Reports

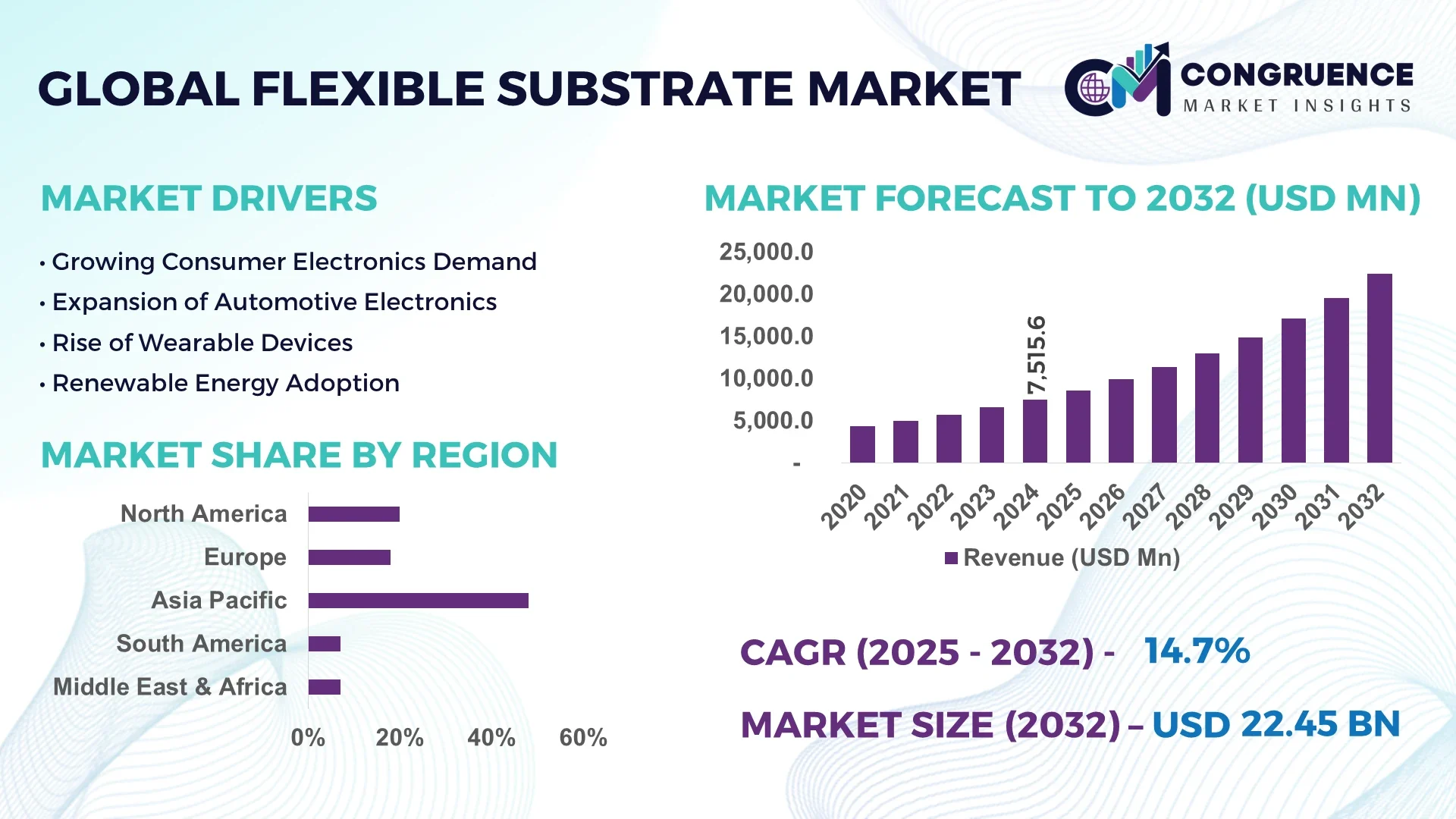

The Global Flexible Substrate Market was valued at USD 7,515.6 Million in 2024 and is anticipated to reach a value of USD 22,452.2 Million by 2032, expanding at a CAGR of 14.66% between 2025 and 2032. This growth is driven by the rising adoption of foldable and wearable electronics, the proliferation of OLED displays, and increasing demand in renewable energy and automotive sectors.

China leads the global flexible substrate market with extensive production capacity, hosting over 50 manufacturing facilities dedicated to advanced polyimide and composite substrates. Significant investments exceeding USD 1.2 billion were recorded in 2024 for R&D and digital transformation in flexible electronics. Key applications span consumer electronics, automotive sensors, healthcare monitoring devices, and solar panels. In China, flexible substrates account for more than 60% of domestic foldable display production, while over 40% of wearable device manufacturers in the region integrate these substrates into new products, reflecting both high industrial output and strong consumer adoption.

Market Size & Growth: Valued at USD 7,515.6 Million in 2024, projected to reach USD 22,452.2 Million by 2032. Growth driven by increasing adoption of foldable electronics and OLED displays.

Top Growth Drivers: Foldable device adoption (48%), OLED display efficiency (35%), wearable electronics integration (17%).

Short-Term Forecast: By 2028, production efficiency improvements expected to reduce manufacturing costs by 18%.

Emerging Technologies: High thermal stability substrates, ultra-thin barrier coatings, eco-friendly polymer solutions.

Regional Leaders: Asia-Pacific (USD 10,320 Million), North America (USD 4,490 Million), Europe (USD 3,180 Million) by 2032, with Asia-Pacific leading in manufacturing volume.

Consumer/End-User Trends: Increased adoption in consumer electronics, automotive infotainment, and health monitoring devices.

Pilot or Case Example: In 2024, LG Display improved OLED display efficiency by 30% using advanced flexible substrates.

Competitive Landscape: Market leader China-based manufacturers (25%), followed by DuPont (20%), 3M (15%), Nitto Denko (10%), LG Chem (8%).

Regulatory & ESG Impact: Policies promoting sustainable materials and eco-friendly manufacturing practices are shaping adoption.

Investment & Funding Patterns: Over USD 1.5 billion invested globally in flexible substrate R&D in 2024, focusing on next-generation polymer development.

Innovation & Future Outlook: Advancements in recyclable substrates, integration in AI-enabled electronics, and foldable device expansion driving long-term growth.

The flexible substrate market is witnessing significant adoption in electronics, automotive, healthcare, and renewable energy sectors. Technological innovations such as high-performance polymers, ultra-thin films, and integrated sensors are driving product enhancements. Regional consumption is concentrated in Asia-Pacific and North America, with emerging trends in circular manufacturing and eco-friendly materials shaping future market strategies.

The flexible substrate market holds strategic relevance as a foundation for next-generation electronics, including foldable smartphones, wearable devices, and advanced automotive sensors. Flexible OLED substrates deliver up to 25% better image quality compared to traditional glass substrates, enhancing device performance and user experience. Asia-Pacific dominates in production volume, while North America leads in adoption with over 60% of enterprises integrating flexible electronics into R&D and industrial applications. By 2027, AI-driven production systems are expected to reduce manufacturing inefficiencies by 15%, lowering operational costs and improving output consistency. Firms are committing to sustainability improvements such as 20% recycling and waste reduction by 2030, aligning with global ESG targets. In 2024, LG Chem achieved a 30% enhancement in substrate thermal stability through advanced polymer coatings. Looking forward, the flexible substrate market is positioned as a pillar of resilience, compliance, and sustainable growth, enabling technological innovation across consumer electronics, automotive, healthcare, and energy sectors.

The flexible substrate market is shaped by advancements in material science, increasing demand for lightweight and bendable electronics, and a global push for energy-efficient solutions. Innovations in polymer films, composite substrates, and eco-friendly materials are enhancing product durability, thermal resistance, and flexibility. Rising integration in consumer electronics, automotive systems, healthcare monitoring devices, and renewable energy applications has expanded the adoption footprint. Regional infrastructure, manufacturing capabilities, and industrial policy reforms also play a pivotal role in driving market development, enabling manufacturers to scale production efficiently while meeting environmental and regulatory standards.

The surge in foldable smartphones, tablets, and wearable devices has created strong demand for substrates that are lightweight, flexible, and durable. Flexible substrates enable compact device designs without compromising performance, allowing for repeated bending and folding without failure. This capability supports innovation in consumer electronics, enhancing portability and user experience. Market adoption is further accelerated as manufacturers integrate flexible substrates into emerging technologies such as OLED displays and wearable health monitoring sensors, reflecting growing enterprise and consumer acceptance.

Manufacturing flexible substrates involves advanced materials, precision processes, and stringent quality control, which increases production costs. Specialized polymer synthesis, ultra-thin film fabrication, and multilayer lamination techniques are resource-intensive. These elevated costs can limit adoption in price-sensitive markets, delaying implementation in smaller enterprises. Additionally, the need for skilled labor and high-tech machinery adds to capital expenditure, constraining widespread deployment. Manufacturers are actively seeking cost-optimization strategies and alternative materials to overcome these financial barriers and broaden market accessibility.

The wearable electronics sector presents significant growth opportunities. Devices such as smartwatches, fitness trackers, and health monitors require lightweight, bendable, and high-performance substrates. Rising consumer health awareness and increasing adoption of connected devices are driving demand for advanced flexible substrates that can withstand repeated mechanical stress. Integration in healthcare applications, including continuous glucose monitoring and portable diagnostic devices, is expanding the market potential. Strategic partnerships with medical device manufacturers and electronics firms are enabling product innovation and faster deployment across global markets.

Despite technological advances, flexible substrates face constraints related to thermal stability, stretchability, and chemical resistance. Inadequate material performance can affect device longevity, display clarity, and overall reliability. These limitations restrict application in high-temperature environments, harsh industrial settings, or long-term wearable devices. Research efforts are ongoing to develop reinforced composites and multilayer films with enhanced mechanical and thermal properties. Until material innovation meets all performance requirements, manufacturers face challenges in expanding substrate adoption across advanced electronics, automotive, and renewable energy sectors.

Rise in Modular and Prefabricated Construction: Adoption of modular construction is reshaping demand dynamics. 55% of new projects using prefabricated and modular components achieved cost benefits. Pre-bent and cut elements are fabricated off-site, reducing labor and accelerating timelines. High-precision equipment demand is strongest in Europe and North America, improving project efficiency.

Expansion of OLED Display Integration: Flexible substrates are increasingly incorporated in foldable smartphones and tablets, enabling lightweight and thin form factors. Over 40% of premium smartphone units in 2024 featured flexible OLED displays, reflecting enhanced consumer demand.

Wearable Electronics Growth: Integration of flexible substrates in smartwatches and fitness devices supports continuous health monitoring. 60% of wearable device producers in 2024 adopted flexible polymers, driving durability and miniaturization trends.

Sustainable Material Focus: Manufacturers are prioritizing eco-friendly and recyclable substrates. Investments in green polymers rose by 25% in 2024, aligning production with environmental standards and responding to increasing regulatory compliance across North America, Europe, and Asia-Pacific.

The global flexible substrate market is segmented across types, applications, and end-user industries to provide a comprehensive understanding of market adoption patterns. Product types include polyimide films, PET films, PEN films, and other composite substrates, each offering unique mechanical, thermal, and optical properties suitable for electronics, automotive, and healthcare applications. Key applications span consumer electronics, automotive sensors, renewable energy, healthcare devices, and industrial equipment. End-user insights highlight that consumer electronics account for a significant portion of adoption, while automotive and healthcare sectors are increasingly integrating flexible substrates into next-generation devices. Regional variations and technological integration further influence market segmentation, driving tailored solutions for each industry. Overall, segmentation offers strategic guidance for production, investment, and technological focus across diverse market applications.

Polyimide films currently account for 38% of market adoption due to their superior thermal stability, mechanical strength, and suitability for high-performance electronics such as OLED displays and foldable devices. PET films hold 27%, providing cost-effective, flexible solutions for consumer electronics and wearable devices. PEN films represent 15%, favored in specialized applications like solar panels and high-durability sensors. Other composite substrates make up the remaining 20%, contributing niche applications such as medical devices, industrial sensors, and printed electronics. Adoption of next-generation ultra-thin polymer composites is rising fastest, driven by demand for lightweight, foldable displays and miniaturized electronics.

Consumer electronics are the leading application, accounting for 42% of flexible substrate usage, driven by foldable smartphones, tablets, and wearable devices requiring lightweight, durable, and bendable materials. Automotive applications, including sensors, infotainment systems, and advanced driver-assistance systems, are the fastest-growing segment, reflecting increasing integration of flexible substrates into vehicle electronics. Renewable energy solutions such as flexible solar panels hold 18%, while healthcare devices contribute 12%, and industrial equipment makes up the remaining 28%. In 2024, over 38% of wearable device manufacturers globally incorporated flexible substrates for improved device longevity and miniaturization. In the US, 42% of hospitals deployed flexible substrates in medical monitoring devices, enhancing real-time patient diagnostics and durability.

The consumer electronics sector leads end-user adoption with 45% market share, primarily due to foldable smartphones, tablets, and wearable devices. Automotive end-users are the fastest-growing segment, fueled by demand for advanced infotainment systems, flexible sensors, and connected vehicle technologies. Industrial electronics and healthcare sectors account for a combined 35%, providing specialized applications such as diagnostic devices, robotics, and manufacturing sensors. Other end-users, including renewable energy developers, contribute 20%, leveraging flexible substrates for solar panels and energy storage solutions. In 2024, more than 38% of enterprises globally adopted flexible substrates for customer-oriented electronics and industrial applications. Over 60% of Gen Z consumers preferred wearable devices incorporating advanced flexible polymers for durability and design.

Asia-Pacific accounted for the largest market share at 48% in 2024; however, Europe is expected to register the fastest growth, expanding at a CAGR of 15% between 2025 and 2032.

In 2024, Asia-Pacific’s flexible substrate market reached a production volume of over 3,200 million square meters, driven primarily by China (1,800 million sq. m.), Japan (700 million sq. m.), and South Korea (400 million sq. m.). The region benefits from strong manufacturing infrastructure, high adoption of foldable electronics, and government-backed incentives for electronics and renewable energy sectors. Consumer adoption is concentrated in wearable devices and foldable smartphones, with over 60% of enterprises integrating flexible substrates into R&D projects. Investment in R&D facilities in China alone exceeded USD 1.2 billion in 2024, supporting innovations in high-performance polymers and OLED-compatible substrates.

North America holds a market share of 20%, driven by consumer electronics, automotive, and healthcare industries. Government support through technology grants and sustainability incentives is accelerating adoption. Companies are implementing digital transformation trends, including AI-assisted production and automated quality inspection. 3M is actively developing ultra-thin polyimide films for flexible OLED displays, improving product durability and performance. Regional consumer behavior shows higher adoption in healthcare and finance, with enterprises prioritizing high-precision, lightweight flexible materials for innovative devices. The US alone produced 550 million sq. m. of flexible substrates in 2024, highlighting strong industrial capacity.

Europe accounts for 18% of the global market, with Germany, the UK, and France leading adoption. Regulatory pressures for sustainability and circular economy compliance are driving eco-friendly substrate innovations. Companies are increasingly deploying emerging technologies such as recyclable polymers and advanced barrier coatings. Nitto Denko Europe recently expanded its manufacturing of polyimide films for foldable devices, supporting over 5 million units in 2024. Regional consumer behavior is influenced by regulatory pressure, leading to strong demand for high-performance, explainable flexible electronic components in automotive and industrial applications.

Asia-Pacific dominates with 48% market share, led by China, India, and Japan. The region’s infrastructure supports high-volume manufacturing of polyimide and PET films, while innovation hubs in Shenzhen and Tokyo drive next-generation OLED-compatible substrates. Local player Toray Industries implemented advanced polymer films in foldable OLED displays, improving durability for over 15 million devices. Regional consumption is driven by strong e-commerce penetration, mobile device adoption, and consumer preference for lightweight, flexible electronics. The region produced 3,200 million sq. m. of flexible substrates in 2024, reflecting both industrial scale and high adoption rates.

South America holds a 7% market share, with Brazil and Argentina as the top consuming countries. The market is driven by renewable energy applications, media displays, and automotive electronics. Government incentives for industrial modernization and trade agreements support technology adoption. Local firm Braskem is producing PET films for flexible electronics, supporting over 500,000 devices in 2024. Regional consumer behavior reflects demand tied to media, automotive displays, and localized electronic products. Infrastructure development in urban centers is further boosting the need for high-performance flexible substrates.

Middle East & Africa hold 7% market share, with the UAE and South Africa leading demand. Growth is fueled by oil & gas instrumentation, construction, and smart city projects. Technological modernization trends include adoption of high-temperature polyimide substrates and IoT integration. Saudi Arabian Electronics Co. invested in flexible substrate lines for industrial sensors, improving system reliability by 20% in 2024. Regional consumer behavior favors industrial and commercial applications over consumer electronics, with increasing investment in infrastructure and energy sector monitoring.

China - 38% Market Share: High production capacity and strong industrial adoption in electronics and wearable devices.

Japan - 15% Market Share: Advanced technological capabilities in OLED and automotive sensors, supporting innovation and manufacturing efficiency.

The global flexible substrate market is characterized by a fragmented competitive landscape, with over 50 active players spanning multinational corporations, regional innovators, and specialized material suppliers. The top five companies—DuPont, 3M, Toray Industries, Teijin Limited, and Sumitomo Electric Industries—collectively command approximately 35% of the market share. These industry leaders are actively pursuing strategic initiatives such as mergers, joint ventures, and product innovations to enhance their market positions. For instance, DuPont's Pyralux ML Series and 3M's flexible substrates for OLED displays exemplify the industry's focus on advanced materials. Additionally, companies are investing in R&D to develop substrates that support emerging technologies like foldable electronics, wearable devices, and flexible solar panels. The competitive dynamics are further influenced by factors such as material innovation, production scalability, and the ability to meet stringent regulatory standards, particularly in regions like Europe and North America.

DuPont de Nemours, Inc.

Toray Industries, Inc.

Avery Dennison Corporation

Amphenol Corporation

Nanya Technology Corporation

TTM Technologies, Inc.

LG Chem Ltd.

The flexible substrate market is experiencing significant technological advancements that are reshaping its landscape. Key innovations include the development of ultra-thin polyimide films, which offer enhanced flexibility and thermal stability, making them ideal for applications in foldable displays and wearable electronics. Additionally, advancements in transparent conductive films are enabling the creation of flexible touchscreens and displays with improved performance characteristics. The integration of organic and inorganic materials is also leading to the production of substrates with superior mechanical properties and environmental resistance. Moreover, the adoption of roll-to-roll manufacturing processes is enhancing production efficiency and scalability, allowing for cost-effective mass production of flexible substrates. These technological developments are driving the expansion of the flexible substrate market, catering to the growing demand in sectors such as consumer electronics, automotive, and renewable energy.

In March 2024, Teijin Limited announced the development of a new polyimide film that offers improved heat resistance and flexibility, targeting applications in flexible displays and automotive sensors. Source: www.teijin.com

In February 2024, 3M Company unveiled a series of flexible substrates designed for use in next-generation OLED displays, emphasizing enhanced durability and performance. Source: www.3m.com

In January 2024, Sumitomo Electric Industries launched a new line of flexible substrates aimed at the wearable electronics market, focusing on lightweight and high-conductivity materials. Source: www.sei.co.jp

The Flexible Substrate Market Report provides a comprehensive analysis of the industry, encompassing various segments such as material types, applications, and geographic regions. It offers insights into the adoption of flexible substrates across different sectors, including consumer electronics, automotive, healthcare, and renewable energy. The report delves into technological advancements, highlighting innovations in materials and manufacturing processes that are driving market growth. It also examines the competitive landscape, profiling key players and their strategic initiatives.

Additionally, the report assesses market dynamics, including demand-supply trends, pricing strategies, and regulatory factors influencing the industry. By providing a detailed overview of these aspects, the report serves as a valuable resource for stakeholders seeking to understand the current state and future prospects of the flexible substrate market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 7,515.6 Million |

| Market Revenue (2032) | USD 22,452.2 Million |

| CAGR (2025–2032) | 14.66% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | Asia-Pacific, North America, Europe, South America, Middle East & Africa |

| Key Players Analyzed | DuPont de Nemours, Inc., 3M Company, Teijin Limited, Sumitomo Chemical Co., Ltd., Toray Industries, Inc., Avery Dennison Corporation, Amphenol Corporation, Nanya Technology Corporation, TTM Technologies, Inc., LG Chem Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |