Reports

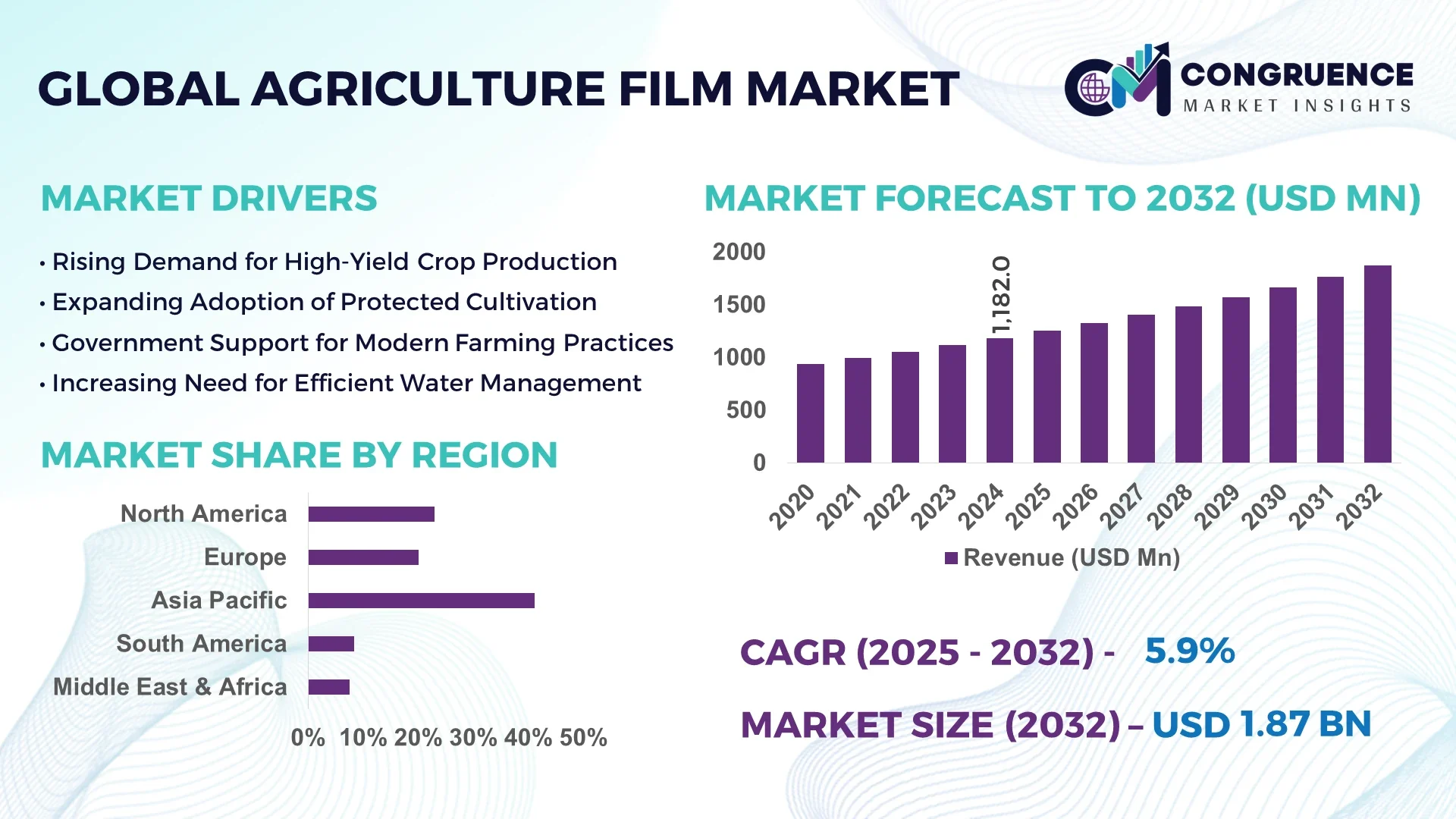

The Global Agriculture Film Market was valued at USD 1,182.0 Million in 2024 and is anticipated to reach a value of USD 1,875.4 Million by 2032 expanding at a CAGR of 5.94% between 2025 and 2032.

China stands as the leading country in the Agriculture Film Market, supported by its robust manufacturing infrastructure, extensive R&D investments in polymer science, and high-volume production capacities. The country hosts over 300 specialized facilities for film production, driven by government-led initiatives promoting sustainable agricultural practices. Advanced multi-layer extrusion technologies and significant adoption of biodegradable films are also accelerating product innovation across various agricultural applications such as greenhouse coverage, mulch films, and silage wraps.

The Agriculture Film Market plays a critical role in enhancing agricultural productivity, protecting crops, and optimizing water usage. This market caters to key sectors including horticulture, floriculture, and silage preservation, with mulch films accounting for a significant share due to their soil-conditioning benefits. Technological innovations such as UV-stabilized and photo-selective films are improving crop yield and lifecycle efficiency. Furthermore, biodegradable films are gaining traction amidst rising environmental regulations across the EU and North America. Government subsidies and eco-friendly mandates in countries like Germany, the U.S., and Japan are fostering market adoption of sustainable film variants. Regionally, Asia-Pacific dominates consumption due to intensive farming practices, while Latin America is emerging due to expanding greenhouse cultivation. Future trends suggest an increasing preference for high-performance films with nano-layered structures, smart coatings, and enhanced recyclability, aligning with global climate resilience goals and precision agriculture techniques. The industry outlook remains optimistic, bolstered by growing investments in smart agriculture and advanced polymer development.

Artificial Intelligence (AI) is significantly reshaping the Agriculture Film Market by driving smarter production systems, optimizing supply chains, and enhancing product performance analytics. AI-driven predictive modeling tools are now being used to assess the longevity and degradation behavior of agriculture films under varying environmental conditions, reducing product failure rates and improving quality control processes. For manufacturers, AI-integrated extrusion equipment equipped with machine vision systems can identify micro-defects in film rolls in real time, reducing material wastage by up to 20%. This not only improves operational efficiency but also enhances sustainability performance—a critical factor for industry compliance and ESG reporting.

In logistics and inventory management, AI-enabled demand forecasting is helping suppliers align film production volumes with seasonal agricultural cycles, thereby reducing storage costs and minimizing excess inventory. Additionally, AI-powered analytics are transforming the customer feedback loop, enabling faster customization of films based on geographic climate data, soil condition variability, and UV exposure requirements. In research and development, machine learning algorithms are being used to simulate new polymer blends that offer superior mechanical strength, biodegradability, and light diffusion characteristics—features that are increasingly in demand from modern farming operations.

“In 2024, a leading polymer R&D consortium in South Korea implemented an AI-powered film design simulator that reduced the development time for high-transmittance greenhouse films by 35%, while enhancing their UV resistance by 28% compared to traditional variants.”

The Agriculture Film Market is characterized by evolving dynamics influenced by technology advancements, sustainability mandates, and shifting agricultural practices. Increasing global emphasis on food security and resource optimization is fueling demand for multifunctional films that enhance productivity. Polymer science innovations are enabling lighter, more durable, and environmentally friendly films. Furthermore, climatic uncertainty is accelerating the deployment of protective films in greenhouses and open-field farming. Meanwhile, industry players are diversifying their offerings to include recyclable and bio-based solutions, responding to regulatory pressure and consumer demand. These developments are fostering a competitive landscape marked by rapid product innovation, strategic collaborations, and regional diversification in manufacturing and distribution.

Innovative applications of agriculture films are propelling market growth, especially with films engineered for specific functions such as light diffusion, thermal insulation, and pest control. For example, the use of nano-additives and multilayer structures allows for precise control over light transmission and moisture retention, enhancing crop yields significantly. Advanced mulch films embedded with degradable polymers are increasingly used across horticultural zones to suppress weed growth and conserve soil moisture. These new-generation films, produced through co-extrusion and AI-assisted film mapping, are also contributing to more uniform crop growth and reduced dependency on chemical inputs. Adoption has risen particularly in regions with water scarcity and high solar exposure.

The Agriculture Film Market faces notable constraints due to environmental regulations related to plastic usage and disposal. Traditional polyethylene-based films, while cost-effective, pose recycling challenges and contribute to agricultural plastic waste accumulation. In countries with stringent environmental policies like Germany and France, non-compliant films are restricted, increasing the burden on manufacturers to innovate. Additionally, farmers in emerging markets often lack access to organized collection and recycling systems, resulting in improper disposal and soil contamination. These factors are compelling stakeholders to invest in sustainable alternatives, but the higher costs and lower durability of biodegradable films remain barriers to widespread adoption.

The growing adoption of controlled-environment agriculture presents a lucrative opportunity for the Agriculture Film Market. Greenhouse installations have surged globally, especially in China, Spain, and Mexico, where year-round cultivation is essential. These systems rely heavily on specialty films for temperature regulation, light diffusion, and humidity control. UV-blocking and thermally insulating films are enabling farmers to optimize crop cycles and reduce energy consumption. As governments push for food security and climate-adaptive farming, subsidies and grants for greenhouse projects are expanding. This trend is expected to accelerate demand for advanced agricultural films, including smart films with embedded sensors for real-time condition monitoring.

While biodegradable films are a promising alternative to conventional plastics, they face limitations in high-temperature and high-UV agricultural environments. Many such films degrade prematurely under extreme conditions, reducing their effectiveness in regions like the Middle East and sub-Saharan Africa. Moreover, their performance varies significantly depending on soil composition, irrigation practices, and microbial activity. This inconsistency creates hesitancy among large-scale farmers who prioritize predictable yield outcomes. Additionally, the cost of developing high-performance biodegradable films that match the strength and flexibility of traditional materials remains high, further constraining market scalability in budget-sensitive regions.

Surge in Biodegradable Mulch Film Usage: Farmers across Europe and North America are increasingly switching to biodegradable mulch films due to stricter regulations on plastic waste. In 2025, biodegradable variants accounted for over 18% of mulch film installations in the EU, driven by national subsidies and improved compostability performance. These films are also being used in organic farming systems to comply with sustainability certifications, significantly altering product development strategies.

Advancements in Light-Diffusing Films: A growing trend involves using light-diffusing agriculture films that scatter sunlight evenly across crop surfaces, enhancing photosynthesis. In regions with high solar radiation, such as Spain and Australia, these films have improved crop yield by up to 12% in controlled trials. New polymer formulations allow better customization for specific crops like tomatoes and cucumbers, supporting increased adoption.

Integration of Smart Sensor-Compatible Films: Films designed to work with embedded sensors are entering the market, particularly for high-tech greenhouse applications. These smart agriculture films enable real-time monitoring of temperature, humidity, and UV exposure, helping farmers adjust growing conditions instantly. In pilot projects across Israel and the Netherlands, this technology has led to a 15–20% improvement in overall crop efficiency.

Rising Demand for Multilayer Co-Extruded Films: Multilayer co-extrusion technology is gaining momentum as it enables the production of films with tailored functionalities such as anti-drip, infrared-blocking, and antimicrobial properties. Demand for these high-performance films is increasing, especially in Asia-Pacific, where intensive agriculture and climatic variability require robust protective solutions.

The Agriculture Film Market is segmented based on product type, application, and end-user insights, each offering unique growth avenues and value propositions. Segmentation by type includes mulch films, greenhouse films, silage films, and others. Among these, mulch films and greenhouse films lead the market due to their broad adoption in intensive farming and controlled-environment agriculture, respectively. Application-based segmentation reveals widespread usage across crop production, horticulture, floriculture, and silage preservation, with crop production being the most dominant. End-user segmentation covers commercial farming enterprises, agri-cooperatives, and research institutions. Commercial farming leads in terms of volume demand and product innovation adoption, while research entities are exploring niche film applications involving biodegradable and sensor-compatible variants. Each segment reflects evolving agricultural practices and regional preferences, shaping the overall demand for high-performance and sustainable agriculture films.

The Agriculture Film Market encompasses several key product types, including mulch films, greenhouse films, silage films, and specialty films. Among these, mulch films are the dominant segment due to their widespread use in weed suppression, moisture retention, and temperature control. They are extensively adopted across open-field cultivation zones in Asia and North America. The consistent demand for food crops and vegetable production continues to fuel their use across large-scale farming operations.

Greenhouse films represent the fastest-growing segment, driven by the global shift toward protected cultivation and climate-resilient farming. These films are particularly valuable in regions with temperature extremes or inconsistent rainfall, such as the Mediterranean and parts of Latin America. Technological enhancements like UV resistance, infrared filtering, and light diffusion are adding further value to greenhouse films, making them indispensable for high-yield crop cultivation.

Other types, including silage films and fumigation films, serve specific agricultural purposes. Silage films are integral to livestock farming and feed preservation in countries with large dairy and meat industries. Though niche, specialty films—such as photodegradable and biodegradable variants—are gaining interest due to environmental concerns and regulatory pressure.

Agriculture films are applied across various agricultural functions, including crop production, horticulture, floriculture, silage preservation, and soil solarization. Among these, crop production is the leading application, driven by the global demand for staple grains, vegetables, and fruits. These films help optimize soil temperature, reduce water loss, and suppress weed growth, which significantly improves productivity and cost-efficiency for farmers.

Floriculture is the fastest-growing application, propelled by rising demand for ornamental plants, flowers, and decorative greenery in urban and export markets. Controlled cultivation environments, particularly using greenhouse films, enable consistent flowering cycles and quality enhancement, making them highly beneficial for floriculture businesses.

Other applications such as horticulture and soil solarization also play critical roles in niche areas. Horticulture benefits from light-diffusing films that enhance fruit color and size, while solarization films are used for pest and disease management without chemical inputs. Silage preservation films support livestock farming by maintaining the nutritional quality of stored feed under variable weather conditions, particularly in temperate zones.

End-users in the Agriculture Film Market include commercial farming enterprises, agricultural cooperatives, research institutions, and government-supported agricultural projects. Commercial farms are the leading end-users, owing to their scale of operations, consistent investment in advanced agricultural technologies, and need for high-efficiency products. These enterprises actively adopt multilayered and specialized films to boost yield and reduce labor and water usage.

Government-supported projects are emerging as the fastest-growing end-user category. National initiatives aimed at improving food security, climate adaptability, and rural development are resulting in large-scale greenhouse and drip irrigation projects that heavily rely on agriculture films. These programs are especially active in countries like India, Mexico, and Egypt, where policy-driven subsidies facilitate access to advanced agricultural materials.

Agricultural cooperatives and research institutions also contribute to the market landscape. Cooperatives often promote the use of biodegradable and recyclable films among smallholder farmers, while research institutions are experimenting with innovative film compositions and smart functionalities, influencing future product development and regulatory standards.

Asia-Pacific accounted for the largest market share at 41.2% in 2024; however, Latin America is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

The Agriculture Film Market is being shaped by regional shifts in cultivation practices, policy incentives, and environmental mandates. Asia-Pacific dominates due to its extensive farming operations, expanding greenhouse infrastructure, and strong domestic manufacturing of plastic and polymer-based products. Meanwhile, Latin America's rapid expansion is fueled by government-backed agricultural modernization programs and increased adoption of greenhouse farming technologies. Each region’s growth trajectory is also supported by regional climate conditions, land use patterns, and technology transfer from leading film producers. North America and Europe continue to show steady demand, bolstered by sustainable farming practices and stricter regulatory frameworks. The Middle East & Africa region, while smaller in share, is experiencing gradual growth due to rising food security investments and climate-adaptive farming initiatives.

North America held approximately 21.5% of the global Agriculture Film Market in 2024, led by the United States and Canada. Mechanized farming, high-value crop cultivation, and stringent food safety norms are key demand drivers. The U.S. Department of Agriculture has introduced several grants promoting sustainable plastic use and recycling in commercial farming, fostering demand for biodegradable and recyclable films. Increasing deployment of advanced silage films in livestock operations across the Midwest and Pacific Northwest is notable. The region is also witnessing digitization of agriculture, with precision farming integrating sensor-compatible films and UV-reflective materials. Regulatory efforts such as limiting single-use plastics have prompted producers to develop multi-season films with longer durability, aligning with environmental goals.

Europe accounted for 23.8% of the Agriculture Film Market in 2024, with Germany, France, and the Netherlands leading demand. Strict EU environmental directives and the Green Deal’s sustainability targets have pushed the market toward biodegradable and compostable film variants. Regional authorities are actively promoting circular economy policies that impact product design and end-of-life film disposal. Germany remains at the forefront of technological integration, with widespread use of light-diffusing greenhouse films and infrared-blocking mulch films. France and the UK are adopting sensor-integrated films as part of smart greenhouse projects. The EU’s CAP (Common Agricultural Policy) continues to provide financial incentives for eco-compliant technologies, further accelerating adoption across multiple agricultural sub-sectors.

Asia-Pacific is the largest and most dynamic Agriculture Film Market, with a market volume share of 41.2% in 2024. China, India, and Japan dominate consumption due to large-scale crop cultivation, favorable government subsidies, and strong local production capacities. China’s leadership in polymer extrusion technology and India’s subsidy-driven greenhouse farming programs are significantly influencing product innovation and accessibility. The region also benefits from a rapidly modernizing agri-infrastructure with expansion of cold chains and irrigation systems. Japan’s R&D in photodegradable and heat-insulating films is setting a global benchmark. Asia-Pacific’s agriculture technology hubs, particularly in Shandong (China) and Maharashtra (India), are developing AI-integrated films for high-efficiency farming, further reinforcing regional dominance.

In South America, Brazil and Argentina are the key contributors to the Agriculture Film Market, which held a 9.6% share in 2024. Brazil’s focus on increasing productivity in soybeans, corn, and sugarcane has led to rising usage of mulch and silage films. Agricultural expansion into previously uncultivated areas is increasing demand for UV-resistant and water-conserving films. Argentina is experiencing steady uptake in greenhouse cultivation, especially for vegetables and fruits aimed at export markets. The MERCOSUR trade bloc has facilitated easier cross-border trade of agricultural technologies, including plastic films. Government programs supporting rural infrastructure and farm modernization continue to encourage local and foreign investments in film production and distribution facilities.

The Middle East & Africa held 3.9% of the Agriculture Film Market in 2024, with growth fueled by increasing adoption of climate-resilient agricultural solutions. The UAE and South Africa are key countries investing in modern greenhouse technologies and water-efficient farming. Regional demand is rising for high-barrier films that can withstand high solar radiation and arid conditions. Governments across the region are pushing forward food security agendas with subsidies for protected farming systems that utilize high-performance agricultural films. Innovations include heat-shielding films and UV-resistant biodegradable variants developed to address extreme climates. Strategic trade agreements with Asian polymer producers are enabling more affordable imports of quality films, further stimulating adoption in developing agricultural zones.

China – 27.3% Market Share

High production capacity and investment in advanced multilayer extrusion technologies.

India – 13.1% Market Share

Strong end-user demand from government-subsidized greenhouse and drip irrigation farming initiatives.

The Agriculture Film Market features a competitive landscape with over 150 active manufacturers and solution providers operating globally, ranging from large polymer processing companies to specialized agricultural input firms. Market participants compete on innovation, product durability, sustainability, and regional customization. Key players have adopted strategic partnerships, particularly with agritech companies and raw material suppliers, to strengthen supply chain resilience and accelerate eco-friendly product innovation. Mergers and acquisitions are also reshaping the industry, especially in Europe and Asia-Pacific, where consolidation is improving production capabilities and expanding geographic reach.

Innovation remains central to competition, with companies investing in R&D for multilayer co-extrusion, biodegradable composites, and sensor-compatible films. Over 30% of global players have launched new film types in the last two years, often targeting niche applications such as UV-selective coverage or thermally insulated greenhouse films. Additionally, digital integration and the use of AI in manufacturing processes are helping firms optimize production efficiency, improve product consistency, and reduce waste. Competitive intensity is highest in high-demand regions such as China, the U.S., and Germany, where regulatory frameworks and consumer preferences continuously shape market strategies.

Berry Global Inc.

RKW Group

Armando Alvarez Group

BASF SE

Trioplast Industrier AB

Ab Rani Plast Oy

Plastika Kritis S.A.

Coveris Holdings S.A.

Kuraray Co., Ltd.

Dow Inc.

Novamont S.p.A.

POLIFILM Group

Ginegar Plastic Products Ltd.

BioBag International AS

The Agriculture Film Market is being transformed by a wave of technological advancements aimed at improving durability, sustainability, and performance under varying climate conditions. One of the most impactful innovations is multilayer co-extrusion technology, enabling manufacturers to combine multiple polymer layers in a single film structure. These films provide targeted functionalities such as UV blocking, thermal insulation, light diffusion, and anti-drip effects, thereby enhancing crop quality and yield efficiency.

The integration of nanotechnology in film production is also advancing, with nano-additives improving film strength, flexibility, and resistance to environmental degradation. Moreover, photodegradable and biodegradable polymers, such as PLA and PBAT-based composites, are gaining traction as eco-friendly alternatives to traditional polyethylene. In 2024, over 20% of new product launches in the segment included bio-based or biodegradable materials.

Another significant trend is the development of sensor-compatible films, designed for use in smart farming systems. These films enable real-time monitoring of greenhouse conditions through embedded or adjacent IoT sensors, improving crop management efficiency. Digital twin simulations and AI-based modeling are now used to design and test film performance before full-scale production, accelerating innovation cycles and reducing trial-and-error costs. These technologies not only meet sustainability mandates but also align with precision agriculture practices adopted across developed and emerging economies.

• In January 2024, Trioplast Industrier AB introduced a new range of silage films containing 50% post-consumer recycled content, improving circularity without compromising film strength or elasticity under high-pressure wrapping conditions.

• In March 2024, Ginegar Plastic Products Ltd. launched a photo-selective greenhouse film optimized for high-UV regions, increasing crop productivity by 15% in pilot studies conducted in Southern Spain and Israel.

• In October 2023, Kuraray Co., Ltd. expanded its biodegradable polymer film line with new PBAT-enhanced mulch films that deliver higher tensile strength and predictable soil decomposition within 120 days under field conditions.

• In December 2023, Berry Global Inc. partnered with a Southeast Asian agri-cooperative to roll out AI-monitored greenhouse films embedded with QR-coded traceability features for improved transparency and crop cycle planning.

The Agriculture Film Market Report offers a comprehensive analysis of the global industry landscape, covering multiple dimensions such as product types, end-user segments, applications, technology trends, and geographic distribution. The report segments the market into mulch films, greenhouse films, silage films, and specialty films, analyzing performance attributes and material innovations across each category.

Applications reviewed include crop production, floriculture, horticulture, silage preservation, and soil solarization, with tailored insights into how each use-case influences film design and functionality. End-user analysis highlights commercial farms, government-led farming initiatives, cooperatives, and research institutions, each contributing uniquely to market demand.

Geographically, the report evaluates regional dynamics across Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, providing in-depth coverage of market leaders such as China, India, the U.S., and Brazil. Technological coverage includes the latest advancements in biodegradable materials, multilayer extrusion, nano-enhanced films, and smart agriculture integration.

The report also identifies niche segments gaining traction, including sensor-compatible films, photo-selective variants, and films developed for extreme climatic conditions. This holistic approach makes the report a critical resource for decision-makers, investors, and stakeholders seeking actionable insights in a rapidly evolving agricultural input industry.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 1,182.0 Million |

| Market Revenue (2032) | USD 1,875.4 Million |

| CAGR (2025–2032) | 5.94% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Berry Global Inc., RKW Group, Armando Alvarez Group, BASF SE, Trioplast Industrier AB, Ab Rani Plast Oy, Plastika Kritis S.A., Coveris Holdings S.A., Kuraray Co., Ltd., Dow Inc., Novamont S.p.A., POLIFILM Group, Ginegar Plastic Products Ltd., BioBag International AS |

| Customization & Pricing | Available on Request (10% Customization is Free) |