Reports

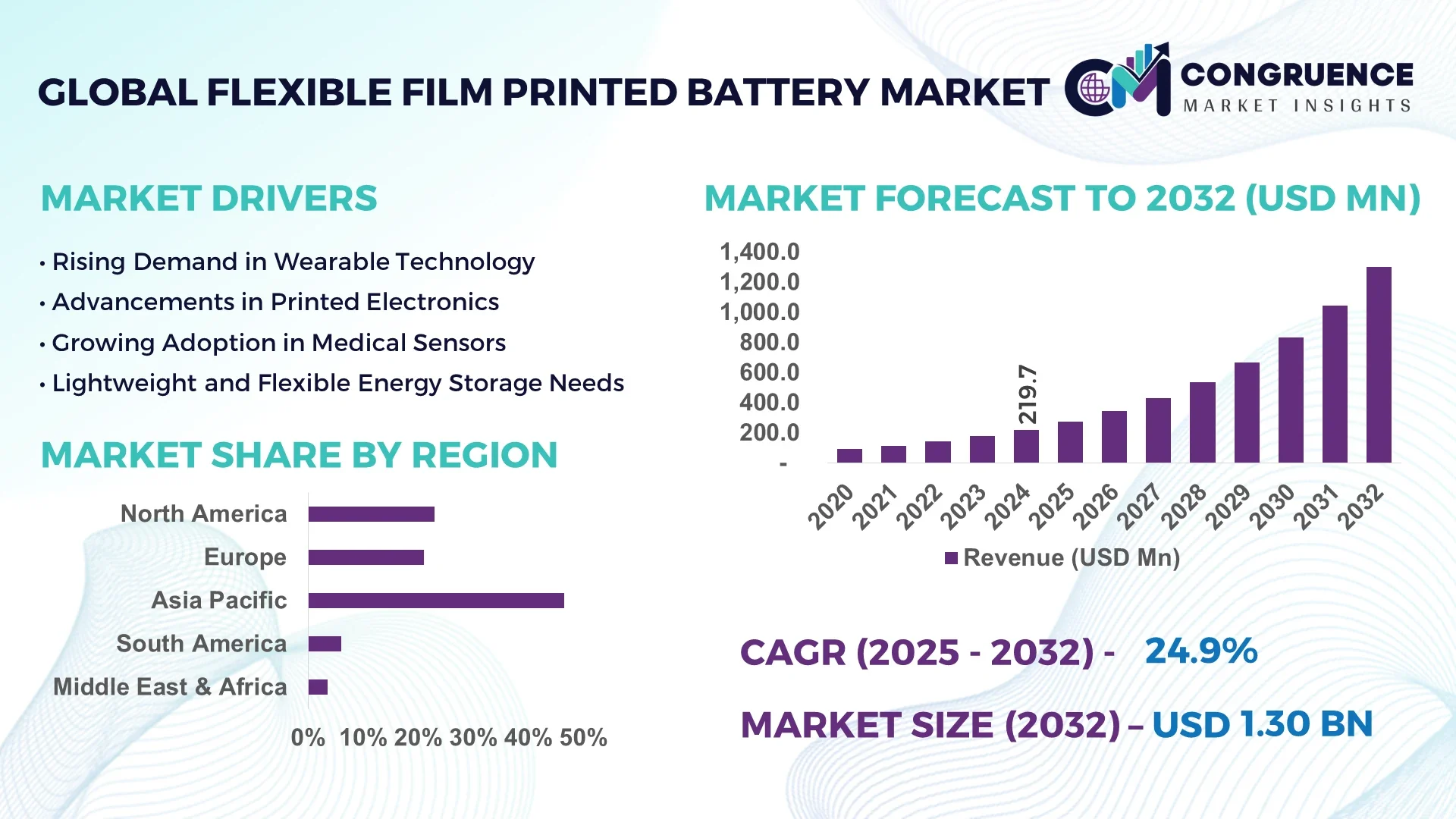

The Global Flexible Film Printed Battery Market was valued at USD 219.7 Million in 2024 and is anticipated to reach a value of USD 1,301.2 Million by 2032 expanding at a CAGR of 24.9% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

China currently dominates the flexible film printed battery market, leveraging its robust electronics manufacturing ecosystem. With over 60% of global production capacity, Chinese firms lead in innovations for wearable electronics, smart packaging, and medical sensors. Aggressive investment in R&D and mass-scale roll-to-roll printing facilities allows faster commercialization of ultra-thin and high efficiency printed battery solutions tailored to consumer electronics.

Global demand for flexible film printed batteries is accelerating across multiple sectors. The wearables market is driving demand for ultra-lightweight, bendable power sources, integrating printed batteries into fitness bands, smart watches, and e-textiles. In the medical domain, flexible batteries are embedded into disposable health patches and diagnostic sensors for minimally invasive monitoring. The IoT revolution also sees sensors powered by printed batteries built directly into packaging and smart labels, offering unprecedented form-factor flexibility. Innovations in conductive inks, solid polymer electrolytes, and roll-to-roll production are reducing overall device cost while enhancing safety, recyclability, and customized form factors.

Artificial Intelligence (AI) is reshaping the flexible film printed battery market through advanced process control, predictive diagnostics, and material optimization. In manufacturing, machine learning algorithms analyze real-time sensor data from roll-to-roll printing lines to detect anomalies and optimize printing temperature, extrusion rates, and curing times. This minimizes defects such as delamination or micro-voids, improving production yield by up to 15%, while ensuring consistency across large-area substrates.

In design and material science, AI-driven simulations guide the development of new conductive polymer formulations that balance flexibility with high ionic conductivity. Genetic algorithms generate novel polymer structures, expediting lab-scale synthesis by orders of magnitude. Additionally, predictive analytics applied to large performance datasets enables battery engineers to forecast end-of-life behavior under various bending cycles, temperature ranges, and discharge loads—leading to designs that last 10–20% longer in wearable devices.

AI also plays a key role in quality assurance. Computer vision systems, powered by deep learning, scan each printed battery for microscopic faults—cracks, uneven layer thickness, or ink depletion. These systems identify up to 98% of defects inline, allowing for real-time rejection and remediation, reducing scrap rates significantly.

In supply chain and application engineering, AI models predict performance under custom form factors. For example, when integrating batteries into curved surfaces like flexible displays or smart labels, AI solvers optimize layer composition and printing paths to maximize energy density without compromising flexibility. They also forecast battery health metrics for end-user alert systems in medical patches, allowing seamless energy management across an entire device life-cycle.

By embedding smart analytics in every phase—from molecular formulation to end-use diagnostics—AI accelerates innovation and commercialization in flexible film printed batteries, unlocking new applications in wearables, healthcare, and IoT ecosystems.

“An AI model tapped into how zinc ions interact with water under varying salt concentrations, revealing why high salt levels maximize battery performance,” demonstrating that AI-augmented analysis can pinpoint electrolyte optimization strategies to improve ion conduction and extend cycle life.

Fitness trackers, smart patches, and connected sensors need ultra-thin, flexible power packs. In 2024, over 500 million wearable devices shipped—with ~65% integrating printed or flexible batteries. OEMs are now specifying battery thickness under 200 µm and weight below 0.5 g, leading battery developers to refine high-conductivity formulations and test bending endurance to 10,000 cycles.

Printed batteries currently offer 10–30 Wh/L, well below traditional lithium-ion cells (150–250 Wh/L). This energy gap restricts their use in high-load applications or large devices. To compensate, manufacturers must oversize cells or hybridize with rigid modules, hampering flexibility benefits and increasing system complexity.

Printed batteries can be fully integrated into labels, sensors, and patches used across logistics, diagnostics, and point-of-care medical tests. The active pharmaceutical packaging sector is expected to deploy over 2 billion sensor-enabled labels by 2027; printed batteries could power each embedment without external modules, enabling secure tamper alerts, NFC communication, and prolonged shelf monitoring during transport or storage.

Transitioning from prototype to continuous manufacturing involves precise control of ink rheology, substrate tension, curing ovens, and multilayer registration. Yield losses due to layer misalignment or defective electrolytes can exceed 20% in pilot runs. Manufacturers must invest in inline QC systems and robust process control, raising capex and delaying breakeven timelines.

Embedded Energy in Textiles and Packaging: Manufacturers are embedding printed batteries directly into fabrics, tags, and labels using seamless roll-to-roll processes. In 2024, a major sports apparel brand integrated printed batteries into workout shirts to power biometric sensors, enabling performance tracking without external modules. This integration enhances wearability and user comfort while providing continuous energy support.

Multifunctional Hybrid Devices: The convergence of printed sensors, antennas, and flexible circuitry with batteries is creating multifunctional devices like smart patches. In Europe, over 250,000 medical biosensor patches using integrated printed batteries were trialed in 2024, showcasing real-time connectivity, disposable use, and patient comfort. This holistic integration trend opens new markets for self-contained, flexible energy modules.

Biodegradable and Eco-friendly Materials: As sustainability becomes critical, printed battery developers are shifting to biodegradable substrates and non-toxic inks. In Asia, pilot lines now incorporate water-based carbon inks and cellulose films to produce batteries that degrade in soil without leaching harmful chemicals. This aligns with circular economy demands and unlocks applications in food packaging and environmental monitoring.

Custom Shape Printing and 3D Integration: Advances in shape-adaptive electrodes and 3D-printable battery pastes are enabling power sources molded for unique device architectures. Consumer product companies in 2025 showcased concept devices with batteries conforming to curved displays and e-textiles. This trend demonstrates how customizable form factors allow designers greater freedom without increasing bulk or compromising performance.

The Flexible Film Printed Battery Market demonstrates dynamic segmentation across specific types, applications, and end-user categories. Each segment reflects evolving industry needs, from ultra-thin power sources for wearables to disposable energy solutions in smart packaging and healthcare. Among types, Thin Film Batteries lead, while Printed Batteries show the fastest growth due to scalable production advantages. Applications are diversifying—Wearable Devices dominate, but Smart Packaging is experiencing the fastest adoption. In terms of end-users, Healthcare remains the largest segment; meanwhile, Retail & Packaging is growing most rapidly. This segmentation highlights how flexible form factors and environmental sustainability advantages are unlocking new opportunities across industries.

The Flexible Film Printed Battery Market is segmented into Thin Film Batteries and Printed Batteries. Thin Film Batteries accounted for more than 60% of total market revenue in 2024. Their stronghold results from proven performance in medical devices, wearables, and consumer electronics. They offer high energy density and reliability while maintaining flexibility and thinness, making them suitable for applications requiring extended battery life and robust performance.

Printed Batteries are the fastest growing segment, projected to expand by over 30% annually through 2032. This growth is fueled by demand in disposable and low-cost applications, such as smart packaging, RFID/NFC tags, and interactive labels. The ability to print batteries on flexible substrates at scale and the use of sustainable materials offer a significant cost advantage. Ongoing improvements in printed battery performance, such as higher cycle life and better energy output, are helping this segment close the gap with thin film batteries, positioning it as a critical enabler for IoT and mass-market applications.

Key application segments include Wearable Devices, Medical Devices, Smart Packaging, Consumer Electronics, and Others. Wearable Devices led the market in 2024, accounting for approximately 45% of global revenue. The rise in fitness bands, smartwatches, and biometric patches drives this leadership position. OEMs in this space demand ultra-thin batteries that can endure frequent flexing, support high cycle life, and maintain safety during prolonged skin contact.

Smart Packaging is the fastest growing application segment, with projected growth exceeding 35% annually. Brands in retail, pharmaceuticals, and logistics are embedding flexible batteries into packaging for smart labels, temperature sensors, and interactive consumer engagement via NFC. The ability to integrate batteries seamlessly within packaging structures, without compromising design or sustainability goals, is accelerating adoption. Meanwhile, Medical Devices and Consumer Electronics maintain steady demand as flexible batteries enable new form factors in diagnostic patches, drug-delivery systems, foldable phones, and flexible displays.

The primary end-user segments include Healthcare, Consumer Electronics, Retail & Packaging, Logistics & Transportation, and Others. In 2024, Healthcare dominated the market, contributing about 40% of total revenue. This leadership stems from the increasing use of flexible batteries in biosensors, wearable health monitors, and disposable medical patches. Healthcare OEMs value flexible batteries’ safety, skin compatibility, and compliance with strict medical standards.

Retail & Packaging represents the fastest growing end-user segment, forecast to grow at more than 38% annually. As brands seek to differentiate products and add interactive functionality, demand for battery-powered smart packaging is surging. Applications include freshness indicators, tamper-evident labels, and NFC-powered consumer engagement tools. Consumer Electronics remains a robust segment, where foldable devices, flexible displays, and smart textiles drive battery innovation. Logistics and transportation sectors are increasingly adopting flexible batteries for shipment tracking and cold chain monitoring, further diversifying market demand.

Asia-Pacific accounted for the largest market share at 46.5% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 27.4% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

The dominance of Asia-Pacific is driven by large-scale manufacturing hubs in China, Japan, and South Korea, coupled with aggressive government incentives for flexible electronics. Meanwhile, North America’s fast growth is propelled by strong demand from medical device manufacturers and a rapidly expanding smart packaging market. Europe maintains a well-established presence in high-quality printed batteries for medical and consumer applications, while South America and the Middle East & Africa are emerging markets, primarily driven by demand for smart packaging and logistics solutions.

North America is witnessing robust demand for flexible film printed batteries in wearable healthcare devices. The region recorded sales of over 85 million wearable patches and medical monitoring devices powered by flexible batteries in 2024. The U.S. leads regional growth due to strong investment in digital healthcare and rising consumer demand for remote monitoring devices. In Canada, demand for smart labels in pharmaceutical packaging is also driving adoption. Local manufacturers are increasingly focusing on printed battery solutions optimized for skin-contact safety and biocompatibility. Additionally, collaborations between medical OEMs and battery innovators are pushing advancements in ultra-thin and high-reliability battery formats.

Europe’s market is driven by strong regulatory support for sustainable packaging and a growing smart packaging ecosystem. Over 450 million printed smart labels integrated with flexible batteries were deployed across the European FMCG sector in 2024. Germany, France, and the U.K. are at the forefront of this trend, with leading retailers adopting battery-powered NFC tags and anti-counterfeiting labels. Additionally, Europe’s focus on biodegradable and recyclable battery materials is fostering innovation in green battery solutions. The medical device sector also contributes significantly, particularly in wearable health patches and in-home patient monitoring solutions that comply with stringent EU medical standards.

Asia-Pacific remains the dominant force in the flexible film printed battery market, accounting for over 46.5% of global revenue. China leads in production scale, with local companies supplying more than 65% of printed batteries used globally. Japan and South Korea contribute through high-end innovations, particularly in conductive inks and thin film battery technologies for foldable electronics. The region benefits from vertical integration, with materials, printing equipment, and battery assembly capabilities co-located in manufacturing hubs. In 2024, over 600 million smart packaging units and 200 million wearable devices in Asia-Pacific incorporated flexible printed batteries, showcasing the region’s leadership in both volume and innovation.

South America’s flexible film printed battery market is emerging, with Brazil and Argentina driving regional adoption. In 2024, over 100 million smart labels and printed sensor tags were deployed in Brazil’s logistics and cold chain sectors, supporting agricultural exports and pharmaceutical shipments. The retail industry is also adopting interactive packaging powered by printed batteries to enhance customer engagement. Limited local manufacturing capacity currently leads to high import reliance; however, investments in roll-to-roll printing facilities are underway in key markets. The growth of e-commerce logistics and demand for product traceability are expected to fuel continued expansion in the region.

The Middle East & Africa market is seeing increasing demand for flexible film printed batteries in smart logistics and security tags. In 2024, more than 60 million battery-powered tracking and anti-theft tags were used across major logistics hubs in the UAE and South Africa. The region’s growing cold chain industry for pharmaceuticals and perishables is driving adoption of printed battery-powered environmental sensors. In addition, the luxury goods sector in the Gulf states is adopting battery-powered anti-counterfeit labels for high-value consumer products. Investments in local R&D centers and partnerships with European and Asian manufacturers are helping to localize supply chains and reduce dependency on imports.

China - holds the highest market share globally, contributing approximately 39.5% of total revenue in 2024 due to its unparalleled scale of manufacturing and vertical integration.

United States - ranks second, contributing around 18.7%, driven by advanced healthcare applications and strong demand for smart packaging and wearable devices.

The flexible film printed battery market features a mix of specialized firms, electronics giants, and innovative startups. Competition is intense, driven by technological differentiation, scale of production, IP portfolios, and partnerships. Large manufacturers focus on vertical integration—controlling conductive ink formulation, substrate sourcing, printer fabrication, and battery roll-out—to ensure consistency and rapid scaling. Their aim is to reduce unit costs and engage in co-development with OEMs for wearables and medical devices.

Meanwhile, agile startups invest heavily in R&D, rapidly prototyping novel materials such as biodegradable polymer electrolytes and shape-shifting fluid electrodes. Competitive edge hinges on securing niche IP, especially for solid-state and zinc-based printed chemistries. Global players form partnerships and alliances: equipment vendors supplying roll-to-roll systems collaborate with ink formulators and medical OEMs for co-branded product launches.

Cost reduction and sustainability are key differentiators. Companies offering recyclable or biodegradable battery layers outperform those using conventional PET and metal electrodes. As major electronics and packaging OEMs require certifications (e.g., ISO 13485, IEC 62133), manufacturers with dedicated compliance programs gain market access. The entry barrier for new players is rising due to high upfront investments in pilot lines and QC infrastructure, but industry-wide consortiums are emerging to share best practices. Overall, the landscape is defined by rapid innovation, strategic alliances, and vertical scale.

Blue Spark Technologies

Printed Energy

Thinfilm Electronics ASA

Enfucell

Cymbet Corporation

TDK Corporation

Planar Energy Devices, Inc.

Nippon Chemi-Con Corporation

IMEC

PragmatIC Semiconductor

Technology in this market spans printed zinc-polymer systems, thin-film solid-state lithium, biodegradable electrolytes, and shape-conforming fluid electrodes. Each technology addresses specific performance and application needs.

Printed Zinc-Polymer & Carbon Inks: Relying on zinc-carbon chemistry, these systems power disposable smart labels and biosensor patches. Manufacturers report areal capacities up to 54 mAh/cm² in printed AgO–Zn prototypes, with flexible substrates supporting thousands of bend cycles.

Thin‑Film Solid‑State Lithium: These offer rechargeable capabilities for wearables and e‑textiles. Using printed stainless-steel substrates and solid electrolytes, units achieve higher volumetric energy and longer cycle life, appealing to medical device OEMs emphasizing durability.

Fluid or Shape‑Shifting Electrodes: The newest frontier uses conductive polymers and lignin‑based fluid inks that can be molded or 3D‑printed into any shape—ideal for soft robotics and dynamic wearable devices.

Stretchable Lithium‑Ion Designs: Development includes fully elastic components capable of expanding by up to 5000% without losing charge capacity over multiple cycles — a breakthrough for true flexible electronics integration on skin or fabrics.

Supporting all technologies are roll-to-roll printers capable of sub‑micron registration, inline QC, and lamination, enabling scalable production. Research also explores biodegradable cellulose substrates and conductive graphene/carbon nanotube networks, aiming to balance flexibility, sustainability, and cost. These innovations collectively expand both performance and application access for next-gen printed battery systems.

In April 2025, Linköping University researchers unveiled a shape‑shifting fluid battery with toothpaste‑like consistency, allowing molding into arbitrary forms using sustainable lignin-based conductive polymers—paving the way for customizable power in soft electronics.

In July 2024, a fully stretchable lithium‑ion battery using elastic polymer electrolyte expanded up to 5000% strain and retained charge through nearly 70 cycles, signaling viable stretchable energy storage for wearable health monitors.

In June 2024, Tsinghua University introduced a safer, lower‑cost flexible battery for wearable tech featuring a self‑healing mechanism and improved mechanical reliability tailored for skin‑contact devices.

In May 2025, researchers published the fluid electrode shape‑shifting battery in a leading scientific journal, emphasizing the role of lignin and conductive polymers to enable eco‑friendly and form‑adaptive energy solutions for wearable and textile integration.

This report offers a comprehensive outlook on the flexible film printed battery sector, covering market performance, material innovations, technology ecosystems, value chain analysis, infrastructure investment, and regulatory frameworks. It details segmentation by chemistry (zinc‑polymer, lithium solid-state, fluid electrodes), format (primary vs. rechargeable), and voltage classes (below 1.5 V to above 3 V). Performance indicators such as energy density, mechanical endurance (bend lifespan), reel length/yield, and recyclability criteria are benchmarked across segments.

The scope also examines application verticals—from disposable smart packaging and NFC tags to medical patches and smart textiles—highlighting implementation drivers like skin compatibility, regulatory compliance, integration feasibility, and UX design considerations. Geographically, it spans maturity (Japan/Korea), scale (China, U.S.), and emerging demand (Brazil, UAE).

Additionally, strategic insight is provided through competitive profiling of major players and technology trend spotting for future sectors such as fluid electrodes and stretchable cells. The report also assesses global regulatory landscapes (FDA, RoHS, ISO), supply chain resilience, cost evolution, and environmental impact—all packaged into actionable insights for companies seeking to expand or innovate in this fast‑evolving technology domain.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Flexible Film Printed Battery Market |

| Market Revenue (2024) | USD 219.7 Million |

| Market Revenue (2032) | USD 1,301.2 Million |

| CAGR (2025–2032) | 24.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Blue Spark Technologies, Printed Energy, Thinfilm Electronics ASA, Enfucell, Cymbet Corporation, TDK Corporation, Planar Energy Devices, Inc., Nippon Chemi-Con Corporation, IMEC, PragmatIC Semiconductor |

| Customization & Pricing | Available on Request (10% Customization is Free) |