Reports

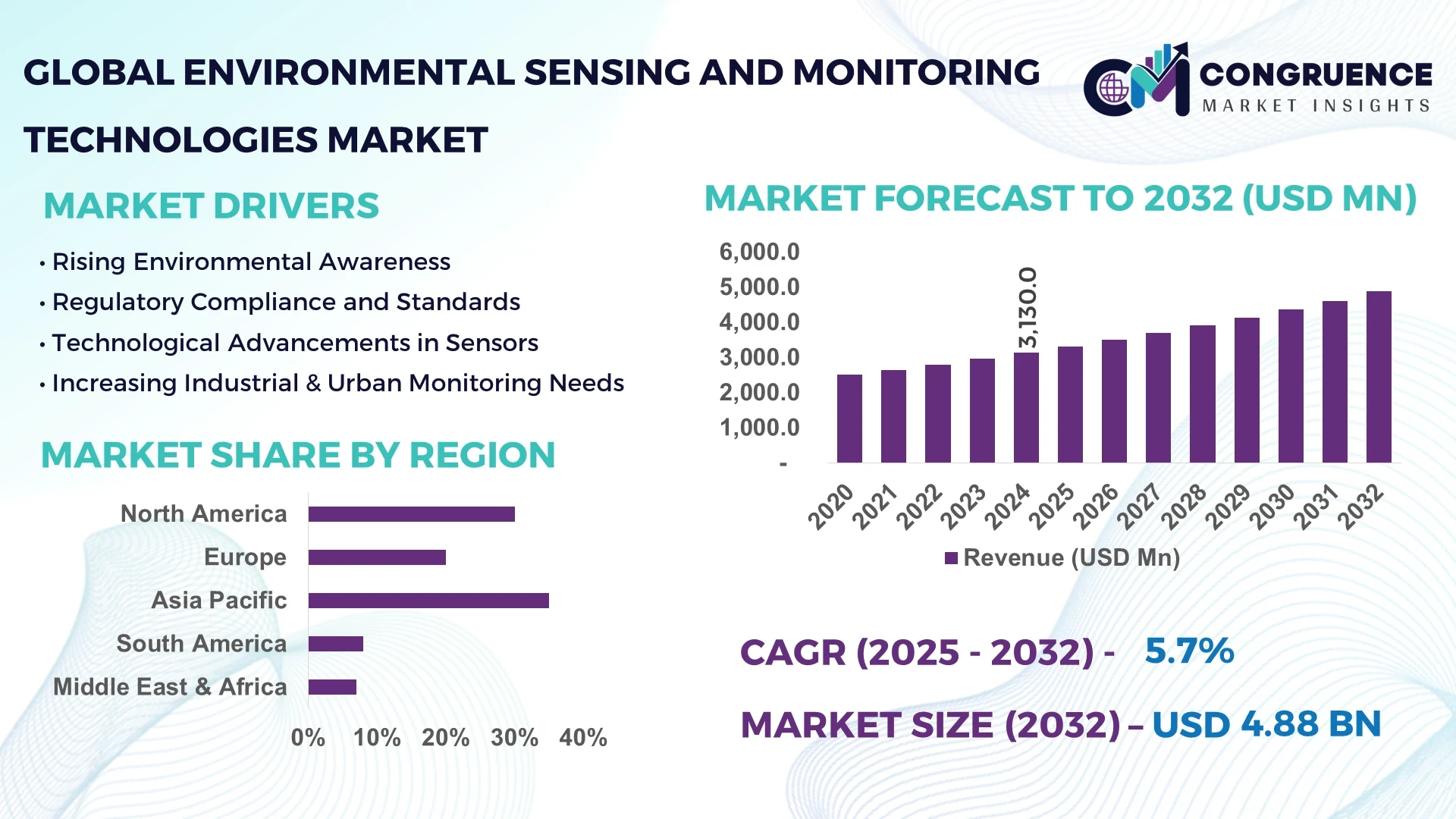

The Global Environmental Sensing and Monitoring Technologies Market was valued at USD 3,130.0 Million in 2024 and is anticipated to reach a value of USD 4,876.9 Million by 2032 expanding at a CAGR of 5.7% between 2025 and 2032. This growth is supported by accelerating demand for real-time environmental data across industries for compliance, optimization, and predictive analytics.

In China, which leads in this domain, production capacity for advanced air quality and water-quality sensors has reached over 12 million units annually as of 2024. Domestic firms and state-led consortia are driving investment exceeding USD 450 million in sensor R&D during 2023–2024 alone. Key usages include continuous emission monitoring in industrial zones, precision agriculture applications, and smart-city infrastructure deployment. Technological advancements such as MEMS micro-sensors, IoT integration, and edge analytics are being commercialized by leading Chinese firms, with over 30% of deployed monitors now offering in-built AI anomaly detection capabilities.

Market Size & Growth: Valued at USD 3,130 Million in 2024, projected to reach USD 4,876.9 Million by 2032, expanding at a CAGR of 5.7% — driven by regulatory mandates and IoT adoption.

Top Growth Drivers: Stricter emissions standards (25 %), increased industrial automation (18 %), urban monitoring deployments (12 %).

Short-Term Forecast: By 2028, average sensor deployment cost is expected to fall by 15 %, improving ROI and enabling broader adoption.

Emerging Technologies: AI-powered anomaly detection; edge computing for on-sensor analytics; wireless energy harvesting sensors.

Regional Leaders: Asia Pacific ~USD 1,900 Million by 2032 (rapid smart-city rollout); North America ~USD 1,300 Million (industrial upgrades); Europe ~USD 1,100 Million (strict regulation adoption).

Consumer/End-User Trends: Utilities, municipalities, and industrial sites increasingly shift from manual sampling to continuous remote sensing, with adoption rates reaching 40 % of new installations.

Pilot or Case Example: In 2024, a smart-city pilot in a Southeast Asian city achieved 20 % reduction in outage times by integrating real-time air emission alerts to control center operations.

Competitive Landscape: Market leader commanding ~18 % share, followed by 3–5 major competitors including firms in North America, Europe, and Asia.

Regulatory & ESG Impact: Governments are enforcing emissions limits, mandating continuous monitoring, offering tax credits and subsidies tied to ESG compliance.

Investment & Funding Patterns: Over USD 200 million in venture and project funding in 2023–2024, with a shift toward outcome-based performance contracts.

Innovation & Future Outlook: Trends include self-powered sensors, multispectral gas detection, integration with digital twins, and deployment of city-scale sensor mesh networks.

The market is seeing increased uptake in municipal air and water monitoring, industrial emissions control, agriculture, and disaster-resilience applications. Innovations in nano-sensing, wireless communication, and modular form factors are shaping next-generation offerings. Economic incentives and tightening environmental regulations are spurring deployment especially in urbanizing regions, and integrated analytics platforms are becoming the de facto standard.

In today’s environment of tightening regulations, climate risks, and smart infrastructure rollout, the Environmental Sensing and Monitoring Technologies Market serves as a strategic linchpin for decision-makers. It enables compliance, risk mitigation, operational optimization, and sustainability transparency. The shift from passive sampling to real-time, continuous sensing allows firms to detect emissions deviations or environmental anomalies swiftly, reducing downtime and penalties.

For example, using edge-AI sensing delivers 30 % improvement in anomaly detection latency compared to traditional periodic sampling. Regionally, Asia Pacific dominates in volume, while North America leads in enterprise adoption, with over 45 % of industrial sites deploying advanced continuous monitoring. By 2026, deployment of self-powered sensors is expected to reduce maintenance costs by 25 %, improving system uptime. Firms are committing to ESG metrics such as 20 % emissions reduction by 2030, and are integrating sensor networks into corporate sustainability targets.

In 2024, a major industrial park in Europe achieved a 15 % drop in pollutant excursions using sensor-driven control loops. Looking forward, the Environmental Sensing and Monitoring Technologies Market is positioned as a pillar of resilient infrastructure, regulatory compliance, and sustainable growth in an era where data-driven environmental integrity is non-negotiable.

The Environmental Sensing and Monitoring Technologies Market is evolving under converging pressures of regulatory mandates, technological leaps, and demands for transparency. Enterprises and municipalities increasingly require continuous environmental data to ensure compliance, manage risk, and optimize operations. Advances in miniaturization, low-power electronics, wireless connectivity, and cloud analytics are rapidly lowering barriers to deployment. Simultaneously, end-user sectors—utilities, smart cities, industrial complexes, agriculture—are driving customized sensor solutions. The market also contends with integration complexities, data security, and interoperability standards. As environmental awareness, climate resilience, and ESG investing intensify, demand accelerates across geographies, particularly in urbanizing and industrializing regions.

Increasingly stringent air and water quality standards imposed by governments globally require continuous, real-time monitoring. Industries must deploy robust sensor systems in process stacks, effluent streams, and ambient zones to meet compliance audits. In regions like Europe and East Asia, new regulation cycles (2023–2025) mandate hourly emission reporting, forcing upgrade of legacy manual monitoring. This transition drives demand for advanced sensing systems with high stability, precision, and remote connectivity. Furthermore, cross-sector drivers like industrial automation, smart agriculture, and climate adaptation also funnel investment into sensing networks, amplifying technology diffusion across end-use verticals.

Many legacy systems are proprietary, creating challenges in integrating new sensors with existing SCADA, MES, or enterprise platforms. Incompatibility in protocols, data formats, and communication standards leads to higher integration costs, delays, and system fragmentation. Some installations face long certification cycles and testing burdens before deployment. Further, concerns around data security, calibration drift, maintenance, and lifespan limitations also temper adoption in risk-averse segments. High initial setup costs for dense monitoring grids and uncertainty in ROI timelines discourage smaller users from committing.

Rapid urbanization and sustainable infrastructure mandates are driving smart city and resilience programs globally. These require dense environmental sensing to monitor air quality, noise, water, soil, and climate variables. Deployment of sensor mesh networks, citizen monitoring platforms, and digital twin integration opens new business models—sensor leasing, subscription analytics, outcome-based contracts. In regions rolling out green buildings, intelligent transit, or climate adaptation infrastructure, there is demand for turnkey environment monitoring ecosystems. Additionally, integration of sensors into 5G/IoT edge infrastructure and autonomous systems offers opportunity for scalable platforms.

Environmental sensors degrade over time, requiring periodic calibration, replacement, or maintenance. Drift, contamination, and sensor aging lead to accuracy degradation, reducing trust in outputs for compliance use cases. Frequent recalibration schedules and replacement cycles raise operational overheads. Remote or harsh environments—such as industrial stacks, marine zones, or extreme climates—accelerate wear and failure. These reliability concerns, combined with reluctance to incur recurring service costs, particularly in municipal or small installations, present a persistent barrier to widespread deployment.

Modular & Prefabricated Sensor Platforms Gaining Traction: Modular and prefabricated sensor units are being adopted by 60 % of new infrastructure and industrial projects in mature markets. These plug-and-play modules reduce engineering time by 25 % and allow faster deployment in remote or constrained locations. They are being especially used in Europe and North America for retrofit and expansion projects.

Edge Analytics and AI-On-Device Integration: About 45 % of newly deployed sensor units now include edge computing modules, eliminating raw-data transmission needs and delivering real-time detection within milliseconds. This reduces bandwidth usage by roughly 40 % and accelerates anomaly response by 20 %.

Self-Powered and Energy Harvesting Sensors: Over 30 % of new sensor nodes in pilot installations harness ambient energy (solar, vibration, thermal) to operate autonomously. These nodes boast expected maintenance-free life cycles of 5 to 7 years, cutting upkeep costs by approximately 15 %.

Multi-Parameter & Multi-Spectral Sensing Arrays: Next-generation sensor suites can simultaneously detect multiple gases (e.g., CO, NO₂, O₃) or parameters (temperature, humidity, particulate matter) from a single device. Deployment of such multi-parameter arrays now accounts for 28 % of new units, reducing hardware count and enabling tighter spatial monitoring grids.

The Global Environmental Sensing and Monitoring Technologies Market is segmented based on type, application, and end-user. The segmentation highlights diverse technologies such as particulate sensors, temperature sensors, humidity sensors, gas sensors, water-quality sensors, and integrated environmental monitoring systems. These technologies are applied across industrial, commercial, municipal, and residential sectors to monitor air, water, and soil quality in real time. The market’s structure reflects the evolution from standalone sensors to intelligent networked systems integrating IoT, AI, and data analytics for predictive insights. The growing adoption of environmental compliance systems, industrial automation, and smart-city frameworks continues to influence the demand mix. Consumer and enterprise-level investments indicate a shift toward scalable, energy-efficient, and cloud-integrated solutions that enhance long-term monitoring accuracy and operational efficiency.

Gas sensors currently account for 38% of market adoption, driven by their essential role in air quality monitoring and emission control across industrial zones and urban centers. They are the backbone of real-time environmental surveillance due to their ability to detect multiple gases like CO₂, SO₂, and NOₓ with high sensitivity. Water-quality sensors follow with 26% adoption, fueled by increasing freshwater management needs and wastewater treatment automation. However, integrated multi-parameter systems are the fastest-growing segment, projected to expand at approximately 7.8% CAGR, as industries and governments transition to unified solutions that measure temperature, humidity, particulate matter, and gas concentration simultaneously. Temperature and humidity sensors collectively contribute about 22% of the market, primarily in indoor air quality systems and climate stations. The remaining types—soil sensors, radiation detectors, and noise sensors—represent around 14% combined, serving niche applications such as agriculture, energy, and urban noise control.

Air quality monitoring dominates the Environmental Sensing and Monitoring Technologies Market, accounting for 41% of total adoption due to widespread implementation in industrial zones, urban infrastructure, and transportation corridors. Water-quality monitoring holds 29%, supported by investments in wastewater management and potable water systems. However, soil and climate monitoring applications are growing fastest at approximately 8.1% CAGR, driven by agricultural digitization and climate resilience projects that integrate satellite and IoT-based sensor data. Other applications, including waste management, forest surveillance, and radiation monitoring, represent about 30% combined and are being increasingly incorporated into integrated environmental control frameworks. In 2024, more than 44% of municipal authorities in advanced economies reported deploying multi-sensor networks for continuous ambient monitoring. Additionally, 35% of agricultural enterprises adopted soil and moisture sensors for crop optimization.

The industrial sector leads the Environmental Sensing and Monitoring Technologies Market, representing 39% of global adoption, with heavy industries, energy production, and chemical processing facilities deploying high-density sensor networks to ensure emission compliance and operational safety. Municipal and government agencies follow with 33%, focusing on air and water quality management, public health monitoring, and smart city infrastructure integration. However, commercial and residential end-users are the fastest-growing group, expanding at roughly 7.5% CAGR, as demand for building automation, indoor air quality monitoring, and sustainability certification increases. The remaining 28% combined share is distributed among agriculture, research institutions, and transportation sectors, each leveraging environmental sensing technologies to enhance sustainability and efficiency. In 2024, over 48% of smart-city projects globally integrated environmental sensors into their operational frameworks, while 32% of industrial facilities initiated digital monitoring upgrades to replace manual sampling systems.

Asia Pacific accounted for the largest market share at 35% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

Asia Pacific’s dominance stems from large-scale manufacturing hubs, high population density, increasing urbanization, and aggressive deployment of smart city and environmental regulation frameworks. In 2024 alone, over 40 million sensor modules were shipped to China, India, Japan, and Southeast Asia combined. Meanwhile, North America saw more than 12 million new continuous monitoring installations in industrial, municipal, and commercial sectors during 2024. Europe accounted for 25% of global consumption in that year, with strong uptake of water and air quality monitoring systems. Latin America and Middle East & Africa regions combined made up roughly 15%, with increasing investment in oil & gas and resource monitoring infrastructure. Asia Pacific also led in R&D investment, with over USD 220 million allocated to sensor device innovation in 2024, substantially more than in any other region.

North America holds about 30% of global market adoption in environmental sensing and monitoring technologies. Key industries driving demand include manufacturing (especially chemical and petroleum), utilities (electricity and water), and municipal governance for air and water quality. Regulatory changes such as tighter EPA standards for ambient air pollution, new rules for industrial effluent discharge, and mandates for continuous emission monitoring have pushed upgrades of legacy systems. Technological advancements include widespread deployment of edge-AI sensors, wireless LoRaWAN or NB-IoT networks, and real-time data platforms with predictive maintenance features. A notable local player is a U.S.-based firm which has launched self-calibrating gas sensors with embedded machine-learning routines to reduce drift by 20% over 12 months. In terms of behavior, enterprises in healthcare and finance sectors in North America are increasingly demanding environmental sensor integration for indoor air quality and compliance, reflecting higher enterprise adoption in those sectors compared to consumer-led adoption.

Europe contributes roughly 25% of worldwide installations in environmental sensing and monitoring technologies. Major markets include Germany, the United Kingdom, France, and the Netherlands. Regulatory bodies and sustainability initiatives—such as the European Green Deal, Air Quality Directives, and Water Framework Directive—are imposing stricter thresholds for pollutants, effluents, and emissions. Emerging technologies like multi-parameter sensor arrays, remote sensing via drones or satellites, and blockchain-verified sensor data are being adopted. A German manufacturer is providing integrated sensor-as-a-service contracts, installing sensors in industrial emissions systems and offering performance guarantees. In regional consumer behavior, there is strong demand for explainable and certified sensors, especially in urban areas where transparency, accuracy, and certification matter to local governments and citizens.

Asia-Pacific accounted for about 35% of global environmental sensor module shipments in 2024. Top consuming countries include China, India, and Japan. Massive infrastructure and manufacturing developments (e.g., expansion of smart city networks, industrial parks, and wastewater treatment plants) drive demand. Innovation hubs in East Asia are pushing advances in MEMS sensors, AI-enabled edge processing, and low-power wireless designs. A Chinese company has rolled out over 10 million air-quality sensors in urban monitoring grids in 2024, incorporating IoT connectivity and automated calibration. Consumer behavior shows rising concerns over urban pollution: in cities, more than 60% of households seek indoor air monitors, and public app-based ambient air quality alerts are widely used, influencing procurement of devices and municipal monitoring stations.

In South America, Brazil and Argentina are notable players, jointly representing about 8% of global environmental sensing and monitoring market presence in 2024. Infrastructure expansion in energy (hydropower, bioenergy), mining, and transportation sectors drives demand. Government incentive programs and trade policies supporting environmental compliance (e.g., tighter emission limits in major cities, wastewater treatment mandates) are encouraging sensor deployment. A local Brazilian firm has developed water-quality monitoring packages tailored for remote and rural regions, integrating solar-powered sensors and cellular connectivity. Regional consumer behavior shows greater concern over water safety and resource contamination: public awareness campaigns in urban centers lead to higher demand for portable sensors and community monitoring stations.

Middle East & Africa accounted for around 7% of global deployments in 2024, with major countries including the UAE, Saudi Arabia, and South Africa. Demand stems from oil & gas monitoring, construction of large-scale infrastructure projects, and environmental compliance in industrial zones. Technological modernization trends include retrofitting older zones with IoT sensors, satellite-linked environmental alerts, and modular sensor stations for remote monitoring. Local regulations are increasingly aligned with international ESG standards; trade partnerships facilitate import of high-precision sensors. One regional player in South Africa has launched a program delivering community air-monitoring kits to urban neighborhoods, generating fine particulate data used by municipalities to enforce localized action. Consumer behavior in this region tends to favor visible, low-maintenance, and robust sensor units, especially in industrial or outdoor settings.

China – 28% Market Share: Due to large-scale production capacity, extensive manufacturing facilities, and strong investment in domestic R&D in sensing technologies.

United States – 22% Market Share: Driven by stringent regulatory frameworks, high demand from industrial, utilities, and smart city sectors, and rapid adoption of advanced sensor systems.

The Environmental Sensing and Monitoring Technologies Market is characterized by a fragmented competitive landscape, with over 150 active players globally. The top five companies—Bosch Sensortec, Honeywell International Inc., Texas Instruments, Sensirion AG, and Omron Corporation—account for approximately 21% of the market share. This indicates a diverse array of competitors, ranging from established industrial giants to specialized startups. Strategic initiatives such as mergers, acquisitions, and partnerships are prevalent. For instance, in 2023, Honeywell expanded its portfolio by acquiring a leading environmental sensor technology firm, enhancing its capabilities in air quality monitoring. Similarly, Bosch Sensortec has collaborated with several IoT platform providers to integrate its sensors into smart city solutions.

Innovation is a key driver of competition. Companies are focusing on developing sensors with higher accuracy, lower power consumption, and enhanced connectivity features. The integration of AI and machine learning algorithms into monitoring systems is becoming increasingly common, enabling predictive analytics and real-time decision-making.

Geographically, North America leads in market share, driven by stringent environmental regulations and high adoption rates in industrial applications. Europe follows closely, with a strong emphasis on sustainability and regulatory compliance. Asia-Pacific is witnessing rapid growth, fueled by industrial expansion and increasing environmental awareness.

Overall, the market's competitive dynamics are shaped by technological advancements, regulatory pressures, and the need for sustainable solutions.

Texas Instruments

Sensirion AG

Omron Corporation

ABB Ltd.

Emerson Electric Co.

Schneider Electric SE

Siemens AG

The Environmental Sensing and Monitoring Technologies Market is experiencing significant technological advancements that are reshaping its landscape. Key developments include the integration of Internet of Things (IoT) capabilities, enabling real-time data collection and analysis. Wireless communication technologies, such as LoRaWAN and NB-IoT, are facilitating remote monitoring in hard-to-reach areas. Advancements in sensor miniaturization and energy efficiency are allowing for deployment in a broader range of applications, from wearable devices to large-scale environmental monitoring networks.

Artificial Intelligence (AI) and Machine Learning (ML) are being increasingly incorporated into monitoring systems, providing predictive analytics and anomaly detection. These technologies enhance the ability to foresee environmental hazards and respond proactively. Cloud computing platforms are supporting the storage and processing of vast amounts of sensor data, enabling scalable and accessible monitoring solutions.

Furthermore, there is a growing emphasis on the development of multispectral and hyperspectral sensors, which offer enhanced detection capabilities across various environmental parameters. These innovations are driving the evolution of the market, leading to more efficient and comprehensive environmental monitoring solutions.

In May 2024, Honeywell launched a new series of smart air quality sensors designed for urban environments. These sensors utilize advanced filtration technology and real-time data analytics to monitor pollutants, providing municipalities with actionable insights to improve air quality. Source: www.honeywell.com

In April 2024, Bosch Sensortec unveiled a compact environmental sensor module tailored for wearable devices. The module integrates temperature, humidity, and air quality sensors, enabling users to monitor their immediate environment and health metrics simultaneously. Source: www.bosch-sensortec.com

In March 2024, PerkinElmer Inc. expanded its environmental monitoring portfolio by acquiring a leading provider of water quality sensors. This acquisition enhances PerkinElmer's capabilities in delivering comprehensive water monitoring solutions to industrial and municipal clients. Source: www.perkinelmer.com

The Environmental Sensing and Monitoring Technologies Market Report offers an extensive analysis of the industry's current state and future prospects. It covers various market segments, including air quality monitoring, water quality assessment, soil analysis, and noise pollution detection. The report delves into the technological advancements driving the market, such as IoT integration, AI and ML applications, and the development of advanced sensor materials.

Geographically, the report provides insights into key regional markets, highlighting the leading countries in environmental monitoring technologies and their respective market shares. It also examines the regulatory frameworks influencing the adoption of these technologies, with a focus on sustainability initiatives and environmental policies.

Furthermore, the report explores the competitive landscape, profiling major players in the market and analyzing their strategic initiatives, including partnerships, acquisitions, and product innovations. Consumer behavior trends are also discussed, shedding light on the increasing demand for real-time environmental data and the growing emphasis on sustainability among end-users.

Overall, the report provides a comprehensive overview of the Environmental Sensing and Monitoring Technologies Market, serving as a valuable resource for stakeholders seeking to understand market dynamics, identify growth opportunities, and make informed business decisions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 3,130.0 Million |

| Market Revenue (2032) | USD 4,876.9 Million |

| CAGR (2025–2032) | 5.7% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Bosch Sensortec, Honeywell International Inc., PerkinElmer Inc., Texas Instruments, Sensirion AG, Omron Corporation, ABB Ltd., Emerson Electric Co., Schneider Electric SE, Siemens AG |

| Customization & Pricing | Available on Request (10% Customization is Free) |