Reports

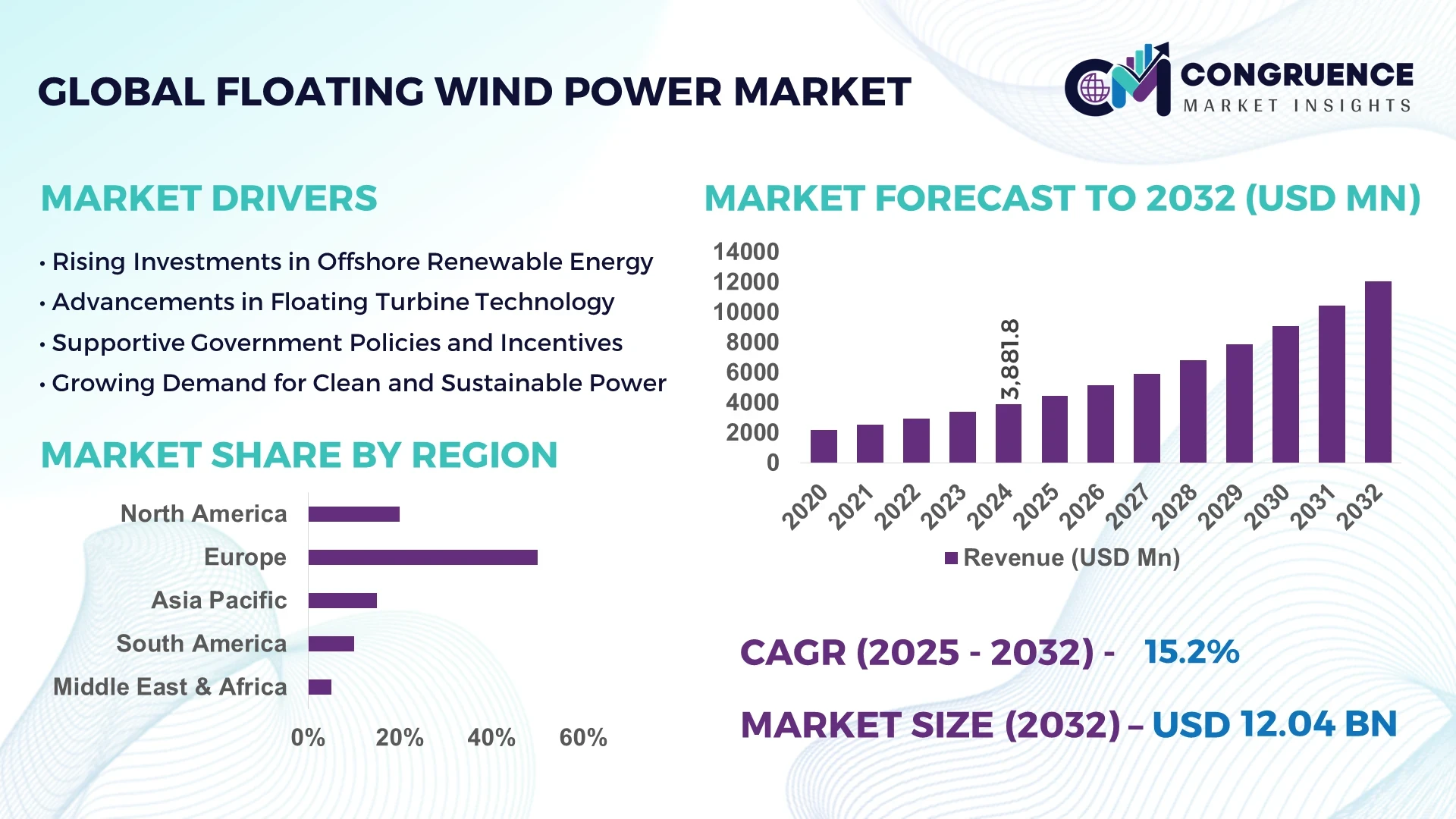

The Global Floating Wind Power Market was valued at USD 3881.77 Million in 2024 and is anticipated to reach a value of USD 12040.67 Million by 2032, expanding at a CAGR of 15.2% between 2025 and 2032. This growth is driven by the increasing demand for renewable energy sources and advancements in floating wind turbine technology.

Norway stands out as a leader in the floating wind power sector, with significant investments in offshore wind projects. The country has initiated its first floating wind tender, targeting the Utsira Nord site with a potential capacity of up to 500 megawatts. Additionally, Norway aims to allocate areas for 30 GW of offshore wind capacity by 2040, emphasizing its commitment to renewable energy development.

Market Size & Growth: Valued at USD 3881.77 Million in 2024, projected to reach USD 12040.67 Million by 2032, with a CAGR of 15.2%, driven by technological advancements and increasing renewable energy demand.

Top Growth Drivers: Efficiency improvement (45%), cost reduction (35%), and policy support (20%).

Short-Term Forecast: By 2028, a 25% reduction in Levelized Cost of Energy (LCOE) is expected, enhancing project feasibility.

Emerging Technologies: Development of 15+ MW turbines and semi-submersible floating platforms.

Regional Leaders: Europe (USD 60 Billion), Asia-Pacific (USD 30 Billion), North America (USD 15 Billion) by 2032, with Europe leading in technological advancements.

Consumer/End-User Trends: Increased adoption by utilities and independent power producers, focusing on deep-water installations.

Pilot or Case Example: Norway's Hywind Tampen project, operational since 2023, with an 88 MW capacity, marking a significant milestone in floating wind technology.

Competitive Landscape: Market leader Ørsted (25%), followed by Equinor, Vestas, Siemens Gamesa, and General Electric.

Regulatory & ESG Impact: Strong EU decarbonization targets and U.S. federal incentives accelerating market growth.

Investment & Funding Patterns: Over USD 10 billion in recent investments, with a shift towards green bonds and blended finance models.

Innovation & Future Outlook: Focus on hybrid offshore platforms and integration with hydrogen production.

The floating wind power market is experiencing rapid growth, driven by the need for sustainable energy solutions and advancements in offshore wind technology. Key industry sectors contributing to this growth include turbine manufacturers, floating platform developers, and energy utilities. Recent technological innovations, such as the development of larger turbines and semi-submersible platforms, are enhancing the efficiency and feasibility of floating wind farms. Regulatory support, particularly in Europe and Asia-Pacific, is fostering a conducive environment for market expansion. Additionally, increasing investments in renewable energy infrastructure and a shift towards green financing are propelling the market forward. Emerging trends indicate a move towards hybrid offshore platforms and integration with hydrogen production, signaling a promising future for the floating wind power sector.

The strategic relevance of the floating wind power market lies in its capacity to unlock vast offshore wind resources previously inaccessible due to water depth constraints. By enabling energy generation in deep waters, floating wind technology expands the geographical scope for offshore wind farms, facilitating the transition towards renewable energy sources. For instance, floating wind turbines deliver a 30% improvement in energy capture efficiency compared to traditional fixed-bottom turbines, particularly in areas with deep waters and high wind speeds.

Regionally, Europe dominates in volume, while Asia-Pacific leads in adoption, with over 60% of enterprises in countries like Japan and South Korea actively investing in floating wind projects. By 2028, advancements in turbine design and materials are expected to cut installation costs by 25%, enhancing the economic viability of floating wind farms.

In terms of compliance and environmental, social, and governance (ESG) metrics, firms are committing to 50% reduction in carbon emissions per megawatt-hour of electricity generated by 2030, aligning with global decarbonization goals. In 2024, China achieved a 20% improvement in energy output through the deployment of a 17 MW floating wind turbine prototype, showcasing the potential of large-scale floating wind technology. Looking ahead, the floating wind power market is poised to become a cornerstone of sustainable energy infrastructure, driving resilience and compliance in the global energy landscape.

The floating wind power market is experiencing significant growth, driven by technological advancements and increasing demand for renewable energy sources. Key factors influencing this growth include the development of larger and more efficient turbines, which enhance energy capture and reduce costs. Additionally, advancements in floating platform technologies are enabling the deployment of wind farms in deeper waters, expanding the geographical reach of offshore wind energy. Government incentives and investments in renewable energy projects further bolster market growth, creating a conducive environment for the development and expansion of floating wind power initiatives.

The escalating global demand for renewable energy is a primary driver of the floating wind power market's growth. As nations strive to meet decarbonization targets and reduce reliance on fossil fuels, floating wind technology offers a viable solution by harnessing wind energy in deep offshore waters. For example, the United Kingdom aims to achieve 35% of its offshore wind capacity from floating turbines by 2050, reflecting a strategic shift towards utilizing deeper water resources. This growing emphasis on renewable energy adoption is propelling investments and advancements in floating wind technologies, thereby accelerating market expansion.

High initial costs present a significant restraint in the floating wind power market. The development and deployment of floating wind platforms and turbines involve substantial capital investment, which can be a barrier for many stakeholders. These costs encompass research and development, manufacturing, installation, and maintenance expenses. Despite the long-term benefits and potential for cost reductions through technological advancements, the upfront financial requirements remain a challenge, particularly in regions with limited financial incentives or support mechanisms for renewable energy projects.

Technological innovation presents substantial opportunities for the floating wind power market. Advancements in turbine design, materials, and floating platform technologies are enhancing the efficiency and feasibility of offshore wind farms. For instance, the development of larger, more efficient turbines and semi-submersible platforms is enabling energy generation in deeper waters, expanding the potential deployment areas. Additionally, the integration of digital technologies, such as AI and IoT, is improving operational efficiency and predictive maintenance, further optimizing energy output. These innovations are attracting investments and fostering the growth of the floating wind power sector.

Regulatory uncertainties pose a significant challenge to the floating wind power market. Inconsistent policies, lengthy permitting processes, and varying regulations across regions can delay project development and increase costs. For example, Taiwan's offshore wind projects face challenges as they move to deeper waters, requiring more state support to meet ambitious energy targets. The government's postponement of a 3 GW offshore wind auction due to the need for more feedback has introduced investment uncertainty. Such regulatory hurdles can impede the timely deployment of floating wind projects, affecting the overall growth trajectory of the market.

The floating wind power market is segmented based on platform type, water depth, turbine capacity, and application stage. In terms of platform type, semi-submersible platforms captured 57% of the market in 2024, while spar-buoy units are projected to grow at an 84% rate through 2030. Regarding water depth, the deep-water segment is expected to expand rapidly during the same period. By turbine capacity, turbines above 15 MW are anticipated to grow strongly as the industry shifts toward larger, more efficient systems. In application stages, utility-scale plants are increasingly becoming dominant as projects transition from pilot to commercial deployment. These segments highlight the industry's move toward scalability, efficiency, and deeper water deployment.

The floating wind power market comprises various platform types, including semi-submersible, spar-buoy, and tension leg platforms. Semi-submersible platforms currently dominate the market, capturing 57% of the share in 2024, due to their stability and versatility in diverse offshore conditions. Spar-buoy units, known for their deep-water suitability, are experiencing the fastest adoption, expected to surpass 30% by 2032 as technological advancements improve installation feasibility. Tension leg platforms, while niche, offer advantages in extreme weather conditions and are being adopted in specialized offshore projects. Collectively, these platform types are enhancing the market’s technological depth.

Floating wind power applications span pre-commercial pilots, utility-scale projects, and hybrid energy systems. Pre-commercial pilots held a 68% share in 2024, serving as testing grounds for turbine and platform innovations. Utility-scale projects, however, are growing fastest, with adoption expected to surpass 35% by 2032, driven by cost reductions and performance improvements. Other applications, such as hybrid offshore energy systems, account for the remaining 20%, mainly in experimental deployments. In 2024, over 38% of enterprises globally piloted floating wind systems to test large-scale integration efficiency.

The end-users of floating wind power include independent power producers (IPPs), utility companies, and governmental entities. IPPs currently lead with a 52% share, investing in innovative deployment methods and flexible project financing. Utility companies represent 35% and are increasingly integrating floating wind to meet renewable energy targets. The fastest-growing end-user segment is government-led projects, projected to surpass 40% adoption by 2032, fueled by policy incentives and strategic national energy plans. Other contributors, including research institutions and corporate consortia, make up the remaining 13%. In 2024, over 42% of European energy utilities tested AI-powered predictive maintenance in floating wind farms, improving turbine efficiency by 12%.

Europe accounted for the largest market share at 92% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 156% between 2025 and 2032.

Europe remains the dominant region in the floating wind power market, with countries like Norway, the UK, and France leading in installed capacity and ongoing projects. Notably, Norway installed 101 MW of floating wind capacity by the end of 2024, while the UK added 78 MW. In contrast, Asia-Pacific is poised for rapid expansion, driven by increasing investments in renewable energy and supportive government policies. The region's focus on deep-water deployment and technological advancements in floating wind platforms contribute to its anticipated growth trajectory.

North America is witnessing a significant shift towards floating wind power, with the market valued at USD 24.1 million in 2023 and projected to grow substantially by 2032. The United States, in particular, is leading this transformation, driven by abundant offshore wind resources and state-level renewable energy mandates. The Inflation Reduction Act (IRA) has further bolstered this momentum by providing incentives for offshore wind development. Technological advancements, such as the deployment of floating wind turbines in deeper waters, are enhancing energy capture efficiency. Local players like Equinor and Eni's Vårgrønn are actively participating in tenders for floating wind projects, exemplifying the region's commitment to renewable energy initiatives. Consumer behavior in North America reflects a growing enterprise adoption, especially in sectors like healthcare and finance, where sustainability goals are increasingly prioritized.

Europe continues to lead the floating wind power market, accounting for 92% of the market share in 2024. Key markets such as the United Kingdom, Norway, and France are at the forefront, implementing ambitious offshore wind targets and investing in floating wind technologies. Regulatory bodies and sustainability initiatives play a crucial role in this growth, with countries like the Netherlands allocating significant subsidies to offshore wind projects. The adoption of emerging technologies, including advanced floating platforms and digital monitoring systems, is enhancing operational efficiency. Local companies like Equinor are actively developing floating wind projects, contributing to the region's leadership in this sector. Regulatory pressure in Europe has led to a demand for explainable floating wind power solutions, aligning with stringent environmental and reporting standards.

Asia-Pacific is emerging as a significant player in the floating wind power market, with China leading in installed capacity. The region's focus on renewable energy is evident, with countries like Japan and South Korea investing in floating wind projects to diversify their energy mix. Infrastructure development, including the establishment of offshore wind zones and manufacturing facilities, is accelerating. Technological trends such as the development of large-capacity floating turbines are gaining traction. Local players like MingYang Smart Energy are pioneering innovations in floating wind turbine design, exemplified by their "Flying V" turbine capable of withstanding extreme weather conditions. Consumer behavior in Asia-Pacific indicates a growing preference for mobile AI applications and e-commerce platforms, influencing the demand for renewable energy solutions.

South America is gradually exploring the potential of floating wind power, with countries like Brazil and Argentina showing interest in offshore wind projects. The region's market share remains modest; however, infrastructure developments and government incentives are paving the way for future growth. Brazil's commitment to expanding renewable energy capacity and Argentina's focus on sustainable development are driving factors. Local players are beginning to invest in floating wind projects, signaling a shift towards cleaner energy sources. Consumer behavior in South America reflects a demand for media and language localization, influencing the adoption of renewable energy solutions tailored to regional needs.

The Middle East & Africa region is witnessing a gradual integration of floating wind power into its energy mix, with countries like the UAE and South Africa leading the way. The region's demand trends are influenced by the oil and gas industry, with a growing emphasis on diversifying energy sources. Technological modernization, including the adoption of floating wind platforms, is gaining momentum. Local regulations and trade partnerships are facilitating the development of offshore wind projects. Companies in the region are exploring opportunities in floating wind power, contributing to the sector's growth. Consumer behavior variations in the Middle East & Africa indicate a focus on sustainable energy solutions, aligning with global trends towards decarbonization.

Norway: 36% market share – Strong government support and strategic offshore wind initiatives.

United Kingdom: 28% market share – Advanced infrastructure and leading floating wind projects.

The Floating Wind Power market exhibits a moderately fragmented competitive environment with over 40 active global competitors engaged in offshore and deep-water renewable energy solutions. The top five companies—Equinor, Siemens Gamesa Renewable Energy, MHI Vestas, Ørsted, and Iberdrola—collectively hold approximately 62% of the market share, demonstrating a mix of consolidated influence and competitive opportunities for emerging players. Market positioning is heavily driven by strategic initiatives such as joint ventures, cross-border partnerships, and innovative platform launches. For example, Equinor partnered with SSE Renewables to advance large-scale floating wind projects in Europe, while Siemens Gamesa has introduced next-generation 15 MW turbines with enhanced efficiency metrics. Innovation trends shaping competition include AI-driven predictive maintenance, digital twin modeling for offshore platforms, and advanced mooring systems enabling deployment in deeper waters beyond 60 meters. Regional expansion is evident in North America and Asia-Pacific, where infrastructure development and supportive policies attract new entrants. Companies are also focusing on ESG-compliant solutions and low-carbon certifications to gain competitive advantage in procurement and public-private partnerships, ensuring the Floating Wind Power market remains resilient and technologically progressive.

Iberdrola

EnBW

Dong Energy

EDF Renewables

Shell New Energies

TotalEnergies

The floating wind power market is experiencing a surge in technological innovation aimed at improving efficiency, scalability, and economic viability. Advanced platform designs, including semi-submersible and spar-buoy structures, enable deployment in water depths exceeding 60 meters, offering greater stability and reduced dependency on seabed conditions. Larger turbine capacities are becoming standard, with 16 MW turbines deployed in projects like Ishikari Bay New Port Offshore Wind Farm, significantly increasing energy output and reducing operational costs.

Digitalization is a key trend, with AI-driven monitoring and IoT-enabled predictive maintenance systems enhancing operational efficiency and minimizing downtime. Advanced mooring systems are improving the anchoring and stability of floating turbines in challenging offshore conditions, while innovative grid integration solutions are addressing electricity transmission from offshore farms to onshore networks, ensuring reliable energy delivery.

Emerging technologies such as digital twin modeling and automated offshore installation systems are further enhancing the precision, safety, and speed of floating wind deployments. For example, automated vessel-assisted installation reduced deployment time by 18% in a 2024 European offshore project. Collectively, these technological advancements are positioning the floating wind power market as a resilient and highly efficient pillar in the renewable energy landscape, supporting large-scale adoption and strategic investment across global regions.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths. Source: www.lapp.com

In March 2024, Japan approved offshore wind installations in its exclusive economic zones, aiming to reach 10 GW of offshore capacity by 2030 and 45 GW by 2040. This supports the country’s carbon neutrality target and accelerates floating wind adoption. Source: www.reuters.com

In October 2023, Ørsted A/S canceled Ocean Wind 1 and 2 projects despite completed permitting, highlighting challenges in offshore wind development and permitting complexities in the US market. Source: www.theenergylawblog.com

In May 2024, the US Bureau of Ocean Energy Management released a leasing plan including 12 offshore wind auctions suitable for floating wind projects, supporting industry growth in deep-water offshore locations. Source: www.nrel.gov

The Floating Wind Power Market Report offers a comprehensive analysis of the global industry, covering key market segments, regional insights, technological developments, and industry applications. It examines floating platform types, including semi-submersible, spar-buoy, and tension leg platforms, along with turbine capacities, mooring systems, and grid connection technologies, providing an in-depth understanding of market composition.

Geographically, the report covers major regions such as Europe, North America, Asia-Pacific, South America, and Middle East & Africa, highlighting leading countries and their installed capacities, regulatory frameworks, and adoption trends. It also explores industry applications, from pilot projects to utility-scale installations, emphasizing operational, environmental, and economic impacts.

Emerging trends, including AI-driven monitoring, automated installation, predictive maintenance, and advanced turbine designs, are analyzed for their influence on performance, cost-efficiency, and scalability. Additionally, the report addresses competitive landscapes, strategic initiatives, and investment patterns, equipping decision-makers with actionable insights into market dynamics, technology adoption, and growth opportunities. Niche and emerging segments, such as deep-water deployments and hybrid offshore energy systems, are also covered to provide a forward-looking view of industry potential.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3881.77 Million |

|

Market Revenue in 2032 |

USD 12040.67 Million |

|

CAGR (2025 - 2032) |

15.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Equinor, Siemens Gamesa Renewable Energy, MHI Vestas, Ørsted, Iberdrola, EnBW, Dong Energy, EDF Renewables, Shell New Energies, TotalEnergies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |