water treatment, and chemical processing is a major growth driver. Industrial players are increasingly deploying advanced flow meters to improve process efficiency, meet quality standards, and reduce operational risks. Technologies such as ultrasonic and Coriolis meters are being adopted for their high accuracy in harsh environments. Additionally, automation trends and regulatory compliance are pushing companies to invest in sophisticated flow monitoring solutions that offer minimal error margins.

Despite their technological advancements, modern flow meters often come with high acquisition and setup costs, especially those embedded with smart features or used in hazardous environments. Furthermore, periodic calibration, specialized maintenance, and the need for skilled personnel to operate and interpret flow data can impose additional burdens, particularly on small and mid-sized enterprises. This financial barrier limits market penetration, especially in emerging economies where budget constraints are prominent.

The proliferation of IoT across industrial landscapes presents lucrative opportunities for the flow meters market. Smart flow meters with built-in connectivity allow for real-time diagnostics, automated reporting, and remote management—enhancing reliability and performance. Industries are increasingly investing in digital infrastructure, and flow meters are at the forefront of this transition. As predictive maintenance and data-driven decision-making gain traction, smart flow meters are expected to witness strong demand across utility management, oil pipelines, and large-scale industrial processes.

Flow meters used in extreme temperatures, corrosive chemical exposure, or high-pressure conditions often face degradation or loss of accuracy. Designing meters that maintain precision and durability under such extremes remains a major engineering challenge. Additionally, integrating smart technologies in these environments without compromising the meter’s integrity or safety compliance poses significant hurdles. These technical constraints limit the applicability of smart flow meters in critical sectors like mining, deep-sea drilling, and nuclear energy.

Rise in Modular and Prefabricated Construction: The rise of modular building methods in construction has significantly increased the demand for accurate, space-efficient flow meters. These pre-engineered units demand reliable plumbing and fluid management systems that can be installed with minimal adjustments. Flow meters that offer easy installation, compact size, and high measurement accuracy are gaining popularity, particularly in North America and Europe.

Growing Emphasis on Renewable Energy: With growing global emphasis on renewable energy, industries are seeking flow measurement solutions that align with green technologies. For instance, in biogas and hydrogen production plants, specialized flow meters are used to monitor gas generation, conversion rates, and pipeline distribution. Their application ensures safety, operational control, and compliance with emerging environmental regulations.

Advancements in Non-Invasive Flow Measurement Technologies: Ultrasonic and electromagnetic flow meters, which do not require direct contact with the fluid, are gaining traction due to their durability and lower maintenance requirements. These meters are ideal for sterile environments such as pharmaceutical production or food processing facilities, where contamination risks must be minimized. Their adoption is steadily replacing conventional mechanical flow meters in precision-driven sectors.

Widespread Adoption of Wireless Monitoring and Connectivity: The demand for wireless-enabled flow meters is rising across industries that manage vast and distributed assets. These devices simplify installation, reduce cabling costs, and offer real-time monitoring through centralized platforms. Their utility in remote or hazardous environments—like offshore rigs or chemical plants—makes them essential tools for enhancing operational safety and efficiency.

The global flow meters market is segmented by type, application, and end-user, each contributing uniquely to the market's dynamics. Understanding these segments provides insights into the market's current state and future prospects.

Flow meters are categorized into various types, including magnetic, ultrasonic, Coriolis, differential pressure, vortex, thermal, and positive displacement meters. Among these, magnetic flow meters held the largest market share in 2024, accounting for over one-fourth of the market. Their dominance is attributed to high accuracy, non-invasive measurement, and compatibility with various corrosive liquids, making them ideal for water and wastewater applications.

Vortex flow meters are anticipated to grow at the fastest rate due to their versatility in measuring liquids, gases, and steam. Their reliability, lower maintenance requirements, and cost-effectiveness make them a preferred choice in industries seeking flexible flow measurement solutions.

Flow meters are widely used in oil & gas, water and wastewater management, chemical processing, power generation, food and beverages, and pharmaceuticals. The oil & gas industry currently leads the application segment, driven by the critical need for precision and reliability in exploration, refining, and distribution.

However, water and wastewater management is expected to be the fastest-growing segment, supported by global water conservation initiatives, infrastructure upgrades, and rising regulatory standards. The increasing adoption of non-invasive flow meters, particularly ultrasonic and magnetic types, is transforming utility operations and public water systems.

The end-user market for flow meters includes industrial, commercial, and residential sectors. The industrial sector dominates due to high-volume applications in process control, utilities, and manufacturing. Flow meters play a vital role in ensuring efficient production, safety compliance, and process automation.

The commercial sector is experiencing notable growth, with widespread use in HVAC systems, commercial water supply networks, and facility management. Flow meters help reduce energy consumption and improve water use efficiency in office buildings, malls, and educational institutions.

The residential sector, while still emerging, is gaining importance due to the adoption of smart meters in homes. These devices allow consumers to monitor real-time water usage, detect leaks, and contribute to water conservation efforts. The growth of smart home technologies is expected to fuel demand in this segment.

Europe accounted for the largest market share at 36% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.3% between 2025 and 2032.

Europe’s dominance is driven by advanced industrial infrastructure and stringent regulatory frameworks. In contrast, Asia-Pacific benefits from rapid urbanization, expanding industrial base, and government-backed infrastructure initiatives that are boosting flow meter adoption across various sectors.

Technological Integration and Industrial Automation Drive Growth

North America captured approximately 25% of the global flow meters market in 2024. The U.S. continues to dominate due to its strong presence in oil & gas, water treatment, and chemical processing sectors. Technological advancements, including the adoption of smart and digital flow meters, are enhancing accuracy and real-time data tracking. Canada is emerging as a growth driver, supported by investments in sustainable water management and energy efficiency.

Sustainability Goals Fuel Market Expansion

Europe holds a 36% share of the global market, making it the leading region in 2024. This is largely due to stringent EU regulations on emissions, water usage, and energy efficiency. Germany, the UK, and France lead in flow meter adoption for industrial and municipal applications. The emphasis on sustainable practices and adoption of Industry 4.0 technologies has accelerated demand for intelligent flow measurement solutions.

Infrastructure Growth and Industrialization Boost Demand

Asia-Pacific represents 35% of the global market share and is poised to grow at the fastest rate through 2032. China, India, and Japan are major contributors. Urban development, rapid industrialization, and smart city projects are key growth catalysts. Demand for water management systems and oil & gas exploration in the region is boosting the uptake of flow meters, particularly non-invasive and digital variants.

Energy Projects and Water Infrastructure Drive Usage

South America accounts for around 10% of the market, with Brazil and Mexico as key contributors. Brazil’s push to modernize its oil and gas infrastructure and enhance water distribution networks is driving the demand for precision flow meters. Mexico is witnessing steady growth, driven by its expanding manufacturing and energy sectors.

Oil Dominance and Water Scarcity Fuel Demand

Middle East & Africa hold roughly 10% market share, with Saudi Arabia and UAE being the primary markets. The demand is concentrated in the oil & gas industry, where flow meters are critical for operations. The increasing need for water conservation in arid regions is also supporting the adoption of advanced flow monitoring systems in municipal and industrial applications.

China: The largest contributor globally with an estimated market value of USD 207.0 million in 2024. Growth is driven by massive investments in water infrastructure and widespread industrial automation.

United States: Holding a market value of approximately USD 184.0 million in 2024, supported by high demand for accurate flow measurement in oil & gas, chemical processing, and smart water systems.

The global flow meters market is witnessing intense competition among leading manufacturers and new entrants. Companies are focused on product innovations, smart technologies, and expanding their geographic footprint. Increasing demand from oil & gas, water treatment, pharmaceuticals, and food & beverage sectors has led to the development of highly accurate, energy-efficient, and digital flow measurement solutions. Strategic mergers and acquisitions, along with collaborative R&D initiatives, are playing a pivotal role in market consolidation. Additionally, market players are heavily investing in enhancing product capabilities such as remote monitoring, diagnostics, and wireless communication to meet evolving customer demands. Technological upgrades in non-invasive and portable flow meters are creating new avenues for competition. As industries transition toward smart manufacturing, the integration of AI, IoT, and edge computing into flow meters is becoming a key competitive differentiator.

Siemens AG

Emerson Electric Co.

ABB Ltd.

Endress+Hauser Group

Yokogawa Electric Corporation

Honeywell International Inc.

KROHNE Group

Badger Meter, Inc.

Azbil Corporation

Bronkhorst High-Tech B.V.

Schneider Electric SE

Fuji Electric Co., Ltd.

Hitachi Ltd.

Flow Meter Group

McCrometer, Inc.

Brooks Instrument

TSI Incorporated

GPI (Great Plains Industries)

SmartMeasurement Inc.

OMEGA Engineering

Technological advancement is a cornerstone of growth in the flow meters market. Digital transformation has enabled the development of intelligent flow meters that offer real-time data capture, self-diagnostics, and seamless integration with industrial control systems. Coriolis and ultrasonic flow meters are gaining traction for their high accuracy and suitability in a wide range of applications, including hazardous and high-pressure environments.

Electromagnetic flow meters are favored in water and wastewater treatment due to their reliability and minimal maintenance. Additionally, the rise in demand for non-intrusive technologies has led to the popularity of clamp-on ultrasonic meters, which reduce downtime and installation costs. The integration of wireless technology has further enabled remote operation and reduced the need for wired infrastructure in hard-to-reach or hazardous areas.

Advancements in miniaturization and sensor technology are enabling compact flow meters suited for biomedical and laboratory applications. Furthermore, the convergence of AI and machine learning with flow measurement systems is paving the way for predictive maintenance, energy optimization, and operational efficiency across sectors.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In April 2024, ABB announced that its VortexMaster FSV400 and SwirlMaster FSS400 flowmeters achieved Ethernet-APL certification. This certification supports high-speed communication and power delivery over a two-wire system, enhancing process automation systems.

In March 2024, Yokogawa Electric Corporation finalized its acquisition of Adept Fluidyne Pvt. Ltd., a prominent Indian manufacturer of magnetic flow meters. This move enhances Yokogawa’s position in South Asia’s growing industrial flow measurement sector.

In January 2024, Siemens unveiled the SITRANS FST020 clamp-on ultrasonic flow meter. Designed for water and wastewater applications, it offers easy, non-intrusive installation and delivers accurate measurements across a wide range of pipe sizes and materials.

This Flow Meters Market Report covers comprehensive insights into the global flow meters industry. It includes detailed segmentation by type, application, and end-user, highlighting key trends shaping each category. The report provides regional market assessments across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, focusing on market dynamics, industrial policies, and investment opportunities.

The report evaluates how technological innovations, particularly AI, IoT, and wireless communication, are revolutionizing the flow measurement landscape. These insights support businesses in adapting to smart industry demands and capitalizing on emerging sectors like environmental monitoring, renewable energy, and digital infrastructure.

Furthermore, the report profiles major market players and analyzes their strategies in terms of product innovation, partnerships, and geographical expansion. The findings in this report aim to guide stakeholders, from manufacturers and suppliers to investors and policymakers, in identifying growth areas, anticipating challenges, and formulating data-driven strategies for future success in the flow meters market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Flow Meters Market |

| Market Revenue (2024) | USD 920.0 Million |

| Market Revenue (2032) | USD 1,373.8 Million |

| CAGR (2025–2032) | 5.14% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Siemens AG, Emerson Electric Co., ABB Ltd., Endress+Hauser Group, Yokogawa Electric Corporation, Honeywell International Inc., KROHNE Group, Badger Meter, Inc., Azbil Corporation, Bronkhorst High-Tech B.V., Schneider Electric SE, Fuji Electric Co., Ltd., Hitachi Ltd., Flow Meter Group, McCrometer, Inc., Brooks Instrument, TSI Incorporated, GPI (Great Plains Industries), SmartMeasurement Inc., OMEGA Engineering |

| Customization & Pricing | Available on Request (10% Customization is Free) |