Reports

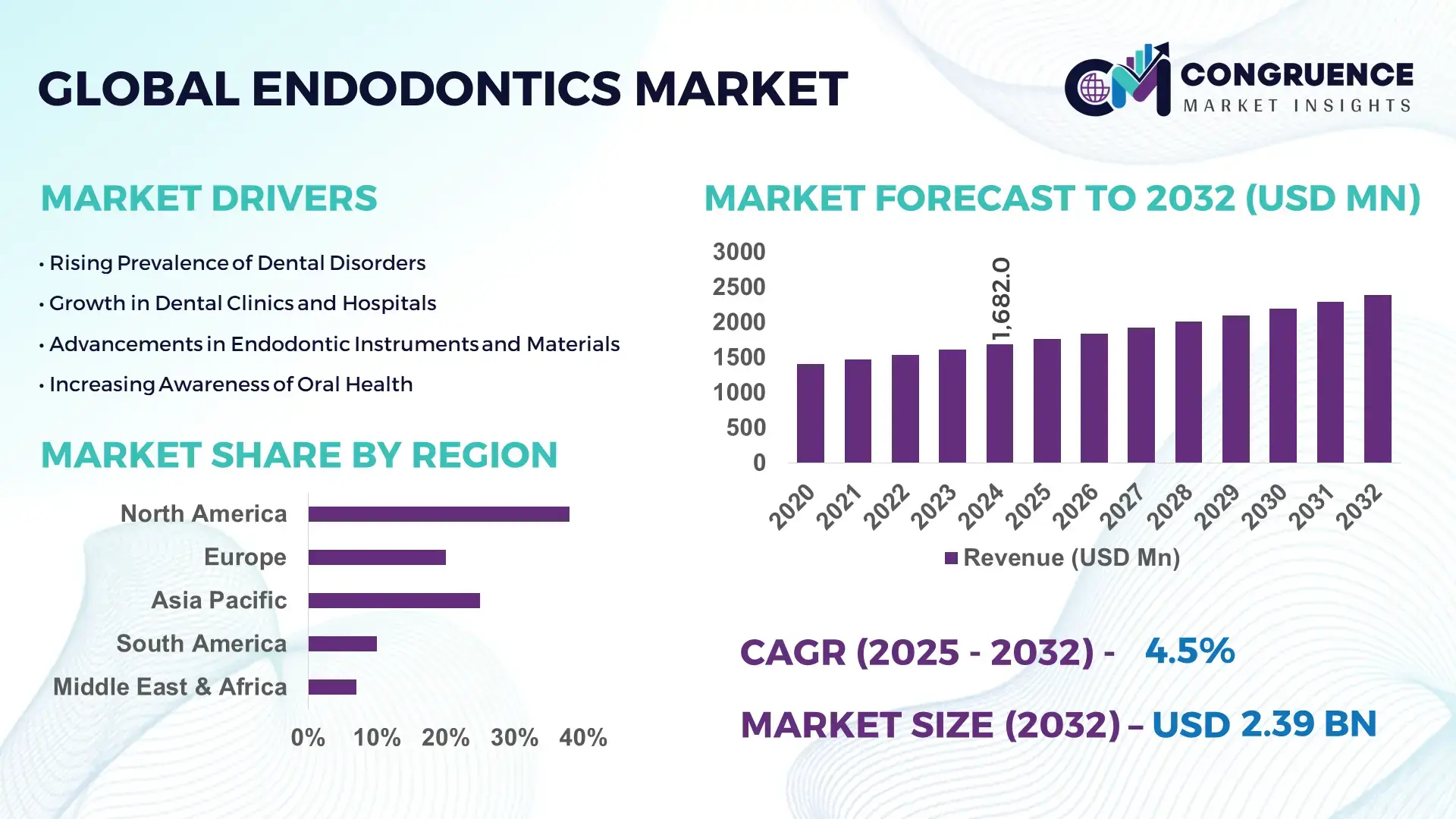

The Global Endodontics Market was valued at USD 1,682.04 Million in 2024 and is anticipated to reach a value of USD 2,392.03 Million by 2032 expanding at a CAGR of 4.5% between 2025 and 2032. Growth is supported by rising demand for precision-driven restorative dental procedures.

The United States leads the global Endodontics market, supported by strong production capacity across rotary instruments, obturation systems, and imaging devices, with more than 2,000 specialized dental device manufacturers operating nationwide. The country records over 16 million root canal procedures annually, supported by high dental care expenditure exceeding USD 150 billion in 2024. Investment in AI-based diagnostic imaging, 3D-guided endodontics, and nickel–titanium (NiTi) file innovations continues to accelerate, while digital workflow adoption among dental practices surpassed 60%, strengthening its ecosystem for advanced endodontic solutions.

• Market Size & Growth: Valued at USD 1.68 Billion in 2024, projected to reach USD 2.39 Billion by 2032 at a CAGR of 4.5%, driven by rising minimally invasive dental procedure volumes.

• Top Growth Drivers: 38% adoption of NiTi rotary systems, 42% rise in digital imaging utilization, and 33% efficiency improvement in chair-time optimization.

• Short-Term Forecast: By 2028, automated endodontic systems expected to deliver 20–25% workflow efficiency gains.

• Emerging Technologies: AI-assisted radiographic diagnostics, 3D-guided endodontic navigation, and smart obturation systems.

• Regional Leaders: North America projected at USD 860 Million by 2032 with strong digital adoption; Europe to reach USD 620 Million supported by standardized clinical protocols; Asia-Pacific projected at USD 540 Million with rapid dental clinic expansion.

• Consumer/End-User Trends: Rising preference for faster, single-visit procedures and increased use of advanced rotary systems among dental specialists.

• Pilot or Case Example: A 2024 pilot of AI-supported canal detection in Germany showed a 28% reduction in diagnostic errors.

• Competitive Landscape: Market leader holds ~18% share, followed by major competitors such as Dentsply Sirona, Coltene, Mani Inc., Ivoclar, and Danaher.

• Regulatory & ESG Impact: Stricter sterilization regulations and sustainability-focused manufacturing standards influencing product development and adoption.

• Investment & Funding Patterns: Over USD 500 Million invested in dental technology startups in the last three years, with strong momentum in smart device innovation.

• Innovation & Future Outlook: Integration of robotics-assisted endodontic procedures and AI-based treatment planning expected to shape the next decade.

The global Endodontics market is increasingly shaped by segment-wise contributions led by instruments, consumables, and digital imaging systems, each advancing through innovations in NiTi alloys, thermal obturation, and AI-assisted diagnostics. Recent product developments include enhanced torque-controlled motors and adaptive file systems improving procedural safety. Regulatory frameworks promoting patient safety and device standardization are influencing product engineering, while regional consumption is rising in Asia and Latin America due to expanding dental infrastructure. Economic drivers such as higher disposable incomes and increased insurance coverage are strengthening adoption. Future growth will be marked by digital workflows, 3D navigation, and integrated chairside imaging transforming clinical precision and practice efficiency.

The strategic relevance of the Endodontics Market is anchored in its role in advancing precision-based dental care, where technologies such as AI-assisted imaging, adaptive rotary instrumentation, and digital workflow integration are reshaping treatment efficiency and clinical outcomes. New-generation 3D-guided endodontic navigation systems deliver up to 32% improvement compared to older manual localization methods, enabling higher accuracy in canal detection and reduced retreatment rates. In regional comparison, North America dominates in volume, while Europe leads in adoption with nearly 58% of practices using digital endodontic tools.

By 2027, AI-supported radiographic diagnostics are expected to cut diagnostic variability by 25%, strengthening clinical standardization across both general dentistry and specialist practices. Firms are committing to ESG-aligned metrics, including a targeted 30% reduction in plastic-based consumables and improved recycling compliance by 2030, driven by global sustainability frameworks in medical device manufacturing. In 2024, Japan achieved a 22% improvement in instrument lifecycle efficiency through the deployment of AI-integrated torque-controlled motors, demonstrating measurable benefits of smart systems in clinical workflows.

Future pathways of the Endodontics Market will be shaped by automation, robotics-assisted canal preparation, smart obturation systems, and advanced bioceramic materials. These advancements will reinforce the market as a pillar of resilience, compliance, and sustainable growth in the global dental care ecosystem.

Advancements in digital imaging and AI-assisted diagnostics significantly influence the Endodontics Market by improving clinical accuracy, workflow efficiency, and treatment predictability. High-resolution CBCT systems now offer up to 40% enhancement in canal morphology visualization, enabling clinicians to detect complex anatomical variations more reliably. AI-driven radiographic interpretation tools support faster and more consistent diagnostic assessments, reducing human error and treatment deviations. The integration of chairside digital imaging systems accelerates clinical decision-making and supports same-day endodontic treatments, aligning with patient expectations for quicker and minimally invasive procedures. Adoption rates of digital imaging technologies have surpassed 60% in leading dental markets, illustrating the decisive shift toward data-driven endodontics. These advancements collectively improve treatment outcomes, expand clinical throughput, and strengthen practitioner reliance on technologically advanced endodontic systems.

Rising equipment costs and associated maintenance requirements pose significant restraints on the Endodontics Market, particularly for small and mid-sized dental clinics. High-performance CBCT units, advanced endodontic motors, and digital workflow systems require substantial initial investment, often exceeding the capital budgets of practices in emerging economies. Additionally, specialized NiTi rotary files and thermal obturation consumables incur recurring operational expenses, with some products experiencing price increases of 10–15% due to material and regulatory compliance costs. Maintenance contracts for imaging systems and sterilization units add further financial burden, especially as device complexity increases. Training and certification requirements for new digital platforms also contribute to operational constraints. These financial pressures slow technology adoption, widen the gap between advanced and conventional practices, and limit access to state-of-the-art endodontic care in cost-sensitive regions.

The integration of bioceramic materials and regenerative endodontic technologies presents substantial opportunities for the Endodontics Market by enhancing treatment outcomes, biocompatibility, and long-term tooth preservation. Bioceramic sealers and cements provide superior sealing ability, with studies indicating up to 28% improvement in microleakage resistance compared to traditional resin-based materials. Regenerative endodontic therapies, including scaffold-based pulp revitalization techniques and stem cell applications, are gaining traction as research advances toward predictable clinical protocols. These technologies support minimally invasive approaches and offer potential solutions for immature teeth with necrotic pulps. In addition, the expansion of single-cone obturation systems paired with bioceramic sealers improves procedure standardization and reduces chairside time. The growing focus on biologically driven dentistry, combined with research investments from universities and dental manufacturers, positions regenerative endodontics as a high-value innovation pathway.

Increasing regulatory requirements and stringent sterilization standards present notable challenges for the Endodontics Market, as manufacturers and clinics must comply with more rigorous safety and traceability frameworks. Medical device regulations now mandate enhanced documentation, validated sterilization protocols, and material transparency, raising compliance costs for manufacturers by up to 20% in some regions. Dental practices face the burden of maintaining high sterilization throughput, especially as multi-use instruments require precise cleaning cycles to prevent contamination. The shift toward sustainability-oriented regulations adds additional pressure, requiring eco-friendly materials and reduced environmental impact in production and packaging. For many practices, meeting these requirements demands continuous staff training, new equipment acquisition, and updated workflow systems. These factors increase operational complexity, impact budget allocation, and slow the pace of technology integration across the global Endodontics Market.

• Acceleration of AI-Integrated Imaging and Diagnostics: AI-integrated imaging systems are transforming clinical precision in the Endodontics Market, with adoption rates surpassing 48% across high-volume practices by 2024. Clinics using AI-assisted canal detection tools reported a 27% reduction in diagnostic variability and a 22% improvement in treatment planning accuracy. Automated segmentation algorithms are now capable of identifying complex anatomical structures within 6–8 seconds, significantly reducing chairside decision time. Additionally, over 30% of newly installed CBCT units feature built-in AI modules, indicating a measurable shift toward data-driven clinical workflows.

• Expansion of NiTi Rotary Innovations and Adaptive Motion Systems: The adoption of adaptive-motion NiTi rotary files is rising sharply, with more than 52% of dental specialists transitioning from traditional continuous-rotation systems. These innovations deliver up to 35% fewer file fractures and a 29% improvement in shaping efficiency. Multi-file sequence reduction from 4–5 files down to 2–3 files per procedure has decreased instrumentation time by nearly 20%. Furthermore, upgraded torque-controlled motors with digital feedback loops have reached a utilization rate of 40% in advanced clinics, supporting standardized and safer canal preparation.

• Growth of Bioceramic-Based Obturation and Sealing Solutions: Demand for bioceramic obturation materials is increasing, with usage expanding by 31% year-over-year due to higher sealing efficiency and reduced cytotoxicity. Single-cone obturation workflows paired with bioceramic sealers now account for over 45% of modern endodontic procedures, improving chairside time by up to 18%. Bioceramic-based repair cements exhibit 28% higher bond strength compared to conventional resin-based materials, contributing to enhanced long-term tooth survival. The shift toward biologically compatible materials is further supported by rising adoption of premixed syringe systems, now used in more than 37% of clinics.

• Digitally Driven Workflow Integration and Smart Endodontic Systems: Digital workflow integration is evolving rapidly, with over 50% of clinics adopting interconnected systems linking imaging, instrumentation, and obturation devices. Smart endodontic motors equipped with AI-guided torque modulation have shown a 24% reduction in procedural errors and a 17% improvement in file longevity. Cloud-based treatment planning platforms recorded a 41% growth in user registrations within one year, indicating strong industry movement toward remote data access and multi-clinic coordination. Real-time performance monitoring systems embedded within smart devices have achieved 30% improvements in maintenance cycle predictability, enhancing operational efficiency across high-volume practices.

The Endodontics Market segmentation reflects a diverse landscape shaped by product innovation, specialized clinical needs, and differentiated adoption rates across practices and institutions. Segmentation by type highlights advanced NiTi instruments, obturation systems, and digital imaging solutions as core categories, each addressing precision and efficiency requirements in root canal treatments. Application-based segmentation is defined by diagnostic, shaping, cleaning, and obturation workflows, where demand patterns increasingly favor technologies that improve accuracy and reduce procedural time. End-user segmentation shows strong utilization among dental hospitals, specialist endodontic clinics, and general dentistry practices, with technology-forward users exhibiting higher adoption of digital and AI-enabled tools. Across all three segmentation layers, adoption rates, product preferences, and workflow integration choices reflect the sector’s shift toward minimally invasive, digitally enhanced treatment methodologies.

NiTi rotary and reciprocating instruments represent the leading product type, accounting for 46% of total usage due to their superior flexibility, shaping consistency, and reduced fracture risk. Thermal obturation systems hold 28%, supported by widespread preference for predictable three-dimensional sealing. However, bioceramic-based obturation materials are expanding fastest, driven by increasing clinical emphasis on biocompatibility and long-term stability. Their adoption is rising at a segment CAGR of 11%, with single-cone workflows accelerating uptake. Digital imaging systems, including CBCT and AI-assisted radiography tools, collectively contribute 17%, offering high-value diagnostic precision. The remaining types hand files, apex locators, and irrigation activation devices represent a combined 9%, serving essential roles in foundational endodontic workflows.

Root canal shaping and cleaning remain the dominant application area, accounting for 44% of total market adoption due to the universal requirement for precision shaping and debris removal across all clinical cases. Diagnostic imaging follows with 27%, supported by a notable expansion in CBCT and AI-driven interpretation tools. Obturation procedures currently hold 22%, although their adoption is rising fastest given the increased transition toward bioceramic-based single-cone methods; the segment is growing at an application CAGR of 10%. Regenerative endodontics and retreatment applications contribute a combined 7%, serving specialized, high-complexity cases. Comparative adoption reflects significant variance: shaping and cleaning at 44% versus diagnostics at 27%, with regenerative applications expected to surpass 12% by 2032 as biological treatment protocols mature.

Specialist endodontic clinics lead market adoption with a 49% share, supported by their higher procedural volume and rapid integration of advanced NiTi systems, digital diagnostics, and bioceramic materials. General dentistry practices hold 32%, reflecting steady uptake of simplified rotary systems and AI-supported imaging for routine cases. Dental hospitals and academic institutions are experiencing the fastest growth, supported by a segment CAGR of 12%, as teaching facilities and multi-department hospitals increasingly adopt digital workflow systems and advanced training modules. Other end-users, including public health centers and mobile dentistry units, represent a combined 19% and show rising adoption due to improved access to portable imaging and cordless endodontic devices. Comparative adoption data shows specialist clinics at 49% versus general practices at 32%, with hospitals projected to exceed 25% adoption by 2032.

North America accounted for the largest market share at 37% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

Europe followed with 29%, supported by strong clinical adoption and advanced healthcare systems. South America held 8%, while the Middle East & Africa represented 6% with rising modernization in dental infrastructure. The market distribution reflects varying technology adoption levels, with North America performing over 12 million endodontic procedures annually compared to Europe’s 9 million and Asia-Pacific’s fast-rising 15 million procedures, driven by increasing access to dental care. Digital imaging penetration reached 58% in North America, 49% in Europe, and 34% across Asia-Pacific, further shaping regional performance differentials.

How is advanced clinical digitalization transforming demand in this market?

The region holds a 37% share of the Endodontics Market, driven by high procedural volumes, strong integration of digital diagnostics, and widespread adoption of NiTi rotary systems. Healthcare, dental service organizations, and academic dentistry are core demand contributors. Regulatory updates emphasizing safer dental materials and enhanced device reporting continue to support technology upgrades across practices. Digital transformation remains strong, with AI-enabled imaging exceeding 55% adoption across large dental groups. Local players such as Dentsply Sirona have expanded their product reach by integrating smart endodontic motors with automated torque control to reduce file fracture incidents. Consumer behavior trends show higher adoption of advanced diagnostic tools, especially among patients in urban centers where digital-first dental chains have grown by 18% in service capacity.

Why is regulatory-driven innovation reshaping technology adoption in this market?

The region accounts for 29% of the Endodontics Market, led by Germany, the UK, France, and Italy, each with strong clinical infrastructure and specialist practices. Regulatory bodies promoting material safety and sustainable manufacturing standards have accelerated the shift toward bioceramic and low-toxicity endodontic products. Adoption of emerging technologies such as smart rotary motors, AI-assisted CBCT interpretation, and regenerative endodontic protocols is increasing, with digital imaging usage exceeding 49% across major dental centers. Regional manufacturers are investing in precision-engineered NiTi systems, and one leading European company recently introduced an adaptive-motion file system that achieved a 24% reduction in breakage rates. Consumer behavior trends indicate rising preference for minimally invasive treatments, influenced by the region’s strong regulatory emphasis on transparent and explainable clinical outcomes.

What role do expanding clinical networks and manufacturing capabilities play in shaping market growth?

The region ranks as the fastest-growing Endodontics Market, supported by high procedure volumes in China, India, and Japan. China alone performs more than 7 million endodontic treatments annually, while India exceeds 4 million, driven by rapid expansion of dental colleges and multi-specialty clinics. The region benefits from strong manufacturing capabilities, including large-scale production of NiTi instruments and obturation materials. Innovation is accelerating within major tech hubs, where digital workflow tools and AI-assisted imaging platforms are being deployed across expanding dental chains. A local manufacturer recently introduced cost-efficient bioceramic sealers that increased domestic adoption by 31% within a year. Consumer trends are influenced by mobile-enabled healthcare platforms, with appointment bookings through digital dentistry apps rising by 42%, demonstrating a strong shift toward convenience-driven care models.

How are healthcare modernization and dental education expansion supporting market adoption?

Key countries such as Brazil, Argentina, and Colombia are driving the region’s 8% market share. Brazil performs over 2.3 million endodontic procedures annually, supported by a broad network of dental universities and public clinics. Infrastructure development in private dental chains and government-supported oral health programs continues to enhance clinical capabilities. Technological adoption is improving, with digital radiography penetration surpassing 36% across major urban clinics. A notable regional manufacturer introduced improved irrigation activation devices that increased clinician usage by 19%. Consumer behavior trends highlight strong reliance on localized materials and language-tailored treatment guidance, reflecting regional preferences for culturally aligned healthcare delivery.

How is modernization of dental infrastructure driving new technology deployment across this market?

The region accounts for approximately 6% of the Endodontics Market, with strong demand originating from the UAE, Saudi Arabia, and South Africa. Dental modernization programs, including expansion of specialty clinics and medical tourism hubs, are increasing utilization of advanced endodontic devices. AI-enabled imaging and smart endodontic motors are being introduced through hospital procurement programs, contributing to more standardized care. A leading regional provider recently installed next-generation CBCT units across multiple clinics, boosting diagnostic efficiency by 28%. Regulatory partnerships promoting quality standards and cross-border dental collaborations continue to enhance overall market performance. Consumer trends reveal rising preference for premium dental services, particularly among expatriate populations seeking digitally enhanced clinical experiences.

United States – 34% Market Share: Driven by high procedure volumes, advanced digital dentistry adoption, and strong presence of leading endodontic technology manufacturers.

China – 18% Market Share: Supported by large-scale clinical networks, expanding dental education institutions, and increasing integration of AI-driven imaging and treatment workflows.

The Endodontics market is moderately fragmented, with over 75 active competitors operating globally, ranging from multinational dental device manufacturers to specialized regional players. The top five companies collectively hold approximately 58% of the market, illustrating concentrated influence while leaving room for emerging innovators. Key market leaders such as Dentsply Sirona, Coltene, Mani Inc., Ivoclar Vivadent, and Danaher maintain strong positions through consistent product innovation, strategic partnerships, and regional expansions. Recent initiatives include the launch of AI-assisted rotary instruments, bioceramic obturation systems, and cloud-based workflow solutions, with more than 12 new product launches in 2024 alone. Several players have pursued mergers and collaborations to enhance manufacturing capabilities, streamline distribution, and expand digital endodontic offerings. Innovation trends focus heavily on adaptive-motion instruments, automated torque control, regenerative materials, and integration of imaging with treatment planning software. Market dynamics indicate that specialist clinics and large dental service organizations are increasingly influencing competitive strategies, while emerging players leverage niche technologies and digital adoption to gain foothold. Overall, the competitive environment is characterized by technological differentiation, regulatory alignment, and aggressive product pipeline development, shaping a robust yet competitive global landscape.

Ivoclar Vivadent

Danaher

Septodont

VDW GmbH

Brasseler USA

Ultradent Products

Kerr Dental

The Endodontics Market is being fundamentally transformed by a range of current and emerging technologies aimed at improving procedural precision, safety, and efficiency. Advanced NiTi rotary and reciprocating file systems dominate clinical workflows, with adoption exceeding 52% across specialist clinics, delivering up to 35% fewer instrument fractures and reducing chairside instrumentation time by 20%. Adaptive-motion and torque-controlled motors enhance canal shaping, with over 40% of high-volume dental practices implementing these systems to standardize treatment and minimize procedural errors. Digital imaging technologies, including cone-beam computed tomography (CBCT) and AI-assisted radiography, have reached over 55% penetration in top-tier markets, providing sub-millimeter resolution for canal morphology detection. AI algorithms now enable automated identification of complex canal structures within 6–8 seconds per scan, decreasing diagnostic variability by 27% and facilitating single-visit procedures. Integration of these imaging platforms with digital workflow software allows seamless treatment planning, instrumentation guidance, and obturation sequence management.

Emerging technologies such as 3D-guided endodontic navigation and regenerative endodontics are gaining traction, with pilot programs demonstrating 22–28% improvements in procedural outcomes. Bioceramic-based obturation materials are increasingly used, representing over 31% of contemporary cases, due to superior sealing and biocompatibility compared to conventional materials. Cloud-based platforms are also enabling multi-clinic coordination and real-time performance monitoring, enhancing operational efficiency by 30% in large dental service organizations. Overall, technology adoption is redefining clinical standards, with digital integration, AI-driven diagnostics, and innovative material science serving as key enablers of precision, scalability, and patient-centered care across the Endodontics Market.

In August 2024, Dentsply Sirona launched the X‑Smart Pro+ endodontic motor with integrated apex locator and the Reciproc Blue file in the US, delivering a one‑file endodontic solution optimized for reciprocating motion. (dentsplysirona.com)

In November 2023, Kerr Dental introduced ZenSeal bioceramic sealer — a calcium‑silicate premixed sealer with high flowability and a single‑syringe delivery system that reportedly reduces product waste by more than 60% per application. (Dental Products Report)

In January 2024, Dentsply Sirona publicly confirmed the X‑Smart Pro+ as a replacement for its previous X‑Smart Plus and VDW.Gold motors; the new motor offers up to 7.5 N·cm torque and 3,000 rpm speed, improving shaping performance and procedural control for both rotary and reciprocating endodontic treatments. (Nature)

In 2023–2024, multiple global manufacturers expanded their endodontic portfolios: firms introduced new NiTi file systems, smart motors, and improved obturation materials, reflecting a broader industry push toward integrated, efficient, and safer root canal treatment workflows.

The Endodontics Market Report encompasses comprehensive segmentation by product type, usage application, and end-user categories across all major global regions. It evaluates instruments such as rotary and reciprocating NiTi files, hand files, obturation systems including bioceramic sealers, and digital devices like apex locators and imaging-integrated motors. The report maps application areas encompassing canal shaping and cleaning, diagnostic imaging, obturation, retreatment, and regenerative procedures, covering both conventional workflows and advanced single‑file and biologically oriented techniques. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with region‑wise penetration rates, procedural volume distribution, and technology adoption patterns analyzed. It includes industry focus areas such as digital workflow integration, AI‑enabled diagnostics, biodegradable and biocompatible obturation materials, and sustainable manufacturing practices. Additionally, the report delves into emerging and niche segments like regenerative endodontics, robotics-assisted procedures, eco‑friendly consumables, and cloud-based practice management systems. Further, it assesses competitive dynamics, innovation pipelines, regulatory and compliance developments, and investment patterns, providing decision-makers with a holistic view of current state, potential growth levers, and strategic threats across the global Endodontics market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1682.04 Million |

|

Market Revenue in 2032 |

USD 2392.03 Million |

|

CAGR (2025 - 2032) |

4.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Dentsply Sirona, Coltene, Mani Inc., Ivoclar Vivadent, Danaher, Septodont, VDW GmbH, Brasseler USA, Ultradent Products, Kerr Dental |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |