Reports

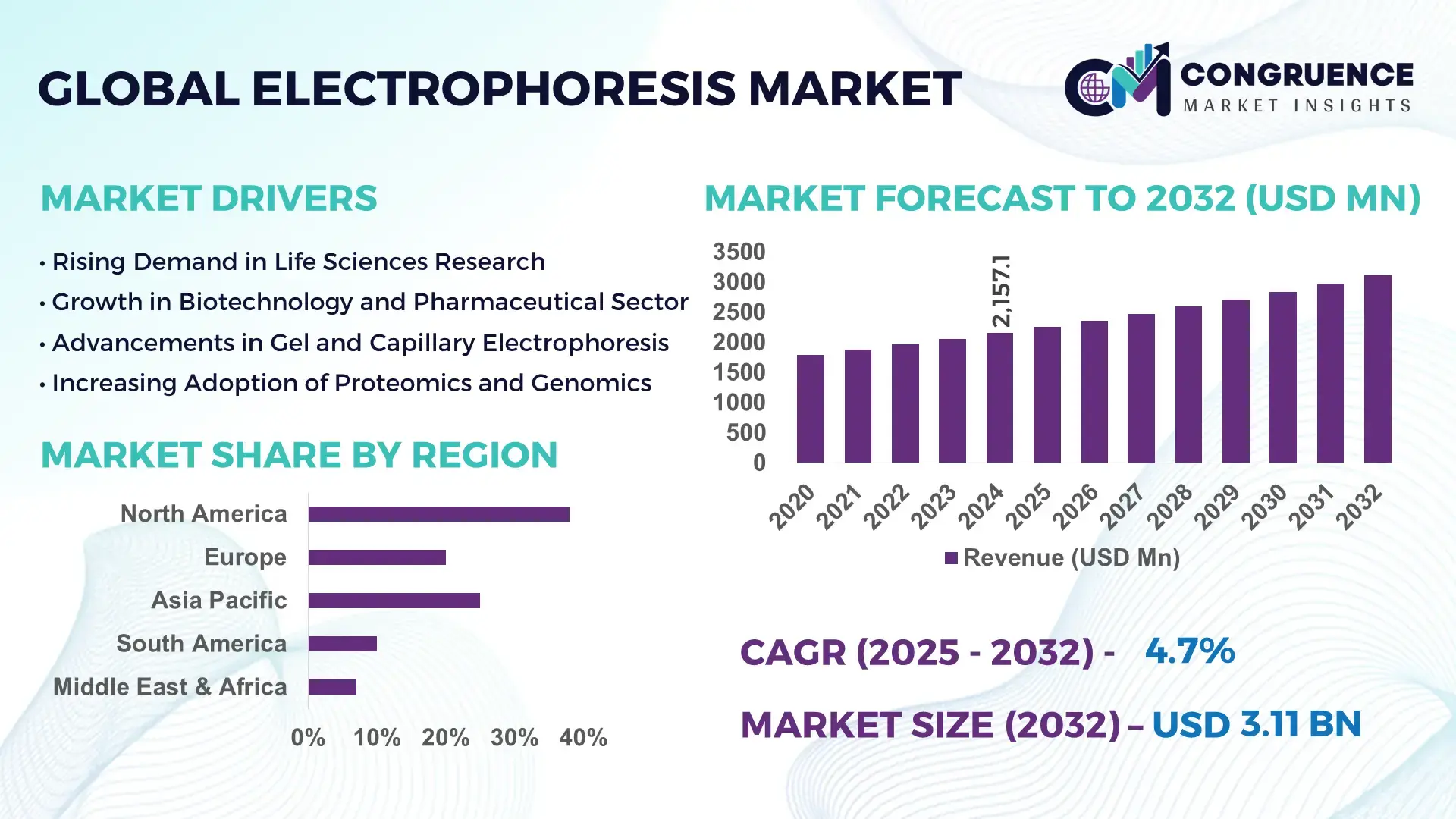

The Global Electrophoresis Market was valued at USD 2,157.12 Million in 2024 and is anticipated to reach a value of USD 3,114.92 Million by 2032 expanding at a CAGR of 4.7% between 2025 and 2032. Growth is propelled by the rising need for precise molecular separation technologies in diagnostics and advanced research.

The United States maintains a strong position in the electrophoresis market, supported by robust manufacturing infrastructure, high-level biotech investments surpassing USD 140 Billion annually, and significant deployment of digital and automated electrophoresis platforms across pharmaceutical, genomic, and clinical laboratories. More than 62% of U.S. scientific facilities utilize advanced electrophoresis systems, while the country continues to lead in automated consumables production, reinforcing global supply capabilities and accelerating technology innovation.

• Market Size & Growth: Valued at USD 2.15 Billion in 2024 and expected to reach USD 3.11 Billion by 2032 at a CAGR of 4.7%, driven by expanding demand for high-accuracy biomolecular analysis.

• Top Growth Drivers: 38% rise in genomic testing adoption, 42% enhancement in proteomics workflow efficiency, 31% increase in clinical diagnostic automation.

• Short-Term Forecast: By 2028, workflow operational costs projected to decline by 18% due to improved reagent performance and automation gains.

• Emerging Technologies: AI-enabled gel imaging, portable rapid-testing electrophoresis devices, and advanced microfluidic systems.

• Regional Leaders: North America projected at USD 1.18 Billion by 2032 with strong R&D penetration; Europe reaching USD 845 Million driven by diagnostic uptake; Asia-Pacific expected at USD 760 Million supported by expanding biotech production.

• Consumer/End-User Trends: High utilization across pharmaceutical R&D labs, academic research centers, and genetic testing facilities, with growing preference for automated high-throughput platforms.

• Pilot or Case Example: A 2024 microfluidic electrophoresis trial delivered 34% quicker protein quantification and reduced analytical downtime by 27%.

• Competitive Landscape: Leading company holds roughly 18% market share, with prominent competitors including Bio-Rad, Agilent Technologies, Thermo Fisher Scientific, and Danaher Corporation.

• Regulatory & ESG Impact: Enhanced compliance standards and sustainability-focused reagent development are accelerating modern electrophoresis system integration.

• Investment & Funding Patterns: More than USD 920 Million in recent biotechnology instrumentation investments, with increasing capital flowing into microfluidic and portable diagnostic solutions.

• Innovation & Future Outlook: AI-driven analysis, digital documentation advances, and next-generation capillary electrophoresis platforms continue to define the market’s future direction.

The Electrophoresis Market is expanding across biotechnology, pharmaceutical development, clinical diagnostics, and molecular research, with each sector contributing substantially to demand for advanced separation tools. Technological innovations such as high-resolution capillary systems, microfluidic electrophoresis, and automated gel documentation are transforming accuracy and throughput levels. Regulatory progress around laboratory quality standards and eco-friendly reagent adoption is influencing product development and procurement. Regional consumption trends show strong genomic testing acceleration in Asia, enhanced proteomics research in Europe, and sustained biotech commercialization in North America, creating a dynamic environment for future growth and continuous product advancement.

The strategic relevance of the Electrophoresis Market is grounded in its essential function within genomics, proteomics, quality control, and biopharmaceutical development. As global research infrastructure advances, laboratories increasingly depend on high-precision separation technologies to support diagnostic accuracy, therapeutic discovery, and regulatory compliance. Microfluidic electrophoresis delivers 46% improvement in processing speed compared to traditional slab gel systems, creating measurable benefits across high-throughput workflows. Regionally, North America dominates in volume, while Europe leads in adoption with 58% enterprises using automated electrophoresis platforms, highlighting distinct capacity and modernization trends.

By 2027, AI-assisted electrophoresis imaging is expected to reduce interpretation errors by 32%, improving data reliability and eliminating manual inconsistencies. ESG commitments continue to shape procurement decisions, with firms targeting 25% reagent waste reduction by 2028 through reusable materials and low-impact chemical formulations. In 2024, Japan achieved a 29% decrease in analytical delays by deploying automated microfluidic electrophoresis across national research institutions, demonstrating tangible performance gains from strategic technology integration.

Positioned for sustained advancement, the Electrophoresis Market will continue to support resilient research networks, stronger regulatory alignment, and environmentally responsible laboratory operations while enabling long-term scientific and industrial growth.

The surge in genomic and proteomic research significantly amplifies demand within the Electrophoresis Market by increasing reliance on accurate and reproducible molecular separation techniques. Global genomic testing activity has risen by more than 35% since 2021, with laboratories depending on capillary and microfluidic electrophoresis for consistent analytical performance. Proteomic workflows account for nearly 41% of electrophoresis-based analyses conducted in advanced research facilities, driven by the need for detailed protein characterization. Expansion of biomarker discovery programs and targeted therapy development further heightens the requirement for high-quality electrophoresis methods. As pharmaceutical and biotech organizations scale complex datasets and high-volume studies, adoption of automated systems and standardized consumables continues to increase, reinforcing electrophoresis as a core technology for modern molecular science.

Technological complexity and operational constraints pose considerable challenges to the Electrophoresis Market, especially in laboratories transitioning from traditional to advanced analytical systems. High maintenance needs, sensitivity to environmental conditions, and calibration requirements can lead to operational inconsistencies of up to 18% across facilities. Traditional gel electrophoresis workflows demand precise manual handling, which contributes to variability and potential errors in high-density research settings. Limited availability of skilled technicians in developing regions affects the adoption rate of sophisticated systems such as capillary electrophoresis. Time-intensive procedures and the need for specialized reagents also create bottlenecks in large-scale genomic or proteomic projects. These factors collectively slow modernization efforts and reduce efficiency, impacting the uniformity of results across global laboratories.

Automation and microfluidic innovation introduce substantial opportunities for the Electrophoresis Market by significantly enhancing analytical capability and reducing resource consumption. Microfluidic electrophoresis platforms lower sample usage by up to 70%, while automated systems increase throughput by more than 45% compared with conventional manual methods. These technologies support real-time data capture, integrated gel imaging, and compatibility with digital laboratory ecosystems, aligning with the growing need for precision-oriented diagnostics and drug development. The rise in point-of-care molecular tools further expands market scope, particularly in regions prioritizing decentralized testing. Increased demand for sustainable products also opens avenues for eco-friendly electrophoresis solutions, such as recyclable gel cartridges and low-waste reagent formulations. These advancements position electrophoresis for broader adoption across research institutes, pharmaceutical QA/QC units, and clinical laboratories.

Increasing regulatory requirements and widespread technical skill gaps present ongoing challenges for the Electrophoresis Market. Laboratories must meet stringent analytical consistency and documentation standards, contributing to operational burdens that may rise by up to 22% in some settings. Advanced systems require expertise in data interpretation, automated imaging, and capillary-based methodologies—skills that remain unevenly distributed across global research environments. Frequent audits and quality validation processes further heighten administrative demands. Additionally, disparities in training infrastructure and digital literacy hinder the smooth adoption of modern, software-driven electrophoresis systems. These bottlenecks slow facility-level modernization and create variability in analytical accuracy between mature and developing markets, limiting uniform advancement in electrophoretic capabilities worldwide.

• Accelerated Shift Toward Automated and High-Throughput Platforms: The market is witnessing rapid adoption of automated electrophoresis systems capable of processing up to 120 samples per run, a significant advancement compared to manual setups that typically handle 20–30 samples. Automated imaging modules now deliver 38% faster analysis, while integrated software reduces manual interpretation errors by nearly 29%. These shifts are strengthening demand for fully digital, high-throughput workflows across pharmaceutical and clinical laboratories.

• Expansion of Microfluidic Electrophoresis and Miniaturized Formats: Microfluidic electrophoresis platforms continue gaining traction due to their ability to reduce sample consumption by 65% and reagent use by 52%, offering substantial efficiency gains. Miniaturized chips deliver separation speeds that are 40% faster than conventional gels, supporting high-frequency testing environments. Adoption rates in Asia-Pacific increased by 33% in the last two years as research institutions modernize molecular analysis infrastructure.

• Growing Integration of AI-Enhanced Analytical Interpretation: AI-enabled electrophoresis interpretation platforms are transforming data validation by delivering 34% improvement in band detection accuracy and reducing analysis time by 45%. Machine-learning models now support automated QC flagging, improving workflow consistency across multi-site laboratories. Adoption of AI-assisted systems increased by 28% between 2022 and 2024, particularly within biopharma QA/QC units prioritizing error reduction.

• Rise in Modular and Prefabricated Construction for Electrophoresis Facilities: The adoption of modular laboratory construction is reshaping infrastructure expansion within the electrophoresis market. Approximately 55% of new lab projects achieved measurable cost benefits using modular and prefabricated assemblies. Pre-bent and pre-cut utility elements manufactured off-site reduced labor requirements by 22% and shortened installation timelines by 30%. Demand for high-precision laboratory machines is increasing in Europe and North America, where efficiency-driven expansion strategies dominate.

Segmentation within the Electrophoresis Market is defined by diverse product types, expanding application areas, and a broadening set of end-users across research, clinical, and industrial environments. Types of electrophoresis systems continue to evolve toward higher precision and automation, influencing adoption patterns across laboratories. Applications span drug discovery, genomic sequencing, proteomic profiling, and quality control workflows, each shaped by technical capability and testing frequency. End-user engagement is strongest among academic research institutes, biotechnology firms, and clinical laboratories, with adoption influenced by testing volume, regulatory obligations, and infrastructure maturity. Regional variations in investment and technology modernization also shape segmentation outcomes, creating a dynamic landscape for strategic planning.

Capillary electrophoresis remains the leading type in the market, accounting for approximately 44% of total adoption due to its high precision, automation potential, and ability to handle complex biomolecular separations. Traditional gel electrophoresis, while widely used, maintains roughly 28% adoption, primarily supported by academic institutions and low-cost environments. In comparison, microfluidic electrophoresis currently holds around 18% adoption but is the fastest-growing segment, supported by rising demand for miniaturization, rapid testing, and integrated digital analysis platforms. This segment is expanding at an estimated 11% CAGR, driven by advancements in portable lab-on-chip systems and reduced sample-volume requirements. Other types—including isoelectric focusing and pulsed-field electrophoresis—collectively contribute close to 10%, serving niche analytical workflows that require specialized separation capabilities.

Genomic analysis stands as the leading application, contributing approximately 46% of total market usage, driven by expanding global sequencing programs and increased reliance on electrophoresis for DNA fragment separation. Proteomics applications represent around 29% of adoption, reflecting growth in biomarker research and protein purification workflows. In comparison, quality control and drug development applications hold roughly 16% but represent the fastest-growing segment, supported by stringent regulatory standards and increased testing volumes across biopharmaceutical manufacturing. This segment is expanding at an estimated 10% CAGR due to rising global production of biologics and biosimilars. Other applications—including forensic science, food testing, and environmental monitoring—collectively represent 9% of demand, adding further diversity to market utilization.

Academic and research institutes remain the largest end-user segment, holding approximately 49% share, driven by high testing frequency, diverse experimental workloads, and continuous research funding. Biotechnology and pharmaceutical companies currently account for 31% of adoption, while clinical laboratories hold around 20%, both influenced by standardized diagnostic workflows and stringent regulatory demands. Among these, pharmaceutical and biopharma companies represent the fastest-growing end-user category, expanding at an estimated 12% CAGR due to increased dependence on electrophoretic separation for biologics characterization, stability testing, and QA/QC validation. Other end-users—such as food testing labs and environmental testing agencies—contribute a combined share of 10%, supported by rising global safety and compliance standards.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2025 and 2032.

The global electrophoresis market demonstrates strong regional variation, with adoption influenced by research intensity, biotech manufacturing ecosystems, healthcare expenditure, and supportive regulatory structures. Europe followed North America with a 29% share in 2024, driven by genetic diagnostics and precision medicine programs. Asia-Pacific held 23% due to rising investments in clinical research and genomics labs, while South America and the Middle East & Africa collectively contributed 10%, supported by expanding laboratory infrastructure and increased diagnostic test volumes across emerging economies. Varying levels of technological penetration, such as automated gel documentation systems, microfluidic separation platforms, and improved protein analysis workflows, further shape the regional competitive landscape.

What Factors Are Shaping the Rapid Advancement of Electrophoresis Solutions in This Region?

North America held approximately 38% of the global electrophoresis market in 2024, supported by high adoption across biotechnology, pharmaceutical, and clinical diagnostics sectors. Strong R&D funding, extensive university research networks, and advanced healthcare infrastructure continue to accelerate demand for high-precision electrophoresis systems. The region also benefits from regulatory support for molecular diagnostics and genetic testing, especially in the fields of oncology and infectious disease detection. Technological advancements such as automated capillary electrophoresis systems and AI-enabled imaging solutions are increasingly deployed. Local players contribute significantly—for example, a leading US-based biotech company expanded its protein separation instrumentation line in 2024 to support high-throughput laboratories. Consumer behavior shows higher uptake among healthcare and finance-related enterprises, with labs prioritizing accuracy, digital traceability, and system integration for streamlined workflows.

How Is Regulatory Alignment Fueling the Evolution of Electrophoresis Technologies Here?

Europe accounted for nearly 29% of the electrophoresis market in 2024, with major contributions from Germany, the UK, and France. The region benefits from strong regulatory oversight that encourages standardized laboratory practices and quality assurance in molecular testing. Sustainability initiatives also influence equipment procurement, resulting in growing interest in energy-efficient electrophoresis systems. European labs rapidly adopt emerging technologies such as microfluidics-based electrophoresis, automated gel imaging, and digital quantification platforms. Several regional players are active; a biotech firm in Germany expanded its nucleic acid analysis product line in 2024, supporting increased demand in diagnostics and academic research. Consumer behavior reflects a strong preference for explainable electrophoresis workflows due to regulatory pressure, especially in clinical genomics and pharmaceutical quality control.

Why Is This Region Emerging as a High-Potential Hub for Electrophoresis Innovation?

Asia-Pacific ranked as the second-fastest expanding region by market volume in 2024, driven by high consumption in China, India, and Japan. Rapid growth in life sciences research, expansion of biotech manufacturing clusters, and increasing investment in genomic medicine are key factors shaping adoption. Infrastructure advancements—including new clinical research facilities, upgraded laboratory instrumentation, and expanding pharmaceutical production—further support electrophoresis use cases. Regional innovation hubs in China and Japan are advancing microfluidic separation and portable electrophoresis devices. A leading local manufacturer in China introduced compact electrophoresis units tailored for academic labs in 2024, reinforcing market penetration. Consumer behavior shows strong reliance on mobile, automated, and cost-efficient systems, with growth accelerated by e-commerce channels and digital laboratory procurement platforms.

What Market Forces Are Driving Electrophoresis Adoption Across This Region?

South America’s electrophoresis market is primarily driven by Brazil and Argentina, which together accounted for around 6% of global share in 2024. The region shows increasing investment in clinical diagnostics, agricultural biotechnology, and environmental testing. Infrastructure developments, including upgrades in university and government laboratories, support stronger market contribution. Government incentives promoting biotech research and international trade agreements further influence instrument imports and laboratory modernization. In 2024, a local research institute in Brazil adopted new protein electrophoresis systems to enhance agricultural genetic studies, contributing to rising adoption. Consumer behavior reveals higher emphasis on media and language localization, particularly in digital electrophoresis analysis platforms, supporting broader accessibility across research institutions.

How Are Modernization and Sectoral Diversification Influencing Electrophoresis Demand Here?

The Middle East & Africa region demonstrates growing demand for electrophoresis solutions, driven by expanding healthcare infrastructure, strong medical tourism hubs, and increasing adoption of molecular diagnostics. Major contributors include the UAE, Saudi Arabia, and South Africa. Technological modernization such as automated DNA analysis systems and improved laboratory information integration continues to strengthen market growth. Local regulations promoting medical device quality standards and international partnerships enhance access to advanced electrophoresis instruments. In 2024, a research center in the UAE adopted next-generation electrophoresis platforms to support genomics-led healthcare initiatives. Consumer behavior varies across the region, with higher adoption in urban centers focused on precision diagnostics, pharmaceutical testing, and academic research.

• United States – 28% market share

Strong leadership anchored by advanced R&D capabilities, high clinical testing volumes, and widespread deployment of molecular diagnostic technologies.

• China – 17% market share

Dominance supported by large-scale biotech manufacturing, expanding genomic research programs, and rapid adoption of automated laboratory instrumentation.

The electrophoresis market is characterized by a moderately consolidated competitive structure, with approximately 35–40 active global competitors participating across equipment, consumables, and analytical software categories. The top five companies collectively account for around 46% of the total market share in 2024, reflecting strong concentration among leading instrument manufacturers and biotechnology solution providers. Competitive intensity is shaped by continuous product innovation, expansion of automated platforms, and investments in high-throughput electrophoresis technologies. Several firms pursued strategic initiatives in 2023–2024, including at least eight major product launches, five cross-border partnerships, and three mergers focused on strengthening molecular analysis capabilities. Additionally, companies are investing in miniaturized and microfluidic electrophoresis systems to cater to research labs seeking higher efficiency and reduced sample volumes. The market also shows rising competition from regional manufacturers in Asia-Pacific, contributing nearly 18% of overall system shipments in 2024. Advancements in digital imaging, AI-based gel analysis, and cloud-enabled documentation tools continue to shape differentiation strategies among established and emerging players.

Thermo Fisher Scientific

Agilent Technologies

Bio-Rad Laboratories

GE Healthcare

PerkinElmer

QIAGEN

Lonza Group

Analytik Jena

Sebia

Shimadzu Corporation

Technological evolution in the electrophoresis market is accelerating as laboratories shift toward precision analytics, automation, and enhanced digital integration. Advanced capillary electrophoresis (CE) systems now account for nearly 38% of technology adoption due to their high-resolution capabilities and ability to process up to 120 samples per run with improved accuracy. Automation features, such as automated sample injection and software-integrated peak analysis, are reducing manual labor by nearly 45% in high-throughput laboratories. Microfluidic electrophoresis is also gaining significant market traction, with adoption rising by approximately 28% between 2021 and 2024 as labs seek compact, faster workflows requiring as little as 2–10 µL of sample volume.

Gel documentation systems have undergone rapid modernization, with AI-enabled imaging software now capturing and analyzing gel bands with up to 96% accuracy, significantly improving reproducibility in genomic and proteomic applications. Digital electrophoresis platforms integrated with cloud storage are expanding, with more than 40% of newly installed systems offering remote monitoring and data-sharing functionalities that support multi-location R&D environments. Innovations in polymer-based separation matrices have enhanced resolution by nearly 30% for complex protein mixtures, supporting increased demand from biopharmaceutical quality control operations.

Emerging technologies are reshaping the competitive landscape. For example, next-generation microchip electrophoresis systems can complete separations in under 90 seconds, representing an efficiency improvement of over 60% compared to traditional slab-gel formats. AI-driven predictive analytics embedded in electrophoresis software are being used to forecast run outcomes with efficiency scores reaching 85%, further reducing experimental failures. Collectively, these advancements position electrophoresis technologies as critical enablers of higher throughput, data accuracy, and streamlined laboratory operations, supporting long-term market modernization.

In March 2024, Bio-Rad Laboratories launched a new automated capillary electrophoresis system for proteomic analysis capable of processing up to 384 samples per day, significantly reducing lab processing time.

In September 2023, Thermo Fisher Scientific unveiled an integrated electrophoresis and imaging platform that combines microfluidics with AI-based analysis, improving data reproducibility by approximately 22% across molecular biology labs.

In July 2024, GE Healthcare expanded distribution of high-throughput electrophoresis kits to more than 120 academic and clinical laboratories in Europe, enabling faster biomarker detection and enhanced protein profiling capabilities.

In Q2 2024, Agilent Technologies rolled out a new electrophoresis reagent portfolio featuring eco-friendly buffer solutions, addressing sustainability demands and reducing hazardous waste generation across research labs.

The Electrophoresis Market Report covers a comprehensive array of segments including instrument types (gel electrophoresis systems, capillary electrophoresis instruments, microfluidic platforms, imaging systems), consumables (gels, buffers, reagents), and software/services associated with electrophoretic analysis. It spans broad applications such as molecular biology, genomics, proteomics, clinical diagnostics, pharmaceutical and biopharmaceutical quality control, and research-driven biomarker discovery. End-users profiled range from academic and research institutions, clinical laboratories, and pharmaceutical/biotechnology companies to forensic, environmental, and food-testing labs.

Geographically, the report addresses detailed regional breakdowns covering North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa — with country-level focus including major markets like the U.S., Germany, China, India, Japan, Brazil, and UAE. Technological coverage includes traditional gel electrophoresis, capillary electrophoresis, microfluidic electrophoresis, hybrid systems, and digital imaging platforms, reflecting both established and emerging technologies. The report also highlights segmentation by end-user industry focus areas such as academic research, clinical diagnostics, biopharma manufacturing, and regulatory/compliance laboratories. Niche and emerging segments—such as portable point-of-care electrophoresis devices, eco-friendly reagent solutions, and AI-enabled data analysis systems—are included, emphasizing evolving trends in sustainability, automation, and decentralised analytics.

Overall, the scope provides decision-makers and industry professionals with a holistic view of market structure, regional dynamics, technology trends, end-user distribution, and emerging opportunities, offering actionable insight for strategic planning, investment decisions, capacity expansion, and technology adoption across global electrophoresis applications.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2157.12 Million |

|

Market Revenue in 2032 |

USD 3114.92 Million |

|

CAGR (2025 - 2032) |

4.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Thermo Fisher Scientific , Agilent Technologies , Bio-Rad Laboratories , GE Healthcare, PerkinElmer, QIAGEN, Lonza Group, Analytik Jena, Sebia, Shimadzu Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |