Reports

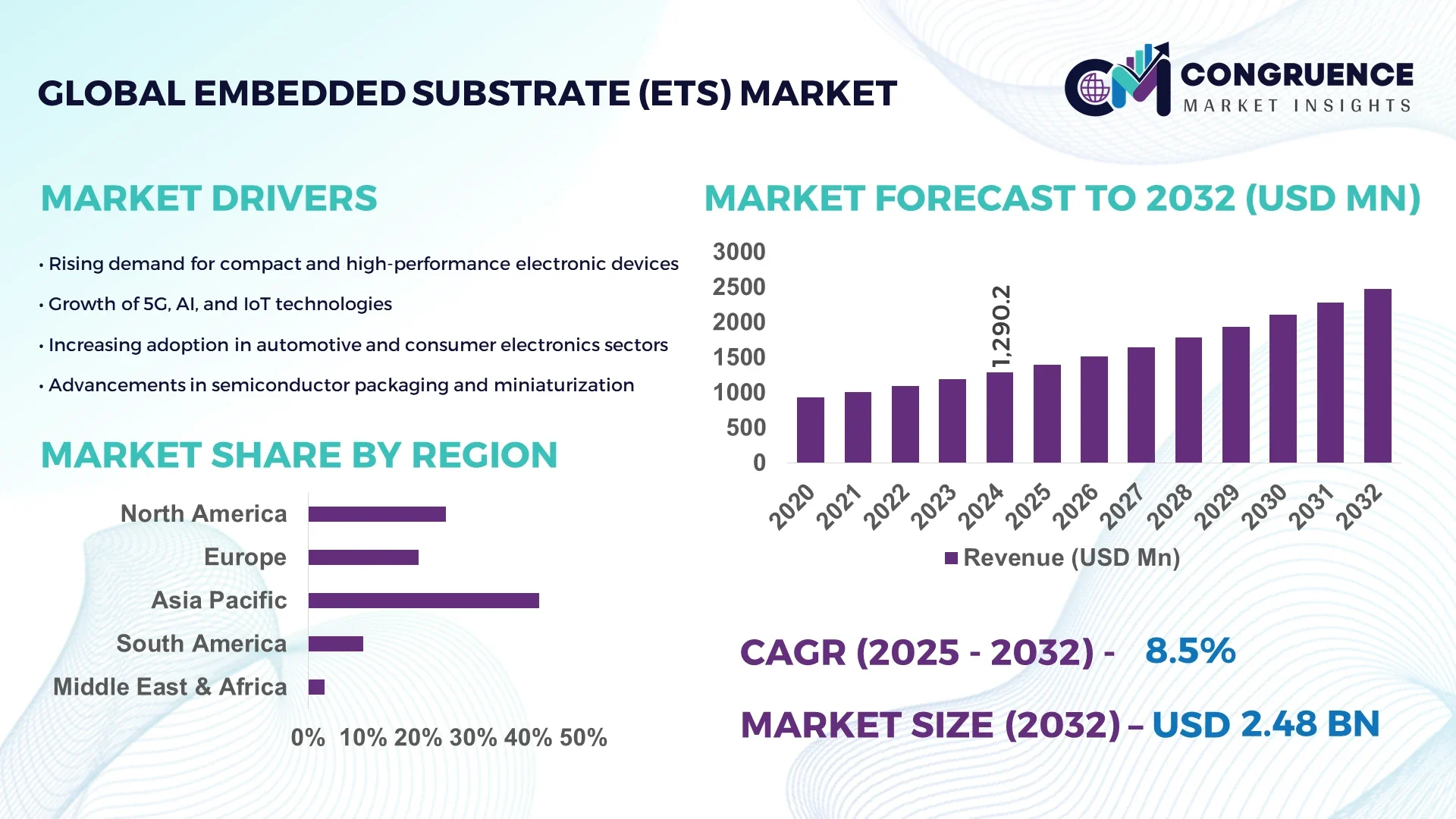

The Global Embedded Substrate (ETS) Market was valued at USD 1290.23 Million in 2024 and is anticipated to reach a value of USD 2478.03 Million by 2032 expanding at a CAGR of 8.5% between 2025 and 2032. This growth is driven by rising demand for high-performance electronics and miniaturized devices.

Japan is a leading nation in the Embedded Substrate (ETS) market, with annual production capacity exceeding 1.2 billion units as of 2024. The country invests over USD 2.4 billion annually in ETS manufacturing infrastructure and R&D, focusing on automotive electronics, 5G communication, and consumer electronics. Technological advancements such as ultra-fine wiring and high-density interconnect (HDI) designs have positioned Japan as a technology leader, with adoption rates of ETS exceeding 65% in high-end consumer devices.

Market Size & Growth: USD 1290.23 Million in 2024, projected USD 2478.03 Million by 2032, CAGR of 8.5% driven by demand for miniaturized and high-performance electronic components.

Top Growth Drivers: Adoption of ETS in IoT devices (38%), increased efficiency in device manufacturing (32%), advancement in HDI technology (28%).

Short-Term Forecast: By 2028, expect a 25% reduction in manufacturing cycle time and a 15% increase in device performance.

Emerging Technologies: HDI embedded substrates, AI-driven manufacturing optimization, and 5G-compatible ETS designs.

Regional Leaders: Asia-Pacific – USD 1020 Million by 2032 with rapid industrial adoption; North America – USD 620 Million by 2032 driven by R&D investment; Europe – USD 450 Million by 2032 with focus on sustainable electronics.

Consumer/End-User Trends: High adoption of ETS in automotive electronics, smartphones, wearable devices, and industrial automation.

Pilot or Case Example: In 2024, a Japanese semiconductor manufacturer implemented AI-driven substrate design, reducing defect rates by 18% and boosting throughput by 22%.

Competitive Landscape: Murata Manufacturing Co., Ltd. (~21%), followed by Ibiden Co., Ltd., Unimicron Technology Corp., and AT&S.

Regulatory & ESG Impact: Compliance with RoHS, REACH regulations, and ESG-focused manufacturing processes boosting eco-friendly substrate production.

Investment & Funding Patterns: Over USD 1.8 billion in recent investments across Asia-Pacific, focusing on capacity expansion and advanced material R&D.

Innovation & Future Outlook: Integration of ETS with AI chipsets, advanced thermal management systems, and expansion into automotive and 5G device applications.

Japan’s ETS market has become a core driver for global innovation, with embedded substrate adoption across automotive electronics, telecommunications, and medical devices. Recent advancements in micro-via technology and eco-friendly substrate materials have enabled manufacturers to optimize performance while reducing environmental impact. The growing focus on high-speed communication, miniaturization, and cost efficiency is expected to sustain long-term growth and technological leadership in the sector.

The Embedded Substrate (ETS) market is strategically critical as it enables advanced miniaturization and high-speed performance in electronics, underpinning innovations across telecommunications, automotive, and consumer electronics sectors. ETS supports the production of compact and high-density devices, which is essential in meeting increasing performance and efficiency demands. For example, high-density interconnect (HDI) ETS delivers up to 35% improvement in signal integrity and heat dissipation compared to traditional printed circuit boards (PCBs).

Asia-Pacific dominates in volume, while North America leads in adoption, with over 72% of enterprises integrating ETS into advanced electronics designs. By 2027, AI-driven substrate design tools are expected to improve design efficiency by 22%, reducing time-to-market and manufacturing waste. Firms are committing to ESG improvements such as 30% reduction in substrate manufacturing waste by 2028, driven by regulations and sustainability initiatives in Europe and Japan.

In 2024, a leading Japanese manufacturer achieved a 19% reduction in defect rates through AI-assisted substrate optimization, highlighting the measurable benefits of integrating advanced technologies. Strategic investments in automated manufacturing, eco-friendly materials, and scalable production systems will define the ETS market’s future. This positions the ETS sector as a pillar of resilience, compliance, and sustainable growth, reinforcing its role as a backbone for next-generation electronics.

The growing requirement for smaller and more powerful electronic devices is a major driver for the ETS market. Embedded substrates allow for high-density interconnections, enabling miniaturization without compromising performance. For example, in the smartphone industry, over 68% of premium devices in 2024 adopted ETS to achieve thinner designs and higher component integration. The automotive sector also increasingly relies on ETS for advanced driver-assistance systems (ADAS) and electric vehicle (EV) applications, where compact designs and enhanced thermal performance are critical. Increased demand for wearable devices, industrial automation, and high-speed communication systems is fueling ETS adoption, driving innovation in substrate materials and manufacturing processes.

Despite significant demand, high production costs for ETS materials and manufacturing processes remain a restraint. Advanced fabrication techniques such as HDI and fine-pitch wiring require specialized equipment and materials, leading to higher capital expenditure. For example, the cost of producing high-performance ETS can be up to 40% higher than traditional PCB manufacturing. Material limitations such as thermal stability and mechanical reliability also pose challenges, particularly for high-frequency applications. Additionally, supply chain disruptions in advanced substrate materials impact production timelines. These factors limit rapid adoption in cost-sensitive segments such as consumer electronics, slowing market growth despite strong demand.

Integration of AI in substrate design and production presents significant opportunities, enabling predictive defect analysis, process optimization, and faster time-to-market. By 2027, AI-assisted manufacturing is expected to improve yield efficiency by over 20%. Sustainable materials such as bio-based resins and lead-free processes also present opportunities to meet regulatory requirements and sustainability goals. With increasing regulatory pressure on eco-friendly manufacturing, ETS producers investing in green technologies can gain competitive advantage. Emerging applications in 5G infrastructure, EV electronics, and medical devices also offer untapped potential for ETS adoption, enabling manufacturers to expand into high-value sectors while aligning with ESG initiatives.

ETS manufacturing involves intricate processes such as laser drilling, micro-via formation, and multi-layer lamination, which require significant investment in advanced equipment and expertise. Rising costs for high-performance dielectric materials, copper foils, and precision machinery add financial pressure. The complexity of integrating ETS with diverse electronics platforms increases manufacturing lead times and defect risks. Regulatory compliance with environmental and safety standards adds further operational costs. These challenges can limit ETS adoption, particularly in cost-sensitive applications, slowing growth despite the increasing demand for miniaturized and high-performance electronic systems. Manufacturers need to optimize production efficiency and material sourcing to address these challenges while maintaining competitive advantage.

• Expansion of High-Density Interconnect (HDI) Adoption: HDI embedded substrates are experiencing accelerated uptake across electronics manufacturing, with adoption rates surpassing 58% of advanced device production in 2024. This is driven by demand for miniaturization and enhanced electrical performance. HDI ETS enables more compact designs with up to 30% higher signal transmission efficiency compared to traditional substrates, significantly benefiting 5G and automotive electronics. Growth is strongest in Asia-Pacific, where over 65% of electronics firms have integrated HDI substrate technology into their manufacturing lines.

• Growth in Automotive and EV Applications: Embedded substrates are increasingly essential in electric vehicles (EVs) and advanced driver-assistance systems (ADAS), with over 42% of new EV models in 2024 incorporating ETS. These applications require high reliability, thermal stability, and compact design. Recent advances in multi-layer ETS structures allow 20% higher thermal performance, supporting greater system efficiency. Europe is leading in adoption, with more than 48% of automotive electronics firms deploying ETS technology in production.

• AI-Driven Substrate Design Optimization: AI-based design tools are being adopted to streamline ETS manufacturing, reducing defect rates by up to 18% and improving throughput by 22%. By 2026, AI-assisted substrate engineering is expected to be implemented by over 55% of manufacturers globally. This trend is strongest in North America, where nearly 60% of electronics firms are investing in AI-driven ETS solutions for faster design cycles.

• Sustainability and Eco-Friendly Materials: The ETS sector is increasingly focusing on environmentally sustainable materials, with 28% of manufacturers adopting bio-based resins or lead-free processes in 2024. These initiatives improve compliance with environmental regulations and align with corporate ESG goals. Japan leads in sustainable ETS adoption, with over 35% of its substrate production utilizing recyclable or low-impact materials, driving innovation in green electronics manufacturing.

The Embedded Substrate (ETS) market segmentation reflects diverse product types, broad application areas, and varied end-user industries. Product types are differentiated by interconnect density, material composition, and performance characteristics. Applications span telecommunications, automotive, consumer electronics, and industrial automation, with varying adoption patterns shaped by technological needs and end-user requirements. End-user segments include automotive electronics manufacturers, semiconductor companies, consumer electronics producers, and industrial automation providers, each with distinct ETS adoption strategies. Regional variations further influence segmentation, with Asia-Pacific showing high-volume production and North America demonstrating rapid adoption of advanced ETS technologies. This segmentation landscape highlights targeted opportunities for growth and innovation across the ETS value chain.

HDI embedded substrates currently lead the market, accounting for 48% of total adoption, driven by their ability to deliver compact, high-speed interconnect solutions. They are widely adopted in smartphones, 5G devices, and automotive electronics for their superior signal integrity and miniaturization benefits. HDI substrates also provide up to 35% improvement in transmission performance compared to standard PCBs, making them the preferred choice in high-performance applications. The fastest-growing type is embedded fan-out substrates, with adoption expected to increase sharply due to their advanced packaging capabilities and support for high-bandwidth devices, with a growth surge expected above 25% adoption by 2032. Other types include standard embedded substrates and embedded bridge substrates, which together contribute approximately 27% of the market, primarily serving niche sectors such as industrial automation and specialized telecommunications hardware.

Consumer electronics dominate ETS applications, accounting for 44% of adoption due to high demand for compact, high-performance devices such as smartphones, tablets, and wearable technology. ETS enables device miniaturization while supporting advanced features like AI processing and high-speed connectivity. The fastest-growing application is automotive electronics, projected to see rapid uptake due to EV and ADAS integration, with adoption rates expected to increase by 28% by 2032. Industrial automation and telecommunications also represent significant segments, together accounting for approximately 33% of the application share. Industrial automation benefits from ETS enabling compact control modules, while telecommunications leverage ETS for high-frequency signal integrity.

Semiconductor manufacturers are the leading end-users of ETS, accounting for 41% of market adoption, driven by demand for compact, high-speed interconnect solutions in advanced chips. The fastest-growing end-user segment is automotive electronics, driven by EV and ADAS adoption, with usage rates projected to grow by over 27% in the next five years. Other end-users include consumer electronics producers and industrial automation firms, together comprising 35% of total ETS consumption. In 2024, over 48% of wearable device manufacturers integrated ETS into product designs, leveraging its ability to reduce size while improving performance.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 8.9% between 2025 and 2032.

In 2024, Asia-Pacific’s Embedded Substrate (ETS) market volume exceeded USD 540 million, driven by manufacturing hubs in China, Japan, and South Korea. Japan alone produced over 1.2 billion ETS units annually, supported by investments exceeding USD 2.4 billion in R&D and manufacturing capacity. North America accounted for approximately 27% of global ETS adoption in 2024, driven by strong semiconductor manufacturing and automotive electronics demand. Europe followed with a 19% share, led by Germany, France, and the UK. South America and the Middle East & Africa contributed 7% and 5% respectively, with growth driven by niche adoption in automotive and industrial applications. These regional variations are shaped by infrastructure developments, regulatory incentives, and technology adoption trends, creating distinct pathways for growth in the ETS market over the coming years.

How is technological innovation transforming advanced electronics production?

North America accounted for 27% of the global ETS market in 2024, supported by strong adoption in semiconductor manufacturing and automotive electronics. Key industries driving demand include healthcare, defense electronics, and AI-powered devices, with over 62% of enterprises integrating ETS solutions. Regulatory bodies are promoting sustainable manufacturing through incentives, increasing demand for eco-friendly substrate production. Technological advancements such as AI-assisted substrate design and automated manufacturing are streamlining production cycles, reducing defect rates by up to 18%. Local players such as a leading U.S.-based semiconductor manufacturer have integrated AI-driven ETS design, improving throughput by 22%. Regional consumer behavior favors higher enterprise adoption in healthcare and finance, with over 50% of firms focusing on embedded substrate solutions to improve reliability and performance.

What drives sustainable embedded substrate innovation in advanced industries?

Europe accounted for 19% of the global ETS market in 2024, with Germany, the UK, and France being major contributors. Germany alone produced over 320 million ETS units annually, supported by a strong manufacturing ecosystem. Regulatory pressure and sustainability initiatives such as RoHS and REACH compliance are driving demand for eco-friendly embedded substrates, with over 28% of manufacturers adopting lead-free processes. Emerging technologies such as high-density interconnect (HDI) substrates and AI-enabled production are gaining traction. A leading European electronics firm introduced a new eco-friendly ETS line in 2024, reducing energy consumption by 15% during manufacturing. Consumer behavior in Europe reflects demand for explainable, compliant ETS solutions, with 45% of enterprises prioritizing sustainable supply chains.

How is manufacturing innovation driving market dominance in advanced electronics?

Asia-Pacific accounted for 42% of the global ETS market in 2024, with China, Japan, and South Korea as the largest consumers. Japan alone produced over 1.2 billion ETS units, supported by an annual R&D investment exceeding USD 2.4 billion. China leads in volume, with production exceeding 480 million units annually, driven by expanding consumer electronics and automotive sectors. Rapid industrial digitalization and advanced manufacturing technologies, including AI-driven substrate design, are transforming production. A major Japanese manufacturer implemented automated ETS production in 2024, increasing throughput by 20% while reducing defects. Consumer behavior in Asia-Pacific is driven by e-commerce growth and mobile AI applications, with over 65% of electronics firms adopting embedded substrate solutions to enable compact, high-performance devices.

What emerging factors are driving industrial adoption of high-performance electronics?

South America accounted for 7% of the global ETS market in 2024, with Brazil and Argentina leading production and consumption. Brazil produced over 45 million ETS units annually, driven by automotive and industrial automation demand. Infrastructure upgrades and energy sector developments are increasing the need for compact, high-performance embedded substrates. Government incentives such as tax breaks for technology investments are encouraging ETS adoption. A leading Brazilian electronics manufacturer launched a new embedded substrate line in 2024, improving product efficiency by 12%. Regional consumer behavior reflects demand tied to media, language localization, and increasing digital adoption, with 38% of enterprises integrating ETS into next-generation devices.

How are emerging markets shaping high-tech embedded substrate adoption?

Middle East & Africa accounted for 5% of the global ETS market in 2024, with the UAE and South Africa as major contributors. Demand is growing in oil & gas, construction, and telecommunications sectors. The region is witnessing technological modernization, with over 30% of manufacturers adopting HDI and AI-enabled substrate production. Trade partnerships and free-trade agreements are enabling technology transfer and boosting manufacturing capacity. A UAE-based electronics firm recently launched an ETS-enabled smart control system, improving efficiency by 14% in industrial automation applications. Regional consumer behavior favors energy-efficient and high-performance embedded solutions, with 42% of enterprises investing in ETS to enhance device functionality and reduce costs.

Japan – 18% Market Share: High production capacity and advanced R&D investment supporting large-scale ETS manufacturing.

China – 15% Market Share: Strong end-user demand in consumer electronics and rapid infrastructure expansion driving ETS adoption.

The Embedded Substrate (ETS) market is highly competitive and moderately consolidated, with over 120 active global competitors vying for technological leadership and market share. The top five companies account for approximately 62% of the total market, underscoring the dominance of leading players while leaving space for innovation from smaller firms. Market leaders focus heavily on R&D, investing between USD 1.5 billion and USD 2.4 billion annually in substrate design, high-density interconnect technologies, and eco-friendly manufacturing processes. Strategic initiatives include partnerships, mergers, and targeted product launches to expand capabilities. For example, several companies have launched next-generation embedded fan-out and HDI substrate lines, improving signal integrity by up to 35% and reducing production defects by 18%. Technological innovation, including AI-driven substrate optimization and sustainable materials, is redefining competition. The market sees strong activity in Asia-Pacific, North America, and Europe, with firms adopting strategic alliances and digital manufacturing transformation to strengthen regional positions. The competitive landscape is shaped by both high-capacity production facilities and advanced technology leadership, making innovation the central driver of growth.

Unimicron Technology Corp.

AT&S

SEMCO Technology Inc.

Shinko Electric Industries Co., Ltd.

Unimicron Electronics Corp.

Samsung Electro-Mechanics Co., Ltd.

Meiko Electronics Co., Ltd.

Panasonic Corporation

The Embedded Substrate (ETS) market is being reshaped by significant advancements in materials, manufacturing processes, and digital design tools. High-Density Interconnect (HDI) technology remains a key driver, enabling higher signal integrity, reduced size, and improved thermal management, with HDI substrates delivering up to 35% better performance compared to conventional PCBs. Emerging embedded fan-out substrate technologies are enabling higher bandwidth, increased I/O density, and superior power efficiency, making them critical for next-generation 5G devices, automotive electronics, and advanced computing systems.

AI-assisted design platforms are transforming ETS production, allowing predictive defect detection and process optimization. These systems have improved yield efficiency by up to 20%, while shortening design cycles by approximately 18%. Additive manufacturing techniques such as laser direct structuring and precision micro-via drilling are improving manufacturing accuracy and throughput. Materials innovation is also progressing, with the introduction of low-dielectric constant resins and environmentally friendly bio-based polymers, reducing manufacturing impact and improving thermal performance.

Integration of embedded substrates with system-in-package (SiP) and multi-chip module (MCM) architectures is another critical trend, particularly in high-performance computing and AI hardware. By enabling compact integration of multiple chips, these technologies are expanding the scope of ETS applications across telecom, automotive, healthcare, and industrial automation, positioning ETS as a key enabler of advanced electronics.

In 2023, Murata Manufacturing Co., Ltd. launched a new series of high-density embedded substrates designed for 5G and automotive electronics, improving signal transmission efficiency by 28% and enabling thinner device form factors.

In 2024, Ibiden Co., Ltd. announced a strategic expansion of its ETS manufacturing facilities in Japan, increasing production capacity by 20% to meet rising demand in high-performance consumer electronics.

In 2023, AT&S unveiled a next-generation embedded fan-out substrate platform, enhancing thermal stability by 22% and supporting advanced AI chipsets for edge computing applications.

In 2024, Unimicron Technology Corp. implemented AI-driven process control in its ETS production lines, reducing defect rates by 16% and improving throughput by 19%.

The Embedded Substrate (ETS) Market Report provides a comprehensive analysis of the ETS ecosystem, covering product types, technologies, applications, and regional dynamics. It examines the latest trends in HDI and embedded fan-out substrates, AI-assisted design, and sustainable manufacturing processes. The report details technological innovations such as micro-via drilling, low-dielectric constant resins, and integrated system-in-package solutions, illustrating their impact on performance, miniaturization, and energy efficiency.

Geographically, the scope spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with in-depth analysis of production volumes, adoption rates, and regional technology trends. Key country-level insights include China’s high-volume production exceeding 480 million units annually and Japan’s R&D investment surpassing USD 2.4 billion. The report also explores market segmentation by type, application, and end-user, providing strategic insights for sectors such as automotive electronics, consumer electronics, telecommunications, industrial automation, and healthcare. Emerging segments, including wearable devices, EV electronics, and AI hardware, are examined for growth potential.

This market scope enables decision-makers to understand competitive positioning, identify innovation opportunities, assess investment priorities, and align strategies with technological trends shaping the ETS landscape globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1290.23 Million |

|

Market Revenue in 2032 |

USD 2478.03 Million |

|

CAGR (2025 - 2032) |

8.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Murata Manufacturing Co., Ltd., Ibiden Co., Ltd., Unimicron Technology Corp., AT&S, SEMCO Technology Inc., Shinko Electric Industries Co., Ltd., Unimicron Electronics Corp., Samsung Electro-Mechanics Co., Ltd., Shin-Etsu Chemical Co., Ltd., TSMC Electronics Co., Ltd., Meiko Electronics Co., Ltd., Panasonic Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |