Reports

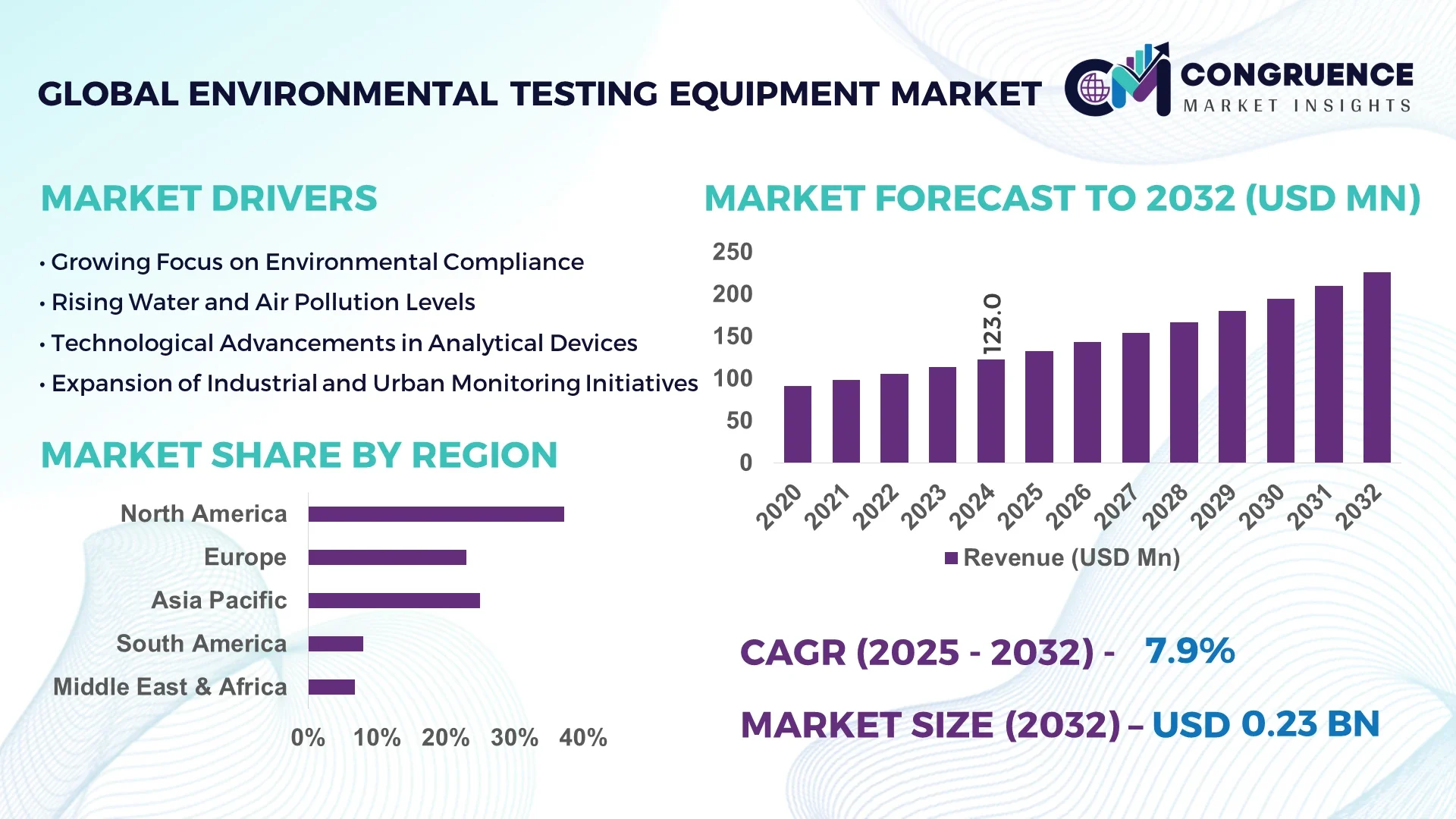

The Global Environmental Testing Equipment Market was valued at USD 123.0 Million in 2024 and is anticipated to reach a value of USD 226.0 Million by 2032, expanding at a CAGR of 7.9% between 2025 and 2032.

In North America, the dominant country in this market demonstrates exceptional production capacity with numerous advanced manufacturing hubs dedicated to sensor arrays, chromatography analyzers, and portable field units. Investment levels remain robust, with several government–industry joint ventures funding state-of-the-art laboratory infrastructure and regional R&D centers focusing on next-generation contaminant detection technologies. Key industry applications include large-scale environmental monitoring, regulatory compliance testing, and industrial emissions analysis. Technological advancements such as the integration of miniaturized IoT-enabled sensors and rapid-response spectrometers are being piloted across U.S.-based test facilities, reinforcing this country’s leadership in high-end instrumentation.

Globally, the Environmental Testing Equipment Market spans multiple industry sectors—most notably government testing services, municipal water and air quality control, industrial facilities, and environmental laboratories. Laboratories and government agencies typically contribute over 40% of equipment adoption due to comprehensive compliance testing needs. Recent product innovations include self-calibrating IoT water-quality monitors, blockchain-integrated soil testing devices, and microplastic-detection infrared analyzers tailored for remote sensing. Regulatory drivers like EPA, ISO 14001, and REACH standards continue to enforce stringent monitoring protocols, catalyzing demand for high-precision, real-time instruments. Economically, expanded infrastructure and urbanization in Asia-Pacific are contributing to rising regional consumption; portable and remote testing models are seeing double-digit volume increases due to field applications in construction, mining, and energy projects. Emerging trends highlight AI-enabled predictive analytics, solar-powered autonomous stations, and multi-parameter handheld units—positioning the market toward remote, sustainable, and data-driven environmental oversight.

Artificial intelligence (AI) is playing a pivotal role in enhancing the Environmental Testing Equipment Market by improving analytical accuracy, reducing manual labor, and enabling real-time data interpretation. Modern environmental testing systems now use AI-powered algorithms to detect patterns in air, water, and soil datasets—allowing anomalies such as microplastic presence, particulate spikes, or contaminant surges to be flagged without human intervention. These systems can cross-reference real-time readings against historical baselines and regulatory thresholds, minimizing false positives and optimizing equipment calibration schedules through predictive maintenance.

In industrial and municipal testing facilities, AI has reduced data-processing time by up to 60%, enabling faster turnaround and operational efficiency. Machine learning models integrated into chromatography and spectroscopy platforms continuously refine detection limits based on cumulative sample data, enhancing both sensitivity and specificity. On-site portable devices leverage embedded AI to perform edge analytics—providing instant pass/fail assessments and alerting operators only when intervention is needed, streamlining field operations and reducing the volume of data transmitted to central servers.

Furthermore, control systems in laboratory-grade instruments now include AI-based diagnostic modules that monitor system health in real time. These modules predict component degradation—such as detector lifespan or pump performance—allowing preemptive replacements and reducing downtime by approximately 25%. Cloud-connected platforms utilize AI-driven dashboards offering trend analysis, cross-site comparison, and compliance reporting across multiple locations, transforming environmental testing into a continuous, adaptive service rather than periodic manual audits.

“In mid‑2024, a leading U.S. laboratory integrated an AI‑enhanced spectrometer module that improved microplastic detection sensitivity by 30% and reduced sample processing time by 45% in water quality assessments.”

The Environmental Testing Equipment Market is experiencing increased demand for portable, IoT-enabled testing devices. These units offer rapid on-site analysis with immediate digitized outputs, which is critical for construction and environmental remediation sectors. In 2024, shipments of portable water-testing kits grew by 22% in North America and Europe. Manufacturers are integrating IoT modules capable of transmitting sample data directly to centralized dashboards, reducing sample turnaround time by up to 35%. This shift is particularly relevant for industries operating in remote locations—such as mining and oil & gas—where field-based, real-time testing reduces operational delays. The ability to perform instant compliance checks supports faster decision-making and cost reduction in logistics and lab fees, advancing the Environmental Testing Equipment Market’s adoption of decentralized testing solutions.

The deployment of high-precision analytical instruments—such as mass spectrometers and high-resolution chromatographs—continues to challenge the Environmental Testing Equipment Market due to significant upfront and maintenance costs. For example, a new generation portable GC-MS system may cost between USD 150,000 and 200,000, excluding annual maintenance which can run to over 10% of purchase price. This capital intensity limits procurement to larger enterprises and government labs, while small-to-mid‑size businesses often defer upgrades or opt for rental models. In emerging markets, inadequate budgets restrict adoption, slowing penetration of advanced systems. Complex compliance regulations amplify the need for certified calibration and operator training, further increasing total cost of ownership and posing a label barrier in scaling capabilities across diverse end users.

Growing investment in renewable energy and industrial waste treatment creates untapped potential within the Environmental Testing Equipment Market. Specifically, biofuel production facilities, solar farms, and wastewater treatment plants require specialized contaminant analysis—ranging from heavy metals to organic residuals. In 2024, over 500 new installations of solar farms and biogas units in Europe initiated dedicated environmental testing protocols. Such facilities need multi-parameter instruments capable of detecting a range of contaminants, opening opportunities for manufacturers to develop modular platforms. Moreover, municipal waste-to-energy projects in Asia-Pacific are forecasting testing module orders with 15–18 month lead times—unprecedented in past cycles. This vertical expansion allows equipment providers to customize solutions for emerging green industries and support regulatory compliance frameworks.

The Environmental Testing Equipment Market faces growing complexity due to divergent regulatory frameworks across geographic regions. Instruments compliant with U.S. EPA standards may not meet EU or APAC norms (e.g., differing detection limits for PM2.5/PM10 or heavy metals in water tests). As a result, manufacturers often need to release multiple versions of the same instrument, adding costs and prolonging time-to-market. Additionally, frequent updates to standards—like the December 2023 revision of the EU’s Drinking Water Directive—create uncertainty. Equipment needs constant revalidation to ensure compliance, which can involve redesigning detection modules or updating firmware. These synchronization delays cost manufacturers up to 6 months in product rollout cycles and complicate global sales strategies, slowing the pace at which the Environmental Testing Equipment Market can respond to international demand.

Growth in Edge Analytics Integration: In 2024–2025, over 40% of new environmental testing instruments incorporated edge-AI capabilities. These systems process data on-device—accelerating anomaly detection in air and water samples—and reduce cloud data traffic by approximately 30%, enhancing operational efficiency in remote deployments.

Surge in Multi‑Parameter Assay Systems: Equipment capable of analyzing multiple environmental factors (e.g., pH, dissolved oxygen, conductivity) in a single test saw sales growth of 18%. Such modular platforms are being adopted across municipal and industrial sectors to streamline compliance testing and reduce laboratory burden.

Expansion of Subscription‑Based Data Services: Approximately 25% of new instrument offerings now include software-as-a-service packages. Users benefit from ongoing software updates, calibration monitoring, and compliance reporting tools, shifting from one-off purchases to recurring, service-driven models while ensuring regulatory alignment.

Advance of Contactless and Remote Monitoring Hardware: The adoption of contactless sampling probes and solar-powered remote stations expanded 15% across Asia-Pacific construction and mining sites. These innovations support continuous environmental surveillance, eliminating the need for personnel deployment and reducing sample collection costs by up to 20%.

The Environmental Testing Equipment Market is strategically segmented based on type, application, and end-user, providing a comprehensive understanding of demand dynamics across sectors. This segmentation enables stakeholders to evaluate technology adoption trends, regulatory dependencies, and equipment customization preferences. In terms of type, the market encompasses a diverse array of instruments including mass spectrometers, gas chromatographs, pH meters, turbidity meters, and sensors. Application-wise, the market serves domains such as water quality testing, air pollution monitoring, soil contamination analysis, and wastewater treatment. End-users span a wide range—from government laboratories and municipal utilities to industrial facilities and research organizations—each with distinct testing standards and operational needs. This multi-dimensional view offers insights into evolving procurement patterns, increasing cross-sector demand for real-time diagnostics, and the rising emphasis on portable, modular testing platforms that align with both compliance and operational efficiency requirements.

Environmental testing equipment types include gas chromatography instruments, mass spectrometry systems, UV-visible spectrometers, pH and conductivity meters, turbidity meters, and portable field analyzers. Among these, gas chromatography instruments hold a leading position due to their precision in detecting complex organic compounds in air and water samples. These systems are widely used in environmental compliance testing by public and private laboratories, especially in developed regions with stringent pollutant control frameworks.

The fastest-growing type is portable multi-parameter analyzers. Their rapid deployment capabilities, ease of use in remote locations, and integration with IoT and AI technologies make them increasingly favored for field-based, real-time testing across industrial and municipal projects. Their use has expanded in disaster response, construction site compliance checks, and rural area water testing where lab access is limited.

Other notable types include spectrometers and sensors, which serve niche roles in high-frequency monitoring systems and mobile stations. Turbidity and DO meters are common in aquatic and wastewater environments, while pH meters remain indispensable in soil and effluent assessments. These instruments, while individually limited in scope, together form critical components in comprehensive environmental diagnostics.

The Environmental Testing Equipment Market addresses a variety of application areas, including water testing, air quality monitoring, soil contamination analysis, and industrial effluent testing. Among these, water testing leads the segment, primarily due to global mandates surrounding drinking water safety, wastewater discharge regulations, and the increased prevalence of contamination events. Water quality testing equipment is widely deployed by both municipal authorities and private water treatment providers.

Air quality monitoring is the fastest-growing application area. This growth is fueled by tightening global emissions regulations, urbanization, and public health initiatives addressing particulate matter and gaseous pollutants. The expansion of real-time air monitoring systems in both indoor and outdoor environments, including smart city infrastructure and industrial zones, is contributing to this surge.

Soil analysis remains a critical application in agricultural and land remediation contexts, especially where historical contamination or pesticide runoff poses ecological risks. Effluent and sludge testing, while smaller in volume, is highly specialized and essential in energy, manufacturing, and chemical processing sectors, where monitoring discharge is closely regulated.

Key end-users in the Environmental Testing Equipment Market include government laboratories, municipal utilities, industrial manufacturers, research institutions, and environmental consultancies. Government and regulatory laboratories represent the leading end-user segment, driven by consistent public sector investments in environmental oversight, pollution surveillance, and statutory testing obligations. These institutions are often equipped with high-end analytical systems and serve as reference bodies for environmental compliance.

The fastest-growing end-user group is industrial manufacturing facilities, particularly in sectors like oil and gas, chemicals, construction, and renewable energy. Their increased investment in on-site environmental monitoring is being driven by evolving compliance requirements, sustainability mandates, and stakeholder expectations around ESG (Environmental, Social, Governance) transparency.

Municipal utilities continue to be core consumers, especially for water and wastewater quality testing. Academic and research organizations are also active participants, contributing to instrument validation, innovation, and early adoption of next-generation equipment. Environmental consulting firms, though smaller in procurement scale, are essential for deploying portable and mobile units across diversified client projects, especially in remediation and impact assessment assignments.

North America accounted for the largest market share at 37.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2025 and 2032.

North America’s lead is underpinned by advanced laboratory infrastructure, strong regulatory compliance frameworks, and consistent public sector funding for environmental surveillance. Meanwhile, Asia-Pacific's surge is driven by rapid industrialization, infrastructure development, and rising environmental awareness in countries like China and India. Regions such as Europe and Latin America are also witnessing steady adoption of digital testing technologies and portable instrumentation, contributing to the global expansion of the Environmental Testing Equipment Market.

North America captured approximately 37.2% of the global Environmental Testing Equipment Market in 2024. The demand is primarily driven by key industries such as oil & gas, chemicals, construction, and municipal utilities, which require continuous environmental monitoring and strict adherence to federal compliance regulations. The U.S. Environmental Protection Agency (EPA) updated air and water quality standards in early 2024, accelerating public and private investment in high-precision analyzers and mobile test units. Technological advancements such as AI-integrated field sensors and cloud-connected environmental diagnostics are widely adopted across sectors. Additionally, government-funded green infrastructure programs are promoting advanced waste and water testing technologies, reinforcing market expansion.

Europe held a market share of approximately 29.6% in 2024 within the Environmental Testing Equipment Market. Major contributing countries include Germany, France, and the United Kingdom, where sustainability goals under the EU Green Deal and REACH regulations are propelling demand for cutting-edge environmental testing solutions. The European Chemicals Agency and local environmental ministries continue to enforce rigorous pollution control standards, prompting industries to upgrade to smart testing platforms. The adoption of digital water testing systems, AI-enhanced sensors, and automated lab equipment is increasing across environmental labs and utility providers. The integration of environmental IoT (EIoT) in smart cities further bolsters this region’s technological momentum.

Asia-Pacific ranked as the fastest-growing region in terms of market volume in the Environmental Testing Equipment Market. China, India, and Japan are the top consumers due to rapid urbanization, rising environmental consciousness, and expanding industrial sectors. Government-led infrastructure development—such as India's Smart Cities Mission and China’s environmental control reforms—are fueling demand for air, water, and soil testing equipment. Regional innovation hubs like Shenzhen, Tokyo, and Bengaluru are fostering R&D in AI-powered and IoT-integrated testing technologies. Additionally, mobile testing vans and drone-enabled monitoring are becoming mainstream in rural and peri-urban projects, significantly boosting the reach and flexibility of environmental monitoring.

South America’s Environmental Testing Equipment Market is gaining momentum with key participation from Brazil and Argentina. Brazil accounts for the largest share within the region, supported by increasing infrastructure investments and regulatory revisions targeting industrial emissions and waste discharge. Energy sector projects, especially in hydroelectric and biofuel production, are deploying high-end monitoring equipment to meet compliance requirements. Argentina is making strides through government-backed initiatives focused on river basin testing and urban pollution control. Regional trade policies promoting green technology imports are easing procurement hurdles. Portable testing instruments are gaining traction in construction and environmental consulting sectors due to rugged terrain and remote site requirements.

The Middle East & Africa region is witnessing growing demand for environmental testing equipment, particularly in sectors like oil & gas, construction, and urban development. Countries such as the United Arab Emirates and South Africa are leading adoption through investments in environmental safety programs and industrial modernization. The UAE's focus on sustainable development is driving installation of real-time air and water monitoring stations across urban zones. In South Africa, mining and energy sector reforms are prompting large-scale deployment of emission and effluent testing devices. Regional trends show a gradual shift toward digital transformation, with emphasis on remote data access and AI-supported analysis platforms. Local regulatory updates and international trade collaborations are facilitating market access and innovation.

United States – 32.4% Market Share

High production capacity, stringent regulatory mandates, and continuous investment in smart monitoring infrastructure.

China – 21.7% Market Share

Strong end-user demand from industrial manufacturing, rapid infrastructure growth, and rising focus on environmental compliance.

The Environmental Testing Equipment Market is characterized by a moderately consolidated competitive landscape, with over 40 active global players engaged in manufacturing, distribution, and innovation. The market includes both well-established instrumentation firms and agile technology startups introducing next-generation environmental diagnostic tools. Leading companies are continuously pursuing strategic partnerships and product innovation to strengthen their market positions. Over the past 18 months, more than 25 new product launches have been recorded, focusing on portable testing kits, multi-parameter monitoring devices, and AI-integrated platforms.

Key players are actively expanding their geographic presence by establishing new production and service centers in high-growth regions such as Asia-Pacific and the Middle East. Additionally, a notable rise in strategic acquisitions and collaborations is shaping the competitive environment—particularly in the areas of cloud-based environmental monitoring and smart sensor development. Manufacturers are heavily investing in R&D to enhance equipment precision, reduce sampling time, and meet the rising demand for remote, automated solutions. Innovation is centered around real-time monitoring systems, modular platforms, and contactless testing technology, which are rapidly gaining traction across multiple industries including municipal utilities, construction, energy, and manufacturing. The competition is intensifying as companies differentiate through speed, digital integration, and regulatory adaptability.

Agilent Technologies

Shimadzu Corporation

Thermo Fisher Scientific Inc.

PerkinElmer Inc.

Horiba Ltd.

Merck KGaA

Waters Corporation

Bruker Corporation

Danaher Corporation

Eurofins Scientific SE

Analytik Jena GmbH

Metrohm AG

Hanna Instruments

Xylem Inc.

Endress+Hauser Group

The Environmental Testing Equipment Market is undergoing rapid technological transformation, primarily influenced by automation, digital integration, and data-centric advancements. One of the most significant innovations is the integration of AI and machine learning algorithms into testing platforms, enabling real-time pattern recognition, anomaly detection, and predictive diagnostics. These technologies reduce testing time by up to 60% while enhancing sensitivity across a broad range of environmental parameters including air particulates, heavy metals, and microplastics.

IoT-enabled sensor networks are increasingly utilized to enable continuous environmental monitoring. These smart sensors, often installed in remote or urban infrastructure, provide live data to centralized platforms and reduce the need for manual sampling. Data transmission is typically cloud-based, secured through blockchain protocols for traceability and compliance tracking. Additionally, portable and handheld multi-parameter analyzers are replacing bulky laboratory equipment, providing on-site results with high accuracy and lower calibration needs.

Laser-induced breakdown spectroscopy (LIBS) and Fourier-transform infrared spectroscopy (FTIR) are being incorporated into compact testing systems to detect a wider array of pollutants. In parallel, solar-powered autonomous testing stations have emerged as sustainable alternatives for field deployment in areas with limited infrastructure. Furthermore, the development of bio-compatible and biodegradable testing components is enhancing environmental sustainability. Software-as-a-service (SaaS) models are also gaining popularity, enabling remote instrument management, automated reporting, and cross-location data benchmarking. These advancements collectively redefine the scope and capabilities of modern environmental testing technologies, aligning with the demands of digitization, efficiency, and global compliance.

• In March 2024, Thermo Fisher Scientific launched a compact, AI-powered water quality analyzer capable of detecting 25 contaminants simultaneously within 8 minutes. This device has been deployed across municipal facilities in Europe and North America to support high-throughput water testing protocols.

• In July 2023, Agilent Technologies announced the opening of a 15,000-square-foot Environmental Innovation Lab in Singapore. The facility focuses on the development of real-time air and soil testing technologies, including sensors optimized for industrial waste emissions.

• In January 2024, Shimadzu Corporation introduced its fully automated gas chromatography unit with embedded IoT connectivity and blockchain-backed traceability. The new system is currently being piloted by environmental agencies in Japan and India.

• In October 2023, Xylem Inc. launched a drone-integrated surface water testing module capable of transmitting data over 20 kilometers. This technology was adopted for river pollution surveillance in remote parts of Southeast Asia.

The Environmental Testing Equipment Market Report provides a comprehensive evaluation of the global market's structure, segmentation, and emerging opportunities. Covering a wide array of instruments including spectrometers, chromatographs, sensors, and portable analyzers, the report categorizes the market by type, application, end-user, and region. Application areas include air quality testing, water analysis, soil contamination monitoring, and effluent assessments—each shaped by distinct regulatory and operational factors.

Geographically, the report addresses insights across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, capturing variations in technology adoption, regulatory standards, and consumption trends. The report outlines evolving end-user demands from sectors such as government laboratories, municipal utilities, industrial manufacturing, and research institutions, reflecting the diverse range of compliance and diagnostic requirements.

Additionally, the report examines cutting-edge innovations like AI-enabled diagnostics, IoT-powered field units, and cloud-based monitoring systems. Special attention is given to mobile laboratories, solar-powered autonomous stations, and bio-integrated sensors, which represent growing niches within the broader market. The analysis also highlights strategic market moves—such as M&A activity, regional expansions, and product diversification—helping stakeholders assess competition and plan market entry or expansion. Overall, the report provides decision-makers with a detailed yet strategic overview of the Environmental Testing Equipment Market's current capabilities and future trajectory.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Environmental Testing Equipment Market |

| Market Revenue (2024) | USD 123.0 Million |

| Market Revenue (2032) | USD 226.0 Million |

| CAGR (2025–2032) | 7.9 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Market Drivers and Challenges, Regional Outlook, Segment Analysis, Competitive Landscape, Technology Trends, Strategic Insights |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Agilent Technologies, Shimadzu Corporation, Thermo Fisher Scientific Inc., PerkinElmer Inc., Horiba Ltd., Merck KGaA, Waters Corporation, Bruker Corporation, Danaher Corporation, Eurofins Scientific SE, Analytik Jena GmbH, Metrohm AG, Hanna Instruments, Xylem Inc., Endress+Hauser Group |

| Customization & Pricing | Available on Request (10% Customization is Free) |