Reports

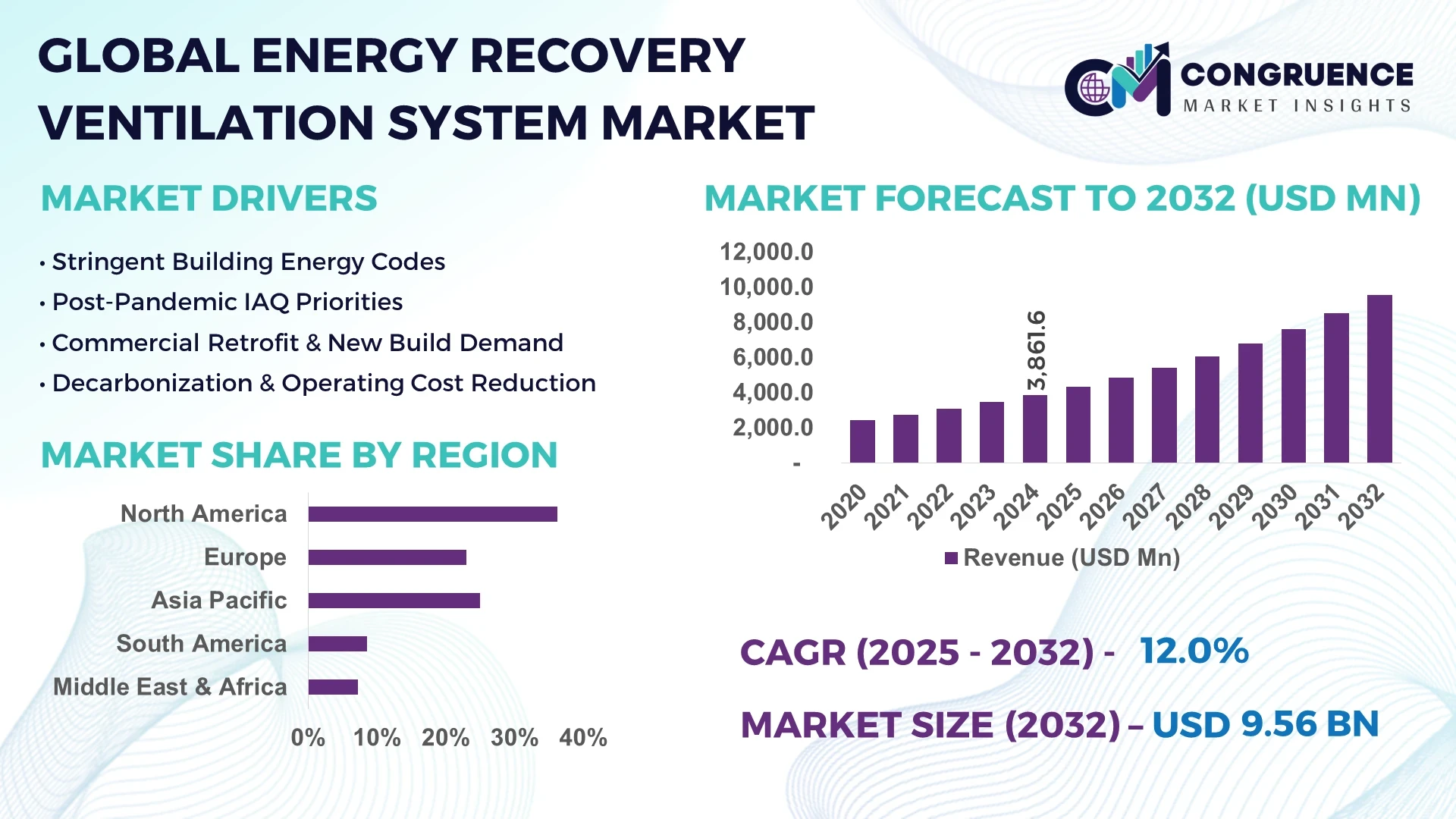

The Global Energy Recovery Ventilation System Market was valued at USD 3,861.64 Million in 2024 and is anticipated to reach a value of USD 9,561.29 Million by 2032 expanding at a CAGR of 12.0% between 2025 and 2032.

The United States, as the dominant country, maintains extensive production capacity for advanced energy recovery ventilation systems with consistent investment in R&D and high-level deployment across commercial and industrial sectors supported by evolving HVAC integration standards and technological advancements in component efficiency.

The Energy Recovery Ventilation System Market is evolving rapidly, driven by stringent indoor air quality standards and rising energy efficiency mandates across regions. Industries such as healthcare, education, commercial offices, and data centers are adopting high-efficiency ERV systems to reduce operational costs while maintaining regulatory compliance on ventilation standards. The integration of heat and moisture recovery technology is becoming a critical focus area, allowing systems to operate efficiently across varying climatic conditions. Advanced filtration modules and automated control interfaces are being integrated to improve operational convenience and monitoring in real-time, ensuring consistent energy savings and extended system lifespans. Additionally, the growing emphasis on sustainable building certifications, including LEED and WELL standards, has boosted the demand for ERV systems as part of green building initiatives globally. With increased urbanization and industrialization, the regional consumption pattern is tilting toward demand for high-capacity centralized systems in Asia-Pacific and Europe, while modular, scalable systems are gaining traction in North America to address retrofitting and space constraints in aging building infrastructures.

Artificial Intelligence (AI) is profoundly reshaping the Energy Recovery Ventilation System Market, enhancing operational performance, predictive maintenance, and system efficiency for facility managers and OEMs alike. By deploying machine learning algorithms, ERV systems can now predict optimal operation schedules based on occupancy patterns and real-time indoor air quality data, ensuring consistent energy conservation without compromising ventilation standards. AI-powered fault detection mechanisms are being utilized to identify and address performance anomalies before they escalate into costly system downtimes, significantly reducing maintenance expenses for commercial buildings.

AI integration within the Energy Recovery Ventilation System Market has also advanced component-level optimization by fine-tuning fan speeds, damper positions, and heat exchanger functions in response to humidity and temperature fluctuations, delivering tangible energy savings across large-scale industrial facilities and high-rise office buildings. Additionally, AI-powered analytics platforms are aiding manufacturers in enhancing system designs based on real-world performance data, shortening product development cycles while addressing user-specific climate challenges. Cloud-connected ERV systems are leveraging AI to create actionable insights, driving facility managers to implement adaptive ventilation strategies aligned with dynamic energy pricing models to minimize operational expenditures. The trend toward smart building ecosystems is fostering deeper AI integration within the Energy Recovery Ventilation System Market, making systems more responsive, sustainable, and economically efficient while aligning with decarbonization goals and green building certifications.

“In February 2025, a leading HVAC technology firm integrated an AI-based dynamic control system within its Energy Recovery Ventilation System product line, resulting in a documented 19% improvement in energy efficiency across multi-tenant office buildings by automatically adjusting ventilation rates based on CO₂ sensors and occupancy data.”

The Energy Recovery Ventilation System Market is experiencing strong momentum driven by stringent indoor air quality regulations, rising energy efficiency standards, and the global push for decarbonization within the building and industrial sectors. Advanced ERV systems are being rapidly adopted across healthcare facilities, commercial complexes, and manufacturing sites due to their ability to reduce HVAC energy consumption while maintaining precise ventilation control. Technological advancements such as integration with building management systems and AI-powered predictive maintenance capabilities are enhancing the operational effectiveness and reliability of ERV systems, leading to greater interest among facility managers seeking sustainable solutions. Growing urbanization and expansion of smart cities are further increasing demand for high-performance, automated ventilation systems that align with green building certifications and evolving environmental regulations.

Rising enforcement of indoor air quality (IAQ) standards globally is a significant driver for the Energy Recovery Ventilation System Market, pushing the adoption of ERV systems in various commercial and industrial buildings. For instance, the U.S. ASHRAE 62.1 and European EN 16798 standards are compelling facility managers to integrate systems capable of maintaining fresh air levels while conserving energy. ERV systems help facilities meet these standards by recovering heat and moisture from exhaust air to precondition incoming fresh air, effectively reducing HVAC loads by up to 50% in many cases. Educational institutions, healthcare facilities, and corporate offices are increasingly investing in these systems to ensure compliance, reduce energy consumption, and maintain a healthy indoor environment, driving steady demand in the market.

The Energy Recovery Ventilation System Market faces challenges from high upfront costs and the complexity associated with integrating ERV systems into existing building infrastructures. Retrofitting older buildings often requires significant modifications to ductwork and ventilation layouts, leading to increased installation costs and project timelines. Additionally, advanced ERV systems with integrated controls and high-efficiency heat exchangers can have a higher capital cost, which can deter small and medium-sized facility owners from adoption despite the long-term energy savings. These challenges are particularly evident in markets with older building stocks and limited budgets for infrastructure upgrades, where decision-makers may postpone investments, thereby slowing down potential market expansion.

Integration of Energy Recovery Ventilation Systems with smart building technologies presents a substantial opportunity for market growth, enhancing system efficiency and user control while aligning with sustainability goals. Smart ERV systems equipped with sensors, IoT connectivity, and AI analytics allow real-time monitoring of indoor air quality and dynamic adjustment of ventilation rates based on occupancy and environmental data. This not only improves operational efficiency but also aligns with energy-saving objectives for green-certified buildings. The growing adoption of smart buildings globally, particularly in urban developments and corporate campuses, is creating avenues for ERV manufacturers to offer innovative, integrated solutions that support decarbonization while improving tenant comfort and operational efficiency.

The Energy Recovery Ventilation System Market is challenged by ongoing maintenance requirements and the technical expertise needed for system management and optimization. High-efficiency ERV systems require periodic cleaning of heat exchangers, filter replacements, and calibration of control systems to maintain peak performance, increasing the operational demands on facility teams. In many regions, there is a shortage of technicians trained specifically to manage and troubleshoot advanced ERV systems, leading to potential system inefficiencies or downtimes. Additionally, facility managers without experience in managing integrated HVAC systems may underutilize the full capabilities of advanced ERV technologies, affecting energy savings and operational goals, thus posing a significant challenge to broader adoption and consistent performance outcomes.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction methods is reshaping demand in the Energy Recovery Ventilation System market. Prefabricated ERV modules are being integrated into modular construction workflows, reducing installation time by up to 40% while maintaining system quality. In Europe and North America, commercial developers are actively shifting toward modular high-rise and healthcare projects, creating consistent demand for scalable, high-efficiency ERV systems that align with fast project turnovers. This trend enables developers to integrate advanced ventilation with reduced on-site labor requirements while ensuring compliance with green building standards.

• Integration with IoT and Smart Building Platforms: IoT integration is emerging as a transformative trend in the Energy Recovery Ventilation System market, enabling real-time monitoring of indoor air quality and energy performance. Advanced ERV systems now feature embedded sensors that track humidity, CO₂, and VOC levels, adjusting ventilation rates automatically to optimize indoor environments. In large commercial buildings, this has led to energy savings of over 20% while ensuring consistent air quality compliance. Smart building integration supports predictive maintenance and advanced fault detection, reducing operational disruptions while aligning with decarbonization targets.

• Demand for Advanced Heat and Moisture Recovery Technologies: The market is witnessing rising interest in ERV systems capable of simultaneous heat and moisture recovery, crucial for maintaining indoor comfort in diverse climatic conditions. In humid regions, these systems prevent excess moisture ingress while recovering latent heat, reducing the load on HVAC systems. In colder climates, heat recovery wheel technologies are seeing higher adoption in healthcare and educational facilities to maintain indoor thermal comfort without increasing energy consumption. Manufacturers are focusing on compact, high-efficiency cores that improve recovery rates by 10–15% while maintaining low pressure drops.

• Regulatory Push for Enhanced Indoor Air Quality Standards: Governments are tightening indoor air quality regulations, accelerating the adoption of Energy Recovery Ventilation Systems in hospitals, schools, and commercial spaces. New standards requiring continuous ventilation in public spaces have driven facility managers to replace or upgrade existing systems with ERVs capable of maintaining constant airflow while minimizing energy use. This regulatory push is also influencing retrofitting projects across older building stocks, creating steady demand for compact, high-efficiency ERV units suitable for space-constrained environments while ensuring compliance with evolving IAQ guidelines.

The Energy Recovery Ventilation System market segmentation spans product types, applications, and end-user categories, each shaping market dynamics uniquely. Types include plate heat exchangers, heat pipe heat exchangers, rotary heat exchangers, and run-around coil systems, each addressing specific operational needs within commercial and industrial HVAC systems. Application areas cover residential, commercial, and industrial settings, driven by varying requirements for indoor air quality management and energy savings. End-users such as hospitals, educational institutions, office buildings, and manufacturing facilities form the backbone of demand, each investing in ERV systems to comply with evolving IAQ regulations while improving operational efficiency. This segmentation allows stakeholders to align product offerings strategically with emerging trends like decarbonization, smart building integration, and modular construction demand, ensuring effective market positioning.

Plate heat exchangers lead the Energy Recovery Ventilation System market due to their compact design, ease of maintenance, and high heat recovery efficiency, making them ideal for commercial office buildings and healthcare facilities. Their ability to maintain separation between exhaust and fresh air streams aligns with hygiene standards in sensitive environments. Rotary heat exchangers are the fastest-growing type, driven by their capability to recover both sensible and latent heat, making them suitable for regions with high humidity levels. Heat pipe heat exchangers and run-around coil systems maintain relevance in niche applications requiring isolated air streams or where installation flexibility is critical, such as in retrofitting projects. Each type's contribution reflects operational needs and climate-specific demands, supporting the growth and diversification of the ERV system landscape while catering to evolving building standards globally.

Commercial applications dominate the Energy Recovery Ventilation System market, driven by the increasing need for energy-efficient solutions in office buildings, retail complexes, and healthcare facilities. These applications prioritize continuous ventilation while reducing HVAC loads to lower operational expenses and enhance indoor air quality. The fastest-growing application segment is industrial facilities, where strict environmental and workplace safety regulations are pushing the adoption of ERV systems to manage air quality while maintaining production environment control. Residential applications, while slower in adoption, are seeing gradual growth with rising awareness of IAQ and the inclusion of ERV systems in sustainable housing projects. The diversity of applications ensures that ERV manufacturers can align their systems with varied regulatory, operational, and comfort requirements across market verticals.

Hospitals and healthcare facilities lead the Energy Recovery Ventilation System market among end-users due to their strict air quality standards and need for reliable ventilation without cross-contamination. These facilities deploy high-efficiency ERV systems to maintain sterile environments while reducing energy consumption across critical care and patient areas. The fastest-growing end-user segment is educational institutions, driven by post-pandemic air quality initiatives and government funding for healthier indoor environments, leading to a surge in ERV installations across schools and universities. Office buildings, retail spaces, and manufacturing facilities also form essential end-user groups, investing in ERV systems to improve energy efficiency and indoor air quality, reflecting the broader trend toward sustainable building operations in both new constructions and retrofit projects.

North America accounted for the largest market share at 36.2% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.4% between 2025 and 2032.

The Energy Recovery Ventilation System Market in North America is driven by strong adoption across healthcare and commercial sectors, supported by advanced HVAC infrastructure and energy efficiency mandates. In Europe, regulatory frameworks emphasizing decarbonization and green building certifications are propelling the demand for advanced ERV systems across Germany, the UK, and France. Asia-Pacific's rapid urbanization and infrastructure expansion in China, India, and Japan are fueling system installations for residential and commercial applications. South America is witnessing gradual adoption in Brazil and Argentina due to government incentives for energy efficiency. In the Middle East & Africa, construction growth in the UAE and Saudi Arabia is boosting demand for high-efficiency ventilation systems, aligning with sustainability goals and modernization initiatives in building technologies across the region.

AI-Enabled Air Quality Management Transforming System Deployments

The Energy Recovery Ventilation System Market in this region held a 36.2% share in 2024, driven by increasing demand from healthcare, education, and commercial office sectors prioritizing indoor air quality improvements. Regulatory frameworks, including stricter indoor air quality mandates and state-level energy conservation codes, are encouraging the adoption of high-efficiency ERV systems across facilities. Digital transformation trends, particularly the integration of IoT-based monitoring and AI-powered predictive maintenance within ERV systems, are enhancing operational efficiencies while reducing maintenance costs. The push for decarbonization across urban developments and retrofitting of aging HVAC systems with energy recovery technologies continues to expand the regional ERV market.

Decarbonization Policies Fueling Advanced Ventilation Adoption

Holding a 29.7% market share in 2024, the Energy Recovery Ventilation System Market in this region is supported by key markets including Germany, the UK, and France, each emphasizing energy efficiency in building operations through regulatory policies such as the European Green Deal and local building codes. Notable adoption of emerging technologies like demand-controlled ventilation and moisture recovery solutions is driving installations in healthcare, commercial offices, and educational facilities. Regulatory bodies across the region are pushing for near-zero energy buildings, prompting rapid replacement of traditional ventilation systems with high-efficiency ERV systems that meet stringent sustainability standards while reducing energy consumption.

Urban Expansion Driving High-Efficiency System Demand

Asia-Pacific ranked as the fastest-growing region for the Energy Recovery Ventilation System Market, driven by expanding infrastructure across China, India, and Japan. These countries are leading the regional demand for ERV systems due to rising urbanization and the rapid development of smart cities integrating advanced HVAC systems for energy-efficient building management. Prefabricated and modular construction trends are further increasing demand for scalable ERV solutions within commercial and residential projects. Regional technology innovation hubs are advancing compact, high-performance ERV units suited for varied climatic conditions, while manufacturers are investing in digital platforms to enhance monitoring and control capabilities within building ventilation systems.

Energy Efficiency Incentives Supporting System Uptake

In this region, Brazil and Argentina are the primary contributors to the Energy Recovery Ventilation System Market, with Brazil leading in system installations across the healthcare and education sectors due to government-backed energy efficiency initiatives. The market in the region is witnessing steady demand as urban centers expand and local regulations encourage improved indoor air quality standards. Infrastructure investments in commercial and industrial facilities are driving installations of ERV systems designed to reduce HVAC energy consumption while aligning with sustainable building targets. Trade policies promoting the import of advanced HVAC technologies are further enabling the adoption of high-efficiency ventilation solutions.

Smart Building Integration Boosting System Installations

The Energy Recovery Ventilation System Market in this region is witnessing increasing demand in the UAE and Saudi Arabia, driven by rapid construction growth across commercial and residential sectors. Adoption of smart building technologies and modernization of HVAC systems are becoming central to regional infrastructure development strategies, with ERV systems playing a critical role in maintaining indoor air quality while reducing energy usage. Regulations promoting energy efficiency within the built environment and partnerships under regional sustainability initiatives are further driving demand. The oil & gas sector’s movement toward sustainable facility operations is also creating opportunities for ERV installations in industrial environments.

United States – 32.4% market share: Strong end-user demand in healthcare and commercial sectors supported by advanced HVAC infrastructure and stringent IAQ regulations drive the Energy Recovery Ventilation System Market in the United States.

China – 19.6% market share: High production capacity and rapid urban infrastructure expansion across commercial and residential sectors support the Energy Recovery Ventilation System Market in China.

The Energy Recovery Ventilation System market features a competitive environment with over 50 active global and regional players focusing on technology advancements, portfolio expansion, and strategic partnerships to strengthen market positioning. Key competitors are emphasizing the development of high-efficiency ERV systems with integrated smart controls and IoT-based monitoring capabilities to cater to evolving regulatory and indoor air quality standards across regions. Product launches featuring compact, modular designs for retrofitting applications and high-capacity centralized systems for large facilities are shaping competitive differentiation. Collaborations with construction firms and green building solution providers are enabling market players to align with decarbonization initiatives and sustainable infrastructure goals globally. Mergers and acquisitions among established HVAC manufacturers and technology startups are supporting innovation in sensor-based demand-controlled ventilation and AI-powered predictive maintenance solutions. This competitive landscape is fostering a dynamic market environment where manufacturers are focusing on digital transformation, energy efficiency optimization, and expanding their global distribution networks to address rising demand across healthcare, commercial, and industrial sectors.

Daikin Industries Ltd.

Mitsubishi Electric Corporation

Johnson Controls International plc

Lennox International Inc.

Panasonic Corporation

Greenheck Fan Corporation

Zehnder Group AG

Systemair AB

Swegon Group AB

Aldes Group

Current and emerging technologies are significantly shaping the Energy Recovery Ventilation System market, focusing on enhancing operational efficiency, reducing energy consumption, and improving indoor air quality management. Advanced heat exchanger technologies, such as enthalpy wheels and polymer membrane cores, are being utilized to achieve higher thermal and moisture recovery rates while maintaining low pressure drops, improving system efficiency by up to 15% in various climate zones. Integration of IoT and smart sensors enables real-time monitoring of CO₂, VOCs, temperature, and humidity, allowing demand-controlled ventilation adjustments that can reduce energy consumption by 20% while ensuring optimal air quality.

AI-powered predictive maintenance technologies are being adopted to analyze performance data, detect system anomalies, and automate service scheduling, reducing unplanned downtimes and extending equipment lifespan. Compact, modular ERV units designed for retrofitting in space-constrained environments are gaining traction, particularly in urban buildings and healthcare facilities requiring continuous ventilation upgrades. Digital twin models are emerging, enabling simulation of ERV system performance under varying occupancy and environmental conditions, helping facility managers optimize configurations. The integration of ERV systems with Building Energy Management Systems (BEMS) is further enhancing the market by enabling centralized control and data-driven decision-making aligned with green building standards and decarbonization goals globally.

• In February 2023, Panasonic launched its new energy recovery ventilation system featuring nanoe™ X technology, capable of inhibiting certain bacteria and viruses while providing continuous ventilation, designed for commercial offices and schools aiming to improve indoor air quality with lower energy consumption.

• In May 2023, Daikin Industries introduced a compact ERV unit designed for retrofitting in high-rise residential buildings, utilizing high-efficiency heat exchange cores and low-noise fans, enabling up to 35% energy savings while maintaining continuous fresh air supply.

• In March 2024, Johnson Controls unveiled an AI-enabled ERV control system that dynamically adjusts ventilation rates based on occupancy and indoor air quality data, achieving a documented 18% improvement in energy efficiency across large commercial installations during pilot projects.

• In July 2024, Zehnder Group launched a next-generation enthalpy exchanger ERV system tailored for healthcare facilities, featuring advanced filtration, antimicrobial treatment, and moisture recovery capabilities, aligning with stricter hygiene standards while supporting lower operational energy use.

The Energy Recovery Ventilation System Market Report comprehensively covers the analysis of product types, including plate heat exchangers, rotary heat exchangers, heat pipe systems, and run-around coil systems, with insights into their operational advantages and adoption patterns across regions. The report evaluates applications in residential, commercial, and industrial sectors, focusing on healthcare facilities, educational institutions, data centers, and office complexes where ventilation efficiency and air quality management are critical.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, detailing regional drivers such as regulatory frameworks, infrastructure growth, and energy efficiency mandates influencing market dynamics. Technological analysis within the report highlights the integration of IoT sensors, AI-based predictive maintenance, and advanced moisture recovery solutions, reflecting the shift toward smart, energy-efficient buildings and sustainable development practices.

Additionally, the report outlines emerging segments such as retrofitting solutions for aging infrastructure, the integration of ERV systems within modular and prefabricated construction projects, and opportunities in niche markets like controlled environment agriculture facilities requiring precise climate and air quality management. This structured scope supports stakeholders in identifying opportunities, understanding technology advancements, and aligning strategic initiatives with evolving regulatory and sustainability trends across the Energy Recovery Ventilation System market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3,861.64 Million |

|

Market Revenue in 2032 |

USD 9,561.29 Million |

|

CAGR (2025 - 2032) |

12% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Daikin Industries Ltd., Mitsubishi Electric Corporation, Johnson Controls International plc, Lennox International Inc., Panasonic Corporation, Greenheck Fan Corporation, Zehnder Group AG, Systemair AB, Swegon Group AB, Aldes Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |