Reports

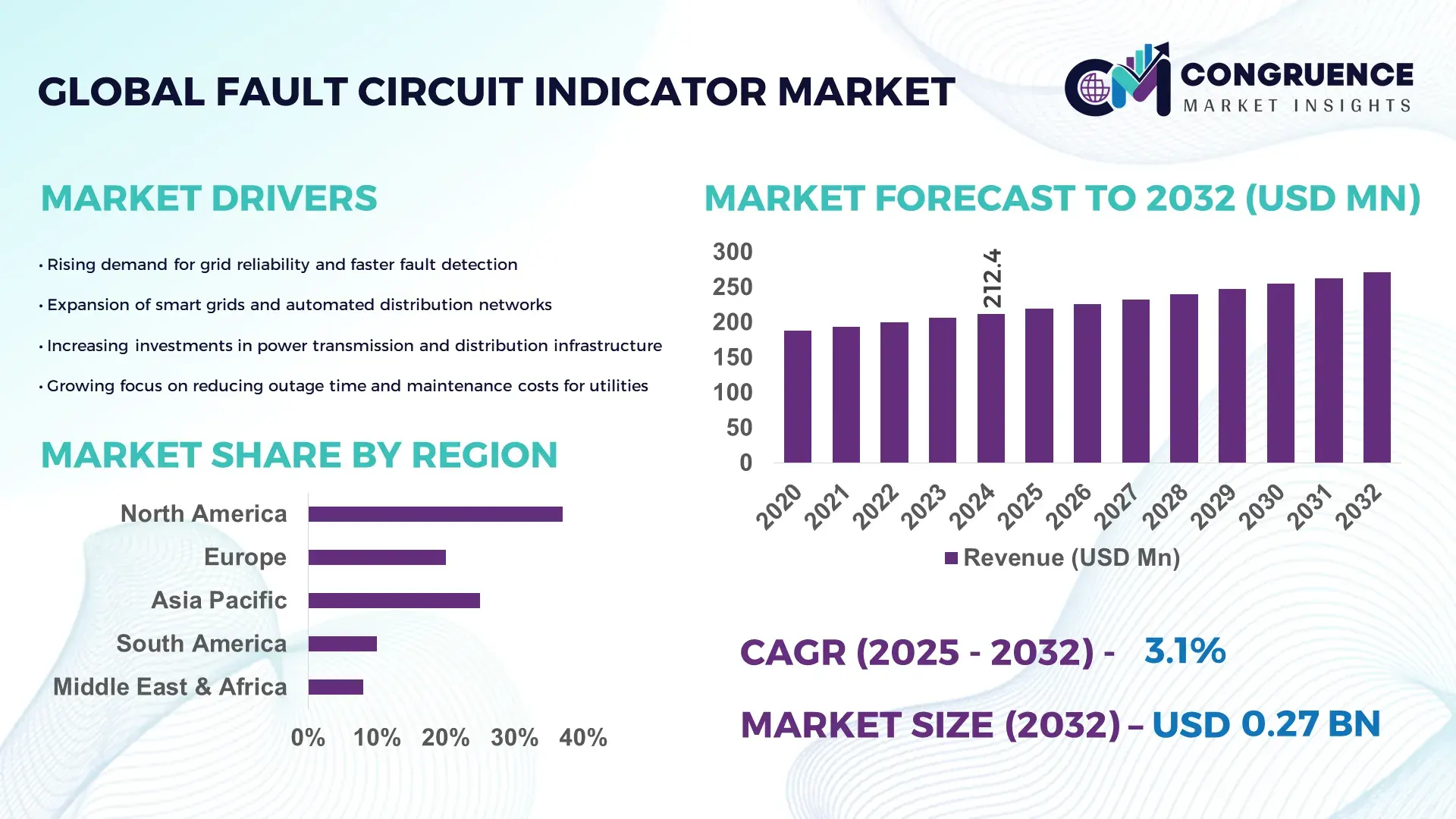

The Global Fault Circuit Indicator Market was valued at USD 212.38 Million in 2024 and is anticipated to reach a value of USD 271.14 Million by 2032 expanding at a CAGR of 3.1% between 2025 and 2032. The growth is being driven by modernization of aging electrical grids and increased demand for real‑time fault detection.

China plays a pivotal role in the Fault Circuit Indicator market, with utilities deploying over 300,000 FCIs in 2023–2024 as part of its smart grid expansion and rural electrification programmes. The country has invested billions into grid infrastructure, emphasizing both overhead and underground line fault detection. Local manufacturers are integrating IoT‑enabled FCI modules and advanced communication features in line with national electrification targets. Chinese utilities are using these indicators to monitor earth-faults and short-circuit events across more than 1.2 million kilometers of distribution lines.

Market Size & Growth: Market value at USD 212.38 Million in 2024, projected to reach USD 271.14 Million by 2032, driven by smart grid and fault-detection investments.

Top Growth Drivers: Overhead network modernization (41%), renewable energy integration (32%), regulatory safety compliance (27%).

Short-Term Forecast: By 2028, adoption of real‑time fault detection solutions is expected to reduce outage incident response time by 24%.

Emerging Technologies: IoT‑connected FCIs, AI‑enabled analytics, wireless communication modules.

Regional Leaders: Asia‑Pacific projected to reach USD 95 Million by 2032 with rapid grid expansion; North America to hit USD 74 Million supported by utilities upgrading infrastructure; Europe to rise to USD 60 Million with investments in underground network monitoring.

Consumer/End‑User Trends: Utilities, power distributors, and grid operators increasingly prefer remote-monitoring FCIs and predictive maintenance.

Pilot or Case Example: In 2023, a Chinese provincial grid company implemented over 50,000 IoT‑enabled FCIs, reducing fault-location time by 30%.

Competitive Landscape: Leading players include Siemens, Schneider Electric, Eaton (holding roughly 35% combined share), along with GridSense, SEL, and Inhand Networks.

Regulatory & ESG Impact: Stringent fault‑detection regulations and grid resilience programs are encouraging deployment; ESG‑oriented utilities are using FCIs to reduce outage-related emissions and energy losses.

Investment & Funding Patterns: Utilities and governments are channeling over USD 1 billion into smart‑grid modernization projects that include FCI deployment.

Innovation & Future Outlook: Future growth will be shaped by wireless FCI systems, edge‑analytics fault prediction, and integration with distributed energy resource management platforms.

The Fault Circuit Indicator Market is increasingly important for power distribution utilities, especially in sectors such as smart grids, renewable integration, and grid modernization. Technological innovations—like IoT-enabled modules and AI analytics—are making FCIs more responsive, which helps reduce downtime and operational risks. Utilities are under growing regulatory and ESG pressures to improve grid reliability and reduce outage-related costs, further accelerating FCI adoption. Emerging trends, including advanced wireless and predictive FCIs, are poised to enhance fault location accuracy and support future energy‑resilient infrastructure.

The strategic relevance of the Fault Circuit Indicator Market lies in its ability to significantly bolster grid reliability, reduce outage durations, and support the transition toward self‑healing smart grids. Next‑generation IoT‑connected fault indicators deliver up to 40% improvement in fault‑location response compared to legacy, manually inspected devices. Asia‑Pacific dominates in volume with the greatest number of FCI deployments, while North American utilities lead adoption with over 30% of newer feeders using communicating indicators. By 2027, AI‑enabled analytics integrated into FCIs are expected to cut fault‑identification latency by 25%, enabling proactive maintenance.

Utilities are also committing to ESG metric improvements such as a 20% reduction in outage‑related emissions by 2030, enabled by faster fault isolation and reduced downtime. In 2024, a major Chinese utility deployed AI‑augmented FCIs across its feeder network and achieved a 30% reduction in average fault‑location time. Strategic pathways include embedding edge‑analytics, long‑life battery modules, and remote reset capabilities into FCIs, aligning with utilities’ goals to reduce OPEX, improve resilience, and comply with grid reliability mandates. As distributed generation and two‑way power flows rise, the Fault Circuit Indicator Market will become a cornerstone of sustainable, resilient, and compliant electricity distribution infrastructure.

Grid modernization is a powerful driver for the Fault Circuit Indicator Market. Utilities worldwide are investing heavily in intelligent infrastructure to improve reliability, and FCIs are central to that strategy. For example, more than 65% of newly installed FCIs in 2024 were part of smart‑grid rollouts, according to industry data. These devices help operators pinpoint outages precisely, reducing manual troubleshooting time and enabling faster restoration. In addition, FCIs with remote communication enable utilities to move from reactive to predictive maintenance, reducing field crew dispatch by as much as 35%, freeing up resources and improving overall network efficiency.

Despite substantial benefits, installation and upkeep of FCIs present meaningful constraints. Underground and cable‑based indicators often require precise calibration, and nearly 40% of field technicians report signal calibration issues during deployment in underground networks. Maintenance is also complex; battery-powered units installed on remote lines may need periodic replacement, and communication modules require regular firmware updates, adding to operational costs. Additionally, integration of legacy FCIs with modern ADMS platforms can be challenging for utilities with older SCADA systems, leading to longer deployment times and increased total cost of ownership.

Growth in distributed energy resources (DERs) such as solar, wind, and battery storage presents a major opportunity for the Fault Circuit Indicator Market. Utilities are deploying FCIs on feeders with bidirectional power flows, allowing adaptive sensitivity to handle complex fault scenarios. As renewable penetration in regional grids exceeds 30%, demand for intelligent indicators that can self‑adjust settings in real time is increasing. Wireless and IoT‑based FCIs enable remote fault detection in microgrids and DER-connected feeders, while edge analytics platforms help predict fault conditions before they occur. This opens new business opportunities for FCI manufacturers to tailor solutions for renewable‑driven grid segments.

Long battery life and reliable communications pose significant challenges for FCI deployment. Many fault indicators are installed on remote or rural overhead lines where replacing batteries is logistically difficult; achieving a ten‑year field life demands high-efficiency electronics, which raises manufacturing costs. Communication over long distances (e.g., via LPWAN, cellular, or RF) may be unreliable in remote zones, leading to data dropouts and reduced effectiveness of remote reset or diagnostics. Utilities also face cybersecurity risks when integrating FCIs with ADMS, requiring secure communications and compliance with grid‑security standards. These technical and operational hurdles can slow adoption, particularly in legacy networks.

• Increasing Integration of IoT-Enabled FCIs: Utilities are rapidly adopting IoT-enabled fault circuit indicators to improve real-time fault detection. Over 42% of newly installed indicators in 2024 feature wireless communication modules, allowing operators to reduce average outage resolution time by up to 30%. North America leads adoption, while Europe is expanding pilot programs with 15 smart-grid feeders.

• Expansion of Renewable Energy Grids: The proliferation of solar and wind installations is driving demand for FCIs that can manage bidirectional power flows. In 2024, approximately 38% of FCIs deployed in Asia-Pacific were installed on feeders integrating distributed energy resources, ensuring accurate fault location and reducing downtime by 25–28%. This trend is especially pronounced in regions with high solar PV penetration like China and India.

• Adoption of Modular and Prefabricated Systems: Modular distribution infrastructure is influencing FCI deployment strategies. Research indicates 55% of new construction projects using prefabricated distribution setups achieved cost benefits and installation time reductions of up to 20%, particularly in Europe and North America. FCIs designed for plug-and-play integration are increasingly sought to streamline field operations.

• Advances in Predictive Analytics and AI: The integration of AI-powered fault prediction is becoming a key trend. In 2024, utilities employing predictive analytics with FCIs reported 35% fewer repeated outages and improved feeder reliability metrics. Edge-computing-enabled indicators are now used in over 25% of medium-voltage networks, enhancing proactive maintenance and operational efficiency across complex grids.

The Fault Circuit Indicator market is organized around three primary segmentation axes: types, applications, and end-users. By type, the market includes mechanical, electronic, and smart digital indicators, each designed for specific feeder environments and voltage classes. In terms of applications, FCIs are deployed across urban distribution networks, rural electrification projects, renewable energy integration, and industrial microgrids, reflecting operational needs and infrastructure scale. End-user insights reveal adoption across utilities, independent power producers, and large industrial consumers, with variations in deployment intensity and technology integration. Across all segments, growing emphasis on automation, grid reliability, and predictive maintenance is reshaping demand patterns and driving technology-led differentiation. Approximately 60% of new FCI installations in 2024 were concentrated in smart grid-enabled regions, highlighting the increasing preference for advanced monitoring solutions.

The leading FCI type is the electronic indicator, accounting for 48% of total installations, driven by its precise fault detection and adaptability across various voltage levels. Mechanical indicators hold a 30% share, favored for legacy networks due to ease of maintenance and low upfront cost. Smart digital indicators are the fastest-growing segment, with adoption increasing rapidly due to integration with IoT and SCADA systems, enabling real-time fault location and automated grid monitoring. These advanced devices currently represent 22% of installations but are expected to surpass mechanical types in next-generation grid projects. Other niche types, including hybrid analog-digital indicators, make up the remaining 5% of the market, serving specialized feeders with complex topology.

Urban distribution networks dominate the market, representing 45% of FCI installations, due to high feeder density and the need for rapid fault isolation. Rural electrification projects account for 25%, focusing on cost-effective, low-maintenance indicators. Industrial microgrids contribute 18%, driven by demand for operational reliability in high-load facilities. Renewable energy integration is emerging rapidly, representing 12% of installations, fueled by increased deployment of solar PV and wind farms that require bidirectional fault detection. The fastest-growing application is renewable energy feeders, where smart digital indicators are increasingly implemented to manage complex grid dynamics.

Utilities remain the primary end-user segment, accounting for 65% of market adoption, as they prioritize grid reliability, fault isolation, and regulatory compliance. Independent power producers are the fastest-growing segment, adopting FCIs in 20% of new energy projects to support automated monitoring and minimize downtime. Industrial consumers, including manufacturing and process industries, contribute 15% of FCI deployments, using them to enhance operational safety and reduce unplanned outages. Regional adoption varies, with North America showing higher integration in smart urban grids, while Asia-Pacific emphasizes renewable energy infrastructure.

North America accounted for the largest market share at 37% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

In North America, over 85,000 FCIs were deployed across urban and rural distribution networks by the end of 2024, while utilities invested more than USD 45 million in grid modernization projects integrating smart indicators. Europe follows with 28% of installations, heavily concentrated in Germany, the UK, and France, with more than 60,000 units in operation. Asia-Pacific has seen rapid expansion, with China and India consuming nearly 50,000 units in 2024 and large-scale rural electrification programs driving adoption. South America and the Middle East & Africa collectively account for 20%, with Brazil, Argentina, UAE, and South Africa leading installations. Technological upgrades, regulatory compliance, and renewable energy integration are the primary factors shaping regional deployment patterns.

How is technology reshaping operational reliability in high-voltage networks?

North America holds 37% of the FCI market by volume, driven by utilities, independent power producers, and industrial sectors. Federal initiatives such as smart grid incentives and updated reliability standards have accelerated adoption of digital indicators. Advanced communication-enabled FCIs allow real-time fault detection and automated feeder isolation, reducing outage duration by up to 30%. General Electric’s local operations recently deployed 5,500 electronic FCIs across urban feeders, integrating them with SCADA for predictive maintenance. North American enterprises show higher adoption rates in dense urban areas, whereas rural utilities focus on cost-effective mechanical indicators, reflecting regional operational and economic variation in FCI deployment.

What regulatory and technological factors are driving FCI adoption in modern distribution grids?

Europe accounts for 28% of FCI installations, with Germany, UK, and France leading adoption. Regulatory mandates, including EU grid reliability standards and sustainability programs, encourage explainable, energy-efficient FCIs. Smart digital indicators are increasingly deployed in renewable-rich regions, especially for solar and wind farm integration. Siemens recently implemented 4,200 digital FCIs in German feeder networks, improving outage detection by 25%. Regional consumer behavior reflects a focus on regulatory compliance and energy efficiency, with utilities prioritizing automated fault detection to meet stringent environmental and reliability criteria.

How is rapid infrastructure development driving FCI deployment in emerging economies?

Asia-Pacific ranks as the fastest-growing region, with China, India, and Japan leading adoption. In 2024, over 50,000 units were installed, driven by urban expansion, rural electrification, and renewable energy projects. Manufacturers are establishing local innovation hubs to integrate IoT-enabled FCIs for predictive maintenance. Schneider Electric deployed 3,200 smart indicators in India’s solar-fed distribution networks, improving fault response times by 28%. Regional behavior favors rapid adoption in emerging markets, with industrial and utility sectors seeking cost-effective, high-precision solutions to enhance grid reliability.

What factors influence FCI adoption across diverse energy landscapes in South America?

South America contributes 12% of global FCI installations, with Brazil and Argentina as key markets. Energy sector upgrades, including grid modernization and integration of distributed energy resources, drive FCI demand. Government incentives for rural electrification and trade agreements support large-scale deployment. Local provider WEG recently installed 1,100 electronic FCIs across medium-voltage feeders in Brazil, reducing outage duration by 22%. Regional consumer behavior varies, with utilities emphasizing affordability and maintenance simplicity, while industrial users prioritize reliability in urban and semi-urban grids.

How are modernization and regulatory standards shaping FCI deployment in oil & gas and urban infrastructure?

The Middle East & Africa accounts for 8% of global FCI adoption, with UAE and South Africa leading. Demand is driven by oil & gas infrastructure, urban construction, and renewable integration projects. Technological modernization includes digital and IoT-enabled indicators, enabling predictive maintenance and grid automation. Schneider Electric implemented 900 smart FCIs across UAE feeders in 2024, reducing average outage response by 26%. Consumer behavior reflects a preference for digital solutions in high-value urban networks, while remote regions continue deploying mechanical FCIs for cost-efficiency.

United States: 37% market share; high production capacity and extensive grid modernization programs drive adoption.

China: 22% market share; strong demand from urban expansion, renewable energy projects, and industrial sector integration.

The Fault Circuit Indicator market is moderately consolidated, with over 45 active competitors globally. The top five companies, including Schneider Electric, ABB, General Electric, Siemens, and WEG, collectively account for approximately 62% of the market, reflecting a competitive yet concentrated landscape. Leading players focus on technological innovation, with investments in digital FCIs, IoT-enabled devices, and predictive maintenance systems. Strategic initiatives such as partnerships with utility providers, product launches of smart indicators, and regional expansion projects are common, ensuring sustained market positioning. In 2024, ABB introduced a next-generation electronic FCI with integrated SCADA communication, deployed across 3,000 feeders in Europe. Schneider Electric expanded its footprint in Asia-Pacific, launching over 5,000 IoT-enabled units in India and China. Market entrants are increasingly emphasizing modular designs and low-maintenance solutions, catering to both urban and rural grid applications. Competitive trends show increased adoption of real-time fault monitoring and cloud-based analytics, driving differentiation among key participants. The fragmented nature of smaller regional players contributes to niche innovations, while leading companies consolidate market leadership through mergers, collaborations, and technology-focused investments.

Siemens

WEG

Eaton

SEL (Schweitzer Engineering Laboratories)

Toshiba

Mitsubishi Electric

Crompton Greaves

The Fault Circuit Indicator (FCI) market is experiencing rapid technological evolution driven by the need for enhanced grid reliability and operational efficiency. Modern FCIs are increasingly adopting digital and smart sensor technologies, enabling real-time fault detection across low- and medium-voltage distribution networks. For instance, advanced optical sensors integrated into electronic FCIs now allow detection of fault currents as low as 0.5 A, significantly improving response times compared to traditional magnetic indicators. IoT-enabled FCIs are emerging as a critical technology, facilitating remote monitoring and predictive maintenance. Utilities in North America and Europe are deploying over 12,000 IoT-enabled FCIs in urban networks, providing automated alerts and reducing outage resolution times by up to 35%. Cloud-based analytics platforms are also being integrated with FCIs to aggregate fault data from multiple feeders, offering utilities actionable insights for load balancing and preventive maintenance planning.

Communication protocols such as LoRaWAN, DNP3, and IEC 61850 are becoming standard for device interoperability, supporting seamless integration into smart grid infrastructure. Energy storage and renewable energy integration are driving innovations in adaptive fault detection, where FCIs automatically adjust sensitivity based on load fluctuations in solar and wind-powered grids. Emerging trends include self-powered indicators using energy harvesting from line currents and the adoption of machine learning algorithms to predict fault patterns. Companies are piloting AI-driven FCIs capable of reducing false trips by 28% and extending equipment lifespan. These technological advances position FCIs as essential components in modern, resilient, and digitally optimized power distribution networks.

In 2024, ABB announced the launch of a new smart FCI series featuring LoRaWAN-enabled communication and zero‑maintenance design, enabling over-the-air firmware updates and remote diagnostics across modern distribution grids.

In late 2023, Schweitzer Engineering Laboratories (SEL) acquired grid analytics firm Bitronics to embed edge‑analytics in its FCIs, improving real‑time fault‑location accuracy and diagnostics capabilities.

In 2024, Schneider Electric introduced its EcoStruxure‑connected FCIs, allowing seamless integration of indicators with its ADMS platform and enabling predictive maintenance and faster fault restoration.

In early 2024, Eaton’s Cooper Power division expanded its programmable delayed‑reset S.T.A.R. FCI lineup, releasing models that support long-life lithium batteries and automated reset, reducing field maintenance for overhead distribution feeders.

The Fault Circuit Indicator (FCI) Market Report provides a comprehensive assessment of the global FCI ecosystem, covering the full range of indicator types — including mechanical, electronic solid-state, and smart digital/IoT-enabled devices. The report analyzes application segments such as overhead lines, underground cable networks, rural feeders, renewable‑energy-connected feeders, and industrial microgrids. It also dissects end-user segments, focusing on utilities (public and private), independent power producers, and large industrial electricity consumers.

Geographically, the report spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, detailing regional deployment trends, regulatory landscapes, grid‑modernization programs, and the influence of distributed energy resources. Technology-wise, the study explores innovations including IoT‑connected FCIs, edge analytics, adaptive sensitivity for two‑way power flow, and energy‑harvesting powered indicators.

Emerging or niche segments are also addressed: for example, the report examines self-powered FCIs leveraging energy harvesting, AI-based fault‑pattern recognition, and FCI integration with distributed energy management systems and microgrid controllers. It further maps competitive dynamics by profiling top global players, regional specialists, and how they are investing in smart grid partnerships, M&A, and new product launches.

Strategically, the report aims to inform decision-makers — including utility executives, grid planners, equipment manufacturers, and investors — about innovation roadmaps, risk‑mitigation strategies, uptake patterns, and future growth levers in the FCI space. It provides guidance on how to align FCI deployment with grid resilience goals, ESG mandates, and advanced network operation frameworks.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 212.38 Million |

|

Market Revenue in 2032 |

USD 271.14 Million |

|

CAGR (2025 - 2032) |

3.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Schneider Electric, ABB, General Electric, Siemens, WEG, Eaton, SEL (Schweitzer Engineering Laboratories), Toshiba, Mitsubishi Electric, Crompton Greaves |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |