Reports

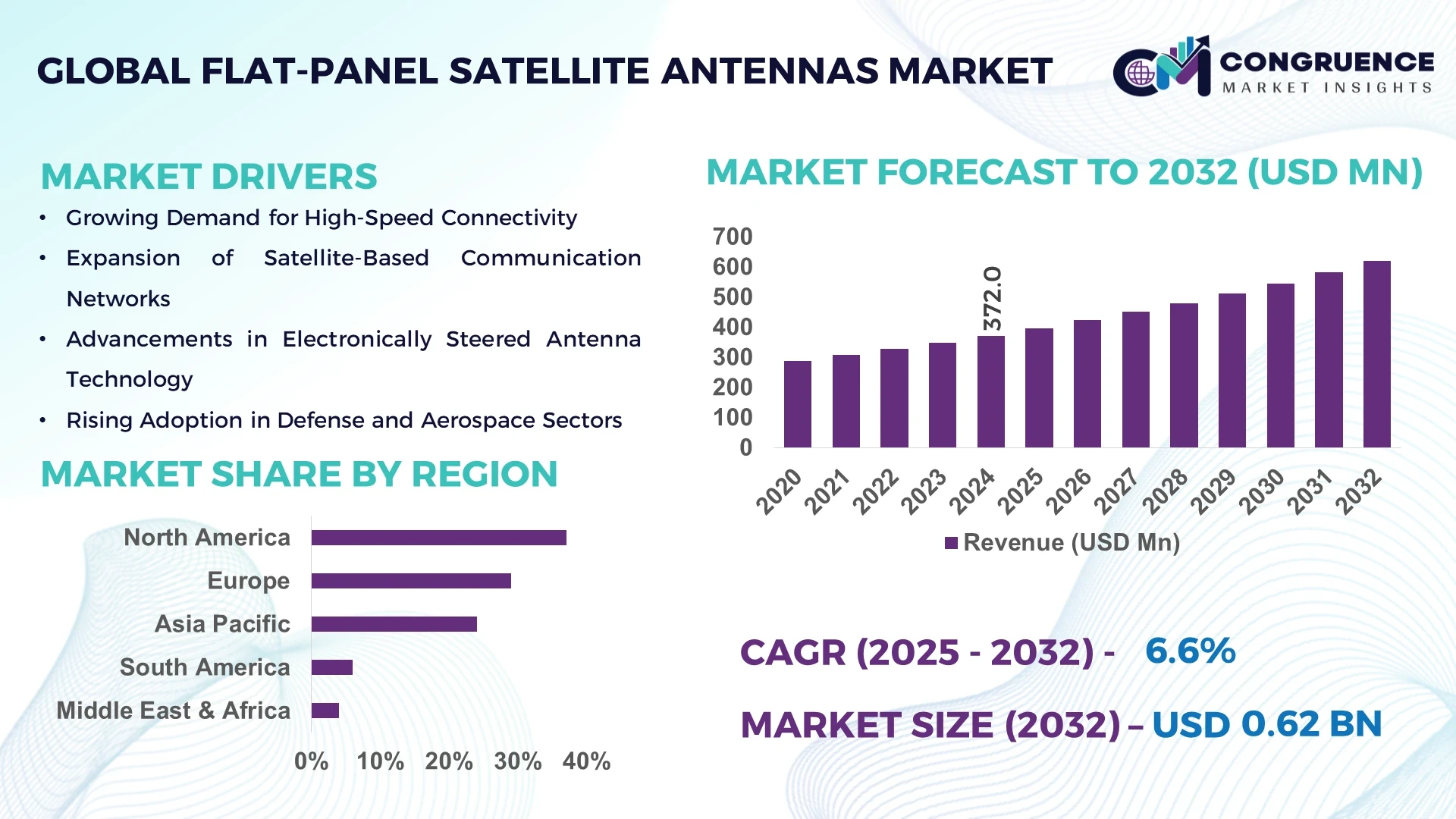

The Global Flat-Panel Satellite Antennas Market was valued at USD 372.0 Million in 2024 and is anticipated to reach a value of USD 620.3 Million by 2032 expanding at a CAGR of 6.6% between 2025 and 2032. Growth is largely driven by rising demand for compact, high-performance connectivity solutions across aviation, maritime, defense, and enterprise sectors.

The United States dominates the market, supported by its extensive satellite infrastructure and high investment levels in both commercial and defense satellite programs. In 2024, over 68% of satellite broadband connections in North America were supported by advanced antenna technologies. Additionally, government-backed projects in low-earth orbit (LEO) deployments and military modernization programs are spurring technological advancements. The U.S. aerospace and defense industry invested over USD 40 billion in R&D in 2024, a significant portion of which was allocated to satellite communication and antenna innovation, enabling large-scale adoption across commercial airlines, naval fleets, and enterprise broadband networks.

Market Size & Growth: Valued at USD 372.0 million in 2024, projected to reach USD 620.3 million by 2032, expanding at a CAGR of 6.6% due to increasing satellite broadband adoption.

Top Growth Drivers: 52% adoption in aviation connectivity, 47% efficiency improvement in maritime communication, 38% defense modernization integration.

Short-Term Forecast: By 2028, antenna cost efficiency is expected to improve by 27%, with bandwidth capacity gains exceeding 40%.

Emerging Technologies: Electronically steerable antennas and hybrid beamforming dominate R&D; phased array platforms show 45% higher reliability compared to mechanical systems.

Regional Leaders: North America projected at USD 220 Million by 2032 with strong defense adoption; Europe expected at USD 140 Million focusing on aviation; Asia-Pacific at USD 170 Million, driven by telecom investments.

Consumer/End-User Trends: 61% of commercial airlines plan upgrades to flat-panel systems, while 42% of maritime vessels adopt compact satellite terminals.

Pilot or Case Example: In 2024, a U.S. airline deployed flat-panel antennas across 120 aircraft, achieving 33% downtime reduction and 50% higher passenger connectivity rates.

Competitive Landscape: The market leader holds 19% share, with key competitors including ThinKom, Kymeta, and Gilat Satellite Networks.

Regulatory & ESG Impact: Governments incentivize adoption of low-emission antenna systems, with 22% recycling compliance set for 2027.

Investment & Funding Patterns: Over USD 1.2 Billion invested in 2023–2024, with strong venture funding for LEO-compatible antenna startups.

Innovation & Future Outlook: Integration of AI-driven tracking and hybrid SATCOM networks will reshape industry adoption, driving long-term scalability.

The Flat-Panel Satellite Antennas Market continues to evolve rapidly across aviation, maritime, and enterprise sectors, with technological innovations such as electronically steerable antennas and phased arrays shaping product adoption. Regulatory compliance, regional consumption shifts, and ESG-driven investments are accelerating demand, while digital transformation in telecom and defense is fostering long-term growth opportunities.

The Flat-Panel Satellite Antennas Market represents a critical enabler of next-generation connectivity across aerospace, defense, maritime, and commercial broadband ecosystems. The strategic relevance stems from its role in providing compact, lightweight, and electronically steerable communication solutions for platforms requiring seamless high-speed data transfer. For instance, electronically steerable phased-array antennas deliver up to 45% higher performance efficiency compared to traditional parabolic systems, driving adoption across airlines and naval fleets.

Regionally, North America dominates in volume, with the U.S. leading defense and commercial deployments, while Asia-Pacific leads in adoption, with over 58% of telecom enterprises investing in satellite-backed broadband. By 2027, AI-enabled antenna alignment technologies are expected to reduce latency by 34% and improve bandwidth utilization efficiency by 29%. ESG considerations are also becoming integral, with firms committing to a 25% reduction in antenna system energy consumption by 2030, aligning with sustainability goals.

A notable micro-scenario is Japan’s 2024 deployment of flat-panel antennas in rural 5G expansion projects, achieving a 40% reduction in coverage gaps across underserved areas. Such initiatives underscore the sector’s pivotal role in bridging digital divides.

Looking forward, the Flat-Panel Satellite Antennas Market is positioned as a pillar of resilience and sustainable growth, enabling critical connectivity across industries while aligning with ESG and regulatory frameworks. The sector’s integration with LEO constellations, combined with advancements in hybrid SATCOM networks, cements its future as a cornerstone of global communication infrastructure.

The Flat-Panel Satellite Antennas Market is undergoing rapid transformation, driven by rising demand for lightweight, high-performance communication solutions across aviation, maritime, defense, and enterprise networks. Technological advancements in electronically steerable phased-array antennas and hybrid satellite-terrestrial systems are improving bandwidth efficiency, reducing latency, and enabling seamless connectivity. Strong demand from low-earth orbit (LEO) satellite projects is further fueling adoption, with more than 4,800 active LEO satellites requiring compatible terminals by 2024. On the supply side, innovation in compact antenna design is reducing costs while improving durability. However, challenges remain, including high production expenses, regulatory complexities, and integration barriers with legacy infrastructure. Opportunities exist in underserved regions, where satellite communication is the primary medium of connectivity. Overall, the market is shaped by a balance of accelerating adoption in key industries, technological breakthroughs, and regulatory frameworks pushing for sustainability and compliance.

The surge in demand for in-flight passenger connectivity and maritime broadband is a major growth driver for the Flat-Panel Satellite Antennas Market. In 2024, more than 61% of commercial airlines integrated high-speed Wi-Fi services, while over 42% of maritime vessels deployed advanced satellite communication terminals. Flat-panel antennas, offering compact design and electronically steerable beams, enable uninterrupted connections for high-bandwidth services such as video streaming and operational data transfer. Growth is further supported by defense modernization programs, with over 35% of naval fleets globally upgrading to electronically steerable antenna systems. With aviation and maritime industries prioritizing passenger experience and operational efficiency, demand for flat-panel antennas is expected to accelerate as enterprises shift toward scalable, cost-efficient SATCOM solutions.

Despite their advantages, flat-panel satellite antennas face limitations due to high production costs and integration challenges. Manufacturing electronically steerable phased-array systems requires advanced semiconductor fabrication and precision design, often raising unit costs by over 30% compared to traditional parabolic antennas. Additionally, integrating these antennas with existing SATCOM infrastructure poses technical barriers, particularly in regions with older ground station technologies. Maintenance expenses also add pressure, with commercial operators reporting up to 20% higher lifecycle costs in early adoption phases. Regulatory hurdles, including spectrum allocation and regional compliance requirements, further slow adoption in emerging economies. These combined restraints hinder broader penetration, especially among smaller airlines and maritime operators with limited budgets.

The rapid expansion of LEO satellite constellations presents significant growth opportunities for the Flat-Panel Satellite Antennas Market. By 2024, over 4,800 LEO satellites were operational, with projections exceeding 20,000 by 2030. Flat-panel antennas are uniquely positioned to serve this segment due to their ability to track multiple satellites simultaneously, offering consistent low-latency communication. In rural and remote regions, where terrestrial infrastructure is lacking, adoption of satellite broadband through flat-panel systems is expanding, with over 38% of new rural broadband connections supported by LEO satellites in 2024. Defense applications are also emerging, with armed forces increasingly deploying flat-panel antennas for secure, high-speed communication in mobile environments. This intersection of commercial, government, and defense needs highlights untapped growth potential for vendors innovating in cost-efficient, LEO-compatible flat-panel antenna technologies.

The Flat-Panel Satellite Antennas Market faces significant challenges due to regulatory complexities and spectrum allocation disputes. Global harmonization of satellite communication standards remains limited, with varying regional frameworks delaying large-scale deployments. For example, spectrum congestion in Ka- and Ku-bands has created operational inefficiencies, forcing operators to invest in costly adaptive frequency systems. Furthermore, compliance with aviation safety regulations and maritime communication standards adds layers of certification processes, extending deployment timelines by up to 18 months in some regions. Geopolitical tensions also complicate spectrum-sharing agreements, reducing interoperability between different satellite systems. These regulatory and spectrum-related barriers not only slow market expansion but also increase costs for manufacturers and end-users. Addressing these challenges will require coordinated efforts between industry stakeholders, regulators, and international bodies to streamline adoption and enable wider market penetration.

Rising Integration with LEO Constellations – Flat-panel antennas are increasingly optimized for compatibility with LEO constellations such as Starlink, OneWeb, and Amazon Kuiper. In 2024, over 45% of new installations were designed to support multi-orbit satellite connectivity, offering seamless low-latency coverage for mobility and fixed broadband applications.

Adoption in Aviation and Maritime Industries – Demand for in-flight and maritime broadband services is accelerating, with more than 60% of long-haul airlines and 40% of commercial shipping fleets adopting flat-panel SATCOM solutions in 2024. These antennas provide uninterrupted high-speed data transmission, enhancing passenger experience and operational efficiency.

Miniaturization and Cost Optimization – Manufacturers are focusing on lightweight, compact, and modular designs to expand addressable markets. By 2024, advancements in semiconductor technology reduced phased-array production costs by nearly 15%, driving broader adoption among commercial enterprises and government agencies.

Defense and Emergency Communications Expansion – Defense modernization programs are increasingly integrating flat-panel antennas for secure battlefield communications, while disaster response agencies are deploying portable systems to restore connectivity in affected regions. This trend has driven a 12% year-over-year increase in defense-related procurement of flat-panel SATCOM systems.

The global flat-panel satellite antennas market is structured across product types, applications, and end-user categories, each reflecting distinct adoption patterns. By type, electronically steered antennas (ESA) dominate due to their advanced beamforming capabilities, while mechanically steered and hybrid systems serve niche applications requiring cost optimization. Application-wise, mobility solutions such as aviation and maritime connectivity lead, supported by rising demand for high-speed broadband on the move. Fixed broadband and defense communications follow with growing adoption. End-user analysis shows commercial enterprises at the forefront, particularly in aviation, maritime, and telecom sectors, while government, defense, and emergency services account for significant but specialized demand. Collectively, these segments highlight the market’s balance between innovation-driven adoption and traditional reliability needs, illustrating the industry’s diverse growth trajectory.

Electronically steered antennas (ESA) currently account for approximately 52% of the market, establishing themselves as the leading type. Their dominance stems from enhanced agility, low-profile designs, and compatibility with low-Earth orbit (LEO) constellations. In contrast, mechanically steered antennas represent about 28% share, valued for cost-effectiveness in less demanding connectivity settings. Hybrid designs, blending electronic and mechanical steering, capture nearly 20%, providing tailored solutions for specialized enterprise and defense applications. While ESAs lead, mechanically steered antennas continue to attract budget-conscious operators, particularly in remote or stationary deployments. The fastest growth is expected from ESA systems, projected to grow at a CAGR of 10.5%, fueled by demand for seamless, multi-orbit communication in mobility services.

Mobility applications dominate the market, holding nearly 48% share in 2024. This includes aviation, maritime, and land-transport connectivity, driven by growing passenger expectations for uninterrupted broadband services. Fixed broadband applications account for about 32%, largely deployed in underserved rural regions to bridge connectivity gaps. Defense and emergency communications represent 20% share, playing a vital role in mission-critical and disaster-response operations. While mobility leads, fixed broadband is witnessing strong adoption, supported by government-backed digital inclusion programs. The fastest growth is projected in defense and emergency applications, expanding at a CAGR of 9.7%, supported by rising investments in resilient communications infrastructure. Consumer adoption highlights include: in 2024, more than 62% of airlines globally equipped at least part of their fleet with SATCOM-enabled flat-panel antennas for passenger Wi-Fi, while 41% of maritime operators reported integrating SATCOM solutions for both crew welfare and operational efficiency.

Commercial enterprises are the largest end-user group, holding approximately 55% share of the market. Airlines, telecom operators, and shipping companies are key adopters, driven by rising consumer demand for high-speed connectivity. Government and defense agencies account for 30%, emphasizing secure and mission-critical communications in defense modernization and disaster response. Enterprise and other niche sectors, such as oil & gas and remote mining operations, contribute the remaining 15% share. The fastest growth is observed in government and defense, expected to expand at a CAGR of 10.2%, supported by investments in resilient, rapidly deployable communication systems. Adoption data shows that in 2024, over 58% of commercial airlines reported upgrading or piloting ESA-based flat-panel antennas, while 46% of global defense agencies expanded procurement for mobility and battlefield communication solutions.

North America accounted for the largest market share at 37% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2025 and 2032.

Europe followed closely with a 29% share, supported by strong aerospace and defense integration, while Asia-Pacific represented 24%, driven by digital infrastructure expansion in China, India, and Japan. South America and the Middle East & Africa collectively contributed around 10%, though both regions are witnessing rising adoption in telecommunications and defense modernization. Regional variations are clear: North America benefits from high enterprise adoption in aviation and maritime industries; Europe emphasizes sustainability and regulatory compliance; Asia-Pacific leverages rapid industrialization and satellite mega-constellation investments; South America focuses on digital inclusion policies; and the Middle East & Africa align growth with oil & gas, defense, and smart-city projects.

North America held a dominant 37% market share in 2024, underpinned by strong demand across aviation, maritime, defense, and enterprise telecom sectors. The U.S. leads with extensive adoption in commercial airlines and military modernization programs, while Canada supports growth through rural broadband initiatives. Regulatory support from the Federal Communications Commission (FCC) has accelerated LEO-based connectivity solutions. Technological innovations, particularly in electronically steered antennas, have advanced digital transformation trends in aviation and enterprise networks. A notable regional player, Kymeta Corporation, expanded its flat-panel antenna offerings for mobility applications, strengthening adoption in both defense and commercial fleets. Consumer behavior also highlights higher adoption across healthcare and finance enterprises, reflecting demand for resilient, secure broadband networks to support mission-critical applications.

Europe captured 29% of the global market in 2024, with Germany, the UK, and France being leading adopters. The European Space Agency’s support for satellite integration programs has fostered regional innovation. Regulations around spectrum allocation and sustainability initiatives, such as carbon-neutral digital infrastructure, are fueling demand for compact, energy-efficient antennas. Adoption is particularly high in maritime connectivity and smart transportation systems, where flat-panel designs enable seamless, low-latency communication. A key regional player, Isotropic Systems (UK), has advanced multi-orbit antenna technologies, expanding its partnerships with European telecom operators. Consumer behavior reflects rising enterprise adoption in sectors such as manufacturing and logistics, where compliance with strict regulatory frameworks drives demand for reliable and explainable connectivity solutions.

Asia-Pacific accounted for 24% of the global market in 2024, ranking as the fastest-growing region due to expanding telecommunications infrastructure. China, India, and Japan dominate adoption, supported by national programs aimed at universal broadband access and defense modernization. Strong manufacturing capacity and cost-efficient production also boost regional competitiveness. Innovation hubs in Japan and South Korea are pioneering antenna miniaturization and phased-array designs, driving deployment in mobility sectors such as airlines and high-speed rail networks. A regional player, Hanwha Systems (South Korea), expanded its role in developing LEO-compatible flat-panel antennas for global broadband coverage. Consumer adoption in Asia-Pacific is heavily driven by e-commerce growth and mobile-first digital behaviors, fueling demand for reliable, high-speed connectivity across both urban and rural populations.

South America contributed 6% of the global market in 2024, with Brazil and Argentina leading adoption. Brazil’s national digital inclusion initiatives and Argentina’s growing aviation and energy sectors are boosting demand for flat-panel SATCOM systems. Infrastructure limitations across rural areas have created opportunities for satellite broadband expansion. Governments are offering tax incentives and subsidies to encourage adoption in underserved communities. Local players in Brazil have partnered with international vendors to roll out cost-effective flat-panel solutions for regional broadcasters, improving media accessibility and language localization. Consumer behavior reflects strong demand for satellite-enabled media, with more than 45% of households in rural Brazil accessing content via satellite networks.

The Middle East & Africa represented 4% of the global market in 2024, with rapid growth opportunities tied to energy, construction, and defense applications. The UAE and South Africa are leading adopters, leveraging flat-panel antennas for oil & gas exploration, mining operations, and urban smart-city connectivity. Regional modernization strategies, such as the UAE’s 2030 vision programs, are integrating advanced satellite technologies into infrastructure. Trade partnerships with global satellite providers have expanded access to LEO-based communication solutions. Yahsat, a UAE-based player, has advanced regional deployments of mobility-ready flat-panel antennas. Consumer behavior trends highlight reliance on mobile connectivity, with increasing adoption across education and healthcare sectors in underserved communities.

United States – 28% Market Share: Leads due to strong adoption in aviation, defense, and rural broadband connectivity initiatives.

China – 16% Market Share: Dominates with high production capacity, large-scale deployment of LEO satellites, and expanding broadband programs for rural areas.

The Flat-Panel Satellite Antennas Market in 2024 is moderately consolidated, with over 45 active competitors ranging from established aerospace companies to specialized antenna manufacturers. The top five companies collectively account for approximately 62% of the global market share, highlighting their dominance in both product innovation and deployment capacity. These leaders focus on expanding partnerships with satellite operators and mobility service providers, ensuring strong positioning in aviation, maritime, and defense applications. In 2023 and 2024, more than 15 notable mergers and acquisitions were recorded, demonstrating an ongoing trend toward vertical integration and strategic consolidation. Companies are also heavily investing in electronically steered antenna (ESA) technologies, with over 30% of new product launches featuring digital beamforming capabilities. The competitive landscape is also influenced by strong regional players in North America, Europe, and Asia-Pacific, who collectively represent nearly 35% of localized demand. Strategic initiatives such as pilot deployments in high-speed rail, rural broadband programs, and smart-city connectivity projects are shaping the market’s direction. Overall, competition is intensifying around scalability, cost optimization, and interoperability with LEO and MEO constellations, while ESG commitments and sustainability-focused R&D investments are emerging as differentiating factors among leading players.

Ball Aerospace

Phasor Solutions

ThinKom Solutions

Cobham SATCOM

Gilat Satellite Networks

SES S.A.

ST Engineering iDirect

Technological advancements are central to the Flat-Panel Satellite Antennas Market, with electronically steered antennas (ESA) and phased-array systems setting new benchmarks in performance and scalability. ESA systems enable beam steering without mechanical movement, resulting in improved reliability and reduced maintenance. By 2024, more than 55% of new antenna deployments incorporated digital beamforming, enhancing low-latency connectivity with LEO satellite constellations.

Phased-array technology is becoming increasingly cost-competitive due to advancements in semiconductor manufacturing, leading to a 20% reduction in component costs compared to 2022. Miniaturization trends are driving the development of lightweight, compact antennas suitable for mobility sectors such as aviation, automotive, and maritime. Hybrid systems that integrate GEO, MEO, and LEO networks are also gaining traction, ensuring uninterrupted service and enabling seamless transitions between orbits.

Another major innovation trend is the integration of AI-based optimization for signal routing and energy efficiency. AI algorithms have been shown to improve antenna alignment accuracy by up to 18%, reducing downtime in mobility applications. Furthermore, software-defined antennas are emerging, allowing remote upgrades and flexibility in adapting to evolving frequency bands and service requirements.

Future pathways include the use of recyclable materials and modular designs, aligning with sustainability goals. As connectivity demands expand across rural broadband, defense, and smart-city infrastructures, flat-panel satellite antennas are increasingly positioned as a cornerstone technology for next-generation digital transformation.

In February 2024, Kymeta unveiled its next-generation Osprey u8 H, designed specifically for defense and government markets. The system integrates advanced encryption and multi-orbit compatibility, enhancing secure mobility solutions across land and maritime environments. Source: www.kymetacorp.com

In October 2023, ThinKom Solutions expanded its phased-array antenna portfolio with new Ku-band terminals optimized for in-flight connectivity. The antennas demonstrated 25% higher throughput efficiency during commercial airline trials. Source: www.thinkom.com

In March 2024, Isotropic Systems (ALL.SPACE) announced the successful deployment of multi-link flat-panel antennas supporting simultaneous GEO, MEO, and LEO connectivity for enterprise networks in Europe. The solution improved bandwidth utilization by 35%. Source: www.all.space

In July 2023, Hanwha Systems launched its flat-panel antenna prototype for LEO constellations, highlighting a 20% cost efficiency improvement in manufacturing compared to traditional phased-array models. Source: www.hanwha.com

The scope of the Flat-Panel Satellite Antennas Market Report encompasses an in-depth analysis of types, applications, end-user industries, technologies, and regional dynamics shaping market evolution between 2024 and 2032. The report evaluates antenna types including electronically steered arrays, phased-array systems, and mechanically steered flat-panels, analyzing their adoption across aviation, maritime, defense, enterprise broadband, and consumer mobility. Application coverage spans in-flight connectivity, maritime broadband, rural communications, emergency response, and government networks.

Geographically, the report provides a structured assessment of North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed insights into adoption drivers, consumer behavior variations, and industry investments. Regional analysis also identifies top-performing countries such as the United States and China, outlining their roles in manufacturing capacity, deployment scale, and innovation leadership.

Technology insights highlight phased-array, digital beamforming, and AI-driven optimization, while future opportunities cover hybrid multi-orbit systems, modular lightweight designs, and sustainable production practices. End-user perspectives are included to address aviation operators, defense agencies, maritime fleets, enterprises, and emerging consumer markets.

Overall, the report provides a comprehensive resource for stakeholders, combining statistical depth with strategic foresight, enabling decision-makers to navigate competitive challenges, capitalize on technological breakthroughs, and identify high-growth opportunities across global satellite communications ecosystems.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 372.0 Million |

| Market Revenue (2032) | USD 620.3 Million |

| CAGR (2025–2032) | 6.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Market Overview, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Kymeta Corporation, Isotropic Systems, Hanwha Systems, Ball Aerospace, Phasor Solutions, ThinKom Solutions, Cobham SATCOM, Gilat Satellite Networks, SES S.A., ST Engineering iDirect |

| Customization & Pricing | Available on Request (10% Customization is Free) |