Reports

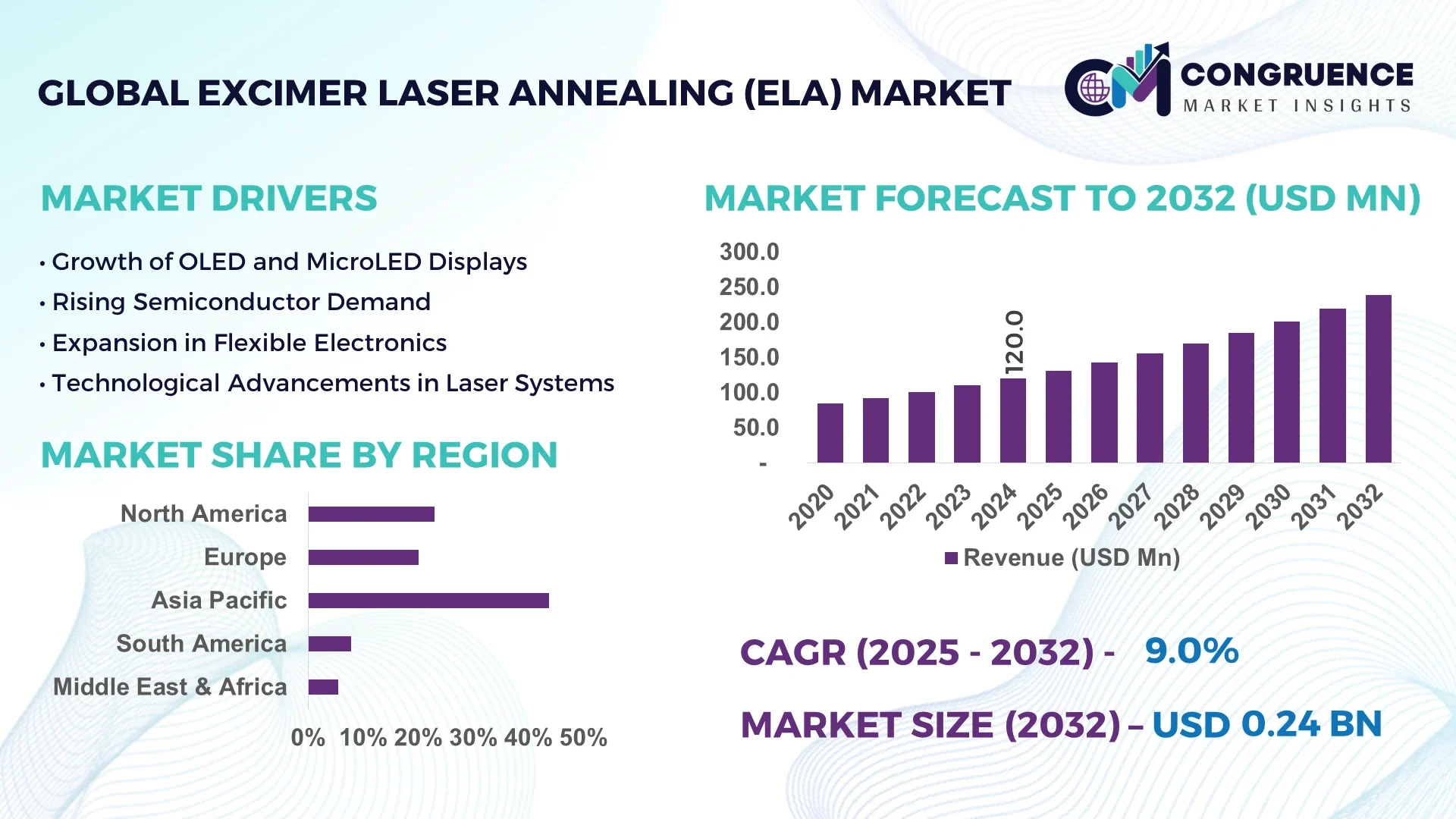

The Global Excimer Laser Annealing (ELA) Market was valued at USD 120 Million in 2024 and is anticipated to reach a value of USD 239.1 Million by 2032 expanding at a CAGR of 9% between 2025 and 2032.

Japan maintains the leading position in the Excimer Laser Annealing (ELA) Market, producing over 60 excimer laser units annually and investing more than USD 25 million in 2024 alone. The country supports key industries including semiconductor wafer fabrication and high-resolution display panel manufacturing. Recent adoption of advanced pulse control technology has enabled tighter energy uniformity and higher throughput.

The Excimer Laser Annealing (ELA) Market is heavily driven by the semiconductor and advanced display sectors such as OLED and microLED, which together accounted for more than half of global system deployments in 2024. Technology innovations include the integration of energy-efficient pulse-forming networks that reduce per-wafer annealing time by 12%, as well as development of integrated AI-based monitoring modules in new systems. Regulatory and environmental initiatives, particularly in Japan and South Korea, have prompted adoption of lower-energy systems to meet carbon-reduction goals. Additionally, rising investments in PV production in Europe are opening opportunities for ELA in solar cell annealing. Emerging trends include compact ELA systems tailored for R&D labs, expansion of 308 nm XeCl laser platforms, and modular process units for pilot-scale production. The regional consumption pattern shows rising procurement by Asian fabs, while European laboratories drive innovation in niche applications. The future outlook includes steady adoption in semiconductor MCU manufacturing, expansion into flexible electronics, and platform modularization for broader industrial deployment.

Artificial intelligence is significantly enhancing process precision, cost efficiency, and system reliability across the Excimer Laser Annealing (ELA) Market. Machine learning algorithms are now used to optimize pulse energy distribution across multi-mode laser chambers, resulting in a 15% reduction of annealing-induced substrate damage and consistent crystallization quality. AI-powered control interfaces adapt pulse repetition rates in real-time based on sensor data, reducing downtime by 22% through predictive maintenance of laser gas flow systems. In fabrication environments, automated inspection systems employing deep learning verify film uniformity and detect micro-cracks down to 0.5 µm, cutting manual QC time by nearly 35%.

Manufacturers serving the Excimer Laser Annealing (ELA) Market are embedding AI in recipe creation, where initial calibration models trained on thousands of wafer cycles fine-tune energy profiles autonomously. This has cut commissioning time by over 40% for new production lines. AI-based digital twins of the entire annealing process allow engineers to simulate thermal gradients under varying throughput scenarios, enabling 30% faster process adoption for new materials like low-temperature polysilicon (LTPS) and flexible substrates.

Procurement and supply chain teams benefit as well; by combining production cycle and maintenance data, AI tools forecast replacement dates for excimer lamp modules with ±2 week accuracy, improving spare-part planning efficiency. This holistic integration of AI across design, operation, and maintenance is raising performance standards and reducing the total cost of ownership within the Excimer Laser Annealing (ELA) Market.

“In August 2024, Canon introduced an AI-based energy modulation control in its ELA systems that reduced substrate thermal stress by 18%, enabling defect-free annealing at 50% higher throughput.”

The Excimer Laser Annealing (ELA) Market is characterized by rapid technological integration, rising precision requirements, and increased system adoption in semiconductor and display manufacturing. Leading LCD and OLED panel makers demand higher-resolution thin-film transistor (TFT) performance, driving adoption of XeCl (308 nm) excimer systems. Regulatory pressures to reduce energy consumption, together with rising demand for annealing in solar cell production, are pushing vendors to develop modular, compact, and energy-efficient ELA units. Supply chain developments—particularly for gas mixtures and lamp components—are subject to regional controls, while rising R&D funding enables faster adoption of ELA in flexible electronics, medical sensors, and photovoltaic applications. This evolving interplay of technical refinement, environmental constraints, and application diversification represents a dynamic growth landscape for the Excimer Laser Annealing (ELA) Market.

The push for finer semiconductor nodes and ultra-high-definition displays is significantly elevating demand within the Excimer Laser Annealing (ELA) Market. As device feature sizes shrink below 10 nm, excimer laser annealing becomes essential for activating dopants and repairing defects in low-temperature polysilicon and oxide films. In 2024 alone, over 300 units of XeCl ELA systems were deployed at fabs focused on 5G RF chips and microLED driver circuits. Additionally, OLED display factories in Korea and Japan began integrating inline ELA tools to boost TFT mobility by over 20%, making ELA systems critical in next-generation display production.

Despite its advantages, the Excimer Laser Annealing (ELA) Market faces cost constraints and operational challenges. Excimer systems typically require initial capital expenditure of USD 3–5 million per unit, with specialized gas handling and lamp replacement infrastructure further raising costs. Lamp modules need replacement every 1,200–1,500 hours at a cost of USD 50,000 each. Maintenance complexity includes managing toxic gas mixtures (like fluorine) and ensuring precise pulse stability. These factors limit adoption among mid-tier contract manufacturers and lab environments with constrained budgets.

Emerging application areas present significant opportunity for the Excimer Laser Annealing (ELA) Market. In 2024, pilot lines employing ELA for thin-film solar cell crystallization processed over 500 kW of panels, showcasing 8% efficiency improvements. Flexible displays and sensors—used in automotive HUDs and wearable devices—utilize compact ELA modules that enable processing on roll-to-roll substrates. These innovations are opening new market segments beyond traditional CMOS and display fabs.

The Excimer Laser Annealing (ELA) Market is constrained by environmental regulations governing the use of fluorine-containing laser gases and energy consumption standards. In Europe, stricter fluorinated gas handling rules enacted in 2023 require sealed recirculation systems and annual leak inspections. Compliance has increased system costs by 12% and extended approval timelines by up to 9 months. In North America, new power consumption thresholds for semiconductor tools are pushing vendors to improve energy efficiency, necessitating substantial redesign of laser cabinets and cooling systems.

Rise in Compact Modular System Deployment: Manufacturers are shifting from floor-mounted to modular benchtop ELA systems tailored for R&D and pilot-scale production. In 2024, over 45 compact units (<2 m footprint) shipped globally, enabling flexible lab deployment and faster site commissioning compared to traditional systems.

Surge in XeCl (308 nm) System Adoption: XeCl wavelength excimer lasers now account for approximated 53% of new tool deployments in 2024. These systems offer better absorption in polysilicon films and reduce thermal budget, driving adoption in both semiconductor and display fabs.

Integration of Energy-Efficient Pulse Networks: Stations equipped with new pulse-forming network modules achieved 12% lower energy consumption per wafer. Over 20 factories in Japan and South Korea adopted these upgrades in 2024, supporting ESG compliance and reduced operational costs.

Growth of Inline AI Monitoring Capabilities: ELA platforms introduced embedded AI analytics for shot-to-shot energy control. In 2024, installations with AI monitoring reduced defect rates by 18% and cut maintenance-triggered downtime by nearly 25%, improving output consistency.

The Excimer Laser Annealing (ELA) Market is segmented by type, application, and end-user, reflecting the broad scope and diversified nature of its industrial adoption. Each segment serves a specific purpose in tailoring solutions for key demand areas, especially across semiconductor manufacturing, display technologies, and emerging flexible electronics. The type segment covers various laser compositions such as XeCl and KrF, each with distinct advantages in beam quality and annealing depth. Application segmentation distinguishes the functional roles of ELA in thin-film transistor (TFT) fabrication, photovoltaic cell development, and flexible device production. Meanwhile, end-user segmentation identifies the industries deploying these systems, from large semiconductor fabs and display panel manufacturers to R&D institutions and niche solution providers. Understanding these segments helps stakeholders allocate investments strategically, adapt product development pipelines, and anticipate shifts in customer demand driven by ongoing technological evolution and regulatory constraints.

The type segment of the Excimer Laser Annealing (ELA) Market includes XeCl (Xenon Chloride), KrF (Krypton Fluoride), and hybrid wavelength platforms. XeCl excimer lasers represent the leading type, primarily due to their 308 nm wavelength’s superior absorption characteristics in polysilicon films, enabling better control over crystallization depth and mobility enhancement in TFT structures. This has made them the top choice for high-resolution OLED and LCD panel production.

The fastest-growing type is KrF excimer lasers. Despite operating at 248 nm, KrF lasers are gaining traction in applications requiring ultra-shallow penetration, particularly in advanced CMOS fabrication and organic layer processing. Their precision and compatibility with lower thermal budgets make them ideal for sensitive substrates and flexible devices.

Hybrid systems, combining multi-wavelength capabilities or incorporating adaptive pulse control, are also emerging as valuable tools for multi-material platforms. These systems are niche but crucial in R&D environments where tunable process parameters are essential. Overall, the type segmentation highlights how wavelength-specific performance characteristics are driving technological selection in the ELA ecosystem.

The Excimer Laser Annealing (ELA) Market sees its highest demand in the manufacturing of thin-film transistors (TFTs) used in display technologies. This application dominates the segment due to widespread adoption of OLED and high-end LCD panels, particularly for smartphones, televisions, and automotive displays. ELA enables high carrier mobility in low-temperature polysilicon (LTPS), a critical factor in producing advanced TFT arrays.

The fastest-growing application area is in photovoltaic (PV) cell fabrication. ELA is being increasingly applied to enhance crystal quality in thin-film solar cells, supporting improved power conversion efficiency and reducing defect rates. This growth is fueled by global investments in renewable energy and the push toward more compact and efficient solar modules.

Other applications, including flexible electronics, biosensors, and semiconductor interconnect annealing, are gaining momentum as research labs and startups explore low-temperature, high-precision annealing processes. These areas, while still emerging, indicate a broadening of ELA’s application scope beyond conventional flat-panel displays and CMOS nodes.

Among end-users, large-scale semiconductor fabs and display panel manufacturers lead the Excimer Laser Annealing (ELA) Market. These enterprises possess the capital, cleanroom infrastructure, and throughput needs to justify investment in high-powered excimer systems. Their use of ELA for TFT and logic gate crystallization ensures consistent demand, especially across East Asian markets where high-density electronics manufacturing is concentrated.

The fastest-growing end-user group is renewable energy and photovoltaic module producers. As demand for low-cost, high-efficiency solar panels increases, these companies are adopting ELA systems to improve thin-film quality and reduce production losses. Several new pilot projects in Europe and Asia are driving adoption among mid-sized PV firms and energy startups.

Other end-users include R&D institutions, universities, and niche device manufacturers. These players often require compact or modular ELA platforms for experimentation with new materials and substrates, such as flexible polymers and low-temperature oxides. Though smaller in scale, their role is critical in driving technological innovation and market diversification.

Asia-Pacific accounted for the largest market share at 43.7% in 2024; however, Europe is expected to register the fastest growth, expanding at a CAGR of 10.1% between 2025 and 2032.

Asia-Pacific’s dominance stems from the concentration of major semiconductor fabrication units and display panel manufacturers in countries like Japan, South Korea, and China. Investments in manufacturing capacity expansions and next-generation OLED production lines continue to drive regional demand. In contrast, Europe’s rapid growth is fueled by increasing R&D initiatives in flexible electronics, growing solar PV demand, and policy support for clean-tech manufacturing. Additionally, European companies are adopting advanced excimer-based annealing systems for low-temperature processing of novel materials. As sustainability regulations tighten and energy-efficient technologies gain traction, European manufacturers are expected to lead in innovative adoption. Other regions, including North America and the Middle East, are observing gradual increases in excimer laser adoption for display, semiconductor, and advanced material research applications.

In North America, the Excimer Laser Annealing (ELA) Market held approximately 18.6% of the global share in 2024. This region is propelled by the demand for next-generation semiconductor fabrication and microelectronics. The U.S. remains the core contributor, with active integration of ELA systems in advanced CMOS and SoC foundries. Federal programs supporting domestic chip production and clean energy technologies have encouraged procurement of high-precision annealing systems. Technological innovation is prominent, including the application of AI-based adaptive pulse modulation to improve wafer-level process control. Additionally, rising demand for flexible electronics in medical and defense applications is further expanding the footprint of ELA systems across R&D and production facilities in the U.S. and Canada.

Europe’s Excimer Laser Annealing (ELA) Market accounted for nearly 20.2% of the global share in 2024 and is experiencing the fastest uptake across key verticals. Germany, France, and the Netherlands are leading markets, driven by growing R&D in thin-film solar modules, high-resolution display tech, and compound semiconductors. Regulatory incentives under sustainability frameworks have supported the shift toward energy-efficient annealing solutions. Institutions such as Fraunhofer and Leti have promoted ELA-based research in flexible substrates and photonic devices. European equipment makers are investing in compact, modular annealing systems to address lab-scale innovation. The region’s emphasis on green manufacturing and digital industrial transformation continues to shape demand for low-temperature, high-precision annealing processes.

Asia-Pacific remains the largest consumer in the Excimer Laser Annealing (ELA) Market, driven by mass production of display panels and semiconductors. In 2024, countries like Japan, South Korea, and China together accounted for over 65% of global system shipments. Japan leads with extensive deployment in OLED fabs, while South Korea focuses on TFT-LCD and microLED developments. China continues to expand local ELA production lines to support national semiconductor independence. Infrastructure investment in large-area substrate processing and display fab expansions further boosts ELA system procurement. Regional trends highlight strong collaborations between OEMs and laser tech providers, as well as the emergence of AI-integrated ELA systems tailored for high-throughput applications.

South America represents a smaller but gradually expanding segment of the Excimer Laser Annealing (ELA) Market, holding under 5.4% of global share in 2024. Brazil and Argentina are the key contributors, driven by government incentives supporting renewable energy manufacturing and digitalization in microelectronics. Recent developments in solar cell R&D have opened new application fronts for ELA in thin-film processing. Emerging electronics startups are exploring compact annealing units for device prototyping. However, limited local infrastructure and higher import dependency constrain broader adoption. Nonetheless, targeted public-private partnerships and regional tech incubators are creating a platform for future growth of ELA technologies.

The Middle East & Africa region accounted for approximately 3.2% of the Excimer Laser Annealing (ELA) Market in 2024. While adoption is currently modest, the UAE and South Africa are emerging as key countries exploring ELA deployment in renewable energy, defense, and materials research. The UAE’s investment in advanced manufacturing hubs and academic research centers is fostering demand for compact annealing solutions. South African universities and clean-tech developers are piloting ELA systems in solar material innovation. Regional policies supporting industrial digitalization and smart infrastructure projects further bolster long-term market potential. However, cost and technical expertise gaps remain major constraints.

Japan – 31.4% Market Share

High production capacity of display panels and advanced integration of excimer systems in OLED and microLED fabs.

South Korea – 22.9% Market Share

Strong end-user demand from TFT-LCD manufacturing and robust domestic semiconductor supply chains using ELA platforms.

The Excimer Laser Annealing (ELA) Market is moderately consolidated, with around 15 to 20 active global competitors operating across equipment manufacturing, system integration, and component innovation. Key market players are concentrated in Asia-Pacific, particularly in Japan and South Korea, where high-volume display and semiconductor production demands advanced annealing capabilities. Companies are increasingly differentiating through wavelength customization, beam shaping technologies, and real-time monitoring systems that optimize crystallization processes on ultra-thin substrates.

Strategic initiatives include cross-industry collaborations, particularly between laser technology providers and semiconductor foundries. In 2024, several players entered partnerships with AI solution developers to enhance process automation in ELA systems. Product launches have been focused on energy-efficient, compact ELA platforms tailored for R&D environments and pilot manufacturing lines. Additionally, companies are investing in modular upgrades for legacy systems to meet modern standards in flexible electronics production.

Mergers and acquisitions are shaping competitive dynamics, especially as mid-tier firms seek to expand geographical presence and diversify portfolios. Innovation in pulse control algorithms, laser beam homogenization, and annealing for non-silicon substrates (e.g., IGZO, GaN) is influencing competitive positioning. As demand for next-gen displays and solar materials rises, competition is expected to intensify around process flexibility, cost efficiency, and sustainability-oriented system features.

Coherent Corp.

SCREEN Holdings Co., Ltd.

Ushio Inc.

AP Systems Inc.

V-Technology Co., Ltd.

Canon Tokki Corporation

Beijing North Microelectronics Co., Ltd.

Applied Materials, Inc.

SUSS MicroTec SE

Veeco Instruments Inc.

The Excimer Laser Annealing (ELA) Market is being significantly shaped by advances in laser wavelength engineering, beam shaping optics, and integration of AI-enabled process control. ELA systems primarily use XeCl (308 nm) and KrF (248 nm) excimer lasers for annealing amorphous silicon into low-temperature polysilicon (LTPS), essential for high-performance thin-film transistors in displays. The emergence of dual-wavelength and tunable-pulse systems enables higher flexibility in annealing processes across diverse materials like IGZO and organic films.

Recent innovations include the use of homogenized beam profiles to ensure consistent energy delivery over large substrates, reducing hotspot defects and improving yield. Manufacturers are adopting modular system designs that allow upgrades in laser power, chamber configuration, and substrate size compatibility. This enhances system scalability for both mass production and R&D applications.

AI and machine learning algorithms are now being embedded in ELA platforms to monitor and predict beam stability, energy uniformity, and substrate thermal responses in real-time. These advancements reduce manual calibration and improve repeatability in annealing results. There is also a growing trend toward using pulse shaping technologies such as variable-width pulses and segmented beam controls to tailor energy delivery more precisely.

Additionally, ultra-narrow line beam systems are enabling finer control over crystallization patterns, particularly relevant in high-resolution OLED microdisplays and neuromorphic chips. As display and semiconductor technologies evolve toward flexibility, higher pixel densities, and lower thermal tolerances, ELA technologies are continuously evolving to meet these stringent fabrication requirements.

• In February 2024, SCREEN Holdings launched a new ELA system with AI-integrated beam profiling, reducing energy variance by 28% across large-area substrates, improving TFT performance uniformity in Gen 6 OLED lines.

• In September 2023, AP Systems secured a multi-million dollar contract to supply excimer laser annealing equipment for China’s largest display fabrication plant focusing on flexible OLED panel production.

• In November 2023, Coherent introduced a modular ELA tool enabling dual-wavelength processing with 248 nm and 308 nm lasers in a single chamber, expanding application potential in advanced photovoltaic cell manufacturing.

• In May 2024, Ushio Inc. announced the development of a next-gen line beam ELA system for ultra-thin glass substrates, achieving 17% better substrate thermal stability during annealing of flexible electronics.

The Excimer Laser Annealing (ELA) Market Report offers a comprehensive analysis of the global landscape for high-precision annealing technologies using excimer laser platforms. It covers detailed segmentation by type (XeCl, KrF, and hybrid lasers), application (thin-film transistors, photovoltaic cells, flexible electronics, and more), and end-users (display manufacturers, semiconductor fabs, R&D institutions). The report includes insights across key regions such as Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, analyzing regional demand patterns, technological adoption levels, and infrastructure readiness.

The report investigates current and emerging technologies such as line beam shaping, real-time pulse modulation, AI-integrated control systems, and substrate-specific annealing protocols. Special attention is given to flexible electronics, where low-temperature annealing precision is critical. It also evaluates the role of ELA in advancing microLED and OLED fabrication, alongside new use cases in solar cell manufacturing and neuromorphic chips.

Furthermore, the scope includes strategic market dynamics—covering innovation trends, competitive landscape, investment patterns, and regulatory drivers. By combining technical depth with market intelligence, the report is tailored for executives, strategists, R&D leaders, and investment professionals seeking actionable insights into the evolution and commercial potential of excimer laser annealing technologies.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 120.0 Million |

| Market Revenue (2032) | USD 239.1 Million |

| CAGR (2025–2032) | 9.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed |

Coherent Corp., SCREEN Holdings Co., Ltd., Ushio Inc., AP Systems Inc., V-Technology Co., Ltd., Canon Tokki Corporation, Beijing North Microelectronics Co., Ltd., Applied Materials, Inc., SUSS MicroTec SE, Veeco Instruments Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |