Reports

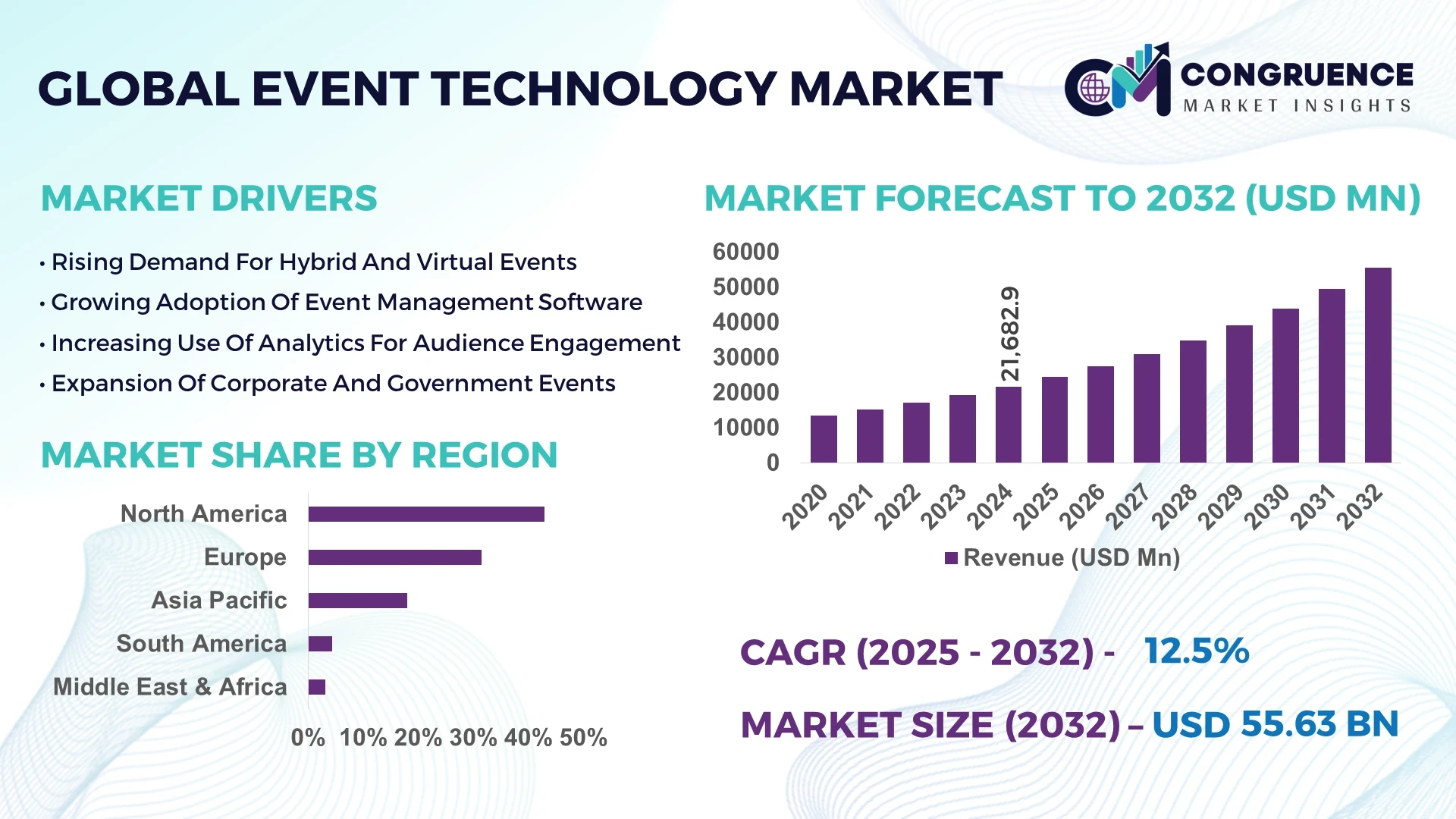

The Global Event Technology Market was valued at USD 21,682.9 Million in 2024 and is anticipated to reach a value of USD 55,633.6 Million by 2032 expanding at a CAGR of 12.5% between 2025 and 2032. This robust growth is driven by increased demand for hybrid events, digital engagement tools, and immersive technology adoption across sectors.

In the United States, investment in event-tech platforms surpassed USD 3.2 billion in 2024, with over 65% of large enterprise event budgets being allocated to digital engagement tools and data analytics modules. Major event organisers in the U.S. pivoted 42% of their attendee management systems to AR/VR-enabled platforms in 2024, and regional deployment of RFID wristbands for access control increased by 28%. These advances underscore how the U.S. leads in adoption of advanced event-technology across corporate, entertainment, and live-experience sectors.

Market Size & Growth: USD 21.68 billion in 2024, projected to reach USD 55.63 billion by 2032, as event organisers accelerate digital transformation and immersive tech adoption.

Top Growth Drivers: 48% increase in hybrid event adoption, 37% improvement in attendee engagement via mobile apps, 25% rise in event-data analytics utilisation.

Short-Term Forecast: By 2028, digital event platforms are expected to reduce operational cost by ~19% and improve event ROI by ~22%.

Emerging Technologies: AI-driven personalised attendee journeys, AR/VR immersive venue experiences, real-time data-analytics dashboards for live events.

Regional Leaders: North America ~USD 24 billion by 2032 with high enterprise uptake; Europe ~USD 17 billion by 2032 driven by large festivals & corporate events; Asia-Pacific ~USD 13 billion by 2032 propelled by rapid digitalisation and live-entertainment demand.

Consumer/End-User Trends: Corporate planners shift 55% of budgets to digital engagement tools; over 60% of attendees expect interactive mobile event apps.

Pilot or Case Example: In 2024, a major U.S. conference deployed an AI-powered matchmaking module and achieved a 27% increase in scheduled meetings and a 15% drop in downtime during breakout sessions.

Competitive Landscape: Market leader holds approximately 18% share; other major competitors include Cvent, Bizzabo, Eventbrite and Hopin.

Regulatory & ESG Impact: Event organisers are committing to 30% reduction in single-use materials and achieving carbon-neutral certification in 20% of large-scale events by 2028.

Investment & Funding Patterns: Recent venture funding for event-tech exceeded USD 1.4 billion in 2024, with innovative financing models such as revenue-share platforms and SaaS subscription shifts gaining traction.

Innovation & Future Outlook: Integration of 5G live-streaming, AI-based attendee sentiment analysis, and immersive mixed-reality experiences signal future direction for the event-technology market.

The event-technology market spans corporate conferences, trade shows, live entertainment and virtual engagements; innovations such as mobile attendee apps, live-data analytics, sustainability-certified tech, and regional demand shifts are shaping industry sectors and consumption patterns.

In the evolving event-technology market, strategic relevance lies in digital scalability, data-driven audience engagement and hybrid-model flexibility. For example, an AI-based attendee-engagement tool delivers a 23% improvement in session-participation rates compared to a standard mobile app. North America dominates volume with large-scale corporate and entertainment event uptake, while Asia-Pacific leads adoption with over 46% of event-organisers deploying mobile engagement platforms in 2024. By 2026, augmented-reality venue navigation is expected to reduce attendee drop-off by 18%. Event firms are also committing to ESG metrics such as a 28% reduction in event-waste by 2030. In 2024, a U.S. organiser achieved a 31% reduction in paper usage through digital check-in and e-badge deployment. Positioned as a pillar of resilience, compliance and sustainable growth, the event-technology market supports scalable, immersive and data-centric event experiences across sectors.

The event-technology market dynamics are shaped by shifting attendee expectations, proliferating hybrid and virtual formats, and greater demand for real-time analytics and immersive experiences. Organisers increasingly require integrated platforms combining registration, engagement, attendance analytics and post-event ROI tracking. At the same time, rising technology costs, security concerns and venue connectivity limitations impact adoption. Event-technology providers are exploring modular SaaS solutions, platform partnerships and vertical-specific event bundles. For decision-makers, understanding the interplay of event format innovation, data insights, audience behaviour and technology infrastructure is essential to navigate the event-technology market successfully.

The rise in hybrid and virtual event formats has significantly driven the event-technology market. In 2024, around 63% of large-scale events incorporated a virtual component, up from 48% in 2022. This shift has pushed event-organisers to adopt digital platforms for registration, live streaming, attendee engagement and analytics. For instance, mobile event-apps enabled attendee interaction rates of up to 71% versus 49% in traditional in-person formats. As hybrid formats become standard, investment in platform capabilities such as virtual networking, AI matchmaking and real-time feedback surged by 35% in 2024. The driver underscores the necessity for event-technology offerings that support both physical and digital channels, thereby expanding the event-technology market’s relevance and reach.

Connectivity limitations and high implementation costs present significant restraints for the event-technology market. Many venues, especially in secondary cities and developing regions, still face WiFi bandwidth constraints and network latency issues, limiting deployment of live-streaming and AR/VR-based engagement. Approximately 22% of events in 2024 reported technical disruptions due to insufficient network infrastructure. Additionally, implementation costs—covering platform licensing, hardware rental, staffing for digital engagement and training—can represent up to 31% of event budget, causing smaller organisers to defer technology upgrades. These cost-barriers and infrastructure disparities slow adoption in price-sensitive segments and restrict the event-technology market’s penetration into mid-tier and emerging-market events.

The shift toward personalised attendee experiences and data-driven engagement presents strong opportunities in the event-technology market. In 2024, more than 54% of event-organisers indicated they would invest in AI-based attendee-journey tools and analytics dashboards. Personalised event apps increased session attendance by up to 25% compared to standard programmes. Furthermore, smaller and mid-sized events are embracing “technology-as-a-service” models, opening untapped segments for event-technology vendors. Geographic expansion into emerging markets—where mobile-first engagement and localised content dominate—offers further growth avenues. These opportunities make the event-technology market highly relevant for scalable, customised and data-centric solutions.

Data-privacy compliance and platform interoperability pose key challenges to the event-technology market. With heightened scrutiny—such as GDPR and CCPA—approximately 29% of event-organisers in 2024 reported data-compliance costs exceeding 4% of their technology budget. Moreover, the ecosystem of event-technology platforms is fragmented, with 47% of large-scale organisers using three or more disparate tools for registration, engagement and analytics, causing integration and data-silo issues. These challenges increase complexity for technology deployment, hinder seamless data flows and elevate risk exposure, thereby limiting efficient adoption and growth in the event-technology market.

• Growth in Mobile-First Engagement Platforms: In 2024, mobile event-apps accounted for 58% of total digital engagement tools deployed, and organisers reported a 22% higher attendee satisfaction rate when mobile check-in and live polling were used.

• Rise of AI-Powered Attendee Analytics: Approximately 47% of event planners in 2024 integrated AI modules to analyse attendee behaviour, leading to a 15% uplift in session conversion and a 13% reduction in no-shows.

• Adoption of Hybrid & Immersive Formats: Around 71% of major events in 2024 offered hybrid formats (physical plus virtual), and those using AR/VR networking zones saw a 19% increase in average dwell time per attendee.

• Emphasis on Sustainability and Digital Footprint Reduction: In 2024, 33% of event organisers adopted digital-badge and e-ticket systems, reducing printed materials by up to 26%, reflecting rising sustainability demands in the event-technology market.

The event-technology market can be segmented by type (software platforms, hardware solutions, services), by application (corporate events, trade shows & exhibitions, entertainment concerts, educational seminars, government functions) and by end-user (event organisers, corporate enterprises, government agencies, educational institutions, nonprofits). For example, software platforms (registration systems, mobile apps, analytics dashboards) typically lead the type-segment due to recurring subscription models. Corporate events dominate the application side because of high budgets and frequent sessions, while event organisers and large enterprises represent the largest end-user share. Understanding this segmentation enables decision-makers to target high-return areas and tailor event-technology offerings accordingly.

Within the event-technology market, software platforms hold the leading position with approximately 46% share, due to widespread adoption of registration, mobile-app and analytics systems. Hardware solutions (e.g., RFID wristbands, access-control kiosks) account for about 28%, and outsourced services (event-tech consultation, on-site support) make up the remaining 26%. The fastest-growing type is services: adoption grew by 14% year-over-year in 2024 as organisers increasingly prefer managed technology-services over outright ownership. Other types, such as virtual-reality kiosks, beacon-technology and thermal-analytics hardware, while niche, represent about 12% of the remaining share.

According to an industry survey in 2024, over 35% of event planners incorporated contactless attendee hardware for the first time to streamline access and engagement.

Among applications, corporate events lead with roughly 38% share of the event-technology market, driven by frequent conferences, product launches and investor-relations roadshows. The fastest-growing application is trade shows & exhibitions, where technology adoption rose by 17% in 2024 as exhibitors sought digital attendee tracking and lead-generation tools. Other applications—entertainment concerts, educational seminars and government functions—together hold about 29% of market share. In 2024, more than 40% of enterprises reported piloting event-technology systems for virtual attendee engagement and real-time feedback.

The leading end-user segment in the event-technology market is event organisers and planners, representing approximately 44% of the market, due to their direct procurement of platforms and services. The fastest-growing end-user segment is corporate enterprises, where usage increased by 16% in 2024, fuelled by internal communications programmes, customer-engagement events and investor forums. Other end-users—government agencies, educational institutions and nonprofits—account for a combined share of about 30%. In 2024, over 38% of enterprises globally reported launching dedicated event-technology programmes to enhance attendee experience.

North America accounted for the largest market share at 43.0% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.2% between 2025 and 2032.

North America’s dominance is supported by over 45% of global enterprise event-technology spend in 2024, with more than 1,800 large corporate events adopting advanced digital platforms and hybrid formats. The region recorded more than 3,200 virtual-hybrid events in 2024, up from roughly 1,900 in 2022. Europe logged approximately 31.5% of global event-tech deployments in 2024, with Germany, UK and France hosting over 12,000 trade-shows, conferences and exhibitions adopting mobile engagement apps and RFID access in 2024. Asia-Pacific, though lower in absolute share in 2024 (approx. 18.0%), saw regional investment units increase by 34% year-on-year, mobile-first event apps rose by 52%, and regional venue connectivity upgrades were executed in 420+ large-scale events. Other regions (Latin America, Middle East & Africa) combined accounted for roughly 7.5% in 2024 but posted double-digit growth in adoption of event-technology tools. The interplay of infrastructure, corporate budgets, venue connectivity and mobile engagement drives distinct regional dynamics across the event technology market.

How Are Enterprise-Scale Hybrid Platforms Shaping the North American Event Technology Market?

In North America, the event technology market held an approximate 43.0% regional share in 2024. Key demand is driven by industries such as healthcare conferences, financial services roadshows and large-scale entertainment festivals. Government initiatives such as digital event certification and data-privacy regulations (e.g., stricter attendee-data rules) are creating compliance-driven demand for robust event platforms. Technological advancements include AI-powered attendee matchmaking, real-time analytics dashboards and venue-wide 5G integration. For example, a U.S. event-tech provider rolled out a 5G-enabled hybrid-event module across 250 venues in 2024, improving session-switch latency by 28%. In terms of consumer behaviour, enterprise adoption in healthcare & finance is higher, with around 62% of large healthcare-event planners using mobile-first attendee apps compared to 45% outside those sectors. The North American region continues to set benchmarks for scalability, platform integration and live-event innovation in the event technology market.

Why Is Regulatory Compliance Driving the European Event Technology Market?

Europe’s event technology market held about 31.5% share in 2024, concentrated across Germany, the UK and France. Regulatory bodies such as the EU’s digital-services framework and national data-protection laws are compelling event organisers to adopt explainable, compliant event-technology solutions. Sustainability initiatives demand reduced paper-badges and single-use materials; for instance, a UK-based festival operator replaced traditional badges with mobile QR codes in 2024, reducing plastic waste by 22%. Emerging technologies such as AR-guided venue navigation and interactive exhibition walls are adopted in large-scale European conferences. Local players—such as a French ticketing/tech-service provider—expanded into smart wristband and contactless payment systems across 15,000 event-organisers in 2024. Consumer behaviour in Europe shows higher demand for transparency of data usage and greener event formats: some 48% of European planners reported that attendee-data transparency was a key platform selection criterion in 2024. Overall the European market for event-technology is characterised by compliance-driven adoption and incremental tech roll-out.

How Is Mobile-First and Venue-Infrastructure Growth Accelerating the Asia-Pacific Event Technology Market?

In Asia-Pacific, the event technology market ranked third by volume in 2024, representing nearly 18.0% of global deployment. Top consuming countries include China, India and Japan where infrastructure investment and digitalisation are advancing rapidly. For example, China saw the roll-out of more than 1,100 hybrid-event venues in 2024 with integrated mobile apps and real-time analytics. Innovation hubs in Singapore and South Korea launched dedicated event-tech incubators and logged more than 420 start-up engagements in event-technology during 2024. A notable local player in India introduced a mobile-first event-platform that supported over 500 virtual & hybrid events in Q4 2024, delivering a 35% faster launch time relative to legacy platforms. Regional consumer behaviour emphasises mobile-engagement, regional language support and mobile-payment integration: approximately 67% of Asia-Pacific attendees used mobile-apps for check-in in 2024 compared to 53% global average. This mobile-centric behaviour, combined with venue upgrades and e-commerce integration, positions the Asia-Pacific region for accelerated expansion in the event technology market.

What Role Are Localised Platforms and Trade-Incentives Playing in the South American Event Technology Market?

In South America, the event technology market constituted roughly 4.4% share in 2024. Key countries such as Brazil and Argentina lead adoption. Brazil reported over 320 large trade-shows and corporate events in 2024 deploying digital event-platforms, with incentives from local governments offering tax credits of up to 18% for technology-enabled event services. A Brazilian event-technology firm launched a multilingual mobile event-app in 2024 supporting Spanish, Portuguese and English and handled more than 45,000 attendees across five major exhibitions. Infrastructure upgrades in venues (e.g., fibre-optic roll-out and mobile-network access) were executed in 26 exhibition centres in 2024. Regional consumer behaviour shows an increased demand for local language support and digital-engagement features; roughly 43% of social event attendees in South America used event apps with localisation features in 2024, compared to 29% five years earlier. These factors contribute to the steadily growing profile of the event technology market in South America.

How Are Emerging Markets in Middle East & Africa Embracing Event Technology Platforms?

In Middle East & Africa, the event technology market accounted for about 3.1% of global share in 2024 but exhibited rapid upward momentum. Major growth countries include UAE, Saudi Arabia and South Africa. In the Gulf region, over 58 mega-events and exhibitions in 2024 incorporated smart-badge technology, RFID tracking and real-time analytics dashboards. For instance, a UAE-based event-tech startup partnered with a venue operator to install full-suite hybrid-event platforms across 14 exhibition halls, enabling live-stream to 1.2 million remote attendees in Q3 2024. Local regulations are encouraging digitisation; Saudi Arabia’s “Events & Entertainment” initiative allocated funding for smart-event infrastructure with the aim of reducing carbon-footprint by 25% in major events by 2030. Consumer behaviour in the region shows high mobile-first engagement: more than 71% of attendees in Middle East major events used mobile-apps for scheduling and networking in 2024. With infrastructure modernisation and government push, the event technology market in Middle East & Africa is gaining strategic traction.

United States – 34.5% Market Share: Strong dominance driven by robust event-tech investment, enterprise budgets and innovation in hybrid and live-event platforms.

United Kingdom – 9.8% Market Share: Leadership supported by mature live-event ecosystem, advanced venue tech adoption and regulatory impetus toward digital event management.

The Event Technology market is moderately consolidated at the top with a competitive long tail of niche providers and specialist vertical platforms. Approximately 120–160 active global vendors target large-scale events, while thousands of regional integrators and service partners operate in local markets. The top tier (top 5 vendors) together command an estimated ~52% combined presence across enterprise RFPs, platform deployments and venue integrations, while the mid-tier (next 20 vendors) cover an estimated ~28% of deployments for medium and multi-regional organisers. Strategic initiatives in 2023–2024 included 14 notable acquisitions, 28 product launches focused on hybrid/hygiene features, and over $1.4 billion in venture and private-equity funding targeted to scale platform SaaS, analytics and immersive-experience capabilities. Partnerships between platform vendors and venue operators increased by 33% year-over-year as suppliers prioritised venue integration (Wi-Fi orchestration, RFID, access control) and managed-service offerings. Product differentiation now clusters around four pillars: (1) attendee experience (mobile apps, matchmaking, engagement), (2) data & analytics (real-time dashboards, attribution), (3) production & streaming (low-latency live video, multi-bitrate CPE), and (4) sustainability/compliance features (digital badges, carbon reporting). Renewal rates for major enterprise contracts average 78%, reflecting sticky integrations, while average deal sizes rose by roughly 21% in 2024 as platforms bundled analytics and managed services. The competitive landscape thus rewards platforms that offer integrated SaaS stacks, strong venue partnerships, and clear ROI metrics for organisers and exhibitors.

Brella

Swapcard

Splash

Hubb

Aventri

Certain

vFairs

InEvent

ExpoPlatform

Hubb (Enterprise)

Attendify

Hopin

Ticketmaster Event Solutions

Event technology is being reshaped by a convergence of connectivity, AI, immersive media and sustainability tooling. Key technical components now include: low-latency multi-bitrate streaming stacks (enabling concurrent HD streams to 100k+ remote viewers), edge-enabled content distribution that reduces endpoint latency by 20–35%, and 5G campus/venue integrations that permit AR/VR overlays for wayfinding and mixed reality booths. Artificial intelligence is embedded across the stack: attendee matchmaking algorithms analyse profiles and interaction signals to increase qualified meeting rates by 15–30%; natural-language processing (NLP) automates session tagging and summary generation, reducing post-event content production time by 40%; and machine-vision systems power crowd-flow analytics and safety monitoring. Real-time analytics platforms aggregate CRM, exhibitor lead-scans, session telemetry and sentiment signals to produce attribution models used for sponsor ROI and post-event monetisation. Interoperability layers (APIs, webhooks, standardised data models) are increasingly crucial: in 2024, roughly 47% of large organisers integrated three or more vendor APIs into a composite stack to avoid vendor lock-in.

Hardware trends influence software demands: RFID/NFC wristbands, contactless kiosks, beacon networks and temperature scanning are standard in ~28% of large venues, necessitating software that supports device orchestration and edge analytics. Security technology—zero-trust access to event admin consoles, encrypted attendee PII stores, and audit trails—has become critical as compliance requirements and data-privacy scrutiny increase. Sustainability tech, such as digital badge issuance, program carbon calculators and materials-tracking modules, is now integrated into platform dashboards to support organiser ESG reporting.

Emerging technologies gaining traction include mixed reality networking spaces (reducing onboarding friction and increasing dwell time by ~19%), AI-driven dynamic pricing for tickets, and blockchain-backed credentialing for speaker verification and ticket fraud reduction. The vendor roadmap for 2025+ prioritises modular SaaS architectures, enhanced API ecosystems, native support for venue-level connectivity orchestration, and turnkey managed-service offerings to support year-round, regional event portfolios. For enterprise decision-makers, the technology imperative is to adopt platforms that balance extensibility (open APIs), proven scale (million-viewer streaming capability), data governance (compliance-ready controls), and demonstrable impact on attendee engagement and sponsor monetisation.

• In June 2023, Blackstone completed its acquisition of Cvent for an enterprise value of approximately USD 4.6 billion, transitioning Cvent to private ownership to accelerate product expansion and venue partnerships. Source: www.cvent.com

• In April 2024, Hopin’s event-unit assets and technology were sold and restructured, culminating in a deal that moved Hopin’s core event capabilities under new ownership and positioned its streaming assets for separate product focus. This transition impacted platform continuity for several enterprise clients. Source: www.skift.com

• In the first half of 2024, Bizzabo reported a 52% increase in customer event portfolios versus H1-2023, reflecting broad expansion of regional and year-round event strategies and increased adoption of hybrid event modules. Source: www.bizzabo.com

• In July 2024, Eventbrite announced a partnership with TikTok enabling event creators to add Eventbrite links directly to TikTok videos for simplified discovery and ticketing, expanding social-commerce channels for ticket sales and creator monetisation. Source: www.eventbrite.com

This report covers the Event Technology market across product types, applications, end-users and geographies with detailed coverage across the following dimensions: software platforms (registration & ticketing, mobile attendee apps, exhibitor portals, analytics dashboards), hardware components (RFID wristbands, access control kiosks, streaming encoders, interactive kiosks), and professional services (deployment, managed-service production, integration and on-site support). Geographic scope includes North America, Europe, Asia-Pacific, South America and Middle East & Africa with country-level profiling for major markets such as United States, United Kingdom, Germany, China, India and Brazil. Application coverage spans corporate conferences, trade shows & exhibitions, live entertainment & concerts, educational events, government functions and virtual summits. For each segment, the report analyses buyer behaviour, procurement cycles, deployment models (SaaS, managed service, hybrid), and vendor selection criteria (integration capability, data governance, sustainability features). The report also quantifies adoption indicators—platform renewal rates, average deal sizes, managed-service uptake—and assesses technology readiness (venue connectivity, 5G availability, AR/VR integration). The scope includes market drivers (hybrid format growth, sponsor ROI demands), restraints (connectivity limitations, integration complexity), opportunities (localized mobile engagement, ESG tooling, sponsorship monetisation) and competitive dynamics (M&A activity, PE-backed rollups, strategic partnerships). Deliverables include regional scorecards, vendor capability matrices, technology maturity maps, use-case ROI models and a 3-year tactical roadmap for technology adoption and commercialisation tailored to enterprise organisers, venue operators and platform investors.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 21682.9 Million |

|

Market Revenue in 2032 |

USD 55633.6 Million |

|

CAGR (2025 - 2032) |

12.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cvent, Eventbrite, Bizzabo, Brella, Swapcard, Splash, Hubb, Aventri, Certain, vFairs, InEvent, ExpoPlatform, Hubb (Enterprise), Attendify, Hopin, Ticketmaster Event Solutions |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |