Reports

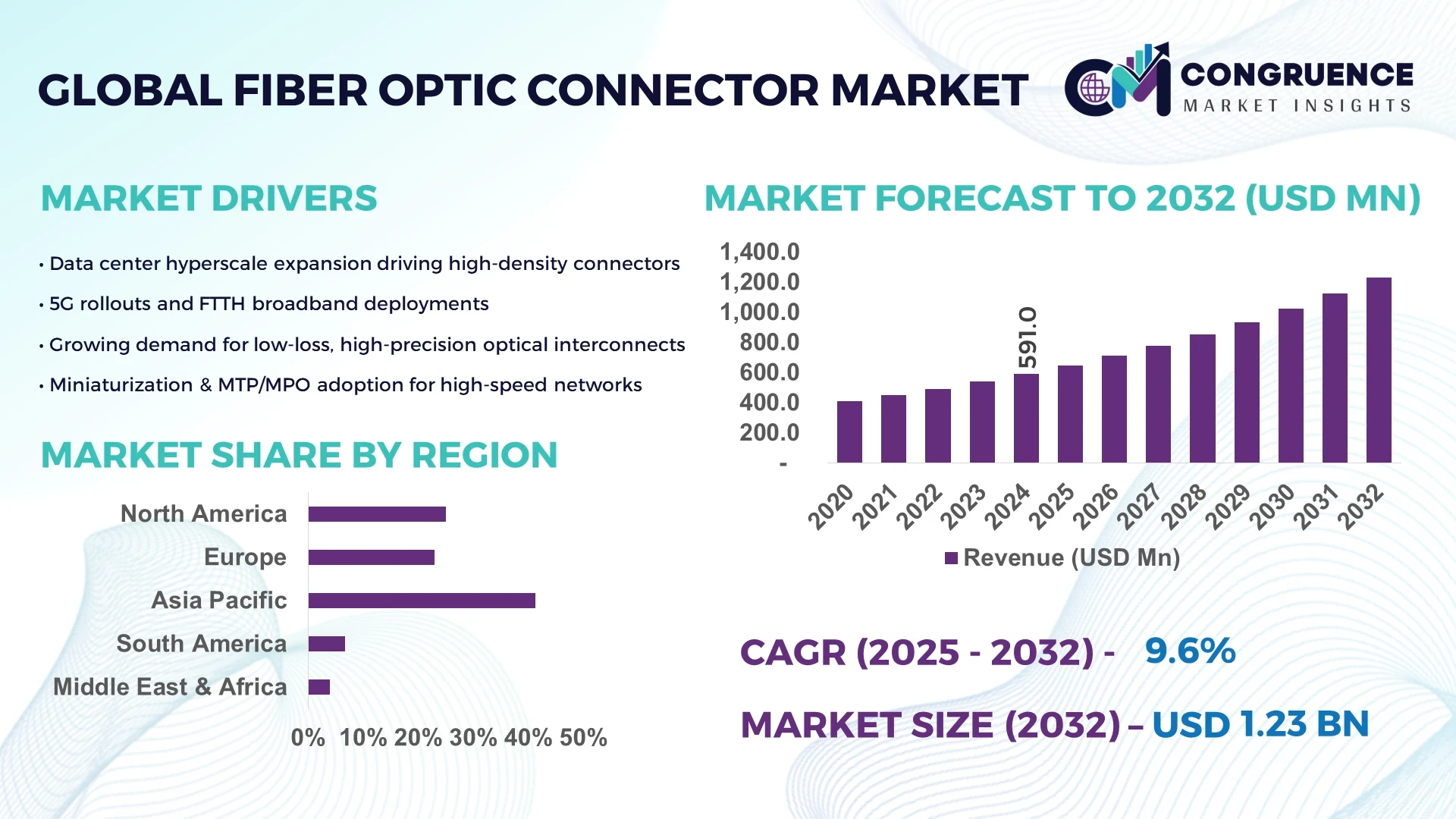

The Global Fiber Optic Connector Market was valued at USD 591.0 Million in 2024 and is anticipated to reach a value of USD 1,230.5 Million by 2032 expanding at a CAGR of 9.6% between 2025 and 2032.

The United States holds a dominant position in the Fiber Optic Connector Market, backed by advanced production infrastructure, high capital investments in fiber-optic R&D, and widespread adoption of high-speed data transmission solutions in defense, telecommunications, and healthcare. The country continues to lead in the development of miniaturized, high-performance connectors for next-generation data centers and 5G network expansion.

The Fiber Optic Connector Market is witnessing steady growth across major industries including telecommunications, data centers, defense, aerospace, and medical diagnostics. The telecom sector remains a major consumer due to global 5G expansion and fiber-to-the-home (FTTH) deployments. Technological innovations—such as push-pull connectors, multi-fiber push-on (MPO) connectors, and high-density interface formats—are enhancing bandwidth performance and installation efficiency. Regulatory frameworks pushing energy efficiency and environmentally compliant infrastructure are encouraging the adoption of sustainable materials in connector production. Emerging economies in Asia-Pacific are showing strong consumption patterns due to infrastructure upgrades, while Europe and North America are driving demand for ruggedized connectors in mission-critical applications. Market players are investing in polymer innovations, ultra-low-loss technology, and AI-powered inspection systems to maintain competitive edge in a dynamic and rapidly evolving landscape.

Artificial Intelligence is significantly transforming the Fiber Optic Connector Market by enhancing manufacturing accuracy, minimizing waste, and streamlining supply chain operations. AI-driven quality control systems are detecting microscopic imperfections in connector alignment and polish, ensuring higher consistency in optical performance. These systems, integrated into production lines, have led to up to 30–35% improvements in yield rates and reductions in manual inspection labor.

AI-powered predictive maintenance tools are also being employed to reduce downtime in manufacturing facilities by forecasting wear and tear on polishing and grinding equipment. In logistics, AI algorithms are optimizing inventory management, shortening lead times, and improving on-time delivery rates across regions. Telecommunications providers are utilizing AI to simulate network configurations, allowing for the optimal placement of fiber optic connectors to reduce signal attenuation and improve bandwidth allocation.

As more enterprises digitize operations and expand their data infrastructure, the Fiber Optic Connector Market is leveraging AI not just for production but also for R&D, allowing quicker prototyping and testing of new connector types. These advances are making manufacturing more responsive and scalable, directly benefiting industries reliant on high-speed, low-loss optical communication systems.

“In early 2025, a leading U.S.-based optical interconnect company deployed a deep learning-driven visual inspection platform that achieved a 98.6% accuracy rate in identifying polishing defects in LC and SC connectors. This implementation reduced manual inspection time by 60% and enhanced product consistency across high-volume batches.”

The Fiber Optic Connector Market is being reshaped by rapid digital transformation, increasing demand for high-speed networks, and growing adoption across defense, medical, and industrial sectors. Industry players are focused on developing compact, low-loss, and field-installable connectors that meet modern performance requirements. Government regulations mandating energy-efficient and sustainable infrastructure are pushing manufacturers to innovate with recyclable and biocompatible materials. On the other hand, challenges like material procurement delays and rising costs are influencing pricing and production planning. Global competition and shifting consumption patterns across regions continue to impact market positioning, with Asia-Pacific emerging as a high-growth consumption hub.

The global expansion of high-speed data networks is driving robust demand in the Fiber Optic Connector Market. Massive rollouts of 5G infrastructure and hyperscale data centers require high-density, high-speed optical connectivity. New data center projects in 2024 integrated MPO and LC connectors supporting 400G and 800G speeds, enabling compact, high-throughput cabling. FTTH deployments are also expanding rapidly in urban and rural settings, increasing demand for quick-installation, pre-terminated connectors. As communication infrastructure scales up to support IoT, AI, and cloud services, the need for low-insertion-loss, thermally stable connectors becomes even more critical for network performance and durability.

The high initial cost of deploying fiber optic infrastructure remains a significant restraint in the Fiber Optic Connector Market. From specialized tools and precision polishing machines to skilled labor and cleanroom environments, the upfront investment is considerable. In rural and remote areas, fiber optic installation can cost up to 40% more due to logistical complexities. Additionally, the cost of compliance with international optical standards and precision testing adds to financial barriers, particularly for small and mid-sized enterprises. These expenses slow down adoption, especially in emerging markets where capital availability and technical expertise are limited.

The growing integration of fiber optics in medical devices presents a major opportunity for the Fiber Optic Connector Market. Connectors are increasingly used in applications like endoscopy, optical coherence tomography (OCT), and minimally invasive surgeries. These medical systems demand high-resolution imaging, light precision, and sterilizable, biocompatible connectors. In 2025, newly introduced optical connectors for flexible endoscopes enhanced real-time image clarity while reducing signal degradation. With hospitals and clinics upgrading diagnostic infrastructure globally, demand for specialized medical-grade connectors is rising—creating new avenues for product innovation and tailored solutions.

The manufacturing of fiber optic connectors poses ongoing challenges due to high precision requirements. The process involves multiple steps—grinding, polishing, end-face geometry alignment, and contamination-free assembly. Even minor deviations can result in sub-optimal optical performance or increased return loss. In 2024, several manufacturers faced rising costs due to inconsistent polishing outcomes in APC connector production. Moreover, maintaining ISO and IEC compliance demands cleanroom operations and continual investment in inspection and testing equipment. These complexities hinder mass-scale production and elevate entry barriers for new market participants.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Fiber Optic Connector Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Surge in Miniaturized and High-Density Connector Designs: Compact devices and dense data centers are driving the need for small, high-density connectors. MPO connectors with up to 144 fibers per unit are becoming common in hyperscale environments. This enables greater bandwidth in smaller physical spaces, helping enterprises expand without increasing infrastructure footprint.

Integration of Smart Testing and Monitoring Tools: Fiber optic connectors now feature embedded diagnostics that monitor insertion quality, temperature shifts, and end-face contamination. Smart connectors introduced in 2025 can alert users of improper connections, reducing downtime and increasing reliability in mission-critical networks.

Eco-Friendly Material Innovation: Sustainability is driving the adoption of low-carbon and bio-based materials in connector housings. Recent pilot programs in the EU successfully tested recyclable polymer components under thermal stress without performance loss, aligning with 2025 environmental compliance directives.

The Fiber Optic Connector Market is broadly segmented by type, application, and end-user, reflecting diverse integration across various sectors. The type segment includes key product formats used in single-mode and multi-mode systems, tailored for high-performance data transmission and bandwidth efficiency. Applications range from telecommunications and data centers to industrial automation and medical diagnostics, driven by the increasing demand for low-latency and high-capacity communication. End-user segmentation reflects widespread adoption across government, commercial enterprises, military, and healthcare institutions. Each segment displays unique growth trajectories based on infrastructure investments, technological developments, and regulatory mandates, offering strategic insights for manufacturers and stakeholders seeking optimized market positioning.

The Fiber Optic Connector Market includes several product types such as LC (Lucent Connector), SC (Subscriber Connector), ST (Straight Tip), MTP/MPO (Multi-Fiber Push-On/Pull-Off), and FC (Ferrule Connector). Among these, LC connectors dominate the market due to their compact size, low insertion loss, and wide adoption in high-density data centers and telecommunications systems. Their push-pull mechanism and single-mode compatibility make them a preferred choice for modern network architectures.

MTP/MPO connectors are the fastest-growing type, driven by rapid data center expansion and increased use in high-speed parallel optical links. Their ability to accommodate up to 144 fibers in a single connector significantly reduces cable management complexity and space requirements.

ST and FC connectors, though less prevalent in current deployments, maintain relevance in legacy systems and niche applications such as instrumentation and industrial environments. SC connectors continue to see use in telecom networks but are gradually being replaced by smaller, more efficient alternatives in newer installations.

The leading application of fiber optic connectors is in telecommunications, where growing internet penetration and 5G deployment are increasing the demand for reliable, high-bandwidth connectivity. Fiber optic connectors are vital in connecting transmission equipment, junctions, and subscriber networks, making them central to modern telecom infrastructure.

Data centers represent the fastest-growing application area, fueled by the global surge in cloud computing, video streaming, and enterprise-level storage solutions. Fiber optic connectors enable fast, uninterrupted data flow across server racks and between distributed facilities, supporting bandwidth-intensive operations with minimal latency.

Other important applications include medical diagnostics, where fiber connectors are integral in imaging devices like endoscopes and OCT systems, and industrial automation, where they ensure noise-immune, high-speed data transfer in harsh environments. Military and aerospace applications also rely on fiber connectors for secure and ruggedized communication links in mission-critical operations.

Among end-users, telecommunication service providers remain the dominant segment, utilizing fiber optic connectors for large-scale infrastructure upgrades, FTTH rollouts, and next-gen network deployment. Their consistent demand stems from the need for high-speed, low-loss transmission in both urban and rural networks.

Data center operators are the fastest-growing end-users, propelled by the expansion of hyperscale facilities, edge computing sites, and distributed cloud networks. These operators require compact, scalable, and high-density connector solutions to meet rising performance and space efficiency needs.

Other contributing end-users include government agencies and defense organizations, which implement fiber-based networks for secure and high-speed communication systems. The healthcare sector is also emerging as a significant end-user, with fiber optics increasingly embedded in diagnostic and surgical equipment for real-time, high-resolution data transmission. Additionally, industrial enterprises are adopting fiber optic connectors to facilitate automation, real-time control, and robust communication within production environments. Each end-user group plays a critical role in shaping demand dynamics across the global landscape.

Asia-Pacific accounted for the largest market share at 41.3% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2025 and 2032.

The Asia-Pacific region leads due to its massive telecommunications infrastructure investments and rapid digitalization in countries like China, Japan, and India. Meanwhile, North America's aggressive 5G rollout plans, coupled with substantial data center expansions and advanced industrial automation, are expected to drive accelerated growth. Other regions, including Europe, South America, and the Middle East & Africa, are also showing promising developments, fueled by national broadband programs, green technology initiatives, and growing healthcare infrastructure.

North America captured 26.7% of the global Fiber Optic Connector Market in 2024, led by robust telecom networks, hyperscale data centers, and widespread 5G deployment initiatives. The United States and Canada are spearheading innovation in optical connectivity, particularly for cloud computing, IoT integration, and AI-driven systems. Government-led initiatives such as broadband infrastructure expansion programs and tax incentives for digital transformation are bolstering industry investment. Additionally, advancements in photonics, high-density connector designs, and intelligent monitoring systems are transforming network efficiency. The integration of fiber optics into defense and aerospace systems also contributes to market expansion, ensuring strong long-term demand in this region.

Europe held 18.9% of the global Fiber Optic Connector Market in 2024, with Germany, the UK, and France leading regional demand. Fiber optic connectors are vital to Europe's push for smart cities, sustainable ICT, and next-gen industrial communication systems. Regulatory bodies such as the European Telecommunications Standards Institute (ETSI) are setting strict guidelines for low-loss, energy-efficient connectivity. The region is also witnessing increased investment in renewable energy infrastructure and EV charging networks, which require rugged and high-speed fiber connectivity. Emerging adoption of Industry 4.0 technologies and the transition to fiber-dominant broadband networks are driving consistent growth across multiple end-use sectors.

Asia-Pacific accounted for the largest share of the Fiber Optic Connector Market at 41.3% in 2024. China, India, and Japan are the top consumers, driven by expanding telecom networks, urbanization, and the digitization of manufacturing. China leads in production scale and fiber optic cable deployment, while India is accelerating FTTH expansion in both rural and metro areas. Japan’s leadership in advanced connector designs and miniaturization technology further strengthens the region's innovation base. Investments in smart infrastructure, 5G trials, and AI-enabled manufacturing hubs are propelling the region’s dominance, supported by favorable government infrastructure policies and a high demand for cloud services.

South America contributed approximately 6.5% to the global Fiber Optic Connector Market in 2024, with Brazil and Argentina being the key contributors. Rapid digital inclusion projects, government-supported telecom upgrades, and fiber backbone development are fueling market growth. Brazil’s national fiber-optic expansion plans are improving rural internet access, increasing demand for field-installable connectors. The energy sector, particularly in renewables and smart grid systems, is also deploying fiber connectivity for real-time monitoring and automation. Government incentives related to IT infrastructure modernization and increased international trade cooperation are expected to drive continued growth in this developing yet strategic region.

Middle East & Africa held 6.6% of the global Fiber Optic Connector Market share in 2024. Countries like the UAE and South Africa are leading regional demand due to increasing investment in telecommunications infrastructure and data centers. The UAE is rapidly deploying fiber for smart city projects, while South Africa is digitizing education and healthcare networks. The oil & gas industry is also utilizing fiber connectors for real-time data monitoring in harsh environments. Regional partnerships, such as African Continental Free Trade Area (AfCFTA), are supporting tech investments and driving cross-border infrastructure projects, pushing the demand for ruggedized, high-speed optical connectivity.

China – 27.4% Market Share

High production capacity and extensive fiber deployment across residential, industrial, and telecom sectors.

United States – 21.6% Market Share

Strong end-user demand from hyperscale data centers and defense applications, along with technological innovation leadership.

The Fiber Optic Connector Market features a competitive landscape with over 150 active companies globally, ranging from multinational manufacturers to specialized component providers. Market leaders maintain strong brand recognition, extensive product portfolios, and established supply chain networks. Key players are focusing on strategic partnerships, technology integration, and geographic expansion to gain a competitive edge. Notable strategies include product miniaturization for high-density environments, ruggedized connectors for military-grade applications, and plug-and-play solutions for telecom and FTTH installations.

In 2023 and 2024, the market saw a significant rise in mergers and acquisitions, especially between European and North American firms aiming to consolidate R&D capabilities. Several players launched next-gen fiber connectors featuring lower insertion loss, higher durability, and built-in diagnostic capabilities. Competition is also intensifying in the AI-integrated manufacturing and smart testing systems space, with companies developing automated defect detection technologies and predictive maintenance algorithms. Regional vendors in Asia-Pacific continue to challenge global incumbents through cost-effective, scalable manufacturing capabilities. The competitive environment remains dynamic, with innovation, speed to market, and customization playing central roles in sustained market leadership.

Amphenol Corporation

TE Connectivity

Molex LLC

Sumitomo Electric Industries, Ltd.

Fujikura Ltd.

3M Company

HUBER+SUHNER AG

Radiall SA

SENKO Advanced Components

Aptiv PLC

Diamond SA

The Fiber Optic Connector Market is undergoing a wave of technological transformation, focusing on higher performance, miniaturization, and smart capabilities. One of the most significant advancements is the development of multi-fiber connectors like MTP/MPO formats that support high-density data transmission with up to 144 fibers in a single unit. These are becoming standard in hyperscale data centers and high-capacity communication hubs.

Low-insertion-loss ferrules, precision-polished end-faces, and angled physical contact (APC) configurations are now widely used to reduce signal attenuation and back reflection. Manufacturers are increasingly using advanced ceramic and polymer materials to enhance connector durability, temperature tolerance, and biocompatibility for medical applications.

Emerging innovations include intelligent fiber connectors embedded with microchips and sensors to monitor alignment quality, signal strength, and contamination. AI-powered polishing and visual inspection systems are optimizing quality control in real time, enhancing production yields by over 30% in some facilities.

Tool-less field-termination connectors are gaining popularity for FTTH and industrial automation, reducing installation time and improving scalability. The rise of photonic integration and quantum communication protocols is also pushing R&D into ultra-low-loss, nano-scale connector designs suitable for future high-frequency and secure transmission systems. These technology trends are reshaping manufacturing, application, and deployment strategies globally.

• In March 2024, TE Connectivity launched a new generation of LC connectors with integrated contamination-resistant design, reducing end-face cleaning frequency by 45% and extending maintenance intervals in mission-critical telecom applications.

• In September 2023, Fujikura unveiled an ultra-compact MPO connector for 800G Ethernet systems, enabling up to 50% space savings in data centers while maintaining high-speed signal integrity.

• In December 2023, HUBER+SUHNER introduced a robust outdoor-rated connector series designed for harsh environments, offering resistance to UV radiation, water ingress (IP68), and extreme temperatures from -40°C to +85°C.

• In May 2024, SENKO Advanced Components deployed a smart connector solution embedded with an RFID tag for real-time port tracking and automated patch panel management in tier-4 data centers across North America.

The Fiber Optic Connector Market Report offers a comprehensive analysis covering a wide spectrum of market segments, including product types such as LC, SC, ST, FC, and MTP/MPO connectors. The study evaluates usage across diverse applications like telecommunications, data centers, medical diagnostics, industrial automation, and military systems. It includes insights into field-installable connectors, push-pull mechanisms, high-density arrays, and emerging smart connector technologies.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, detailing region-specific trends, manufacturing hubs, and consumption patterns. The scope also extends to understanding technological evolution—such as the adoption of AI-driven inspection, biocompatible materials for medical connectors, and smart factory integration.

Additionally, the report includes a strategic review of market dynamics, regulatory frameworks, and competitive positioning of key players. It highlights evolving demand for miniaturization, ruggedization, and sustainability in connector design. The study further identifies untapped opportunities in niche sectors such as renewable energy grid integration, photonics, and remote healthcare systems. By offering detailed segmentation and regional analysis, the report serves as a valuable decision-making tool for stakeholders across the fiber optic ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 591.0 Million |

| Market Revenue (2032) | USD 1,230.5 Million |

| CAGR (2025–2032) | 9.6 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Amphenol Corporation, TE Connectivity, Molex LLC, Sumitomo Electric Industries, Ltd., Fujikura Ltd., 3M Company, HUBER+SUHNER AG, Radiall SA, SENKO Advanced Components, Aptiv PLC, Diamond SA |

| Customization & Pricing | Available on Request (10% Customization is Free) |