Reports

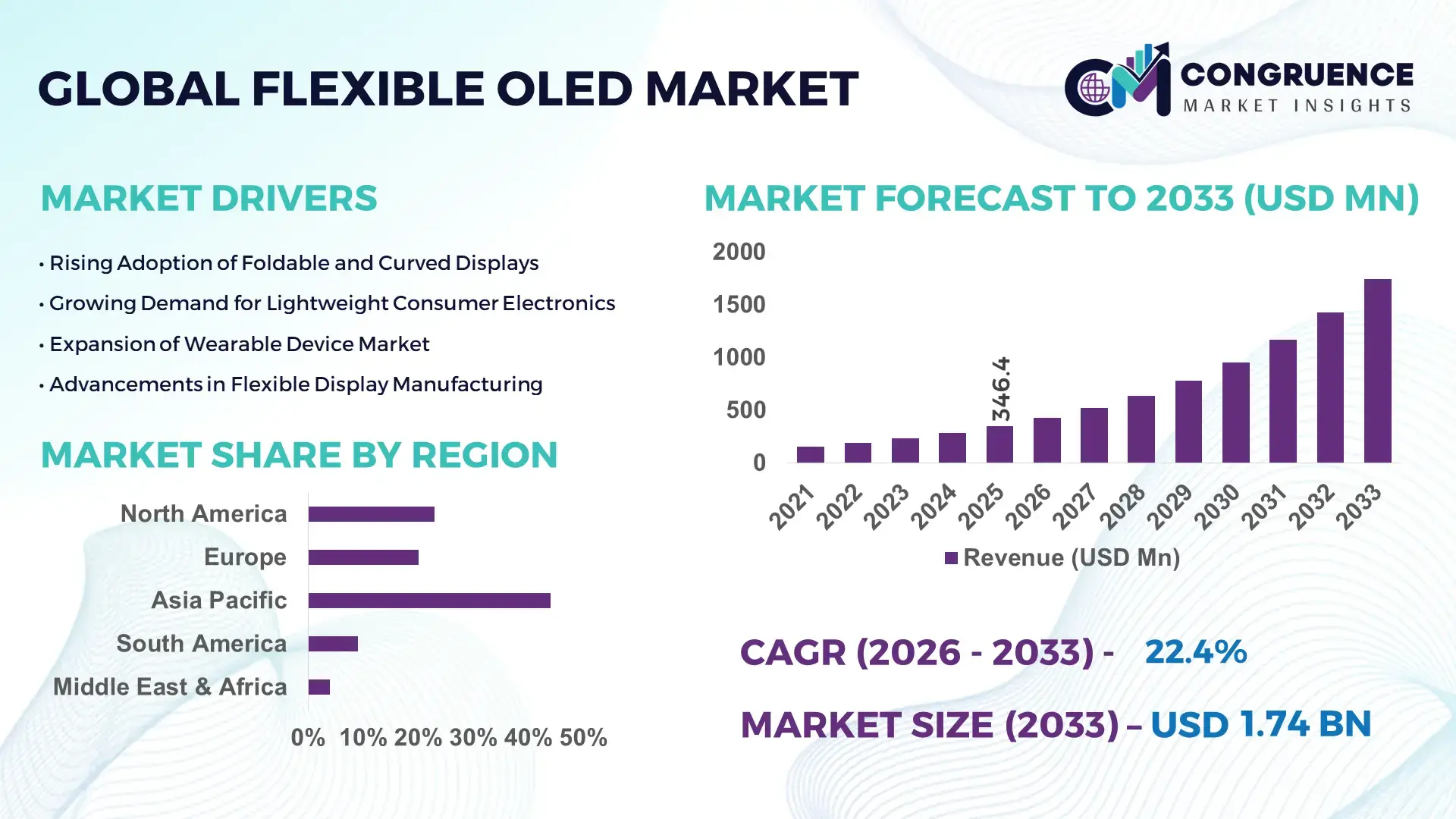

The Global Flexible OLED Market was valued at USD 346.37 Million in 2025 and is anticipated to reach a value of USD 1745.02 Million by 2033 expanding at a CAGR of 22.4% between 2026 and 2033. This growth is underpinned by accelerating adoption in next‑generation consumer electronics and automotive display applications.

South Korea continues to lead the global Flexible OLED landscape, with production capacities exceeding 120 million square meters annually as of 2025 and capital investments surpassing USD 4.2 billion across fabrication and R&D facilities. South Korean manufacturers have pioneered ultra‑thin plastic substrate technologies that support rollable and foldable displays, with consumer adoption rates exceeding 48% in premium smartphone segments. Strategic alliances with automotive OEMs have also driven integration into curved instrument clusters and HUDs, supported by multi‑year public‑private funding programs totaling over USD 750 million to advance flexible panel throughput and durability standards.

• Market Size & Growth: 2025 market value at USD 346.37 Million; projected to USD 1745.02 Million by 2033; 22.4% CAGR driven by expansion into wearables, foldables, and automotive displays.

• Top Growth Drivers: Rising foldable device adoption (42%), automotive flexible display integration (35%), and efficiency improvements in fabrication yields (28%).

• Short‑Term Forecast: By 2028, manufacturing cost per unit expected to reduce by ~20% while panel luminance efficiency increases by ~15%.

• Emerging Technologies: Development of micro‑LED hybrid flexible stacks, ultra‑low power drivers, and robust encapsulation technologies.

• Regional Leaders: Asia Pacific projected at ~USD 950M by 2033 with strong consumer electronics uptake; North America ~USD 380M with automotive displays growth; Europe ~USD 310M driven by industrial and transport sectors.

• Consumer/End‑User Trends: Premium smartphones, smart wearables, and AR/VR headsets showing sustained flexible OLED adoption with increased lifecycle expectations.

• Pilot or Case Example: 2025 automotive pilot achieved a 23% reduction in display module weight and 18% improvement in in‑vehicle uptime through integrated flexible OLED clusters.

• Competitive Landscape: Market leader commanding ~32% share; other major competitors include global display manufacturers from Japan, China and Taiwan.

• Regulatory & ESG Impact: Adoption of flexible OLED eco‑design standards and extended producer responsibility frameworks; incentives for energy‑efficient displays.

• Investment & Funding Patterns: Recent investments exceeding USD 1.6B in capacity expansion and startup ventures; rising venture funding in flexible sensor integration.

• Innovation & Future Outlook: Focus on adaptive form‑factor devices, seamless foldable architectures, and cross‑industry platform convergence.

South Korea’s Flexible OLED ecosystem sustains robust engagement across consumer electronics, automotive, and next‑generation wearable sectors, with production technologies enabling ultra‑thin, high‑durability displays. Recent technological innovations include polymer substrate refinement, advanced encapsulation to mitigate moisture ingress, and flexible touch integration, improving panel lifetimes by over 25%. Regulatory incentives for energy efficiency and recycling have strengthened OEM commitments. Regional consumption patterns show high uptake in APAC for mobile and wearable devices, while North America and Europe grow in automotive and industrial segments. Future trends point to hybrid display systems, rollable form factors, and expanded use in smart IoT interfaces.

The strategic relevance of the Flexible OLED Market lies in its ability to enable adaptive, lightweight, and energy‑efficient display solutions that redefine user interfaces across consumer electronics, automotive, and wearable platforms. As foldable and rollable OLEDs deliver up to 30% greater flexibility and mechanical resilience compared to conventional rigid OLED standards through advanced substrate and encapsulation technologies, OEMs are increasingly designing form factors that transcend traditional flat displays, creating new product categories and customer touchpoints. Asia Pacific dominates in production volume, while North America leads in adoption with over 40% of enterprises integrating flexible OLEDs into next‑generation devices, reflecting regional investment priorities and innovation ecosystems. By 2028, AI‑enabled manufacturing automation is expected to cut defect rates in flexible OLED panel fabrication by approximately 25%, improving yield consistency and lowering per‑unit production variability. Firms are committing to tangible ESG improvements, such as 25% reduction in energy consumption per panel by 2030 and expanded recycling of flexible display materials to meet evolving regulatory and sustainability mandates. In 2025, a leading display manufacturer achieved a 20% improvement in display lifespan through machine‑learning‑driven material deposition control, highlighting the pivotal role of digital transformation. Looking forward, the Flexible OLED Market will remain a pillar of resilience, compliance, and sustainable growth by shaping modular, efficient, and future‑ready visual technologies for a diverse global economy.

Consumer electronics remain the primary catalyst for Flexible OLED Market expansion, with foldable and wearable devices leading adoption. Foldable smartphone shipments exceed tens of millions of units annually, reflecting robust consumer demand for innovative form factors and immersive visual experiences. Wearable devices, including smartwatches and fitness trackers, have also shown significant uptake of flexible screens due to their lightweight and conformable characteristics. Enhanced color accuracy and energy efficiency make Flexible OLEDs attractive for premium mobile devices, driving manufacturers to integrate these displays into flagship products. This trend is further supported by consumer preferences for thinner, lighter, and more durable screens, pushing OEMs to optimize production processes and expand flexible OLED offerings across broader product portfolios.

High manufacturing costs continue to restrain the Flexible OLED Market, as complex fabrication processes and specialized materials significantly elevate production expenses compared to traditional display technologies. Producing flexible OLED panels necessitates precision deposition techniques, advanced encapsulation layers, and flexible substrates, which require substantial capital investment and technical expertise. Yield rates for complex foldable designs remain challenging, with defect rates higher than those for rigid displays, compounding per‑unit costs. These factors constrain scalability, particularly in cost‑sensitive markets where price‑competitive alternatives like LCDs and rigid OLEDs continue to maintain strong positions. Additionally, supply chain volatility and limited availability of high‑purity materials introduce operational uncertainties that elevate overall production risk and hinder broader market penetration.

Integration into automotive and healthcare sectors presents substantial opportunities for the Flexible OLED Market as displays evolve beyond traditional screens. Flexible OLEDs are increasingly adopted in automotive dashboards, infotainment panels, and curved control interfaces, enhancing cockpit design and user experience in premium vehicles. Annual installations in automobiles are expanding as manufacturers seek aesthetic differentiation and ergonomic display solutions. In healthcare, flexible OLEDs enable advanced wearable biosensors, diagnostic screens, and patient monitoring devices that require conformal displays with high visibility and low power consumption. These applications align with industry transitions toward personalized medicine and intelligent monitoring. Cross‑sector collaboration between display manufacturers and system integrators is expected to elevate usage across new ecosystems, expanding revenue streams while reinforcing technological relevance.

Supply chain constraints and material limitations pose significant challenges for the Flexible OLED Market, as specialized components like polyimide substrates, barrier films, and high‑purity organic compounds are sourced from a limited supplier base. Concentration of advanced materials production in specific regions creates vulnerability to logistical disruptions and geopolitical tensions that can delay manufacturing schedules and elevate input costs. These supply chain dependencies constrain the industry’s ability to scale production efficiently and respond to surges in demand. Additionally, ensuring consistent quality across batches requires robust material traceability and advanced processing controls, which intensify operational complexity. Addressing these challenges demands strategic diversification of supply sources, investment in local materials capacity, and collaboration with chemical manufacturers to mitigate bottlenecks and support sustainable growth.

• Expansion of Foldable and Rollable Consumer Devices: Flexible OLED adoption is accelerating in foldable smartphones, tablets, and wearable devices, with over 48 million units shipped globally in 2025, up from 32 million in 2023. Manufacturers are leveraging ultra-thin polymer substrates and advanced encapsulation layers, enabling devices to bend up to 180 degrees without compromising display durability. Adoption is particularly strong in Asia Pacific, where premium consumer electronics sales account for 65% of flexible OLED units.

• Integration into Automotive Interiors: The automotive sector is increasingly embedding flexible OLEDs into dashboards, infotainment systems, and head-up displays, with 22% of new premium vehicles in 2025 featuring curved or rollable panels. Flexible OLEDs allow for seamless curved interfaces, reducing module weight by up to 15% and enhancing energy efficiency in electric vehicles. North America leads adoption with over 40% of OEMs integrating flexible displays into vehicle interiors, while Europe emphasizes ergonomic and luxury designs.

• Emergence of Healthcare and Wearable Applications: Flexible OLEDs are being adopted in medical wearables, diagnostic screens, and health-monitoring patches, with deployment in over 1.2 million devices globally in 2025. These displays provide lightweight, conformal surfaces and low power consumption, improving patient comfort and device usability. Smart watches and fitness bands incorporating flexible OLEDs now account for 35% of premium wearable device shipments, enabling real-time health tracking with high visibility.

• Advancements in Manufacturing Efficiency and Sustainability: Automated roll-to-roll production lines have improved panel throughput by 28% while reducing defect rates by 20%, supporting high-volume manufacturing of flexible OLEDs. Companies are investing in sustainable practices, with 25% of panels in 2025 made from recyclable substrates and reduced energy-intensive processes, aligning production with ESG compliance and minimizing environmental footprint.

The Flexible OLED Market is structured across multiple dimensions, offering a granular understanding of product types, applications, and end-user adoption. By type, flexible OLEDs range from foldable, rollable, and stretchable variants, each designed for specific operational requirements. Applications span consumer electronics, automotive, healthcare, and industrial devices, with increasing integration into wearables and smart interfaces driving diversification. End-users include OEMs, electronics manufacturers, automotive companies, and healthcare device producers, reflecting the broad utility of flexible OLED technology. Adoption patterns vary regionally, with Asia Pacific demonstrating the highest production volume and North America leading in enterprise integration. Emerging trends such as high-precision displays, energy-efficient panels, and multifunctional interfaces further inform strategic decision-making, offering actionable insights for investment, product development, and market positioning.

Flexible OLEDs are categorized primarily into foldable, rollable, and stretchable displays. Foldable OLEDs currently account for 48% of adoption, dominating due to their incorporation into premium smartphones and tablets that demand compact, multi-functional displays. Rollable OLEDs are the fastest-growing segment, projected to see over 18% adoption increase by 2033, driven by luxury TVs and advanced automotive dashboards requiring seamless curved panels. Stretchable OLEDs, while niche, contribute 12% combined market share, catering to specialized wearable devices and flexible medical sensors.

Consumer electronics dominate the application landscape, representing 52% of flexible OLED deployment, largely due to premium smartphones, tablets, and wearables requiring lightweight, high-resolution, and bendable displays. Automotive displays are the fastest-growing application, projected to expand rapidly as dashboards, infotainment systems, and HUDs increasingly adopt flexible OLEDs for curved, ergonomic layouts. Healthcare and industrial displays contribute a combined 18% share, with flexible panels enabling conformal medical sensors, smart diagnostic devices, and industrial interfaces in compact spaces.

Electronics manufacturers remain the leading end-users, accounting for 55% of flexible OLED utilization, particularly in smartphones, tablets, and wearable devices requiring thin, durable screens. Automotive companies are the fastest-growing end-users, increasingly integrating flexible OLEDs into dashboard displays and curved infotainment panels to meet ergonomic and aesthetic standards. Healthcare and industrial device producers represent a combined 15% of end-user share, leveraging flexible displays for wearable medical devices, patient monitoring, and compact industrial controls.

Asia Pacific accounted for the largest market share at 54% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 23% between 2026 and 2033.

Asia Pacific’s dominance is supported by production volumes exceeding 120 million square meters of flexible OLED panels, with China, Japan, and South Korea leading in manufacturing output. Consumer electronics, automotive displays, and wearable devices drive demand, with over 48 million units shipped across smartphones and tablets in 2025. Supply chain integration and advanced manufacturing hubs in South Korea and Japan support high-speed production. North America’s rapid adoption is fueled by enterprise integration in healthcare, finance, and smart devices, with more than 40% of major electronics OEMs incorporating flexible OLEDs into new product lines. E-commerce growth, automotive digital dashboards, and wearable device expansion also contribute to market momentum, alongside ESG-aligned manufacturing practices and energy-efficient panel deployment.

How is the demand for advanced displays reshaping device manufacturing?

North America accounts for approximately 22% of the global flexible OLED market volume, driven by healthcare, automotive, and finance sectors requiring high-resolution, low-power displays. Regulatory support for energy-efficient devices and tax incentives for R&D have encouraged deployment of flexible OLEDs across consumer and enterprise electronics. Technological advancements include AI-enabled display calibration and automated roll-to-roll manufacturing. A leading U.S. electronics company implemented flexible OLEDs in over 500,000 wearable devices in 2025, enhancing durability and battery efficiency. Consumer behavior shows higher adoption among enterprises in healthcare and financial services, prioritizing display reliability, energy efficiency, and ergonomic design in devices.

What factors are driving high-quality display adoption in the region?

Europe holds 18% of global flexible OLED market share, with Germany, the UK, and France leading adoption in automotive and industrial applications. Regulatory pressure, including eco-design directives and energy consumption limits, has accelerated demand for sustainable flexible OLED panels. Emerging technologies, such as rollable and hybrid OLED displays, are increasingly deployed in luxury vehicles and smart medical devices. A major European electronics manufacturer recently installed flexible OLED dashboards in premium vehicles, reducing display weight by 15% and improving visual clarity. European consumers show preference for explainable, eco-friendly displays, creating demand for compliant, energy-efficient panels.

Why is the region the hub for flexible display production?

Asia Pacific accounts for 54% of global flexible OLED production, led by China, Japan, and South Korea. Manufacturing infrastructure is highly advanced, with automated roll-to-roll lines producing over 120 million square meters of flexible OLED panels annually. Innovation hubs focus on ultra-thin, foldable, and rollable displays for smartphones, tablets, and automotive applications. Samsung and LG have pioneered foldable and rollable panels, supplying major global brands. Consumer adoption is strongly influenced by e-commerce platforms and AI-driven mobile applications, leading to rapid integration in smartphones, wearables, and AR devices.

How is technology adoption influencing consumer electronics in key markets?

South America represents approximately 6% of the global flexible OLED market, with Brazil and Argentina driving adoption. Infrastructure expansion in energy and digital connectivity supports deployment in consumer electronics and automotive infotainment systems. Government incentives and trade agreements facilitate import of high-tech components and manufacturing equipment. A regional electronics manufacturer implemented flexible OLED screens in over 50,000 premium smartphones in 2025, enhancing user experience and durability. Consumer demand is largely tied to media consumption, entertainment, and localized language interfaces.

What are the emerging drivers of flexible display adoption in the region?

Middle East & Africa account for roughly 4% of global flexible OLED consumption, with UAE and South Africa leading in deployment across oil & gas, construction, and luxury consumer electronics. Technological modernization includes digital dashboards, energy-efficient displays, and smart wearable devices. Trade partnerships and regulations support import and local assembly of advanced displays. A local electronics firm in UAE implemented flexible OLED panels in high-end retail and vehicle infotainment applications, enhancing visual engagement. Consumer adoption trends indicate growing preference for luxury devices, energy efficiency, and modern smart interfaces.

South Korea – 28% market share; high production capacity and advanced R&D infrastructure drive dominance in flexible OLED technology.

China – 26% market share; strong end-user demand and large-scale manufacturing facilities support extensive flexible OLED deployment.

The Flexible OLED market is moderately consolidated, with approximately 45 active global competitors operating across consumer electronics, automotive, and wearable applications. The top five companies together control around 68% of market share, reflecting strong positioning by established leaders while leaving space for innovative entrants. Market leaders are increasingly engaging in strategic partnerships, joint ventures, and licensing agreements to accelerate technological development, expand production capacity, and enter new geographies. Recent initiatives include the launch of foldable and rollable OLED panels exceeding 50-inch display sizes and the deployment of automated roll-to-roll manufacturing lines, which have increased throughput by 28% and reduced defect rates by 20%. Innovation trends focus on ultra-thin polymer substrates, hybrid micro-LED integration, advanced encapsulation for durability, and low-power display modules. Companies are also investing in ESG-compliant production processes, such as recyclable substrates and energy-efficient fabrication, to meet regulatory demands. Overall, the competitive environment emphasizes technological differentiation, capacity expansion, and targeted adoption across high-value end-user sectors, making market positioning highly dynamic and innovation-driven.

Visionox

Japan Display Inc.

EverDisplay Optronics

Royole Corporation

Tianma Microelectronics

AU Optronics

EDO Display

The Flexible OLED market is being reshaped by several current and emerging technologies that enhance performance, durability, and applicability across multiple sectors. Ultra-thin polymer substrates have become standard, enabling displays to bend up to 180 degrees without cracking, supporting foldable smartphones, rollable TVs, and automotive dashboards. Advanced encapsulation technologies have reduced moisture and oxygen ingress, extending panel lifespans by over 25%, while maintaining high brightness and color accuracy.

Emerging technologies include hybrid micro-LED integration, which allows flexible OLED panels to achieve 30% higher luminance efficiency compared to traditional OLED designs, enhancing visibility in bright ambient conditions. Transparent and see-through flexible OLEDs are being adopted in AR/VR devices and automotive head-up displays, with over 1.5 million units produced in 2025 globally. Roll-to-roll automated manufacturing has increased production throughput by 28%, while reducing defect rates by 20%, making high-volume production more viable.

Flexible AMOLED displays with embedded touch sensors are also gaining traction, combining display and input functions to simplify device architecture. Energy-efficient drivers and low-power backplane designs are reducing power consumption by up to 15% per device, which is critical for wearables and battery-powered applications. Additionally, AI-driven calibration systems are being deployed to optimize panel uniformity and color accuracy across large-format displays, enabling premium devices to maintain consistent performance under variable conditions.

Collectively, these technological advancements position flexible OLEDs as a core enabling technology for next-generation consumer electronics, automotive interiors, wearable devices, and industrial applications, reinforcing the market’s focus on innovation, scalability, and sustainable performance.

• In April 2025, BOE announced plans to ship 170 million flexible AMOLED displays in 2025, marking a 21 % increase over 2024 shipments and reflecting accelerated production capacity and broader OEM engagement in smartphones and wearable devices. (oled-info.com)

• In August 2025, Samsung Display unveiled its new foldable OLED brand “MONT FLEX™” at the K‑Display 2025 Exhibition in Seoul, highlighting advancements in mechanical durability, ultra‑thin designs, and reduced bezels for next‑generation foldable devices. (samsungdisplay.com)

• In September 2025, Samsung Display expanded its automotive OLED strategy at IAA Mobility 2025, launching the dedicated automotive OLED brand “DRIVE™” and showcasing digital cockpit solutions with multi‑laminated flexible OLED screens and L‑shaped panels for enhanced vehicle interfaces.

• In 2024 and 2025, LG Display achieved mass production of industry‑leading flexible OLED panels using plastic substrates and film‑type encapsulation technology, producing some of the thinnest flexible panels (~0.44 mm) for smartphone applications and enabling new design innovations. (LG Display)

The scope of the Flexible OLED Market Report encompasses a multi‑faceted analysis of display technologies built on flexible organic light‑emitting diode platforms, covering product types such as foldable, rollable, and stretchable panels designed for a wide spectrum of applications. This includes consumer electronics (smartphones, tablets, wearables), automotive interiors (dashboards, curved infotainment screens), healthcare devices (wearable health monitors), industrial displays (control panels), and emerging form factors like near‑eye AR displays. The report segments the market by key technologies, manufacturing processes, and material innovations, such as advanced encapsulation techniques and plastic‑substrate AMOLEDs that enable enhanced durability and design freedom.

Geographically, the report assesses major regional markets including Asia Pacific, North America, Europe, South America, and Middle East & Africa, with detailed insights on production hubs, consumption patterns, regulatory trends, and infrastructure readiness. Technological focus areas include LTPO backplane integration for power efficiency, roll‑to‑roll production scaling for volume output, and hybrid display systems combining flexible OLED with other advanced technologies. Industry focus encompasses competitive dynamics, strategic partnerships, product launches, and innovation trends influencing adoption across sectors. Niche segments such as flexible OLED in digital signage, AR/VR near‑eye systems, and automotive digital cockpits are explored, providing decision‑makers with actionable data on capabilities, deployment scenarios, and future trajectories in the flexible OLED landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

22.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Samsung Display, LG Display, BOE Technology Group, Visionox, Japan Display Inc., EverDisplay Optronics, Royole Corporation, Tianma Microelectronics, AU Optronics, EDO Display |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |