Reports

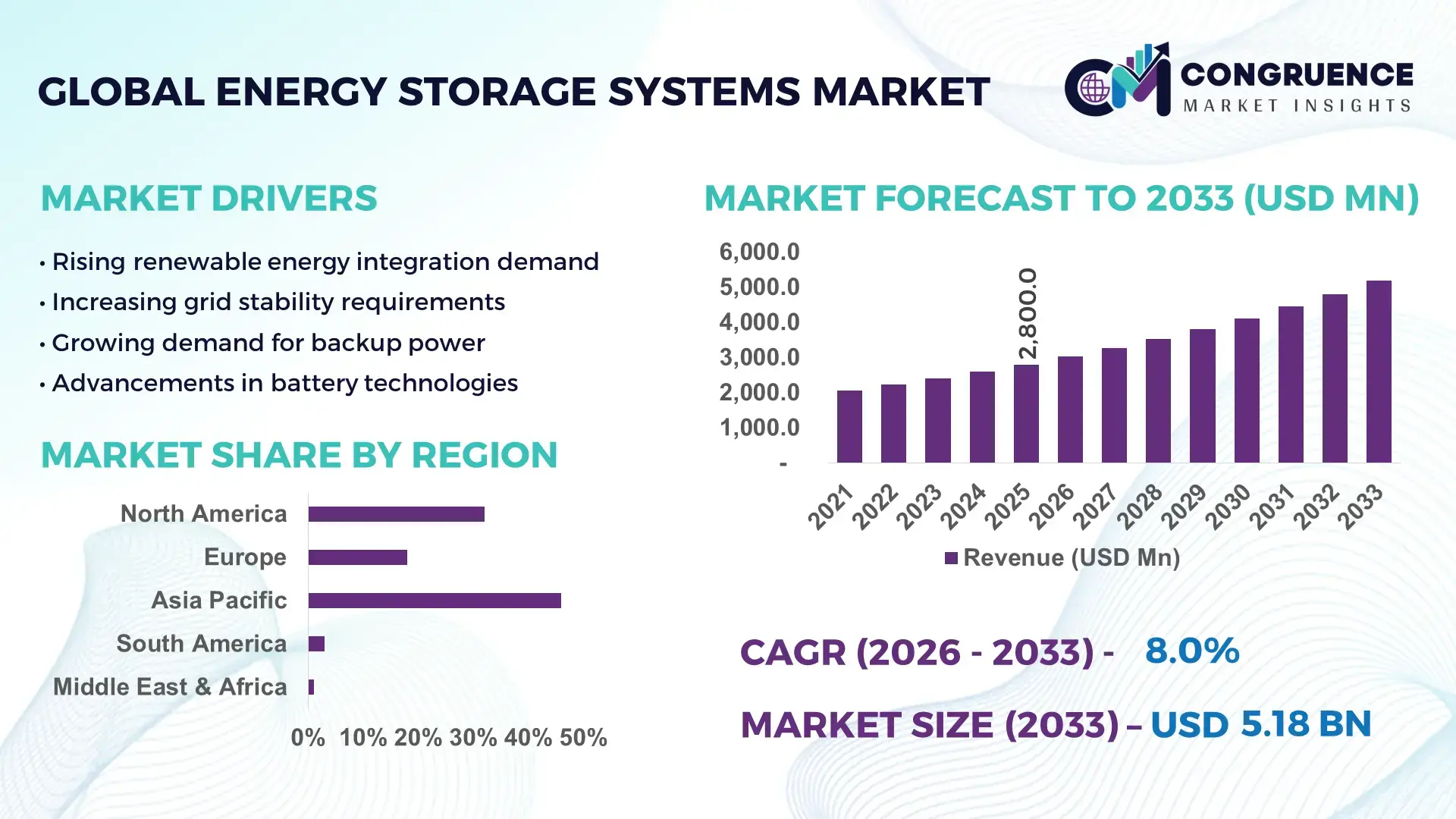

The Global Energy Storage Systems Market was valued at USD 2,800.0 Million in 2025 and is anticipated to reach a value of USD 5,182.6 Million by 2033 expanding at a CAGR of 8.0% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by increasing integration of renewable energy sources and the need for grid stability solutions.

China dominates the Energy Storage Systems Market with over 45% of global lithium-ion battery production capacity in 2025, supported by more than 1,200 GWh annual manufacturing output. The country has invested over USD 50 billion in grid-scale storage projects, with installations exceeding 70 GW across utility and industrial applications. Electric vehicle penetration surpasses 35% of new car sales, significantly boosting demand for battery storage. Additionally, over 60% of utility-scale renewable projects in China incorporate storage integration, while advanced battery technologies such as sodium-ion and solid-state systems are being piloted at scale, enhancing performance efficiency by up to 20%.

Market Size & Growth: USD 2,800.0 Million in 2025, projected to reach USD 5,182.6 Million by 2033, growing at 8.0% due to rising renewable integration and grid reliability demand.

Top Growth Drivers: Renewable adoption (42%), EV penetration (35%), grid modernization (28%).

Short-Term Forecast: By 2028, system costs are expected to decline by 18% while energy density improves by 22%.

Emerging Technologies: Solid-state batteries, sodium-ion storage, AI-enabled energy management systems.

Regional Leaders: Asia-Pacific (~USD 2,200 Million by 2033) driven by manufacturing scale; North America (~USD 1,400 Million) driven by grid upgrades; Europe (~USD 1,100 Million) driven by decarbonization mandates.

Consumer/End-User Trends: Utilities account for over 48% of installations, followed by commercial users adopting hybrid storage for peak shaving.

Pilot or Case Example: In 2025, a 300 MWh battery project improved grid stability by 25% and reduced outages by 18%.

Competitive Landscape: Market leader holds ~16% share; key players include Tesla, LG Energy Solution, Panasonic, BYD, and Samsung SDI.

Regulatory & ESG Impact: Over 70 countries introduced incentives or mandates supporting storage deployment and carbon reduction targets.

Investment & Funding Patterns: Over USD 90 billion invested globally in storage infrastructure and battery innovation projects.

Innovation & Future Outlook: Integration of AI-based optimization and hybrid renewable-storage systems is expected to improve efficiency by over 25%.

Energy Storage Systems Market is supported by utilities (48%), commercial & industrial sectors (32%), and residential users (20%). Advancements such as solid-state batteries improving safety by 30% and AI-driven energy optimization reducing losses by 15% are reshaping the market. Regulatory mandates promoting decarbonization and rising renewable installations exceeding 3,500 GW globally are accelerating adoption, while emerging hybrid storage systems and decentralized grids are shaping long-term growth.

The Energy Storage Systems Market is strategically critical for enabling energy transition, improving grid resilience, and supporting electrification across industries. With renewable energy capacity exceeding 3,500 GW globally, storage systems have become essential to balance intermittent supply and demand fluctuations. Lithium-ion battery systems dominate current deployments, but solid-state batteries are emerging as a transformative technology, delivering 35% higher energy density compared to conventional lithium-ion systems.

Regionally, Asia-Pacific dominates in volume due to extensive manufacturing capacity and large-scale renewable deployments, while North America leads in adoption with over 55% of utilities integrating advanced storage solutions into grid infrastructure. By 2028, AI-enabled energy management systems are expected to improve operational efficiency by 25% and reduce downtime by 20% across grid-scale storage networks.

From an ESG perspective, firms are committing to sustainability targets such as 40% battery material recycling rates by 2030 and reducing lifecycle emissions by 30%. These commitments are driving investments in circular battery supply chains and advanced recycling technologies.

In 2025, a large-scale deployment in China achieved a 22% reduction in grid curtailment through AI-integrated storage optimization, highlighting measurable operational improvements. Additionally, hybrid storage systems combining battery and hydrogen storage are being tested to enhance long-duration energy storage capabilities.

Looking ahead, the Energy Storage Systems Market is positioned as a core pillar of energy resilience, regulatory compliance, and sustainable industrial growth, enabling efficient power utilization and supporting global decarbonization strategies.

The Energy Storage Systems Market is experiencing rapid transformation driven by evolving energy consumption patterns, grid modernization efforts, and increasing renewable energy penetration. Global electricity demand has increased by over 4% annually, requiring efficient storage systems to manage load balancing and peak demand fluctuations. The growing adoption of electric vehicles, which exceeded 14 million units sold globally in 2025, is significantly influencing demand for battery storage technologies. Additionally, over 65% of new renewable energy installations are now integrated with storage solutions to ensure grid reliability. Technological advancements such as AI-based energy management, improved battery chemistries, and hybrid storage solutions are enhancing system performance and efficiency. However, supply chain dependencies for raw materials such as lithium and cobalt, along with infrastructure limitations in developing regions, continue to shape market dynamics. Regulatory frameworks and sustainability goals are further accelerating adoption while pushing innovation in storage technologies and recycling capabilities.

The rapid expansion of renewable energy capacity is a primary driver of the Energy Storage Systems Market. Solar and wind installations have surpassed 3,500 GW globally, with over 70% of new projects requiring integrated storage systems to manage intermittency. Storage systems enable utilities to store excess energy generated during peak production and redistribute it during high-demand periods, improving grid stability by up to 30%. Additionally, countries are mandating storage integration in renewable projects, with over 50 nations implementing policies supporting energy storage deployment. Industrial sectors are also adopting storage solutions to reduce reliance on conventional power sources, achieving up to 20% energy cost savings. The increasing deployment of microgrids and distributed energy systems further supports demand, particularly in remote and off-grid locations. As renewable adoption continues to accelerate, the need for efficient and scalable storage systems is expected to remain a key growth driver.

The availability and cost volatility of critical raw materials such as lithium, cobalt, and nickel are significant restraints impacting the Energy Storage Systems Market. Global lithium demand has increased by over 25% annually, creating supply shortages and price fluctuations that directly affect battery production costs. Over 60% of cobalt supply is concentrated in limited geographic regions, increasing supply chain risks and geopolitical dependencies. Additionally, refining and processing capacities are unevenly distributed, leading to bottlenecks in battery manufacturing. Environmental concerns related to mining activities have also led to stricter regulations, further constraining supply. Recycling infrastructure remains underdeveloped, with less than 20% of battery materials currently being recovered and reused. These factors collectively increase production costs and limit scalability, particularly in emerging markets where infrastructure and investment capabilities are still developing.

Advancements in long-duration energy storage technologies present significant opportunities for market expansion. Technologies such as flow batteries, hydrogen storage, and compressed air systems are gaining traction for their ability to store energy for extended periods exceeding 10 hours. These systems are particularly valuable for grid-scale applications and renewable integration, where energy supply may be inconsistent. Over 40% of utility providers are actively exploring long-duration storage solutions to enhance grid reliability. Hydrogen-based storage systems are also being piloted, with efficiency improvements of up to 50% in energy conversion processes. Additionally, government funding initiatives exceeding USD 20 billion globally are supporting research and development in advanced storage technologies. These innovations are expected to address limitations of conventional battery systems and open new application areas across industrial, utility, and residential sectors.

Infrastructure limitations and integration complexities pose significant challenges to the Energy Storage Systems Market. Grid infrastructure in many regions is not fully equipped to handle large-scale storage integration, requiring substantial upgrades and investment. Over 35% of existing grids face compatibility issues with advanced storage systems, leading to inefficiencies and increased operational costs. Additionally, integrating storage systems with renewable energy sources requires advanced control systems and real-time monitoring capabilities, which are not universally available. Cybersecurity concerns are also increasing, as interconnected storage systems become vulnerable to digital threats. Furthermore, lack of standardized protocols and interoperability issues across different storage technologies complicate deployment. These challenges require coordinated efforts between governments, utilities, and technology providers to ensure seamless integration and optimal system performance.

Rapid expansion of grid-scale battery installations: Over 65% of new renewable projects in 2025 included integrated storage systems, with grid-scale battery capacity exceeding 150 GW globally. Utilities reported up to 30% improvement in peak load management and a 20% reduction in grid instability events through large-scale battery deployments.

Increasing adoption of AI-driven energy management systems: More than 45% of newly installed storage systems are integrated with AI-based optimization tools, improving operational efficiency by 25% and reducing energy losses by 15%. Predictive analytics is enabling better demand forecasting and system reliability.

Growth in electric vehicle-linked storage demand: EV adoption surpassed 35% of global vehicle sales in 2025, driving secondary battery usage for stationary storage applications. Repurposed EV batteries now account for nearly 12% of residential storage systems, improving cost efficiency by 18%.

Emergence of alternative battery chemistries: Sodium-ion and solid-state batteries are gaining traction, with pilot projects showing 20% higher safety performance and 25% improved lifecycle efficiency. Over 30% of manufacturers are investing in next-generation battery technologies to reduce dependency on scarce materials.

The Energy Storage Systems Market is segmented based on type, application, and end-user, each playing a critical role in shaping overall industry dynamics. Lithium-ion batteries dominate due to high energy density and efficiency, while emerging technologies such as flow batteries and hydrogen storage are gaining traction for long-duration applications. Utility-scale applications lead the market as grid operators increasingly deploy storage solutions to stabilize power supply and integrate renewable energy sources. Commercial and industrial applications are also expanding, driven by the need for energy cost optimization and backup power solutions. End-users range from utilities and industrial enterprises to residential consumers adopting decentralized energy systems. Increasing electrification, renewable integration, and advancements in battery technology are influencing segment-level growth, while regulatory mandates and sustainability goals continue to shape adoption patterns across regions and industries.

The Energy Storage Systems Market by type is dominated by lithium-ion batteries, which account for approximately 68% of total installations due to their high energy density, efficiency levels exceeding 90%, and declining production costs driven by economies of scale. Lithium-ion systems are widely used across utility-scale, commercial, and residential applications, making them the leading segment. In comparison, lead-acid batteries hold around 12% share, primarily in backup and off-grid applications, while flow batteries contribute nearly 10%, offering advantages in long-duration storage exceeding 8–10 hours. Other technologies such as sodium-ion, compressed air, and thermal storage collectively account for the remaining 10% share, serving niche and emerging use cases. Among these, flow batteries are the fastest-growing segment, expanding at an estimated CAGR of 12.5% due to increasing demand for long-duration storage and grid-scale applications. Their ability to maintain performance over extended cycles and reduce degradation makes them suitable for renewable integration projects. Sodium-ion batteries are also gaining traction due to their lower dependence on critical raw materials and cost advantages of up to 20% compared to lithium-ion systems.

• In 2025, a national energy program deployed over 500 MWh of flow battery storage systems for grid balancing, improving peak load efficiency by 18% across multiple utility networks.

Utility-scale applications dominate the Energy Storage Systems Market, accounting for approximately 52% of total deployment due to the increasing need for grid stabilization, renewable integration, and load balancing. These systems enable utilities to store excess energy and release it during peak demand periods, improving grid efficiency by up to 30%. In comparison, commercial and industrial (C&I) applications hold around 28% share, driven by demand for energy cost optimization and backup power solutions. Residential applications account for nearly 20%, with growing adoption of rooftop solar systems and home energy storage solutions. The fastest-growing application segment is commercial and industrial, expanding at an estimated CAGR of 10.8%, supported by rising electricity costs and demand for energy resilience. Businesses are increasingly adopting hybrid storage systems to reduce peak demand charges and improve operational continuity. Utility-scale storage continues to expand with the integration of renewable energy, while residential adoption is driven by increasing awareness of energy independence. In 2025, over 40% of enterprises globally reported implementing or piloting energy storage solutions for operational efficiency, while more than 55% of residential solar users opted for integrated storage systems to enhance energy reliability.

• In 2025, a large-scale utility project deployed a 300 MWh storage system, reducing grid outages by 20% and improving renewable energy utilization efficiency by 25% across urban networks.

Utilities represent the leading end-user segment in the Energy Storage Systems Market, accounting for approximately 48% of total demand due to their critical role in managing electricity supply, integrating renewable energy, and ensuring grid stability. Industrial users account for around 30% share, driven by the need for uninterrupted power supply and energy cost optimization, particularly in manufacturing and heavy industries. Residential users contribute approximately 22%, with increasing adoption of home energy storage systems linked to solar installations. The fastest-growing end-user segment is the commercial and industrial sector, expanding at an estimated CAGR of 11.2%, fueled by rising energy costs and the need for energy resilience. Industrial adoption rates exceed 35% in energy-intensive sectors, while over 50% of new commercial buildings are integrating storage systems for energy efficiency and backup power. Residential adoption is also growing, with nearly 40% of solar installations including storage systems. In 2025, more than 38% of enterprises globally reported piloting energy storage solutions for operational efficiency, while over 60% of residential consumers expressed interest in adopting integrated storage systems for energy independence.

• In 2025, a national utility implemented large-scale battery storage across its network, improving grid reliability by 22% and reducing energy losses by 15% in high-demand regions.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2026 and 2033.

Asia-Pacific leads with over 180 GW of installed energy storage capacity, driven by large-scale deployments in China, Japan, and India. China alone contributes more than 70 GW, supported by extensive renewable energy projects and battery manufacturing capabilities. North America follows with approximately 32% market share, with over 90 GW of installed capacity, largely driven by grid modernization and renewable integration in the United States. Europe accounts for nearly 18% share, with strong adoption across Germany, the UK, and France, where over 60% of renewable projects incorporate storage systems. South America and the Middle East & Africa collectively account for around 4%, with emerging adoption driven by energy diversification and infrastructure development initiatives.

North America holds approximately 32% share of the Energy Storage Systems Market, driven by strong demand from utilities, commercial enterprises, and renewable energy developers. The United States accounts for over 80% of regional installations, with more than 75 GW of deployed storage capacity. Key industries such as utilities, data centers, and manufacturing are driving demand, supported by government incentives including tax credits and renewable energy mandates. Advanced technologies such as AI-based energy management systems and grid-scale lithium-ion batteries are widely adopted, improving efficiency by over 25%. Companies like Tesla are actively expanding large-scale battery storage projects, contributing significantly to grid resilience. Consumer behavior indicates higher adoption in commercial sectors, with over 50% of enterprises integrating storage solutions for operational efficiency.

Europe accounts for approximately 18% of the Energy Storage Systems Market, with leading countries including Germany, the UK, and France. Over 65 GW of storage capacity has been deployed across the region, driven by strict environmental regulations and carbon reduction targets. The European Union’s renewable energy directives require increased integration of storage systems, particularly in solar and wind projects. Advanced technologies such as flow batteries and hydrogen storage are gaining traction, with pilot projects improving efficiency by up to 20%. Local players are investing in sustainable battery manufacturing and recycling initiatives. Consumer behavior reflects strong demand for environmentally friendly solutions, with over 60% of renewable energy projects incorporating storage systems to meet regulatory requirements.

Asia-Pacific leads the Energy Storage Systems Market with over 46% share and more than 180 GW of installed capacity. China, Japan, and India are the top consuming countries, collectively accounting for over 75% of regional demand. The region benefits from strong manufacturing capabilities, producing over 70% of global lithium-ion batteries. Infrastructure development and renewable energy expansion are key drivers, with large-scale solar and wind projects integrating storage systems to improve efficiency. Companies such as BYD are expanding battery production facilities, enhancing supply chain capabilities. Consumer trends indicate rapid adoption in industrial and utility sectors, with over 55% of new energy projects incorporating storage solutions.

South America accounts for approximately 3% of the Energy Storage Systems Market, with Brazil and Argentina leading regional adoption. The region has deployed over 8 GW of storage capacity, primarily linked to renewable energy projects such as solar and hydropower. Government incentives and trade policies are encouraging investment in energy storage infrastructure, particularly in Brazil where renewable energy accounts for over 80% of electricity generation. Local players are focusing on hybrid storage solutions to enhance grid reliability. Consumer behavior indicates growing adoption in industrial sectors, where storage systems are used to reduce energy costs and improve operational efficiency.

The Middle East & Africa region holds around 1% market share, with growing demand driven by energy diversification initiatives and infrastructure development. Countries such as the UAE and South Africa are investing in renewable energy projects integrated with storage systems, with over 5 GW of capacity installed. Oil & gas and construction sectors are key drivers, adopting storage solution for energy efficiency and backup power. Technological modernization efforts include deployment of advanced battery systems and grid integration technologies. Local companies are partnering with global players to expand capabilities. Consumer trends show increasing adoption in industrial applications, particularly in energy-intensive sectors.

China– 45% Market share: Driven by large-scale production capacity and extensive renewable integration projects.

United States– 28% Market share: Supported by strong utility demand and advanced grid modernization initiatives.

The Energy Storage Systems Market is moderately fragmented, with over 120 active global and regional players competing across battery manufacturing, system integration, and software solutions. The top five companies collectively account for approximately 45% of the market share, indicating a competitive yet consolidated environment among leading players. Major companies are focusing on strategic partnerships, mergers, and product innovations to strengthen their market position.

Technological advancements are a key competitive factor, with companies investing heavily in next-generation battery technologies such as solid-state and sodium-ion systems. Over 35% of leading firms have announced new product launches in the past two years, focusing on improving energy density and reducing costs. Strategic collaborations between battery manufacturers and energy providers are also increasing, with over 50 partnerships formed globally to enhance deployment capabilities. Additionally, companies are expanding production capacities, with global battery manufacturing capacity exceeding 1,200 GWh. Innovation in AI-based energy management systems is further shaping competition, enabling companies to offer integrated and optimized storage solutions.

LG Energy Solution Ltd.

Panasonic Corporation

BYD Company Ltd.

Samsung SDI Co., Ltd.

Fluence Energy, Inc.

Contemporary Amperex Technology Co., Limited (CATL)

Siemens Energy AG

General Electric Company

ABB Ltd.

Hitachi Energy Ltd.

Schneider Electric SE

Toshiba Corporation

Enphase Energy, Inc.

The Energy Storage Systems Market is undergoing significant technological transformation driven by advancements in battery chemistry, system integration, and digital optimization. Lithium-ion batteries continue to dominate, offering energy densities exceeding 250 Wh/kg and cycle efficiencies above 90%. However, emerging technologies such as solid-state batteries are gaining traction, delivering up to 35% higher energy density and improved safety by reducing risks of thermal runaway. Sodium-ion batteries are also emerging as a cost-effective alternative, reducing dependency on critical materials like lithium and cobalt while lowering costs by up to 20%.

AI and machine learning are increasingly integrated into energy storage systems, enabling predictive maintenance, real-time monitoring, and demand forecasting. These technologies improve system efficiency by up to 25% and reduce operational downtime by 20%. Hybrid energy storage systems combining batteries with hydrogen or thermal storage are also being developed to support long-duration energy storage exceeding 10 hours.

Additionally, advancements in battery recycling technologies are improving material recovery rates, with over 30% of battery materials now being recycled and reused. Digital twin technology is also being implemented to simulate system performance and optimize operations. These technological innovations are enhancing efficiency, reducing costs, and supporting large-scale adoption across utility, industrial, and residential applications.

• In September 2025, Tesla, Inc. introduced its 20 MWh “Megablock” battery energy storage system, integrating multiple Megapack units for utility-scale deployments. The system enhances grid scalability and enables faster installation timelines for large projects. Source: www.tesla.com

• In 2025, Tesla, Inc. reported record energy storage deployments of 46.7 GWh, marking the highest annual installation volume for its energy division. This reflects strong global demand for Megapack and Powerwall systems in both utility and residential sectors.

• In April 2025, Contemporary Amperex Technology Co., Limited (CATL) launched its “Naxtra” sodium-ion battery brand, designed for large-scale energy storage and EV applications. The battery achieves 175 Wh/kg energy density and supports fast charging and improved safety compared to conventional lithium-ion systems.

• In April 2024, Contemporary Amperex Technology Co., Limited (CATL) unveiled its “TENER” grid-scale energy storage system, featuring 6.25 MWh capacity per unit and zero degradation over five years, significantly improving lifecycle performance and operational stability for utility-scale deployments.

The scope of the Energy Storage Systems Market Report encompasses a comprehensive analysis of technologies, applications, and end-user segments across global regions. The report covers key storage technologies including lithium-ion, lead-acid, flow batteries, sodium-ion systems, and emerging solutions such as hydrogen and thermal storage. It evaluates application areas such as utility-scale grid storage, commercial and industrial energy management, and residential energy storage systems, providing insights into adoption patterns and operational performance.

Geographically, the report analyzes major regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, highlighting regional variations in deployment, infrastructure development, and policy frameworks. The report also examines industry verticals such as utilities, manufacturing, energy, and residential sectors, identifying key demand drivers and adoption trends.

Additionally, the scope includes technological advancements such as AI-driven energy management, hybrid storage systems, and battery recycling innovations. It further explores emerging trends such as decentralized energy systems, microgrids, and long-duration storage solutions. The report provides detailed insights into competitive dynamics, investment trends, and innovation strategies shaping the market landscape. Overall, it offers a holistic view of the Energy Storage Systems Market, enabling stakeholders to make informed strategic decisions and capitalize on growth opportunities across diverse industry segments.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,800.0 Million |

| Market Revenue (2033) | USD 5,182.6 Million |

| CAGR (2026–2033) | 8.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Tesla Inc.; LG Energy Solution Ltd.; Panasonic Corporation; BYD Company Ltd.; Samsung SDI Co., Ltd.; Fluence Energy, Inc.; Contemporary Amperex Technology Co., Limited (CATL); Siemens Energy AG; General Electric Company; ABB Ltd.; Hitachi Energy Ltd.; Schneider Electric SE; Toshiba Corporation; Enphase Energy, Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |