Reports

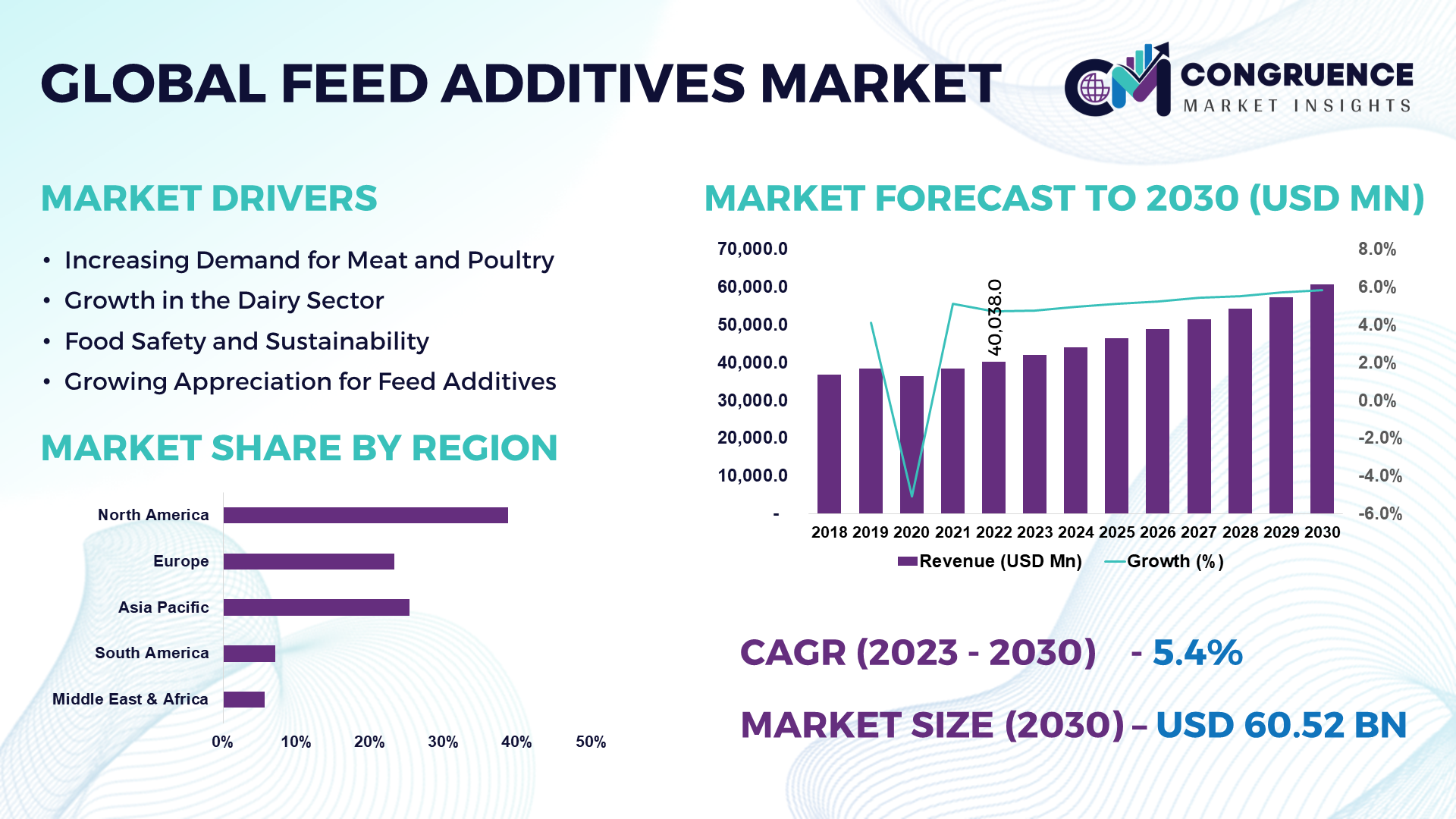

The Global Feed Additives Market was valued at USD 44,478.8 Million in 2024 and is anticipated to reach a value of USD 67,745.1 Million by 2032, expanding at a CAGR of 5.4% between 2025 and 2032. This growth is driven by increasing demand for high-quality livestock products and advancements in feed formulation technologies.

China leads the global Feed Additives market, with a production capacity exceeding 8 million metric tons annually and significant investments exceeding USD 1.2 billion in modern feed additive facilities by 2024. The country has prioritized innovation, with over 35% of domestic production involving enzyme-based additives and probiotics. China’s feed additive industry is heavily integrated with poultry, swine, and aquaculture sectors, serving as the largest consumer of enzyme and amino acid additives globally. Advanced R&D centers in provinces such as Jiangsu and Shandong focus on cost-effective production technologies, while automation adoption in manufacturing has improved operational efficiency by more than 18% over the past five years.

Market Size & Growth: Valued at USD 44,478.8 Million in 2024, expected to reach USD 67,745.1 Million by 2032 at a CAGR of 5.4%, driven by rising demand for sustainable livestock nutrition.

Top Growth Drivers: Increasing protein demand (32%), rising livestock production efficiency (27%), growing aquaculture industry adoption (21%).

Short-Term Forecast: By 2028, cost efficiency in feed formulation expected to improve by 15%.

Emerging Technologies: Enzyme-based additives, precision nutrition software, and microbiome-targeted feed solutions.

Regional Leaders: Asia-Pacific USD 28,400 Million by 2032 (rapid industrial farming adoption), North America USD 16,800 Million (precision nutrition integration), Europe USD 12,600 Million (sustainable feed regulations).

Consumer/End-User Trends: Rising preference for additive-enriched livestock feed among large-scale farms and aquaculture operations.

Pilot or Case Example: 2024 pilot in Brazil achieved 12% improvement in feed conversion ratio through enzyme additive integration.

Competitive Landscape: Cargill Inc. (~14%), Archer Daniels Midland Company, Evonik Industries AG, Novus International, BASF SE.

Regulatory & ESG Impact: Stricter animal welfare laws and environmental sustainability regulations shaping product innovation.

Investment & Funding Patterns: Over USD 850 million in global R&D investment in 2024; increasing venture funding in feed additive startups.

Innovation & Future Outlook: Integration of AI-driven feed optimization and sustainable ingredient sourcing expected to transform the market.

China’s leadership in feed additive production is supported by robust R&D, substantial investments in manufacturing, and increasing adoption of enzyme-based and probiotic solutions. This trend is driven by rising demand for sustainable livestock feed, enabling higher production efficiency.

The Feed Additives Market is strategically relevant as a critical driver for efficiency, sustainability, and nutritional innovation in the livestock and aquaculture industries. The adoption of enzyme-based feed additives delivers up to 18% improvement in feed conversion ratio compared to conventional protein supplements. Asia-Pacific dominates in volume, while North America leads in adoption with over 42% of livestock enterprises implementing advanced feed additive solutions. By 2027, AI-driven feed formulation platforms are expected to improve nutrient efficiency by 14%, enabling cost-effective production and optimized livestock performance. Firms are committing to ESG metric improvements such as a 25% reduction in greenhouse gas emissions from feed production by 2030. In 2024, a pilot program in the Netherlands achieved a 10% reduction in feed waste through microbiome-targeted additive integration, underscoring the potential for measurable efficiency gains. Strategically, the Feed Additives Market is shifting toward precision nutrition, sustainability integration, and digital transformation. This positions it as a pillar of resilience, compliance, and sustainable growth, enabling the industry to address global food security challenges while aligning with environmental and regulatory goals.

Increasing demand for sustainable livestock production is significantly impacting the Feed Additives Market. Over 68% of large-scale livestock producers are integrating enzyme-based and probiotic additives to enhance feed efficiency while reducing environmental impact. Sustainable practices such as nutrient recycling and waste reduction rely heavily on these additives to improve overall production efficiency. For example, in China, adoption of enzyme additives in poultry feed reduced nitrogen emissions by 15%, aligning with environmental goals. This trend is driven by stricter regulatory standards, consumer preference for eco-friendly products, and rising pressure from environmental sustainability initiatives. The integration of sustainable feed additives enables producers to meet regulatory compliance while enhancing livestock productivity, making this driver a key catalyst for market expansion.

The high cost of advanced feed additive formulations is a major restraint for the Feed Additives Market. Specialty additives such as enzymes, probiotics, and organic acids require complex production processes and rigorous quality control, significantly increasing costs. In Europe, feed additive prices are on average 20–25% higher than in developing regions due to strict regulatory compliance and production expenses. Small and medium-scale farms often find it financially challenging to adopt advanced additives, limiting broader market penetration. Additionally, fluctuating raw material prices for key ingredients like amino acids and organic acids add unpredictability to manufacturing costs. These financial barriers slow adoption rates, especially in cost-sensitive markets, restraining the speed at which innovative feed additive solutions can be integrated into livestock nutrition strategies globally.

Precision livestock farming offers significant opportunities for the Feed Additives Market. By integrating AI-driven feed formulation systems, producers can tailor additive composition for specific livestock needs, improving feed efficiency and reducing waste. For example, precision nutrition in aquaculture has enabled a 12% increase in growth rates while lowering feed consumption. Asia-Pacific shows particular potential, with an estimated 48% of livestock producers expected to adopt precision feeding technologies by 2027. These systems allow real-time monitoring of nutrient requirements, enabling targeted use of enzymes, probiotics, and amino acids. The convergence of feed additives with data-driven nutrition strategies presents opportunities for improved productivity, sustainability, and cost-effectiveness, positioning the Feed Additives Market to capitalize on technological innovation.

Regulatory variations and compliance complexities are key challenges for the Feed Additives Market. Different countries have diverse standards for permissible additives, quality testing, and labelling, creating barriers for international trade and product standardization. For example, the EU maintains stringent regulations on additive usage, requiring comprehensive safety evaluations, which increases time-to-market and compliance costs. In contrast, regulatory frameworks in emerging economies are evolving but remain inconsistent, creating uncertainty for global producers. These variations demand high operational adaptability and additional investment in compliance infrastructure. Furthermore, tracking and documenting compliance across regions require advanced supply chain transparency tools, adding complexity and cost. Such regulatory challenges limit market scalability and slow the adoption of innovative feed additive technologies.

• Surge in Precision Nutrition Adoption: Precision nutrition adoption in the Feed Additives market has grown by over 38% in the past three years, driven by demand for optimized livestock health and productivity. Precision systems enable targeted nutrient delivery, improving feed conversion ratios by up to 16% compared to traditional feed approaches. Asia-Pacific leads in implementation, with over 45% of commercial farms integrating precision nutrition solutions by 2024, while North America leads adoption intensity with 42% of enterprises deploying advanced feed formulation technologies.

• Expansion of Enzyme-based Additives: Enzyme-based feed additives have seen a 27% rise in adoption due to their ability to enhance digestibility and nutrient absorption in livestock. These additives are particularly prominent in poultry and aquaculture, where they reduce feed costs by up to 12%. Europe has led enzyme additive integration, with over 51% of feed producers incorporating enzyme formulations in 2024. Meanwhile, developing regions show rapid growth rates, with a projected 33% increase in enzyme additive usage over the next three years.

• Growth in Probiotic Feed Solutions: Probiotic feed additives have gained significant traction, with usage in livestock feed increasing by 31% since 2021. Probiotics contribute to improved gut health and immunity, reducing antibiotic dependency by nearly 20%. North America has seen the most adoption in probiotic feed additives, with 47% of livestock farms incorporating them by 2024. Asia-Pacific is rapidly catching up, with usage expected to grow by over 28% in the coming two years due to rising livestock production demands.

• Digital Integration and AI-driven Formulation: AI and IoT integration in feed additive formulation is emerging as a key trend, improving nutrient efficiency by up to 14% compared to manual formulations. By 2027, over 40% of large-scale feed producers are expected to adopt AI-enabled systems for feed optimization. Europe leads in innovation intensity, with 35% of feed additive manufacturers integrating digital formulation platforms, while Asia-Pacific leads in volume adoption with over 48% of enterprises implementing these technologies.

The Feed Additives Market is segmented across type, application, and end-user categories, reflecting evolving industry needs and technological adoption. By type, enzyme-based and probiotic additives dominate, with significant growth in specialty acid and amino acid additives. Applications are diverse, ranging from poultry and swine nutrition to aquaculture and ruminants, driven by precision feeding demands. Poultry feed applications account for the largest share due to high production volumes and efficiency requirements. End-user segmentation shows commercial livestock producers leading adoption, with increasing interest from aquaculture farms and integrated farming operations. Regional consumption trends highlight Asia-Pacific as a growth leader, while Europe focuses heavily on sustainable and regulatory-compliant feed additive solutions.

Enzyme-based feed additives lead the market, accounting for 38% of total adoption, due to their ability to enhance feed digestibility and reduce waste. Probiotic additives hold 27% of the market, while amino acid and organic acid additives represent 22% collectively. Enzyme additives are favored for poultry and swine feed, improving feed conversion ratios by up to 16%. Probiotics are gaining momentum, particularly in aquaculture, for their ability to improve gut health. Amino acids are increasingly utilized to meet specific nutrient requirements, and organic acids are valued for their preservative and digestive benefits. The remaining 13% is contributed by niche additive types such as antioxidants and phytogenics, which are used in specialized feed formulations.

Poultry feed applications dominate, accounting for 42% of the market, due to the sector’s high global production volumes and demand for optimized growth performance. Swine feed applications follow with 25%, driven by intensive pig farming practices. Aquaculture feed applications account for 18%, showing the fastest growth due to rising seafood demand and sustainable aquaculture practices. Ruminant feed applications account for the remaining 15%, supported by targeted additive integration to improve forage efficiency. In aquaculture, probiotic and enzyme additives have seen adoption increase by 29% in recent years, driven by efficiency and sustainability demands.

Commercial livestock producers are the leading end-user segment, accounting for 46% of adoption, due to their scale and capacity for investment in advanced feed additives. Aquaculture farms follow with 28%, driven by demand for high-quality seafood and sustainable farming practices. Integrated farming operations account for 16%, leveraging additive solutions to optimize cross-sector feed efficiency. Smallholder farms constitute the remaining 10%, with growth potential driven by cost-effective additive solutions. Poultry producers are particularly active adopters, with over 50% implementing enzyme and probiotic additives by 2024. Aquaculture adoption rates have increased by 31% over the last three years.

Asia-Pacific accounted for the largest market share at 39% in 2024, however, South America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

In 2024, Asia-Pacific’s feed additives market exceeded 17,300 kilotons in volume, supported by production in China (8,200 kilotons) and India (4,100 kilotons). South America’s volume reached 3,800 kilotons in 2024, with Brazil contributing 2,400 kilotons and Argentina 900 kilotons. North America accounted for 26% of the market in 2024, while Europe represented 22%. The Middle East & Africa held a smaller share of 5%, but with strong growth potential due to increasing livestock production. Asia-Pacific benefits from high manufacturing capacity, over USD 1.2 billion in R&D investment in feed additive facilities, and rapid technology adoption, with over 48% of farms implementing precision feeding by 2024. South America’s growth is underpinned by government incentives and expansion of aquaculture and poultry farming, with over 35% of farms adopting enzyme-based additives.

North America accounts for 26% of the Feed Additives Market, driven primarily by the poultry, swine, and dairy sectors. The U.S. leads adoption with over 42% of livestock producers integrating enzyme-based and probiotic additives by 2024. Technological advancements such as AI-enabled feed formulation and IoT monitoring systems are transforming livestock nutrition. Regulatory support, including nutrient management programs and sustainable farming incentives, is driving innovation. Companies like Cargill Inc. are actively developing precision nutrition platforms that optimize additive efficiency, reduce waste, and improve animal health outcomes. Regional consumer behavior favors high enterprise adoption of technologically advanced feed solutions, with a preference for verified additive performance and sustainable sourcing. In North America, over 54% of feed producers have integrated digital monitoring into their operations to enhance quality control and traceability, making the region a leader in intelligent feed additive integration.

Europe accounts for 22% of the Feed Additives Market, with Germany, France, and the UK leading in consumption and innovation. Regulatory bodies such as the European Food Safety Authority have set stringent additive safety and environmental guidelines, fostering adoption of sustainable feed additives. Sustainability initiatives drive demand for enzyme-based, probiotic, and organic acid additives, which now constitute over 60% of European feed formulations. Emerging technologies like microbiome-targeted additives are gaining traction. Companies such as Evonik Industries AG have invested in R&D to deliver sustainable additive solutions that improve nutrient utilization and reduce environmental impact. Regional consumer behavior emphasizes explainable feed additives that comply with transparency regulations, leading to higher adoption of certified additive products. In 2024, over 48% of feed producers in Europe incorporated enzyme-based solutions to meet regulatory and environmental benchmarks.

Asia-Pacific holds the largest share of the Feed Additives Market at 39% in 2024, driven by China, India, and Japan. China alone accounted for over 8,200 kilotons of feed additive production in 2024, while India contributed 4,100 kilotons. Top-consuming countries are expanding production infrastructure, with investments exceeding USD 1.2 billion in modern feed additive manufacturing. Technological advancements, including AI-driven feed formulation and microbiome-based solutions, are concentrated in innovation hubs such as Jiangsu and Shandong. Local players like New Hope Liuhe are enhancing production capacity while integrating sustainable additives to meet demand. Consumer behavior in Asia-Pacific shows a preference for precision nutrition, with over 48% of large-scale farms adopting advanced additive solutions, and 52% integrating enzyme and probiotic blends to improve livestock performance and sustainability.

South America accounted for 9% of the Feed Additives Market in 2024, with Brazil and Argentina leading consumption. Brazil contributed 2,400 kilotons, supported by expanding poultry and aquaculture sectors, while Argentina accounted for 900 kilotons. Government incentives for sustainable farming and expanded aquaculture projects have boosted additive adoption. Infrastructure developments in processing and feed manufacturing are enhancing productivity, with enzyme-based additives now integrated into over 35% of feed formulations. Local players such as BRF S.A. are pioneering additive-enhanced poultry feed solutions, improving feed conversion ratios by 11%. Consumer behavior in South America is increasingly tied to sustainability and efficiency, with a growing number of producers seeking advanced additive solutions that enhance productivity while meeting regulatory requirements.

Middle East & Africa accounted for 5% of the Feed Additives Market in 2024, driven by growing demand in poultry and dairy production. Major growth markets include the UAE and South Africa, with increasing investments in livestock infrastructure. Technological modernization, including IoT-enabled feed management and enzyme additive integration, is expanding rapidly. Trade partnerships and government initiatives supporting agricultural innovation are boosting adoption. Local companies are introducing tailored additive solutions to meet environmental and nutritional needs. Consumer behavior in this region reflects a strong preference for additives that deliver proven productivity improvements, with over 38% of farms integrating enzyme and probiotic additives by 2024 to optimize livestock growth and operational efficiency.

China: 21% market share – high production capacity and extensive investment in modern feed additive manufacturing.

United States: 16% market share – strong end-user demand for precision nutrition and technological integration in livestock feed solutions.

The Feed Additives Market is highly competitive and moderately fragmented, with over 120 active global players vying for market share. The top five companies—Cargill Inc., Archer Daniels Midland Company, Evonik Industries AG, Novus International, and BASF SE—collectively hold approximately 58% of the market, indicating significant concentration among leading players. Strategic initiatives such as mergers, acquisitions, partnerships, and product innovations are shaping competitive dynamics. For example, in 2024, Evonik Industries AG launched a proprietary enzyme-based feed additive line to improve nutrient absorption efficiency by up to 15%. Cargill Inc. has expanded its portfolio through partnerships with AI-driven feed formulation startups, enhancing precision nutrition solutions for livestock. Novus International focuses heavily on probiotic and amino acid product innovation, with over 22% of its R&D budget allocated to sustainable feed solutions. Competition is also driven by emerging players in Asia-Pacific and South America, where localized solutions tailored to regional farming practices are gaining traction. Innovation trends such as microbiome-targeted additives, AI-based feed formulation, and sustainable ingredient sourcing are redefining competitive advantage, making R&D investment a critical driver of success in this evolving market.

Novus International

BASF SE

Alltech Inc.

Nutreco N.V.

DSM Nutritional Products

Chr. Hansen Holding A/S

Kemin Industries Inc.

The Feed Additives Market is experiencing transformative shifts driven by technological innovations that enhance animal health, feed efficiency, and sustainability. Artificial Intelligence (AI) and machine learning are revolutionizing feed formulation by enabling real-time analysis of animal health and nutritional needs. These technologies facilitate the development of customized feeding strategies, optimizing feed intake and improving livestock productivity.

Plant-based feed additives, known as phytogenics, are gaining popularity due to their natural origin and health benefits. These additives are used to enhance gut health, improve digestion, and boost immunity in animals, aligning with the growing demand for sustainable and antibiotic-free feed solutions. The application of enzymes in animal feed is enhancing nutrient digestibility and feed efficiency. Enzyme additives break down complex feed components, making nutrients more accessible to animals, which is particularly beneficial in poultry and swine diets.

Incorporating probiotics and prebiotics into animal feed is improving gut health and overall immunity. These additives support the growth of beneficial gut bacteria, leading to better digestion and nutrient absorption, thereby enhancing animal performance. These technological innovations are not only improving the efficiency and sustainability of animal farming but are also aligning with the increasing consumer demand for ethically produced and healthy animal products.

In 2024, Denmark allocated 518 million Danish crowns (approximately $74 million) to support farmers in adopting a feed additive aimed at reducing methane emissions from cattle by up to 30%. This initiative aligns with Denmark's goal to cut overall emissions by 70% by 2030 compared to 1990 levels.

In 2024, the global feed additives industry introduced over 290 new products, focusing on sustainability, efficiency, and animal-specific performance enhancement. Notably, Evonik launched a precision-release methionine product that improved digestibility by 17% in broilers, adopted by over 3,000 commercial poultry farms.

In 2024, the phytogenic feed additives market reached a size of $1.12 billion, up from $1.04 billion in 2023. This growth reflects the increasing demand for natural and sustainable feed solutions in the industry.

In 2024, the United States Feed Additives Market was valued at $6.46 billion and is expected to reach $8.57 billion by 2029, reflecting a growing demand for high-quality animal products driven by health-conscious consumers.

The Feed Additives Market Report provides a comprehensive analysis of the global feed additives industry, encompassing various market segments, geographic regions, applications, technologies, and industry focus areas. The report delves into the types of feed additives, including amino acids, vitamins, enzymes, probiotics, prebiotics, and phytogenics, highlighting their roles in enhancing animal nutrition and health.

Geographically, the report examines key regions such as North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, offering insights into regional market dynamics, growth drivers, and challenges. It also explores the adoption of emerging technologies like artificial intelligence in feed formulation, precision feeding systems, and the development of sustainable and natural feed additives.

The report further investigates the applications of feed additives across various livestock categories, including poultry, swine, cattle, and aquaculture, assessing the specific needs and trends within each segment. Additionally, it addresses the regulatory landscape influencing the feed additives market, focusing on policies promoting animal health, food safety, and environmental sustainability.

By providing detailed insights into market trends, technological advancements, and regional developments, the Feed Additives Market Report serves as a valuable resource for industry professionals, enabling informed decision-making and strategic planning in the evolving feed additives sector.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 44478.8 Million |

|

Market Revenue in 2032 |

USD 67745.1 Million |

|

CAGR (2025 - 2032) |

5.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cargill Inc., Archer Daniels Midland Company, Evonik Industries AG, Novus International, BASF SE, Alltech Inc., Nutreco N.V., DSM Nutritional Products, Chr. Hansen Holding A/S, Kemin Industries Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |