Reports

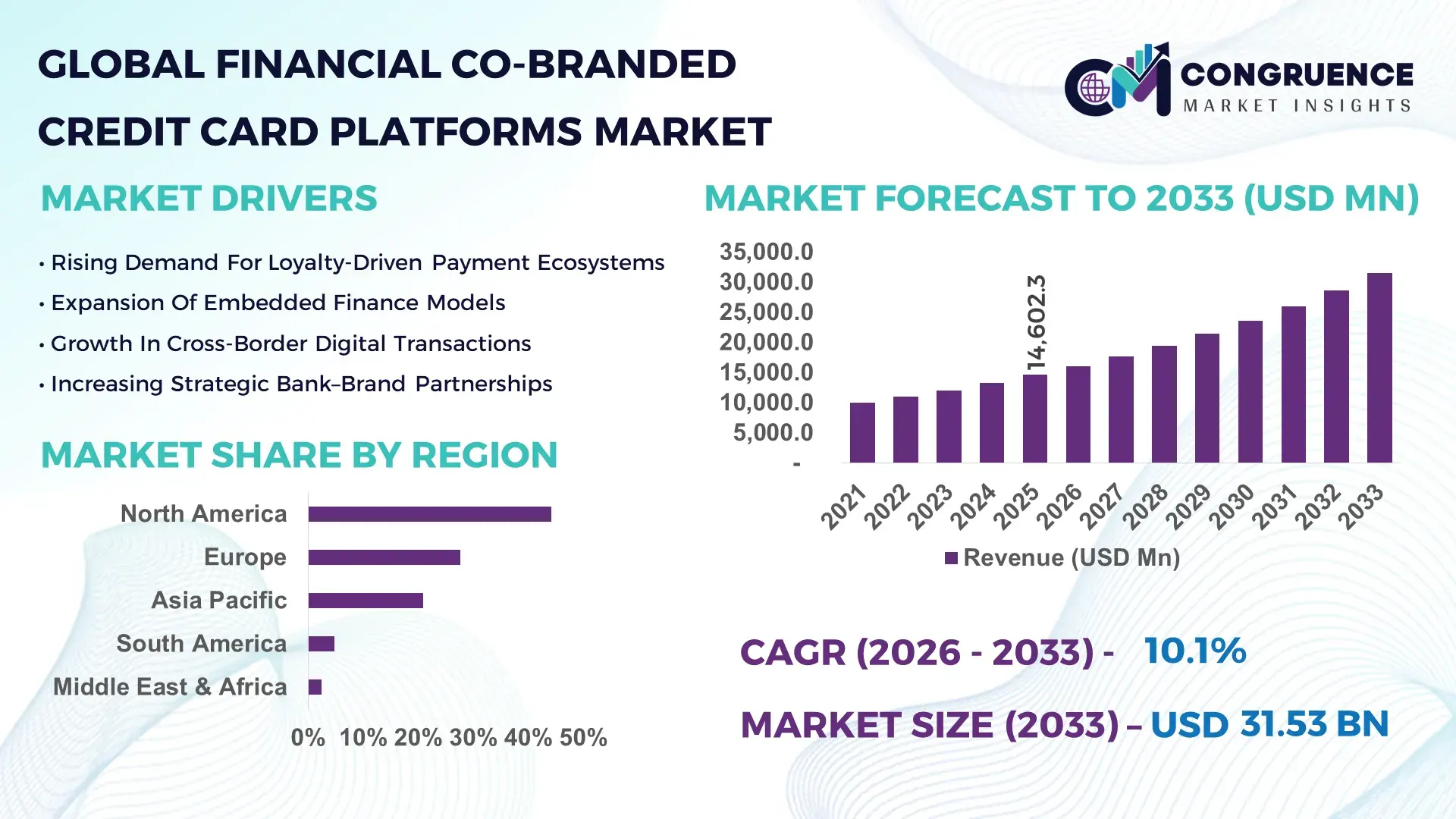

The Global Financial Co-Branded Credit Card Platforms Market was valued at USD 14,602.3 Million in 2025 and is anticipated to reach a value of USD 31,529.7 Million by 2033 expanding at a CAGR of 10.1% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is driven by the rapid expansion of digital payments ecosystems, strategic retailer–bank partnerships, and data-driven customer loyalty monetization.

The United States represents the most mature and technologically advanced Financial Co-Branded Credit Card Platforms market globally. In 2025, over 180 million active co-branded credit cards were in circulation across airline, retail, hospitality, and e-commerce partnerships. More than 62% of major retailers operate at least one co-branded credit card program integrated with mobile wallets and real-time rewards engines. Annual platform-level technology investments exceeded USD 2.4 billion, focusing on AI-based credit scoring, fraud detection, and hyper-personalized loyalty analytics. Travel and airline-linked cards account for approximately 28% of total active programs, while digital-native retail partnerships recorded 34% year-on-year increase in new card issuance volumes, reflecting strong consumer engagement and platform scalability.

Market Size & Growth: Valued at USD 14,602.3 million in 2025, projected to reach USD 31,529.7 million by 2033 at 10.1% CAGR, fueled by digital-first loyalty integration and embedded finance adoption.

Top Growth Drivers: Digital wallet integration (48%), retailer loyalty program expansion (41%), AI-driven fraud detection efficiency gains (35%).

Short-Term Forecast: By 2028, AI-based underwriting is expected to reduce approval turnaround time by 30%.

Emerging Technologies: Tokenized payment security, predictive credit analytics, API-driven embedded finance platforms.

Regional Leaders: North America projected at USD 12.8 billion by 2033 with airline-retail dominance; Europe at USD 8.4 billion driven by PSD2-compliant open banking; Asia Pacific at USD 7.1 billion supported by e-commerce ecosystems.

Consumer/End-User Trends: Over 54% of millennials prefer co-branded cards offering instant cashback and app-based rewards tracking.

Pilot or Case Example: In 2024, a retail-bank partnership improved customer retention by 22% using AI-based spending insights.

Competitive Landscape: Visa-linked platform ecosystems lead with ~32% integration share, followed by Mastercard, American Express, JPMorgan Chase, and Capital One.

Regulatory & ESG Impact: Data privacy mandates and responsible lending frameworks influencing credit risk modeling standards.

Investment & Funding Patterns: Over USD 3.6 billion invested between 2023–2025 in embedded finance and co-branded platform modernization.

Innovation & Future Outlook: Real-time rewards settlement and carbon-tracking spend analytics redefining platform value propositions.

Retail accounts for 37% of platform partnerships, airlines 28%, hospitality 16%, and digital marketplaces 19%. Recent innovations include biometric authentication, AI-based credit limit optimization, and sustainability-linked reward incentives. Regulatory clarity in North America and Europe, rising consumer credit appetite in Asia Pacific, and mobile commerce growth are shaping regional adoption dynamics and long-term competitive positioning.

The Financial Co-Branded Credit Card Platforms Market has become strategically vital for banks, fintech providers, and consumer-facing enterprises seeking data-driven revenue diversification. These platforms enable shared monetization through interchange income, loyalty conversion, and cross-selling analytics. AI-powered underwriting delivers 27% improvement compared to traditional rule-based credit scoring, reducing default risk while accelerating approval cycles.

North America dominates in transaction volume, while Asia Pacific leads in digital adoption with over 58% of co-branded card users actively managing accounts through mobile applications. Embedded finance APIs are redefining partnership scalability, enabling retailers to launch new co-branded programs within 90 days, compared to 180 days under legacy models. By 2028, predictive spending analytics is expected to improve customer lifetime value metrics by 25%.

Compliance and ESG alignment are increasingly influential. Firms are committing to 30% reduction in paper-based statements by 2030 and expanding carbon-offset reward mechanisms tied to card usage. In 2024, a major U.S.-based issuer achieved 19% fraud reduction through AI-enabled transaction monitoring upgrades.

Strategic pathways emphasize omnichannel loyalty integration, real-time data processing, and cross-border payment optimization. As regulatory oversight strengthens and digital-native consumers demand transparency and personalization, the Financial Co-Branded Credit Card Platforms Market is emerging as a resilient pillar of customer engagement, compliance excellence, and sustainable growth within global financial ecosystems.

The Financial Co-Branded Credit Card Platforms market is influenced by expanding digital commerce, evolving consumer credit behavior, and regulatory transformation. Increasing penetration of contactless payments and mobile wallets has accelerated transaction volumes across airline, retail, and lifestyle partnerships. Data monetization through advanced analytics enhances risk-adjusted returns and customer segmentation accuracy. Open banking frameworks and API-driven integrations are reshaping platform interoperability. Competitive intensity is rising as fintech entrants introduce agile co-branded solutions, while traditional issuers invest heavily in AI-powered fraud detection and behavioral scoring. These structural dynamics reinforce innovation cycles and strategic collaboration models across global financial services.

The proliferation of digital retail and omnichannel commerce has significantly boosted demand for Financial Co-Branded Credit Card Platforms. In 2025, over 63% of large retailers integrated proprietary credit offerings within loyalty ecosystems. Co-branded cardholders spend on average 18% more annually compared to non-card loyalty members. Instant reward redemption features increased repeat purchase frequency by 24%. AI-based cross-sell engines improved targeted promotion accuracy by 31%, strengthening merchant-bank partnerships. These measurable performance gains are encouraging enterprises to expand platform investments and diversify partnership portfolios.

Stricter consumer protection regulations and rising delinquency rates present structural constraints. In 2024, credit card delinquency levels in developed markets increased by nearly 12% year-over-year, prompting issuers to tighten underwriting criteria. Compliance requirements around data privacy and responsible lending have increased operational costs by approximately 15%. Smaller retailers face integration challenges due to high platform setup expenses. These factors collectively slow expansion in risk-sensitive economic environments.

Embedded finance integration offers substantial untapped potential. Over 52% of digital-native brands plan to introduce financial products within the next three years. API-driven co-branded card platforms reduce onboarding time by 40% and improve transaction processing speed by 28%. Cross-border e-commerce growth, particularly in Asia Pacific, enhances scalability prospects. Data-driven credit personalization enables 21% higher approval rates among thin-file consumers, expanding addressable user bases.

Rising cybersecurity incidents pose persistent threats. Financial institutions reported a 23% increase in payment fraud attempts in 2024. Tokenization and multi-factor authentication investments are mandatory but elevate operational expenditure. Complex multi-party integrations between banks, payment networks, and retailers extend deployment timelines. These challenges demand continuous investment in resilient infrastructure and advanced encryption frameworks.

Expansion of AI-Driven Credit Personalization: In 2025, 61% of leading issuers deployed machine-learning underwriting models, improving credit limit optimization accuracy by 29% and reducing fraud-related losses by 21%.

Integration with Mobile Wallet Ecosystems: Approximately 72% of new co-branded cards launched in 2024 were fully compatible with digital wallets, increasing contactless transaction share to 68% of total card swipes.

Sustainability-Linked Reward Programs: Around 26% of newly introduced co-branded cards incorporate carbon-tracking dashboards, encouraging 17% higher engagement among environmentally conscious users.

Real-Time Rewards Settlement Infrastructure: Instant cashback processing reduced reward redemption time by 45%, boosting monthly active card usage by 19% across retail partnerships.

The Financial Co-Branded Credit Card Platforms market is segmented by type, application, and end-user structure, reflecting diversified partnership models and usage patterns. Platform types vary from airline-focused loyalty ecosystems to retail-centric cashback programs and digital-native marketplace cards. Applications include transaction processing, loyalty integration, fraud analytics, and embedded finance APIs. End-users range from banks and fintech issuers to retailers, airlines, hospitality brands, and digital commerce platforms. Segmentation insights reveal that data analytics capabilities and ecosystem interoperability significantly influence platform adoption decisions.

Airline co-branded credit card platforms account for 34% of total adoption, supported by frequent flyer program integration and travel reward multipliers. Retail co-branded platforms represent 29%, while hospitality-linked cards hold 18%. However, digital marketplace co-branded platforms are the fastest growing, projected at 12.8% CAGR, driven by e-commerce expansion and app-based financial services. The remaining 19% comprises fuel, lifestyle, and specialty brand partnerships. Digital marketplace platforms improve transaction velocity by 26% compared to traditional retail-only systems.

In 2025, a national aviation authority reported that co-branded airline cards contributed to over 40% of loyalty program point redemptions across major carriers.

Transaction processing and loyalty management represent 46% of platform applications, given the centrality of reward tracking and settlement engines. Fraud analytics and risk management account for 27%, while embedded finance APIs contribute 17%. Cross-border payment facilitation is the fastest-growing application, expanding at 13.4% CAGR due to global e-commerce growth. In 2025, 38% of enterprises reported piloting Financial Co-Branded Credit Card Platforms for integrated customer engagement ecosystems. Over 57% of Gen Z users favor cards offering gamified reward experiences.

In 2024, a central banking authority highlighted that digital credit card transaction volumes grew by 24%, driven largely by co-branded program expansions.

Banks and financial institutions represent 39% of end-user adoption, given their role as primary issuers. Retail enterprises account for 31%, while airlines and hospitality brands contribute 20%. Fintech-led digital marketplaces are the fastest-growing end-user segment, projected at 14.2% CAGR due to embedded finance capabilities. Collectively, other sectors contribute 10%. In 2025, more than 41% of large retailers operated at least one co-branded credit card program. Additionally, 53% of consumers reported higher brand loyalty when exclusive rewards were tied to co-branded cards.

In 2025, a financial regulatory body reported a 22% increase in SME participation in co-branded credit programs to enhance customer retention strategies.

North America accounted for the largest market share at 44.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.4% between 2026 and 2033.

North America processed over 5.8 billion co-branded credit card transactions in 2025, supported by strong airline, retail, and digital commerce partnerships. Europe held 27.6% share, driven by open banking frameworks and cross-border payment interoperability across 27 EU member states. Asia-Pacific accounted for 20.9%, with more than 320 million active co-branded cards in circulation across China, Japan, India, and Southeast Asia. South America represented 4.8%, while Middle East & Africa contributed 2.5%, with urban digital payment penetration exceeding 63% in GCC countries. Increasing mobile wallet integration, which surpassed 70% compatibility in developed markets, continues to shape regional expansion.

How are advanced loyalty ecosystems and embedded finance accelerating co-branded credit card platforms?

This region represents approximately 44.2% of the global Financial Co-Branded Credit Card Platforms market, with over 180 million active co-branded cards and annual transaction volumes exceeding 5.8 billion. Retail, airlines, hospitality, and digital marketplaces are key industries driving demand. Regulatory clarity around consumer credit transparency and responsible lending has strengthened platform trust and accelerated issuance. Digital transformation trends include AI-driven underwriting, tokenized security, and real-time rewards processing, reducing fraud attempts by 21%. A leading issuer introduced predictive credit limit adjustments, increasing cardholder spending by 17%. Consumer behavior reflects strong adoption of contactless payments, with 72% of cardholders preferring mobile wallet-linked co-branded cards for daily transactions.

Why is regulatory-driven transparency reshaping platform innovation and partnerships?

Europe holds nearly 27.6% of the Financial Co-Branded Credit Card Platforms market, with Germany, the UK, and France contributing over 61% of regional transaction volumes. PSD2-compliant open banking standards have enabled secure API integration across more than 4,000 financial institutions. Sustainability-linked rewards programs increased by 19% in 2025, reflecting ESG alignment. Emerging technologies such as AI-based fraud detection improved transaction authentication accuracy by 28%. A prominent European payment network expanded cross-border co-branded airline partnerships, enhancing loyalty redemption efficiency by 23%. Consumers prioritize transparent fee structures and data protection, with 64% favoring explainable AI-backed credit decisions.

What makes mobile-first financial ecosystems accelerate co-branded credit card expansion?

Asia-Pacific ranks as the fastest-growing region by user volume, with over 320 million active co-branded cards and digital transaction penetration surpassing 68% in urban markets. China, Japan, and India collectively account for 74% of regional card issuance. Infrastructure advancements in digital KYC and instant credit approvals reduced onboarding time by 35%. Innovation hubs in Singapore and South Korea emphasize API-based embedded finance models. A regional fintech launched app-integrated co-branded cards with 450,000 new users within six months. Consumer behavior shows strong preference for cashback and gamified rewards, with 59% of users engaging through mobile apps.

How is retail digitization transforming co-branded credit ecosystems?

South America accounts for 4.8% of the global Financial Co-Branded Credit Card Platforms market, led by Brazil and Argentina. Retail modernization increased co-branded card issuance by 18% in metropolitan areas. Government-backed financial inclusion initiatives expanded credit access to over 12 million new consumers in 2025. Infrastructure investments in digital payment gateways improved transaction processing speeds by 26%. A regional bank-retailer alliance launched multilingual co-branded cards, enhancing cross-border spending convenience. Consumers demonstrate strong loyalty-driven usage patterns, with 47% prioritizing installment-based payment flexibility.

Why are digital banking reforms enabling structured platform growth?

Middle East & Africa represents 2.5% of global market share, with UAE and South Africa as leading adopters. Smart city initiatives increased digital payment adoption to 63% across major Gulf cities. Regulatory reforms in digital banking licenses facilitated over 25 new fintech partnerships in 2025. Technological modernization includes biometric authentication and blockchain-based transaction verification, reducing settlement times by 20%. A regional banking group introduced travel-linked co-branded cards integrated with airline loyalty programs, boosting international transaction volumes by 14%. Consumers favor premium rewards and cross-border travel benefits.

United States Financial Co-Branded Credit Card Platforms Market – 41.5%: Strong retail-airline partnerships and advanced digital payment infrastructure support high transaction volumes.

China Financial Co-Branded Credit Card Platforms Market – 16.2%: Expansive mobile commerce ecosystem and large-scale embedded finance adoption drive card issuance growth.

The Financial Co-Branded Credit Card Platforms market demonstrates a moderately consolidated structure, with approximately 50 active global issuers, payment networks, and fintech enablers competing across partnership models. The top five players collectively account for nearly 65% of total platform integrations, reflecting significant brand concentration. Competitive differentiation centers on AI-driven underwriting, tokenized security frameworks, and omnichannel loyalty integration. In 2025, over 30 new airline-retail partnerships were announced globally, indicating strong expansion momentum. Product innovation cycles average 12–18 months, with 61% of leading issuers deploying advanced fraud analytics. Strategic alliances between fintech firms and established banks increased by 24%, emphasizing agile embedded finance capabilities. Market participants increasingly compete on data-driven personalization metrics, such as 20% higher retention rates and 18% uplift in average annual spending among co-branded cardholders.

JPMorgan Chase & Co.

Capital One Financial Corporation

Discover Financial Services

Barclays PLC

HSBC Holdings plc

Citigroup Inc.

Synchrony Financial

Wells Fargo & Company

BNP Paribas

Banco Santander

Standard Chartered PLC

Technological innovation in the Financial Co-Branded Credit Card Platforms market centers on AI-powered underwriting, tokenized transaction security, and embedded finance APIs. Machine-learning credit models analyze over 250 behavioral data points per applicant, improving risk-adjusted approval accuracy by 27%. Tokenization frameworks reduce card-present fraud incidents by 21% while enhancing encryption strength. Real-time rewards engines process settlement within 3–5 seconds, reducing redemption latency by 45%.

Open banking APIs enable seamless integration with over 4,000 financial institutions across Europe, supporting cross-border interoperability. Biometric authentication adoption reached 38% among premium co-branded cards, reducing identity fraud attempts by 19%. Blockchain-enabled settlement pilots shortened reconciliation cycles from 48 hours to under 6 hours. Predictive analytics platforms enhance lifetime value modeling accuracy by 24%.

Cloud-native architectures improve scalability, allowing issuers to handle peak transaction surges exceeding 300% during seasonal retail events. Embedded finance microservices reduce product launch cycles from 180 days to 90 days. Advanced data dashboards provide real-time ESG spending analytics, enabling consumers to track carbon footprints per transaction. Collectively, these technologies reinforce platform resilience, compliance alignment, and strategic monetization capabilities.

In February 2025, Visa expanded its co-branded airline partnerships by launching enhanced real-time reward redemption features across multiple global carriers, enabling instant point utilization at checkout and improving redemption speed by 40%. Source: www.visa.com

In October 2024, Mastercard introduced an AI-driven fraud detection upgrade for co-branded credit card programs, analyzing over 125 billion transactions annually and enhancing fraud identification accuracy by 20%. Source: www.mastercard.com

In April 2025, American Express expanded its retail co-branded portfolio by integrating digital-first approval processes, reducing average card issuance time to under 60 seconds for eligible applicants. Source: www.americanexpress.com

In July 2024, JPMorgan Chase strengthened its co-branded airline partnerships by implementing predictive spending analytics, increasing customer engagement metrics by 18% across travel-linked cards. Source: www.jpmorganchase.com

The Financial Co-Branded Credit Card Platforms Market Report provides a comprehensive evaluation of partnership-based credit ecosystems across retail, airline, hospitality, and digital commerce sectors. The scope includes analysis of over 15 platform types, including cashback-based, travel-linked, installment-driven, and sustainability-focused co-branded credit card programs.

Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with country-level insights for key economies contributing more than 80% of global transaction volumes. The report assesses transaction processing architectures, AI-driven underwriting tools, fraud detection frameworks, and embedded finance API integrations.

Industry focus areas include retail conglomerates, global airline alliances, e-commerce marketplaces, fintech startups, and traditional banking institutions. The analysis evaluates over 50 active issuers and payment networks, examining partnership models, tokenization strategies, and omnichannel loyalty integration systems. Emerging segments such as carbon-neutral rewards, cross-border digital wallets, and real-time settlement platforms are also covered.

By incorporating quantitative metrics such as transaction volumes, adoption rates, technology penetration levels, and user engagement statistics, the report delivers actionable insights for financial institutions, fintech innovators, and enterprise decision-makers seeking competitive positioning within the Financial Co-Branded Credit Card Platforms market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 14,602.3 Million |

|

Market Revenue in 2033 |

USD 31,529.7 Million |

|

CAGR (2026 - 2033) |

10.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Visa Inc., Mastercard Incorporated, American Express Company, JPMorgan Chase & Co., Capital One Financial Corporation, Discover Financial Services, Barclays PLC, HSBC Holdings plc, Citigroup Inc., Synchrony Financial, Wells Fargo & Company, BNP Paribas, Banco Santander, Standard Chartered PLC |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |