Reports

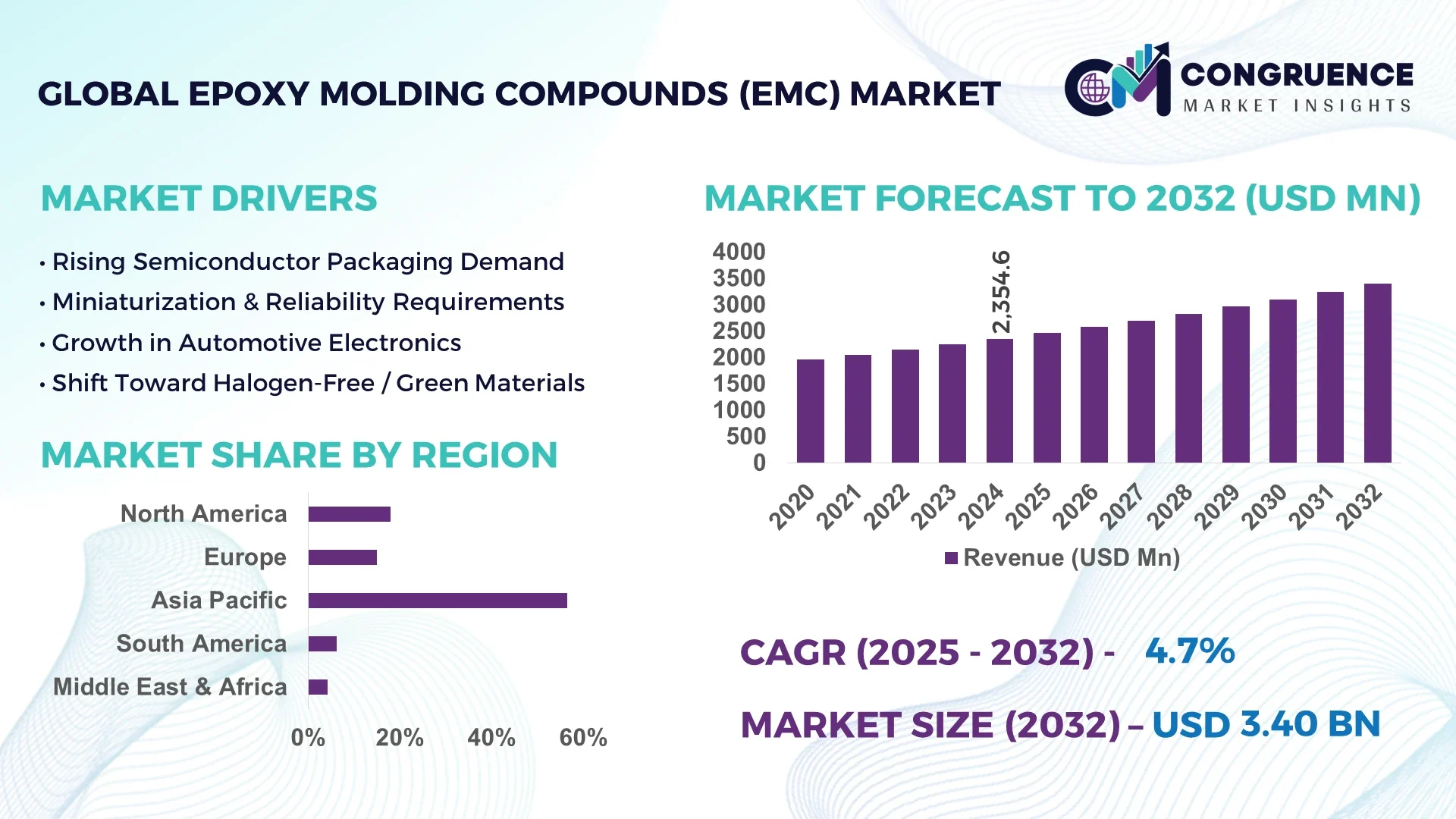

The Global Epoxy Molding Compounds (EMC) Market was valued at USD 2354.59 Million in 2024 and is anticipated to reach a value of USD 3400.08 Million by 2032 expanding at a CAGR of 4.7% between 2025 and 2032.

South Korea remains a pivotal player in the EMC market, driven by its high-volume production capabilities, sustained R&D investments in microelectronic packaging solutions, and a deeply integrated supply chain for semiconductor applications.

The Epoxy Molding Compounds (EMC) market is expanding rapidly due to its essential role in electronic packaging, automotive electronics, and industrial power modules. These thermosetting polymers offer exceptional resistance to heat, chemicals, and mechanical stress, making them ideal for encapsulating semiconductor devices. In 2024, consumer electronics and automotive electronics jointly contributed over 60% of global EMC demand. Technological innovations, including halogen-free and low-stress EMC formulations, are gaining traction due to stricter environmental regulations and the shift toward miniaturized electronics. Regionally, Asia-Pacific leads in consumption owing to the dominance of electronics manufacturing hubs, while North America and Europe are witnessing increased adoption in automotive and aerospace sectors. Future market growth is expected to be influenced by rising EV penetration, demand for advanced driver-assistance systems (ADAS), and expanding 5G infrastructure, where EMCs play a protective role for sensitive components.

Artificial Intelligence (AI) is significantly reshaping the Epoxy Molding Compounds (EMC) Market by revolutionizing how manufacturers approach process control, quality management, and material innovation. One of the most impactful AI applications is predictive modeling, which allows producers to simulate mold flow behaviors and optimize cure cycles, minimizing material wastage and defects. AI algorithms can monitor and analyze large volumes of data generated during the EMC production process, identifying inconsistencies in real-time and triggering automated adjustments. This reduces downtime and enhances the overall efficiency of manufacturing operations.

AI-driven analytics are also accelerating the development of new epoxy formulations tailored for specific applications in semiconductors and automotive electronics. By leveraging machine learning, manufacturers can predict the performance of novel compounds under different thermal and mechanical stresses, expediting R&D cycles. Additionally, AI is enabling enhanced supply chain forecasting, reducing lead times and improving resource allocation for major EMC vendors. The integration of AI in smart factories has further led to improved traceability and compliance with industry standards, particularly in high-reliability sectors like defense and aerospace. As the Epoxy Molding Compounds (EMC) Market becomes more digitally enabled, companies incorporating AI into their production ecosystems are expected to gain a competitive advantage through enhanced productivity, precision, and product consistency.

“In February 2024, a leading semiconductor packaging firm implemented an AI-enabled process optimization system that reduced EMC curing time by 18% and decreased defect rates by 12%, enhancing yield and operational throughput.”

The Epoxy Molding Compounds (EMC) market is shaped by a complex interplay of technological, industrial, and environmental forces. The rising demand for high-performance encapsulants in electronics, especially in semiconductors, sensors, and power modules, continues to propel market expansion. EMCs are increasingly utilized for their superior mechanical, electrical, and thermal properties that support the miniaturization and high-density assembly of modern electronics. Additionally, the transition toward electric vehicles and the adoption of ADAS in automotive manufacturing are major contributors to market growth. Regulatory mandates pushing for halogen-free and eco-friendly formulations are driving R&D investments. However, supply chain fluctuations, raw material price volatility, and stringent quality specifications pose hurdles to consistent growth. Regional dynamics remain strong, with Asia-Pacific emerging as the manufacturing nucleus, while Europe and North America witness increased activity in automotive and industrial electronics.

The continuous evolution of the semiconductor industry and the surge in automotive electronics are key growth drivers for the Epoxy Molding Compounds (EMC) market. In advanced semiconductor packaging, EMCs are essential for protecting ICs from moisture, contaminants, and thermal stress. With the proliferation of compact and high-performance devices—such as smartphones, 5G modules, and memory chips—demand for EMCs has surged. In automotive sectors, EMCs support the durability of components like engine control units (ECUs), battery management systems, and sensors in electric and hybrid vehicles. According to industry data, automotive electronics usage per vehicle has increased by over 15% since 2021, translating into greater EMC consumption. The trend toward electrification and connected mobility continues to open new application avenues for robust, thermally stable encapsulants.

One of the major restraints impacting the Epoxy Molding Compounds (EMC) market is the instability in raw material supply and pricing. Epoxy resins, hardeners, and fillers used in EMC production are largely petroleum-based, making their availability and cost highly sensitive to global crude oil price fluctuations. Moreover, specialty chemicals used in advanced EMC formulations often face supply chain constraints due to geopolitical tensions, export restrictions, or production bottlenecks. For instance, during the first half of 2024, key additives such as antimony trioxide and silica fillers saw price hikes of up to 20% due to reduced output in Asia. This cost pressure directly impacts manufacturers’ margins, limits price flexibility, and can deter smaller players from entering or expanding in the market.

The increasing focus on environmental compliance and sustainable manufacturing is creating significant opportunities in the Epoxy Molding Compounds (EMC) market. As global regulatory bodies push for the elimination of hazardous substances, halogen-free EMC formulations are gaining traction. These environmentally friendly alternatives offer flame retardancy without releasing toxic gases during combustion. Major electronics brands are now mandating the use of RoHS-compliant and halogen-free materials in their supply chains. This trend is particularly strong in Europe and parts of Asia, where environmental standards are strict. Manufacturers investing in bio-based epoxy systems and low-emission curing technologies stand to benefit from premium positioning and broader market access. Furthermore, sustainability-focused government incentives are encouraging R&D toward non-toxic, recyclable EMC solutions.

A persistent challenge in the Epoxy Molding Compounds (EMC) market lies in meeting stringent performance requirements, particularly in high-reliability sectors like aerospace, medical devices, and power electronics. These applications demand EMCs with exceptional long-term thermal stability, moisture resistance, low ionic contamination, and mechanical integrity under variable stress conditions. Achieving these characteristics often involves complex formulations and precise process controls, increasing production complexity and costs. Additionally, qualification cycles in such industries are lengthy, delaying time-to-market for new EMC products. Manufacturers must invest heavily in testing, certification, and compliance documentation to meet international standards like JEDEC, UL 94, and MIL-SPEC, creating entry barriers and slowing down innovation cycles for many players.

Increased Use of Low-Warpage EMCs in High-Density Packages: As chip designs become more compact and integrate higher functionality, warpage during encapsulation has emerged as a significant issue. Low-warpage epoxy molding compounds are seeing a notable rise in adoption across semiconductor packaging lines. These materials minimize deformation in ultra-thin dies and substrates used in fan-out wafer-level packages. In 2024, several leading OSAT providers integrated low-warpage EMCs to support advanced mobile processors and AI chips, reporting up to 25% improvement in final product flatness compared to standard EMCs.

Shift Toward Halogen-Free and Eco-Friendly Formulations: Environmental regulations are pushing manufacturers to move toward halogen-free, low-VOC, and REACH-compliant epoxy molding compounds. In 2024, over 45% of new EMC product launches featured eco-friendly formulations designed for minimal environmental impact. These compounds are increasingly utilized in LED lighting systems, automotive electronics, and smart appliances where compliance with sustainability mandates is critical for global exports and consumer acceptance.

Advanced EMCs for Power Semiconductor Devices: The rising demand for power modules in EVs and industrial applications is driving the development of EMCs with enhanced thermal conductivity and electrical insulation. Manufacturers are focusing on epoxy molding compounds that can sustain operating temperatures above 200°C and ensure dielectric strength for high-voltage components. In 2024, these high-performance EMCs accounted for a growing share of shipments for silicon carbide (SiC) and gallium nitride (GaN) devices, with usage up by nearly 18% year-on-year.

Automation-Driven Efficiency in EMC Dispensing Systems: Automated EMC dispensing equipment is being increasingly adopted to support the precision and consistency required in high-volume semiconductor production. Real-time monitoring and AI-assisted pattern recognition allow for minimal wastage and defect detection in microelectronic encapsulation. In 2024, installation of fully automated EMC lines grew by 22% across major facilities in Taiwan and Japan, cutting process cycle time by 15% while improving throughput and first-pass yield metrics.

The Epoxy Molding Compounds (EMC) market is segmented based on type, application, and end-user industries, reflecting the broad and specialized use cases across the electronics and automotive sectors. In terms of types, the market includes materials such as general-purpose EMCs, low-stress EMCs, and high thermal conductivity compounds, each tailored to specific performance demands. Applications span semiconductors, sensors, LEDs, and power modules, with growing emphasis on compact, high-performance electronic assemblies. Among end-users, consumer electronics, automotive, and industrial sectors drive the bulk of demand, while medical electronics and aerospace sectors are contributing niche but expanding uses. Rapid advancements in miniaturized electronic devices and electric mobility are reshaping these segments by increasing the need for EMCs with enhanced mechanical, thermal, and environmental resistance characteristics.

The market for epoxy molding compounds includes several material types, each engineered for distinct functionalities. General-purpose EMCs are widely used due to their balance of mechanical strength and processability, making them the leading product type across standard semiconductor packaging lines. Low-stress EMCs are gaining momentum, especially in applications involving thin dies and wafer-level chip-scale packaging, where mechanical stress during curing must be minimized. This type is currently the fastest-growing segment, supported by increasing demand for mobile and wearable devices that require ultra-thin profiles. High thermal conductivity EMCs, often filled with alumina or other ceramics, are crucial in power electronics where heat dissipation is vital for performance and reliability. Specialty EMCs, such as optically clear or UV-resistant types, serve niche areas like LED encapsulation and automotive lighting systems. While their market share is comparatively smaller, these variants are essential for high-reliability applications.

Among applications, semiconductor packaging dominates the Epoxy Molding Compounds (EMC) market due to its extensive use in protecting integrated circuits from environmental and mechanical stress. This segment benefits from the widespread adoption of surface-mount technology and flip-chip configurations in consumer electronics. The fastest-growing application is power module encapsulation, driven by the rise in electric vehicles and renewable energy infrastructure. These modules require EMCs with high thermal stability and insulation, making advanced compounds increasingly essential. LED packaging also represents a significant application area, particularly in lighting and automotive electronics, where EMCs provide durability and optical clarity. Additionally, EMCs are gaining traction in sensor applications, especially in automotive safety systems, where reliability under fluctuating temperature and moisture conditions is critical. Overall, applications are diversifying in response to the trend of electronics integration into non-traditional environments and systems.

Consumer electronics remain the primary end-user segment in the Epoxy Molding Compounds (EMC) market, reflecting the vast production of smartphones, tablets, and computing devices requiring robust semiconductor protection. This segment leverages EMCs for system-in-package (SiP) and multi-chip module (MCM) designs, which demand both miniaturization and performance. The automotive industry is the fastest-growing end-user, fueled by the increasing electronic content in modern vehicles, from infotainment systems to battery management and autonomous driving sensors. Demand for EMCs in this sector is reinforced by the surge in electric vehicles and the global move toward cleaner transportation solutions. Industrial automation and power electronics sectors are also significant consumers, utilizing EMCs in motor control units, inverters, and relay systems. While smaller in scale, the aerospace and healthcare electronics sectors are emerging users due to the reliability and environmental protection EMCs offer under extreme conditions.

Asia-Pacific accounted for the largest market share at 56.4% in 2024, however, Region North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

Asia-Pacific’s dominance in the Epoxy Molding Compounds (EMC) market is attributed to its established electronics manufacturing infrastructure and high-volume semiconductor production, particularly in countries such as China, Taiwan, and South Korea. Major EMS (electronics manufacturing services) providers operate large-scale facilities in the region, ensuring constant demand for EMCs used in chip packaging and sensor protection.

Globally, the Epoxy Molding Compounds (EMC) market is experiencing dynamic shifts across regions, driven by industry-specific consumption trends, regional regulatory frameworks, and localized innovation hubs. North America’s acceleration is fueled by rapid digitization in the automotive and aerospace sectors, while Europe is witnessing regulatory-driven demand for halogen-free formulations. Meanwhile, South America and the Middle East & Africa are gaining ground due to industrial diversification and favorable trade incentives. Each region presents a unique mix of end-user concentration and technology adoption pace, reshaping competitive strategies for global and regional EMC suppliers.

Rising Automotive and Aerospace Reliance on High-Reliability Encapsulation Materials

In 2024, the Epoxy Molding Compounds (EMC) market in this region held a market share of 18.7%, primarily driven by strong demand from automotive, aerospace, and defense electronics manufacturers. With EV and ADAS penetration on the rise, the need for thermally stable and electrically insulative materials is growing across critical systems such as inverters and battery control modules. Federal incentives for semiconductor manufacturing are accelerating localized production, increasing reliance on domestic EMC suppliers. Technological advancements in AI-driven quality monitoring and robotics are enhancing EMC dispensing precision, while clean energy policies and Buy America provisions are reshaping procurement behaviors among OEMs. The presence of regulatory bodies like the EPA is also fostering a shift toward halogen-free and low-emission molding compounds.

Green Packaging Regulations Fuel Demand for Sustainable EMC Solutions

The Epoxy Molding Compounds (EMC) market in this region contributed approximately 14.9% of global volume in 2024, led by Germany, the UK, and France. Regulatory frameworks like RoHS and REACH have pushed local manufacturers to adopt eco-friendly EMC formulations, especially in LED lighting and EV battery control systems. Major automotive players are increasing their investment in in-house semiconductor production, requiring durable, compliant encapsulation materials. The shift toward Industry 4.0 has further elevated the adoption of smart EMC dispensing solutions using digital twins and real-time data analytics. Sustainability goals are creating new demand for bio-based alternatives, while growing investment in electric public transportation infrastructure is reinforcing application diversity across high-voltage electronics.

High-Volume Electronics Manufacturing Drives Regional EMC Dominance

Holding the highest market share globally at 56.4%, this region is home to the world's largest consumers of Epoxy Molding Compounds (EMC), including China, South Korea, Japan, and Taiwan. These countries host extensive semiconductor fabs, EMS plants, and automotive electronics hubs that heavily depend on EMC for chip protection. Advanced infrastructure and government-led digital transformation projects are accelerating demand for next-gen EMC materials with low warpage and high thermal resistance. The region is also witnessing rapid adoption of EMCs in renewable energy inverters and smart grid systems. Tech clusters in Shenzhen, Seoul, and Tokyo are key innovation centers for high-density chip packages and AI-integrated manufacturing, supporting continuous market expansion.

Emerging Demand from Automotive Electronics and Energy Infrastructure

South America accounted for approximately 4.6% of the global Epoxy Molding Compounds (EMC) market in 2024, with Brazil and Argentina emerging as key demand centers. The expansion of domestic automotive manufacturing and the modernization of electrical infrastructure have triggered new EMC applications in power modules and ECU systems. Brazil's push for energy self-reliance and grid upgrades is also increasing demand for thermally conductive EMCs. Trade agreements with North American and European electronics companies are improving EMC import efficiency and availability. Government incentives for smart city projects and digital manufacturing adoption are fostering a nascent but growing market for high-specification encapsulation materials in industrial and telecom sectors.

Infrastructure Modernization and Diversified Electronics Fuel EMC Uptake

This region held an estimated market share of 5.4% in 2024, with demand largely centered in the UAE, Saudi Arabia, and South Africa. The region’s diversification from oil to technology and renewable sectors is creating fresh EMC demand in solar inverters, smart meters, and electronic control systems in industrial automation. National infrastructure plans are boosting investments in electronics manufacturing hubs and fostering innovation in encapsulation technologies. Technological modernization across oil & gas instrumentation is also driving adoption of EMCs with superior thermal and chemical resistance. New trade agreements and tax-friendly free zones are incentivizing local assembly of automotive and consumer electronics, contributing to long-term EMC demand growth.

China – 38.1% market share

High production capacity and robust semiconductor and electronics ecosystem across Guangdong and Jiangsu provinces.

South Korea – 12.6% market share

Strong end-user demand from major semiconductor packaging companies and sustained government investment in chip technology R&D.

The Epoxy Molding Compounds (EMC) market is characterized by moderate to high competition, with over 30 active global and regional players offering a diverse range of high-performance encapsulation materials. The competitive landscape is shaped by innovation in material science, expansion into new application domains, and the need for regulatory compliance in eco-friendly formulations. Key market participants are focused on enhancing their portfolios with halogen-free, low-warpage, and thermally conductive EMCs to meet evolving end-user requirements in semiconductors, automotive electronics, and power modules.

Strategic initiatives such as joint ventures, mergers, and product collaborations are increasingly common. In 2024, several EMC manufacturers entered into technology-sharing agreements with semiconductor fabrication firms to co-develop next-generation molding solutions. Investment in R&D is intensifying, particularly in AI-assisted production lines and predictive quality analytics for EMC applications. Additionally, regional expansion into emerging markets in South America and the Middle East is being pursued to capitalize on untapped demand. Companies with vertical integration across resin formulation, molding technologies, and dispensing automation are gaining a competitive edge through cost efficiency and process consistency. With ongoing material innovation and tightening environmental standards, competition is likely to remain dynamic and innovation-driven.

Sumitomo Bakelite Co., Ltd.

Hysol Huawei Electronics Co., Ltd.

Panasonic Holdings Corporation

Henkel AG & Co. KGaA

Shin-Etsu Chemical Co., Ltd.

Kyocera Corporation

Nagase & Co., Ltd.

Hitachi Chemical Company, Ltd.

Namics Corporation

Jiangsu Sanmu Group Co., Ltd.

Technological innovation is playing a pivotal role in reshaping the Epoxy Molding Compounds (EMC) market, particularly in the development of materials engineered to meet the growing demands of miniaturization, thermal management, and environmental compliance. Manufacturers are increasingly integrating nano-fillers, such as nano-silica and alumina, to enhance thermal conductivity while maintaining the compound's flowability and moldability. These modified compounds are being used extensively in power devices and automotive control systems that require high thermal dissipation capabilities.

Advancements in halogen-free EMCs have led to the commercial release of products that not only comply with RoHS directives but also exhibit improved flame retardancy and moisture resistance. The integration of AI and machine learning into EMC formulation and production is also transforming the manufacturing landscape. AI-enabled systems optimize cure cycles, material dispersion, and stress distribution, resulting in fewer defects and improved reliability for advanced semiconductor packages.

EMC dispensing technologies have progressed as well, with high-precision, automated systems now capable of uniform encapsulation on microchips and complex multi-chip modules. UV-curable EMCs and optically clear variants are being explored for sensor applications in wearable electronics and medical diagnostics. As semiconductor nodes continue to shrink, the demand for ultra-low stress, high adhesion EMCs with excellent mold release characteristics will become even more critical.

• In May 2024, Sumitomo Bakelite launched a new EMC grade designed specifically for high-power SiC modules, offering thermal conductivity above 2.0 W/mK and increased resistance to delamination under extreme thermal cycling.

• In October 2023, Shin-Etsu Chemical announced the expansion of its epoxy molding facility in Japan, increasing production capacity by 20% to meet rising demand in the automotive electronics sector.

• In March 2024, Henkel introduced a low-halogen EMC line featuring improved mold flow and reduced warpage characteristics, targeting high-density packaging applications in mobile devices.

• In December 2023, Panasonic unveiled a halogen-free, low-CTE EMC product optimized for thin wafer applications, reporting a 30% improvement in thermal stress resistance compared to conventional offerings.

The Epoxy Molding Compounds (EMC) Market Report provides a comprehensive analysis of the market’s structural components, covering various segmentation layers including types, applications, and end-user industries. It evaluates EMC types such as general-purpose, low-stress, high thermal conductivity, and halogen-free formulations used across diverse electronic assemblies and devices. Applications analyzed span semiconductor packaging, LED encapsulation, sensor modules, and power electronics.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering region-specific insights into consumption patterns, regulatory environments, and supply chain structures. It assesses the dominant roles of China and South Korea in production, alongside emerging growth opportunities in Brazil, UAE, and India.

Industry focus areas include consumer electronics, automotive, industrial automation, aerospace, and renewable energy systems, highlighting evolving demands for high-reliability encapsulation materials. The report also explores how AI, automation, and material science advancements are driving performance enhancement and process efficiency in EMC manufacturing. It incorporates emerging market segments such as UV-curable EMCs and eco-friendly bio-based alternatives. By integrating qualitative and quantitative insights, the report delivers strategic intelligence designed to guide manufacturers, investors, and policymakers across the global value chain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2354.59 Million |

|

Market Revenue in 2032 |

USD 3400.08 Million |

|

CAGR (2025 - 2032) |

4.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Sumitomo Bakelite Co., Ltd., Hysol Huawei Electronics Co., Ltd., Panasonic Holdings Corporation, Henkel AG & Co. KGaA, Shin-Etsu Chemical Co., Ltd., Kyocera Corporation, Nagase & Co., Ltd., Hitachi Chemical Company, Ltd., Namics Corporation, Jiangsu Sanmu Group Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |