Reports

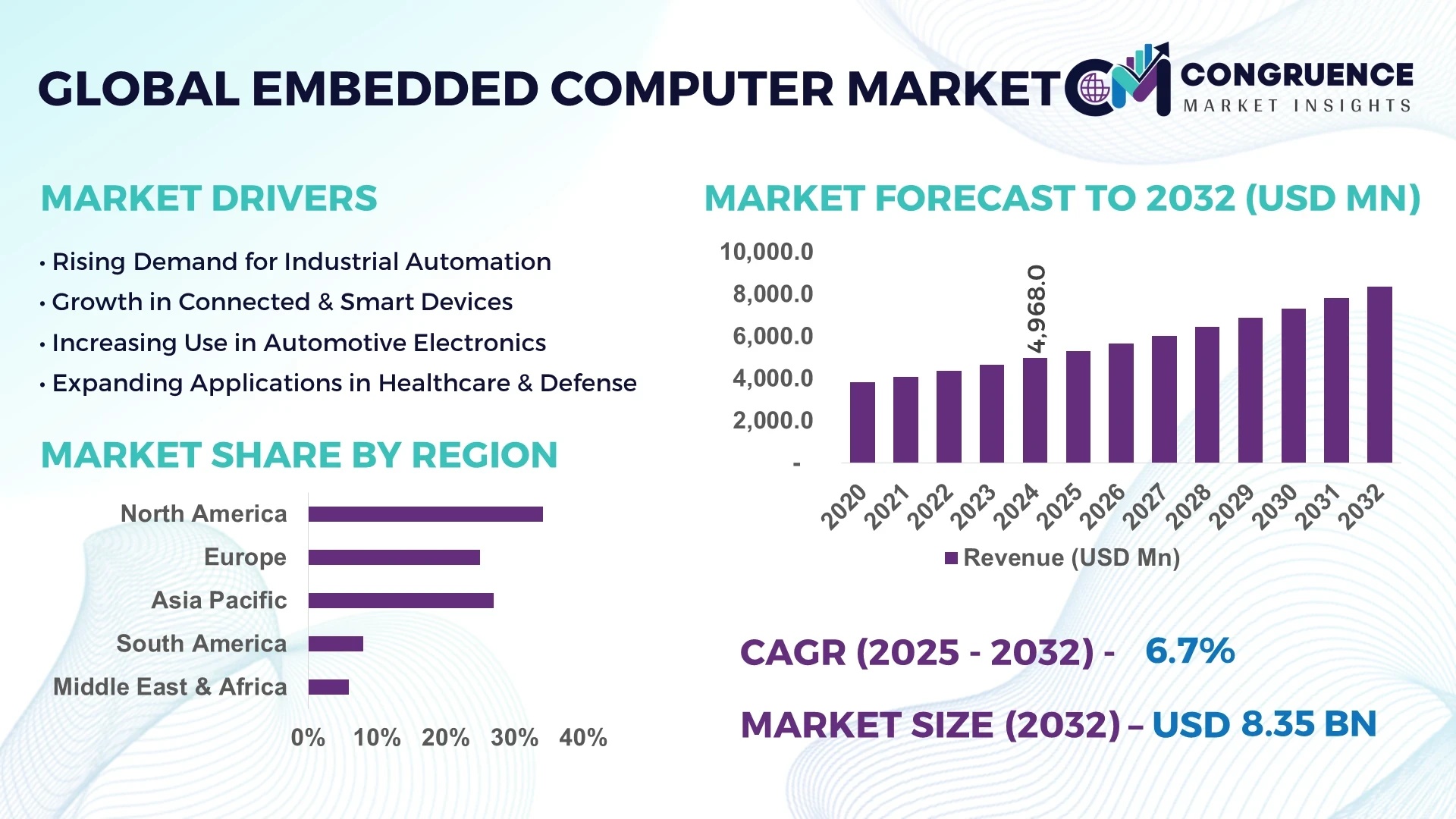

The Global Embedded Computer Market was valued at USD 4,968.0 Million in 2024 and is anticipated to reach a value of USD 8,321.4 Million by 2032 expanding at a CAGR of 6.66% between 2025 and 2032.

The United States underpins production capacity with substantial domestic manufacturing facilities and sizeable R&D investments in embedded computing technologies. Key industry applications span aerospace, industrial automation, automotive systems, and medical devices. Technological advancements include real‑time processing modules, AI‑enabled SoC platforms, and ruggedized edge‑computing units engineered for harsh environments.

Across the Embedded Computer Market, sectors such as industrial automation, automotive electronics, and healthcare contribute significantly to demand. Industrial automation drives adoption of embedded systems in smart factories and predictive maintenance applications. The automotive vertical relies on embedded computing for ADAS, infotainment, and in‑vehicle networking. Healthcare deploys embedded modules in imaging, patient monitoring, and portable medical equipment. Product innovation includes energy‑efficient microcontrollers, embedded vision modules, and modular AI‑accelerated edge computing platforms. Regulatory and economic drivers include stringent safety standards in automotive and healthcare, energy‑efficiency mandates, and infrastructure digitalization policies. Consumption patterns show high demand in North America and Europe, while Asia‑Pacific is increasingly investing in embedded electronics across manufacturing and smart city sectors. Emerging trends include convergence of embedded computing with 5G connectivity, low‑power AI inference, and open‑source real‑time operating systems designed for rapid deployment and scalability.

The Embedded Computer Market is experiencing transformative shifts driven by artificial intelligence integration within edge and embedded platforms. AI functionalities embedded in computing modules are enabling real-time inferencing, predictive analytics, and adaptive control that significantly reduce system latency and enhance operational efficiency. For example, AI-enabled embedded controllers in industrial automation can execute inference tasks within milliseconds, accelerating anomaly detection and production uptime.

Within the Embedded Computer Market, edge AI capabilities allow devices to locally process sensor data—such as vision, motion, or environmental inputs—without constant cloud reliance, reducing data transmission overhead and improving system responsiveness. Deployment of AI accelerators in embedded modules has increased throughput by over 50 percent in tasks such as image recognition and sensor fusion in autonomous systems and robotics. Developers benefit from streamlined AI model deployment on embedded platforms with support for standardized ML frameworks, reducing integration time and increasing lifecycle stability.

Operational performance improvements include dynamic power management driven by machine learning algorithms, which adapt system power usage based on workload, delivering up to 30 percent reduction in energy consumption. Real-time analytics in the Embedded Computer Market also streamline predictive maintenance by flagging abnormal behavior before failure in manufacturing machinery. Additionally, AI‑empowered embedded platforms support multilingual voice processing, local language recognition, and customization for industrial IoT, enhancing usability and localization.

Decision-makers prioritizing system reliability and speed are increasingly selecting AI‑integrated embedded computing solutions. The Embedded Computer Market benefits from vendors offering embedded modules featuring AI cores, neural processing units (NPUs), and sensor‑fusion capabilities, positioning such devices as essential in robotics, healthcare imaging, and automotive safety systems.

“In February 2024, AMD launched its Embedded+ architecture combining Ryzen Embedded processors with Versal adaptive SoCs, enabling edge AI inferencing, sensor fusion, and control functions on a unified board, reducing integration time for ODM partners.”

The Embedded Computer Market Dynamics reflect a convergence of industrial automation, AI deployment, and digital transformation across key verticals. Demand is driven by the shift to real-time edge computing in sectors like automotive, healthcare, and manufacturing. The proliferation of IoT has increased the need for rugged, low-power embedded modules capable of local inference and control. Regulatory mandates over safety, energy efficiency, and cybersecurity are influencing design requirements, particularly in regulated industries. Regional adoption patterns show mature markets in North America and Europe, while Asia‑Pacific surges due to mass manufacturing, smart infrastructure investments, and rising engineering capability. Combined, these dynamics underpin the increasing integration of embedded modules into broader system architectures, supporting scalability, localized intelligence, and system resiliency.

Rapid deployment of automation and Industrial IoT is fueling the Embedded Computer Market. Manufacturing plants leverage embedded controllers to support predictive maintenance, robotics, and machine vision operations. Embedded computing units process data locally from connected sensors, reducing latency and network dependency. Industrial protocols like OPC UA and MQTT are increasingly supported. Factories adopting smart automation can see uptime improvements above 10 percent. Governments in major markets offer automation grants that include funding for embedded hardware in smart manufacturing initiatives, further accelerating adoption.

Designing embedded systems for edge environments remains complex, especially when integrating low-power processors, real-time operating systems, connectivity modules, and optional AI accelerators. Component selection must balance thermal constraints, lifecycle length, and certification requirements. Development cycles in regulated sectors like automotive or medical are lengthy due to safety compliance testing. Incompatible hardware‑software interfaces and lack of standardized platforms increase engineering costs and extend time to deployment, hindering adoption among small and medium‑sized original equipment manufacturers (OEMs).

A growing opportunity lies in deploying specialized embedded AI hardware within verticals such as robotics, smart retail kiosks, and autonomous vehicles. Demand is rising for compact modules featuring on‑board neural accelerators, vision processing units, and low-latency inference engines. Vendors offering modular edge boards enable rapid prototype-to-production transitions. The embedded computer market can benefit from integration with AI frameworks enabling plug‑and‑play deployment. Energy harvesting and ultra‑low power SoCs designed for battery-operated systems further open new applications in remote or mobile environments.

The Embedded Computer Market continues to face challenges from semiconductor supply fluctuations, longer lead times, and rising component costs. Global shortages in microcontrollers and industrial-grade processors impact project delivery timelines. Many systems require components with lifecycle assurances spanning five to ten years—a requirement that conflicts with rapid processor obsolescence cycles. Fluctuations in raw material availability and geopolitical restrictions on technology exports further complicate supplier selection and procurement planning. These factors raise project risk and hinder long-term embedded system deployment strategies.

Surge in AI-Accelerated Edge Modules: Demand is growing for embedded boards equipped with specialized AI cores and neural processing units, facilitating local inferencing in robotics, industrial vision, and smart appliances. Adoption rates for embedded AI modules increased by over 40% in robotics projects in 2024, driven by latency-sensitive edge use cases.

Adoption of Modular Embedded Platforms for OEM Flexibility: OEM developers increasingly deploy modular, plug-and-play embedded boards to accelerate product development. Use of standardized form factors and carrier boards has reduced integration time by up to 25%, particularly in industrial and medical applications requiring fast certification cycles.

Embedded Vision Integration in Machine Inspection: Embedded vision systems—combining cameras, processors, and inference algorithms—are being widely adopted in automotive and industrial inspection. Deployment of embedded vision units is increasing at over 30% annually in smart factory environments to ensure defect detection and quality control at line speed.

Growth in Energy-Efficient Low-Power Embedded Units: Embedded modules featuring energy-saving microcontrollers and power-optimized designs are gaining traction in battery-powered healthcare devices and remote monitoring. Efficiency improvements of over 20% enable longer deployment lifecycles in portable medical platforms and field IoT nodes.

The Embedded Computer Market demonstrates a multifaceted segmentation structure defined by product type, application, and end-user category. Each segment plays a critical role in shaping demand patterns and driving technology adoption across global and regional markets. Product-wise segmentation reveals strong traction for both board-level and system-level embedded computers, with embedded boards gaining preference due to their modularity and compatibility across multiple platforms. Application-based segmentation highlights industrial automation, automotive systems, and medical equipment as major domains where embedded computers play essential roles in enabling real-time processing and device functionality. End-user segmentation spans diverse industries such as manufacturing, healthcare, defense, energy, and transportation, with specific usage patterns reflecting industry-specific regulatory, operational, and technological needs. The increasing demand for smart, connected, and autonomous systems across verticals continues to expand the addressable market for embedded computing solutions.

Embedded Computers are primarily segmented into Single Board Computers (SBCs), Systems on Module (SoM), Box PCs, Industrial Rackmount PCs, and Custom Embedded Systems. Among these, Single Board Computers (SBCs) hold the leading position due to their compact design, cost-effectiveness, and compatibility with diverse industrial and IoT applications. Their plug-and-play configuration, broad OS support, and growing ecosystem for edge AI development drive widespread deployment in automation and medical devices.

Systems on Module (SoM) represent the fastest-growing type, propelled by demand for scalable, power-efficient processing in constrained environments such as wearables, drones, and smart medical tools. SoMs allow developers to accelerate time-to-market while maintaining high levels of customization and integration flexibility. Their low footprint and modularity make them ideal for next-generation embedded AI and sensor fusion tasks.

Box PCs are widely adopted in rugged applications such as transport and manufacturing control systems. Industrial Rackmount PCs cater to centralized industrial control rooms and are prevalent in defense and energy sectors. Custom Embedded Systems serve niche applications requiring specialized interfaces and extreme environmental tolerance, especially in aerospace and maritime use cases.

Embedded Computers are widely utilized across Industrial Automation, Medical Devices, Automotive Electronics, Telecommunications, Consumer Electronics, and Aerospace & Defense. Among these, Industrial Automation leads the market in application scope. Embedded modules are integral to programmable logic controllers (PLCs), robotic systems, and machine vision setups—enabling precision, remote monitoring, and predictive analytics in production environments.

The Medical Devices segment is the fastest-growing application. Increasing reliance on real-time data processing and remote diagnostics has elevated the demand for embedded computing in imaging systems, portable diagnostics, and patient monitoring equipment. This growth is further reinforced by global healthcare digitization efforts and stringent safety standards that embedded systems are equipped to meet.

Automotive Electronics continue to be a crucial application area, particularly with the rise in demand for ADAS, infotainment, and EV battery management systems. In Telecommunications, embedded units facilitate edge networking, while Aerospace & Defense applications require rugged and mission-critical processing, emphasizing system reliability and environmental endurance.

Key end-user segments in the Embedded Computer Market include Manufacturing & Industrial, Healthcare, Automotive, Energy & Utilities, Defense & Aerospace, and Transportation & Logistics. The Manufacturing & Industrial sector holds the leading position, driven by the surge in smart factory initiatives, robotic automation, and demand for real-time process control. Embedded modules enable precision machining, predictive maintenance, and machine-to-machine communication vital for Industry 4.0 environments.

The Healthcare sector stands as the fastest-growing end-user. Embedded computing plays a pivotal role in portable imaging, patient telemetry, and diagnostic devices. Regulatory compliance, growing digital health adoption, and the miniaturization of medical technology contribute to this momentum.

The Automotive sector remains a significant contributor, with embedded systems powering next-gen vehicle functionality and safety systems. Defense & Aerospace end-users demand high-reliability embedded platforms for mission-critical tasks. Energy & Utilities integrate embedded computers for grid control and renewable energy management, while Transportation & Logistics use embedded modules in fleet management and cargo tracking systems for efficiency and safety.

North America accounted for the largest market share at 34.1% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.95% between 2025 and 2032.

This regional disparity highlights the mature demand base in developed economies versus the rapidly growing industrialization and digital infrastructure in emerging markets. North America's leadership is underpinned by technological dominance, robust industrial automation infrastructure, and advanced healthcare and defense sectors. Meanwhile, Asia-Pacific’s projected acceleration is driven by massive investments in smart manufacturing, government-backed digitization programs, and the proliferation of connected devices. Europe remains a steady contributor, particularly due to sustainability and regulatory compliance across embedded electronics. Other regions such as South America and the Middle East & Africa are gaining traction with targeted adoption in energy, transportation, and construction domains.

North America held 34.1% of the Embedded Computer Market in 2024, driven primarily by high demand across manufacturing, defense, and healthcare sectors. The U.S. and Canada are prominent markets, with advanced industrial automation and defense modernization programs fueling embedded system deployment. Government incentives supporting smart manufacturing and AI-driven infrastructure improvements continue to attract significant investments. Regulatory frameworks, including cybersecurity compliance standards in medical and defense sectors, further reinforce embedded computing adoption. The region also benefits from strong digital transformation momentum, with AI at the edge, IoT ecosystems, and machine learning applications pushing the boundaries of operational efficiency and system integration.

Europe maintains a strong position in the Embedded Computer Market with 28.3% market share in 2024, supported by Germany, the UK, and France as top contributors. Germany’s leadership in industrial engineering and robotics complements embedded computing demands in manufacturing. The UK’s healthcare and telecommunication upgrades and France’s transportation infrastructure enhancements are further strengthening market expansion. European regulatory authorities are enforcing environmental and safety compliance, pushing industries to adopt energy-efficient, compact embedded solutions. Additionally, Europe’s strong focus on Industry 5.0 initiatives and digital sovereignty is accelerating the deployment of AI-integrated embedded platforms and promoting supply chain resilience.

Asia-Pacific ranks as the fastest-growing region in the Embedded Computer Market, with China, Japan, South Korea, and India leading consumption volumes. China dominates in embedded system manufacturing and export, driven by its expanding industrial automation and electric vehicle sectors. Japan's precision electronics and robotics industries, coupled with South Korea’s smart city developments and India’s push for semiconductor self-reliance, collectively drive growth. Rapid infrastructure upgrades, widespread adoption of IoT, and innovation hubs such as Shenzhen and Bengaluru are propelling demand for customizable and compact embedded computing systems. Moreover, rising regional investments in 5G and AI chip design are creating a favorable ecosystem for embedded technology advancement.

South America holds a growing yet niche share of the Embedded Computer Market, with Brazil and Argentina representing the key contributors. Brazil’s national efforts to digitalize infrastructure, logistics, and healthcare are directly supporting demand for embedded platforms. In Argentina, the focus is on automating energy management and upgrading manufacturing systems with smart embedded controllers. Government-backed trade policies and increased investments in data connectivity infrastructure are enabling deeper penetration of embedded computing in utility services. Furthermore, as industries adopt smart meters and grid technologies, embedded system deployments are rising in critical infrastructure operations throughout the region.

The Middle East & Africa Embedded Computer Market is gaining traction as UAE and South Africa emerge as key demand centers. The region is witnessing increasing deployment of embedded systems in oil & gas monitoring, construction automation, and public transport systems. Countries like the UAE are prioritizing smart city frameworks, which depend on reliable and compact embedded modules for data processing and real-time analytics. In South Africa, infrastructure development and power management systems are incorporating rugged embedded devices for localized control and fault detection. Regional governments are also engaging in technology trade partnerships to improve access to intelligent industrial computing platforms.

United States – 24.6% Market Share

Strong end-user demand from defense, healthcare, and manufacturing sectors backed by advanced R&D and digital infrastructure.

China – 19.2% Market Share

High production capacity, expanding consumer electronics and industrial automation base drive large-scale embedded computing integration.

The Embedded Computer Market exhibits a dynamic and competitive landscape with over 80 active global and regional players competing across industrial, medical, automotive, and military domains. The market is moderately fragmented, with several companies holding strong regional or industry-specific dominance. Major players are leveraging strategic partnerships, mergers, and acquisitions to expand their technological footprint and product portfolios. A significant trend shaping competition is the push toward AI-enabled edge computing, where embedded platforms now integrate GPU acceleration, neural processors, and real-time analytics capabilities. Leading vendors are also focused on ruggedization, modularity, and compliance with evolving industry standards to cater to critical applications. Innovation cycles are shortening as companies race to meet demands for low-latency processing, compact form factors, and power efficiency. Firms are increasingly offering vertically integrated solutions, combining hardware, firmware, and connectivity protocols to strengthen brand positioning. Emerging players are gaining traction by focusing on customizable embedded platforms tailored to niche industry needs such as robotics, transportation, and healthcare diagnostics.

Advantech Co., Ltd.

Kontron AG

Avalue Technology Inc.

AAEON Technology Inc.

Eurotech S.p.A.

ADLINK Technology Inc.

Radisys Corporation

Congatec GmbH

Premio Inc.

DFI Inc.

Curtiss-Wright Corporation

Beckhoff Automation GmbH & Co. KG

Artesyn Embedded Technologies

MEN Mikro Elektronik GmbH

Nexcom International Co., Ltd.

Technological innovation is a primary driver in the Embedded Computer Market, with advancements focused on edge computing, AI integration, and real-time data processing. The rise of AI-on-the-edge is transforming embedded systems into intelligent, self-sufficient platforms capable of operating without constant cloud connectivity. This trend is particularly strong in smart manufacturing, autonomous vehicles, and predictive healthcare diagnostics.

The shift to System-on-Module (SoM) and Computer-on-Module (CoM) architectures is enabling scalable, compact solutions ideal for space-constrained industrial applications. These modules are now being developed with multi-core ARM and x86 processors, enhanced with hardware-level security and built-in ML acceleration. The market is also witnessing rapid deployment of PCIe Gen4, DDR5 memory, and NVMe SSDs to meet data-intensive needs.

In industrial automation, embedded platforms are increasingly adopting Time-Sensitive Networking (TSN) and 5G connectivity to ensure deterministic performance in mission-critical environments. Additionally, RISC-V architecture is gaining popularity due to its open-source model and flexibility in custom SoC development. Integration of real-time operating systems (RTOS) and virtualization is further enabling high performance in multi-tasking and safety-certified operations.

Energy efficiency, wide-temperature support, and fanless design remain key focus areas, with innovations in thermal management materials and board design contributing to longer lifecycle and reliability in harsh environments.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In April 2024, Advantech released the UNO-238-V2 series powered by Intel® Core™ i5 processors, designed for AI inference at the edge. The fanless system supports 5G modules and dual M.2 expansion, targeting smart factory and industrial IoT use cases.

In November 2023, Kontron launched its COM-HPC Client Module powered by AMD Ryzen Embedded 7000 Series processors. This high-performance module supports PCIe Gen5 and DDR5 memory for graphics-intensive and computing-heavy industrial applications.

In March 2023, ADLINK partnered with NVIDIA to integrate Jetson Orin platforms into its embedded systems. The collaboration aims to accelerate AI workloads in robotics, smart transportation, and edge medical imaging with improved inference performance.

The Embedded Computer Market Report provides a comprehensive examination of the global market landscape, analyzing trends across hardware architectures, form factors, and integration models. The study encompasses diverse product segments, including Single Board Computers (SBCs), System-on-Modules (SoMs), Rugged Embedded PCs, and Panel PCs, used in industrial, automotive, healthcare, and aerospace applications.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, evaluating country-level dynamics, technological readiness, and regional industrial trends. Application-wise, it highlights usage in industrial automation, medical devices, transportation systems, energy management, telecommunications, and smart retail sectors.

The report also evaluates technological domains such as AI/ML integration, real-time control systems, IoT enablement, and 5G readiness, addressing current capabilities and anticipated developments. It includes qualitative and quantitative assessments of end-user industries including OEMs, government agencies, research institutions, and systems integrators.

Additionally, the scope covers analysis of supply chain disruptions, regulatory standards, environmental compliance, and sustainability trends affecting the embedded ecosystem. By profiling both established players and emerging innovators, the report offers decision-makers a strategic lens into the market’s future direction and competitive structure.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 4,968.0 Million |

| Market Revenue (2033) | USD 8,321.4 Million |

| CAGR (2025–2033) | 6.66% |

| Base Year | 2024 |

| Forecast Period | 2025–2033 |

| Historic Period | 2019–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Technological Insights, Segment Analysis, Regional and Country‑Wise Analysis, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Advantech Co., Ltd., Kontron AG, Avalue Technology Inc., AAEON Technology Inc., Eurotech S.p.A., ADLINK Technology Inc., Radisys Corporation, Congatec GmbH, Premio Inc., DFI Inc., Curtiss-Wright Corporation, Beckhoff Automation GmbH & Co. KG, Artesyn Embedded Technologies, MEN Mikro Elektronik GmbH, Nexcom International Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |