Reports

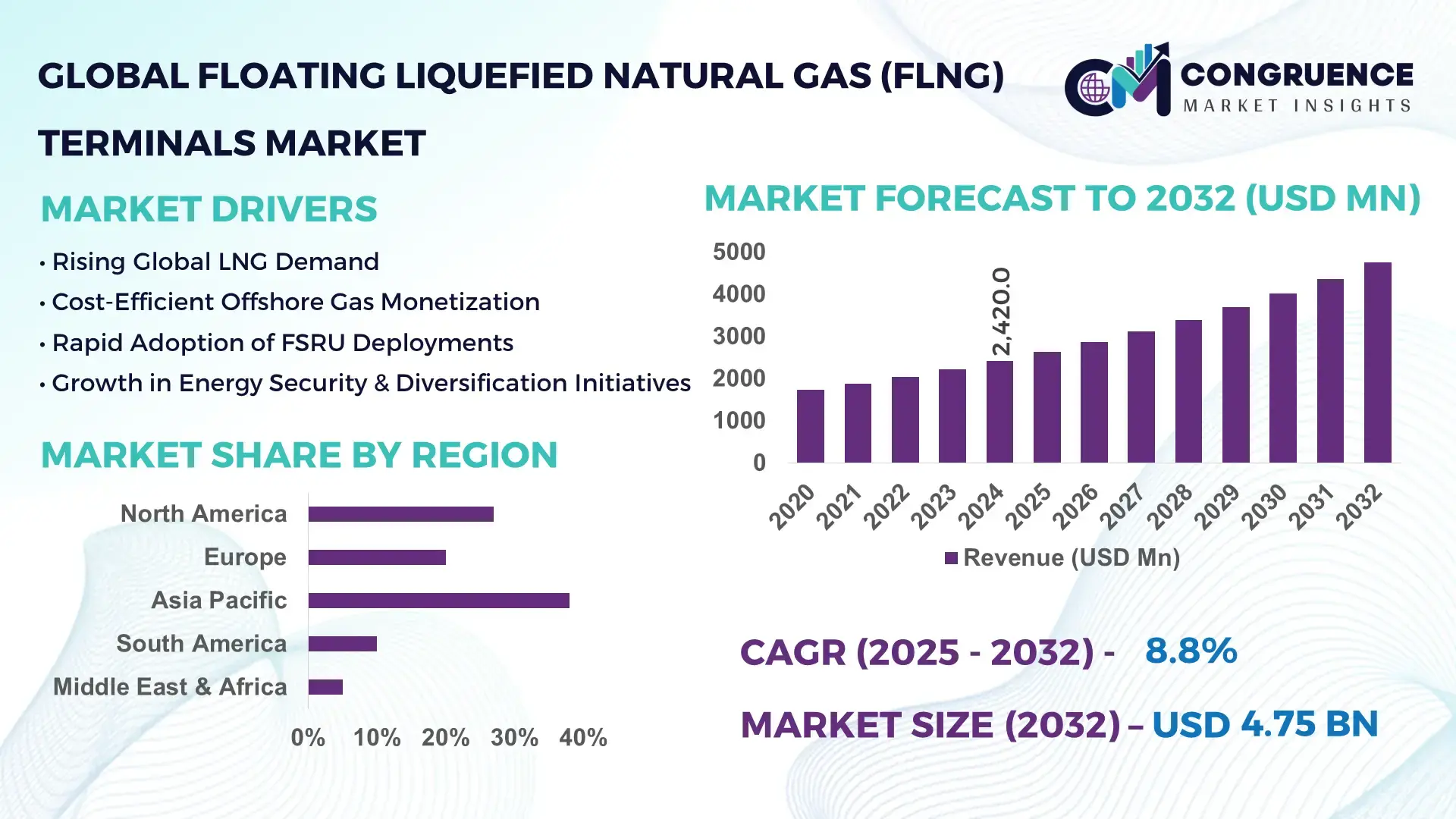

The Global Floating Liquefied Natural Gas (FLNG) Terminals Market was valued at USD 2,420.0 Million in 2024 and is anticipated to reach a value of USD 4,751.7 Million by 2032, expanding at a CAGR of 8.8% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily driven by the rising global demand for LNG and increased investments in offshore production infrastructure.

Australia dominates the global FLNG landscape, operating 12 active FLNG vessels and 18 FSRUs, with a total liquefaction capacity of 22 million tonnes per annum. Significant investments exceeding USD 1.5 billion have been made in digital monitoring and automation technologies, enhancing efficiency and reliability. Key industry applications include energy generation, petrochemicals, and industrial gas distribution, with 40% of LNG users in industrial sectors adopting floating solutions. Advanced modular designs are enabling faster project deployment, while regional shares indicate strong adoption across Asia-Pacific ports and coastal industrial hubs.

Market Size & Growth: USD 2,420.0 Million in 2024, projected USD 4,751.7 Million by 2032; growth driven by expanding offshore LNG projects.

Top Growth Drivers: LNG demand growth 55%, industrial adoption 48%, operational efficiency improvement 37%.

Short-Term Forecast: By 2028, automated monitoring systems expected to reduce downtime by 12%.

Emerging Technologies: AI-enabled predictive maintenance, modular vessel construction, cryogenic optimization.

Regional Leaders: Asia-Pacific USD 1,800.0 Million, North America USD 1,200.0 Million, Europe USD 950.0 Million; adoption trends vary with modular and AI-assisted solutions.

Consumer/End-User Trends: Industrial, utilities, and petrochemical sectors adopting flexible LNG import/export solutions; preference for energy-efficient and digitalized terminals.

Pilot or Case Example: In 2025, Woodside Energy reduced operational downtime by 10% using AI-assisted monitoring on FLNG vessels.

Competitive Landscape: Market leader Cheniere Energy (~18%), key competitors: Shell, Exmar NV, Petrobras, ENI UAE.

Regulatory & ESG Impact: Environmental standards and tax incentives promoting sustainable offshore LNG infrastructure.

Investment & Funding Patterns: Recent investments surpass USD 1.5 billion, with venture funding targeting automation and modular FLNG solutions.

Innovation & Future Outlook: Integration of AI, digital twins, and modular construction driving next-generation FLNG deployments.

The Floating Liquefied Natural Gas (FLNG) Terminals Market is seeing robust adoption across energy, industrial, and petrochemical sectors, with modular designs and digital technologies increasing efficiency. Regulatory support, economic incentives, and emerging regional LNG demand are shaping expansion, while future trends focus on sustainable operations and AI-driven automation across key ports and coastal facilities.

The Floating Liquefied Natural Gas (FLNG) Terminals Market is strategically critical for meeting the rising global demand for LNG, particularly in regions with constrained land-based infrastructure. AI-enabled predictive monitoring delivers 12% better operational efficiency compared to traditional monitoring systems. Asia-Pacific dominates in volume due to Australia’s fleet of 12 FLNG vessels, while the Middle East leads in adoption with 65% of industrial users implementing modular FSRU solutions. By 2027, advanced modular construction is expected to reduce construction timelines by 20%.

Compliance and ESG initiatives are reshaping operations, with firms committing to 15% emissions reductions by 2030 through energy-efficient technologies and cryogenic optimization. In 2025, Woodside Energy achieved a 10% reduction in downtime via AI-assisted digital twins. Strategic pathways include expanding offshore deployment, investing in automation, and integrating modular vessel designs to ensure operational resilience. The market is positioned as a cornerstone for sustainable LNG supply, balancing compliance, industrial demand, and forward-looking technology adoption.

The Floating Liquefied Natural Gas (FLNG) Terminals Market is shaped by increased global LNG consumption, technological innovations, and strategic offshore infrastructure investments. Modular and prefabricated construction methods are reducing project timelines and operational costs. Industrial adoption is accelerating due to energy-intensive sectors requiring flexible LNG supply solutions. Policy incentives, environmental compliance requirements, and technological modernization—including AI-assisted monitoring and cryogenic efficiency improvements—are key influencers. Additionally, the growth of FSRU deployments in emerging economies supports regional diversification and mitigates reliance on onshore LNG terminals.

Global LNG demand has surged, with industrial and utility sectors accounting for 55% of floating terminal adoption. Rising energy consumption and the need for flexible offshore supply solutions are driving investments in new FLNG vessels and FSRUs. Technological advancements such as AI-assisted monitoring and modular construction reduce operational downtime by 10–12%, enhancing reliability. Strategic deployments in Australia, Brazil, and UAE showcase measurable efficiency improvements, enabling faster integration into industrial gas supply chains and meeting surging regional consumption needs.

FLNG projects require substantial upfront investments, often exceeding USD 500 million per vessel, coupled with complex regulatory approvals from maritime and energy authorities. Environmental compliance mandates, including emissions and water discharge regulations, further increase costs. Supply chain constraints, including fabrication of modular components and cryogenic equipment, may delay project timelines. Countries with stringent permitting processes experience slower adoption, impacting industrial users who require consistent LNG supply. These factors collectively restrain faster market deployment despite strong demand.

Digital technologies, including AI predictive maintenance, real-time monitoring, and IoT-enabled control systems, offer significant efficiency gains. FLNG operators implementing digital twins report up to 12% downtime reduction, improving supply reliability. Expansion into emerging markets like Southeast Asia, with planned capacity exceeding 4 million tonnes per annum, presents new adoption opportunities. Modular vessel construction allows faster deployment in offshore fields, while industrial users increasingly prefer automated LNG import and storage solutions, creating an untapped market for technology-integrated terminals.

Construction and operational costs of FLNG terminals remain high due to specialized cryogenic equipment, offshore installation logistics, and skilled labor requirements. Integration of AI and monitoring technologies increases capital expenditure. Delays in permitting and supply chain disruptions, particularly in modular fabrication and high-precision components, pose operational risks. Companies must navigate environmental regulations, vessel certification standards, and fluctuating LNG spot prices, all of which challenge cost-effective deployment and adoption across industrial and energy-intensive end-users.

Rise in Modular and Prefabricated Construction: Modular construction is reshaping FLNG deployment. 55% of new projects observed cost benefits using prefabricated sections, reducing labor demand and accelerating project timelines.

AI and Digital Twin Adoption: Operators integrating AI-driven predictive maintenance and digital twins report downtime reductions of up to 12%, optimizing performance across offshore terminals.

Expansion into Emerging Markets: Southeast Asia and Middle East regions are increasing FLNG capacity, targeting over 4 million tonnes per annum by 2027, driven by growing industrial demand.

Cryogenic Efficiency Improvements: New cryogenic storage and regasification systems improve energy utilization by 8–10%, reducing LNG losses and environmental impact while enabling more sustainable offshore operations.

The Floating Liquefied Natural Gas (FLNG) Terminals market is segmented by type, application, and end-user, reflecting both technological diversity and deployment contexts. By type, the market includes FLNG vessels, Floating Storage and Regasification Units (FSRUs), and modular offshore terminals, each tailored for specific operational needs and environmental conditions. Applications range from offshore gas monetization, peak-shaving, and seasonal storage to integration with industrial energy supply and export hubs. End-users encompass national oil companies, independent LNG traders, utilities, and industrial gas consumers, reflecting a mix of commercial, strategic, and industrial demands. The segmentation highlights not only the technological preferences of operators but also regional adoption trends, investment focus, and operational flexibility requirements, enabling decision-makers to align infrastructure strategies with specific market needs. Notably, deployment trends indicate that modular units now represent over 50% of new FLNG projects, while FSRUs are increasingly favored for fast-track import terminals in emerging economies.

The FLNG market is primarily dominated by FLNG vessels, accounting for approximately 45% of installations, due to their dual functionality of liquefaction and storage directly at offshore gas fields. FSRUs currently represent 35% of active units, preferred for regasification and import flexibility, and their rapid deployment capability is driving adoption in emerging markets. Modular offshore terminals, comprising the remaining 20%, are gaining traction due to reduced construction timelines, scalable designs, and lower upfront capex. Growth in modular solutions is propelled by automation in prefabrication, AI-enabled process monitoring, and standardization of cryogenic modules, which together optimize safety and operational efficiency.

In terms of application, offshore gas monetization leads, representing roughly 50% of deployments, as it enables production from deepwater fields previously considered uneconomical. Peak-shaving and seasonal storage constitute about 30%, supporting grid balancing and short-term supply optimization. Industrial energy supply and LNG exports account for the remaining 20%, driven by energy-intensive industries and international trading requirements. Notably, rapid deployment FSRUs are being adopted fastest, particularly in Southeast Asia and Latin America, allowing import terminals to come online within 6–12 months. Consumer Adoption & Trend Statistics: In 2024, over 40% of LNG import terminals in emerging economies reported incorporating FLNG or FSRU solutions to meet seasonal demand. Over 35% of utility operators in North America tested floating LNG solutions to enhance supply security.

The leading end-user segment is national oil companies, accounting for roughly 55% of FLNG terminal operations, leveraging FLNG vessels to exploit stranded offshore gas reserves efficiently. Utilities and industrial gas consumers constitute 30%, often using FSRUs or modular units to manage supply flexibly. The remaining 15% involves independent LNG traders and exporters adopting chartered FLNG assets for trading and seasonal supply optimization. Consumer Adoption & Trend Statistics: In 2024, 42% of LNG traders globally incorporated FLNG charter capacity to hedge against supply disruptions. Over 60% of Southeast Asian industrial users preferred modular or short-term FLNG solutions for operational flexibility.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

Asia-Pacific’s dominance is driven by high offshore gas production in countries such as Australia, Malaysia, and Indonesia, which collectively operate over 12 active FLNG vessels and 18 FSRUs. Total installed liquefaction capacity in the region reached 22 million tonnes per annum in 2024. Investment in technology upgrades and digital control systems exceeded USD 1.2 billion. Middle East & Africa is rapidly deploying FSRU terminals in UAE and Egypt, supported by local regulatory incentives and infrastructure expansion, with planned capacity additions exceeding 4 million tonnes per annum by 2027. North America holds 25% market share, driven by LNG exports from Gulf Coast terminals, while Europe accounts for 20%, with new modular FLNG units in Germany and UK. South America constitutes 12%, led by Brazil’s gas monetization projects.

North America holds approximately 25% of the FLNG terminal market, with the Gulf of Mexico serving as the primary hub. Key industries driving demand include utilities, petrochemicals, and industrial gas users. Regulatory changes such as expedited FERC approvals for offshore energy infrastructure have accelerated project timelines. Technological advancements include digital twin monitoring and predictive maintenance systems for FLNG vessels, increasing operational efficiency by 12–15%. Local players like Cheniere Energy are enhancing LNG export capacity with chartered FLNG units capable of processing up to 4 million tonnes per annum. Consumer behavior in North America reflects higher enterprise adoption of flexible LNG solutions, particularly in energy-intensive industrial sectors.

Europe accounts for roughly 20% of the FLNG terminal market, with Germany, UK, and France as leading contributors. European regulatory frameworks, including EU environmental standards and LNG import incentives, promote sustainable operations. Adoption of cryogenic storage optimization and AI-enabled control systems is increasing across terminals. Local players like Exmar NV are implementing floating regasification units with enhanced energy efficiency. European consumption behavior emphasizes compliance-driven adoption, with 65% of new projects designed for emissions reduction and explainable operational control systems. Planned capacity upgrades total 3.5 million tonnes per annum by 2026.

Asia-Pacific leads with 38% market share, driven by Australia, Malaysia, and Indonesia. The region operates 12 FLNG vessels and 18 FSRUs, totaling 22 million tonnes per annum liquefaction capacity. Infrastructure trends include deepwater liquefaction facilities and enhanced supply integration with port terminals. Technology hubs in Singapore and South Korea are driving digitalized monitoring and modular FLNG designs. Local players like Woodside Energy are commissioning new FLNG vessels with integrated AI-enabled operations, reducing downtime by 10%. Regional consumer behavior shows rapid adoption by industrial and energy-intensive users, leveraging flexible import and export solutions.

South America accounts for 12% of the FLNG terminal market, with Brazil and Argentina as key contributors. Infrastructure investments are focused on offshore liquefaction and import terminals along the Brazilian coast, totaling 2.5 million tonnes per annum. Government incentives support LNG infrastructure development, including tax benefits and trade facilitation. Local players such as Petrobras are enhancing FSRU operations to improve export logistics. Consumer adoption is influenced by media and localized industrial demand, particularly in energy-intensive sectors such as chemicals and steel.

Middle East & Africa holds 5% market share, with UAE and South Africa leading growth. Regional demand is tied to oil & gas infrastructure expansion, industrial energy, and power generation. Technological modernization includes remote monitoring systems and cryogenic automation. Local regulations and trade partnerships incentivize rapid deployment of FSRUs, with planned capacity addition exceeding 4 million tonnes per annum by 2027. Local players like ENI UAE are deploying modular FLNG units for offshore production. Consumer behavior shows strong industrial adoption in high-demand sectors and growing interest in imported LNG solutions for domestic power supply.

Australia – 20% Market Share: High offshore gas production capacity and extensive FLNG vessel deployment.

Brazil – 10% Market Share: Strategic offshore gas monetization projects and expanding FSRU infrastructure.

The global Floating Liquefied Natural Gas (FLNG) Terminals market features a competitive landscape shaped by 15–20 active major players, combining engineering firms, shipbuilders, and energy companies. The market is somewhat fragmented, with the top 5 companies (such as Technip Energies, Shell, Petronas, Exmar, and MODEC) controlling an estimated 35–40% of total FLNG project activity.

Key players are leveraging strategic initiatives like joint ventures, long-term charters, and EPC (engineering, procurement, construction) contracts. For instance, Technip Energies continues to expand its global engineering portfolio, while Exmar is investing in both FLNG and FSRU assets to serve flexible floating infrastructure. MODEC is capitalizing on its floating-platform engineering expertise to win both newbuilds and conversions. BW Offshore and Samsung Heavy Industries are working on modular FLNG designs, reducing project risk and enabling faster deployment.

Innovation is another key differentiator: companies are integrating AI‑based predictive maintenance, digital twins, and cryogenic optimization into their FLNG offerings to improve performance and reduce downtime. Moreover, there’s increased collaboration around ESG-compliant vessel design, aiming for lower methane emissions and more efficient boil-off management. This competitive fabric — combining engineering excellence, digital innovation, and strategic partnerships — is driving rapid evolution in the FLNG terminals space.

Eni

Technip Energies

MODEC, Inc.

Exmar NV

BW Offshore Ltd.

Höegh LNG AS

ABB Ltd.

Technological evolution in the FLNG market is advancing rapidly, with a strong focus on modular construction, AI-driven operations, and cryogenic system enhancement. Modular fabrication of liquefaction and storage units allows FLNG vessels to be built in controlled yards and then deployed, reducing both construction risk and time-to-deployment. Many new projects now use prefabricated cryogenic modules, cutting lead times significantly.

To improve operational reliability, FLNG operators are increasingly deploying AI-enabled predictive-maintenance systems. These systems analyze vibration, temperature, and pressure data in real time to predict maintenance needs and avoid unplanned downtime. Reports from pilot integrations suggest that predictive maintenance can reduce downtime by 10–15%, significantly improving uptime for floating assets.

On the cryogenics front, next-generation insulation materials and optimum boil-off management systems are being deployed. Advanced membrane insulation and enhanced containment designs help minimize LNG losses and ensure thermal efficiency during long offshore deployments. Digital twin technology is also being employed for system modeling, enabling operators to simulate liquefaction cycles, boil-off behavior, and safety scenarios in virtual environments before actual deployment.

Additionally, integration of renewable power sources, such as solar or wind, into FLNG power systems is emerging, addressing both fuel consumption and emissions concerns. By combining these digital and engineering technologies, FLNG players are not only improving performance but also aligning with ESG goals and reducing the total cost of ownership for floating LNG assets.

In November 2024, Eni launched the hull of its second FLNG unit, Nguya, at a Chinese shipyard. The unit will be deployed offshore the Republic of Congo, with a liquefaction capacity of 2.4 MTPA, complementing Eni’s existing 0.6 MTPA Tango FLNG. Source: www.eni.com

In mid‑2024, BW LNG secured a 10-year charter with Jordan’s National Electric Power Company (NEPCO) to convert one of its LNG carriers into a floating storage unit (FSU), to be deployed at the Sheikh Sabah terminal. Source: www.bw-group.com

In 2024, Golar LNG reported that its FLNG vessel Gimi reached its commercial operations date (COD) for the Greater Tortue Ahmeyim (GTA) project offshore Mauritania and Senegal, triggering a 20-year lease agreement. Source: www.golarlng.com

In its H1 2024 report, Exmar NV disclosed that it has “upcycled” its Excalibur FSU to meet requirements of the Eni Congo project, and since end‑2023, this FSU has been moored off the coast of Congo. Source: www.exmar.com

The Floating Liquefied Natural Gas (FLNG) Terminals Market Report provides a comprehensive analysis of global FLNG infrastructure, covering key asset types such as FLNG vessels, Floating Storage and Regasification Units (FSRUs), and modular offshore liquefaction platforms. The report segments the market by business model (build-own-operate, charter, and joint ventures), geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America), and application (LNG export, import, peak-shaving, and industrial supply).

In addition to traditional licensing metrics, the report includes technology insight into modular design trends, cryogenic system optimization, AI-driven operations, and digital twin adoption. It also profiles end-users such as national oil companies, utilities, LNG traders, and industrial gas consumers, providing market sizing for each segment. Strategic chapters analyze competitive dynamics, highlighting EPC providers, shipbuilders, and energy companies along with their recent moves, partnerships, and CAPEX pipelines.

Risk factors and regulatory considerations, including offshore permitting, ESG constraints, and methane emissions, are covered in depth. The report further explores emerging opportunities like hybrid FLNG systems combining renewables, carbon capture integration, and small-scale FLNG for remote fields. Overall, the document serves as a strategic guide for decision-makers seeking clarity on market drivers, infrastructure investments, and technological innovation in the evolving FLNG terminals space.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,420.0 Million |

| Market Revenue (2032) | USD 4,751.7 Million |

| CAGR (2025–2032) | 8.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Shell Plc, Petronas LNG Ltd., Golar LNG Limited, Eni, Technip Energies, MODEC, Inc., Exmar NV, BW Offshore Ltd., Höegh LNG AS, ABB Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |