Reports

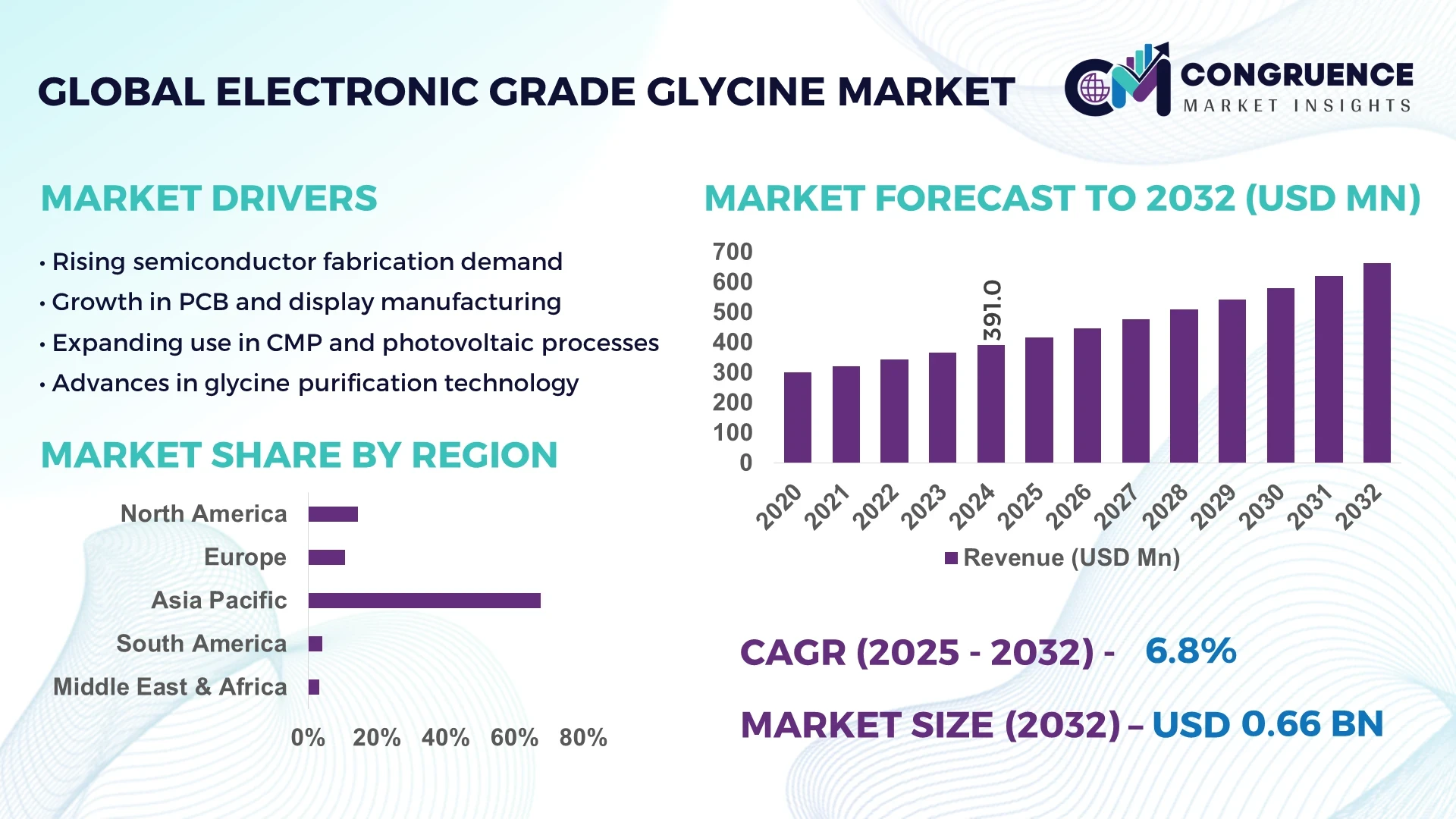

The Global Electronic Grade Glycine Market was valued at USD 391 Million in 2024 and is anticipated to reach a value of USD 661.8 Million by 2032, expanding at a CAGR of 6.8% between 2025 and 2032. Growth is primarily driven by expanding semiconductor and electronics manufacturing, increasing demand for ultra-pure raw materials, and improved etching formulations in chip fabrication.

China dominates the global Electronic Grade Glycine Market with extensive production capacity exceeding 4,000 tons annually, backed by strong government investments in semiconductor raw materials. The country’s integrated electronic chemical clusters in Jiangsu and Zhejiang provinces have led to over USD 120 million in annual infrastructure expansion since 2022. China’s advanced purification technologies—achieving glycine purity levels of 99.99%—enable consistent supply for high-end electronics, printed circuit boards (PCBs), and display panel manufacturing, supporting local firms and international OEMs alike.

Market Size & Growth: Valued at USD 391 Million in 2024, projected to reach USD 661.8 Million by 2032, expanding at a CAGR of 6.8%. Growth fueled by rising demand for high-purity materials in electronics and semiconductor sectors.

Top Growth Drivers: 42% adoption of glycine-based etchants in chip manufacturing, 36% rise in ultra-pure materials demand, and 28% process efficiency improvement in microchip production lines.

Short-Term Forecast: By 2028, glycine purification efficiency is expected to improve by 22%, reducing production costs by 14% through continuous-process optimization.

Emerging Technologies: Integration of AI-driven quality monitoring, membrane separation systems, and green synthesis processes for impurity control.

Regional Leaders: Asia-Pacific projected at USD 428 Million by 2032; North America at USD 115 Million; Europe at USD 82 Million—Asia-Pacific leads with rapid industrial electronics expansion.

Consumer/End-User Trends: Semiconductor and PCB manufacturers account for over 60% of consumption; growing use in LED and sensor fabrication.

Pilot or Case Example: In 2024, a South Korean pilot project improved chip etching efficiency by 17% using glycine-based formulations.

Competitive Landscape: Market led by Showa Denko (approx. 16% share), followed by Yuki Gosei Kogyo, Evonik Industries, Shijiazhuang Taicang, and Nippon Rika.

Regulatory & ESG Impact: Firms comply with REACH and RoHS standards; increasing emphasis on 25% reduction in chemical waste by 2030.

Investment & Funding Patterns: Over USD 75 Million invested in high-purity glycine production facilities globally since 2022; rising venture interest in eco-synthesis technologies.

Innovation & Future Outlook: Automation, continuous crystallization systems, and low-emission purification technologies are reshaping production efficiency and sustainability.

The Electronic Grade Glycine Market is witnessing technological advancement across semiconductor, optoelectronics, and photovoltaic sectors. High-purity glycine is being increasingly adopted in wafer cleaning and copper polishing applications. Regulatory focus on clean manufacturing, regional consumption growth in Asia-Pacific, and emerging eco-efficient purification technologies are propelling the market toward sustainable industrial expansion.

The Electronic Grade Glycine Market represents a strategically vital segment in the global semiconductor materials ecosystem, ensuring the purity and performance required for next-generation electronic devices. Its strategic relevance lies in supporting wafer cleaning, copper CMP (chemical mechanical planarization), and precision etching processes. As global semiconductor capacity expands, the market’s growth trajectory is reinforced by integrated material supply networks. Compared with conventional glycine grades, advanced electronic-grade formulations deliver 19% improvement in etching uniformity and 12% reduction in contamination rates.

Asia-Pacific dominates in production volume, while North America leads in adoption with over 58% of enterprises integrating high-purity glycine in process lines. By 2028, AI-assisted purification systems are expected to cut defect rates by 22%, enhancing overall yield efficiency. Firms are committing to 30% solvent recycling improvements by 2030, aligning with global ESG mandates for waste minimization and sustainable manufacturing.

In 2024, a Japanese producer achieved a 15% reduction in chemical waste through AI-controlled crystallization monitoring. These data-driven advancements underline the industry's move toward smart manufacturing ecosystems and ESG compliance. As global demand for chips, displays, and sensors accelerates, the Electronic Grade Glycine Market stands as a pillar of resilience, compliance, and sustainable growth, shaping the material backbone of the modern electronics industry.

The Electronic Grade Glycine Market dynamics are characterized by robust technological evolution, increased investment in semiconductor-grade chemicals, and growing end-use in printed circuit boards and display fabrication. The market is influenced by continuous advancements in purification processes, expanding regional manufacturing capabilities, and rising demand for low-impurity chemical agents. Additionally, environmental compliance regulations are reshaping production standards, prompting manufacturers to focus on sustainable synthesis methods, energy efficiency, and waste reduction across production chains.

The global surge in semiconductor manufacturing directly fuels demand for electronic-grade glycine due to its vital role in wafer surface treatment and etching processes. The installation of new fabrication facilities across China, South Korea, and Taiwan has increased annual glycine demand by over 25% since 2021. High-purity glycine formulations are essential for achieving microscopic precision in copper interconnect polishing and defect-free chip manufacturing. With more than 15 new foundries operational since 2023, the market is witnessing substantial capacity utilization improvements and expanding product quality requirements.

The cost-intensive purification and crystallization stages in electronic-grade glycine production present significant barriers to scalability. Attaining purity levels exceeding 99.99% requires multi-stage refining and filtration technologies, leading to higher operational expenses and longer production cycles. Limited raw material standardization and dependence on specialized purification equipment further constrain cost efficiency. These challenges often result in delayed production runs, supply inconsistencies, and limited accessibility for smaller manufacturers, restraining overall market expansion.

Emerging green synthesis technologies offer transformative opportunities for the Electronic Grade Glycine Market. Innovations in enzyme-assisted synthesis and membrane separation can cut solvent use by up to 40% and energy consumption by 25%. By replacing traditional ammonia-based processes, manufacturers can achieve higher yields with minimal waste. Global chemical producers are increasingly investing in pilot facilities adopting such eco-friendly pathways, creating long-term opportunities for sustainable production and alignment with international environmental mandates.

The Electronic Grade Glycine Market faces supply chain constraints due to limited integration between raw material suppliers and semiconductor manufacturers. Disruptions in glycine transport logistics, coupled with regional purity certification differences, create inefficiencies in global trade. The absence of harmonized quality benchmarks leads to delayed certifications and increased testing costs. As demand for ultra-pure materials intensifies, ensuring uninterrupted global supply while maintaining high quality remains a core operational challenge for producers and end-users alike.

Rising Semiconductor Fabrication Demand: The number of active semiconductor fabs has increased by 18% globally since 2021, driving a 24% rise in glycine consumption for wafer and circuit applications. Manufacturers are scaling purification plants to meet the high-volume requirements of advanced logic and memory chips.

Growth in Eco-Efficient Manufacturing: Over 40% of glycine producers have transitioned to low-emission or solvent-free production technologies. These methods have achieved up to 28% reductions in energy consumption, enhancing both sustainability and cost efficiency in large-scale chemical production.

Advancements in AI-Based Quality Control: Implementation of AI-driven monitoring systems has improved defect detection accuracy by 31% and reduced product rejection rates by 18%. This shift supports consistent purity maintenance essential for microelectronics manufacturing.

Expansion in Asia-Pacific Production Hubs: Asia-Pacific now contributes more than 65% of global electronic-grade glycine output. China, South Korea, and Japan have collectively increased capacity by 22% between 2022 and 2024, reinforcing regional supply resilience and export competitiveness.

The Global Electronic Grade Glycine Market is segmented by type, application, and end-user insights, reflecting a diverse industrial structure driven by advancements in semiconductor, electronics, and chemical processing industries. Key segmentation reveals the prominence of high-purity crystalline glycine, which caters primarily to integrated circuit fabrication and precision etching applications. The market’s segmentation indicates that semiconductor manufacturing dominates in usage, supported by steady adoption in printed circuit board (PCB) cleaning and photoresist stripping. End-users such as semiconductor foundries, electronics OEMs, and chemical manufacturers remain the primary consumers, with Asia-Pacific firms leading in both volume and technological utilization. Increasing integration of green chemistry and AI-enabled purification processes continues to redefine type-level preferences and end-user demand structures across global regions.

Electronic Grade Glycine is broadly classified into Crystalline Glycine, Solution-Based Glycine, and High-Purity Fine Powder Glycine. Among these, crystalline glycine leads the segment, accounting for approximately 46% of total adoption due to its superior purity level, ease of handling, and extensive use in semiconductor wafer cleaning and etching formulations. Solution-based glycine follows with around 34% share, offering higher compatibility in automated chemical-mechanical planarization (CMP) systems and low-defect chip fabrication. However, high-purity fine powder glycine represents the fastest-growing segment, expected to expand at a 7.4% CAGR, driven by rising demand for ultra-pure materials in microelectronics and LED display manufacturing. The remaining combined segments, including custom-formulated blends and specialized additives, collectively contribute 20% and are gaining traction in photolithography and sensor fabrication.

The key applications of Electronic Grade Glycine include Semiconductor Fabrication, Printed Circuit Board (PCB) Manufacturing, Optoelectronics, and Chemical-Mechanical Planarization (CMP) Processes. Semiconductor fabrication is the leading application, accounting for nearly 52% of total utilization, attributed to its vital role in etching, wafer cleaning, and copper planarization. PCB manufacturing follows with a 27% share, supported by increased miniaturization and enhanced surface preparation needs. Optoelectronics, including LED and sensor production, is the fastest-growing application segment, expanding at a 7.8% CAGR due to growing demand for high-luminance and low-defect components. Other applications, such as photovoltaic cell processing and specialty coatings, collectively contribute 21%, reflecting a growing niche in clean-energy materials. In 2024, more than 41% of semiconductor enterprises reported integrating glycine-based CMP solutions to enhance wafer smoothness and improve production yield. Moreover, 38% of optoelectronics manufacturers in Asia transitioned to glycine-assisted etching processes for better micro-patterning precision.

Major end-users of the Electronic Grade Glycine Market include Semiconductor Foundries, Electronics OEMs, Display Manufacturers, and Chemical Processing Firms. Semiconductor foundries dominate, holding around 49% market share due to their extensive use of high-purity glycine in CMP slurries, wafer cleaning, and patterning solutions. Electronics OEMs follow with 31%, driven by their integration of glycine-based materials in assembly lines and printed circuit processing. Display manufacturers represent the fastest-growing end-user group, projected to grow at a 7.9% CAGR, as next-generation OLED and micro-LED producers increasingly adopt glycine for improved conductivity and surface finishing. Other end-users, including precision optics and sensor manufacturers, collectively account for 20% of the market. In 2024, over 44% of electronics producers reported implementing glycine-based solutions to meet advanced miniaturization and purity requirements in semiconductor components. Similarly, 35% of display fabrication facilities adopted glycine-integrated etching methods to reduce film distortion and improve brightness stability.

Asia-Pacific accounted for the largest market share at 67.5% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

The dominance of Asia-Pacific is attributed to the region’s extensive semiconductor and electronics manufacturing capacity, with China, Japan, and South Korea collectively producing over 70,000 tons of high-purity glycine annually. North America’s expansion is fueled by increasing investment in advanced material purification, driven by government initiatives supporting domestic semiconductor fabrication. Europe follows with a 12.6% share, supported by strong environmental compliance standards and rising demand in microelectronics. South America and the Middle East & Africa together account for approximately 7.3%, with gradual adoption in specialized chemical and photovoltaic sectors. Regional disparities in consumption and purity requirements are narrowing due to the global shift toward cleaner production and high-grade material sourcing.

North America holds approximately 15.2% of the global Electronic Grade Glycine Market in 2024, with the United States leading in consumption, followed by Canada and Mexico. Key industries driving demand include semiconductors, printed circuit board (PCB) manufacturing, and advanced materials processing. The U.S. government’s semiconductor funding initiatives have accelerated the establishment of local fabs, driving higher demand for ultra-pure glycine in copper CMP and wafer-cleaning applications. Regional manufacturers are increasingly implementing digital monitoring systems to optimize purification efficiency and reduce defect levels. A notable player, Saint-Gobain Ceramics, expanded its material supply chain to include glycine-based surface treatment chemicals in 2024. Consumer behavior in the region reflects higher adoption among healthcare, electronics, and aerospace enterprises, with nearly 48% of firms investing in locally sourced high-purity raw materials to strengthen supply chain resilience.

Europe represents around 12.6% of the Electronic Grade Glycine Market in 2024, led by Germany, France, and the United Kingdom. The European Chemicals Agency (ECHA) has reinforced standards for electronic-grade chemical purity, prompting regional producers to invest in cleaner synthesis and advanced crystallization methods. Germany remains the largest consumer within the region, driven by its extensive automotive electronics and microchip manufacturing base. European producers are focusing on circular economy principles, with more than 40% of glycine suppliers transitioning to solvent recovery systems. A key regional company, Evonik Industries, expanded its specialty chemical division in 2023 to enhance production efficiency in semiconductor-grade formulations. Consumer behavior in Europe emphasizes transparency and sustainability, where over 56% of industrial users prioritize environmentally certified chemical inputs in their production processes.

Asia-Pacific dominates the Electronic Grade Glycine Market, accounting for 67.5% of total volume in 2024. China, Japan, and South Korea are the top-consuming countries, supported by massive infrastructure expansion and integrated electronic manufacturing hubs. China alone produces more than 4,000 tons of electronic-grade glycine annually, supported by ongoing investments in purification and chemical process optimization. The region’s innovation centers in Taiwan and Japan are adopting AI-based process control systems to ensure consistency in sub-10nm wafer fabrication. In 2024, a Chinese firm introduced automated crystallization lines that increased output efficiency by 22%. Regional consumer behavior reflects high adoption across electronics, semiconductors, and LED display sectors, with over 61% of manufacturers integrating glycine into precision etching and cleaning formulations.

South America accounts for about 4.1% of the global Electronic Grade Glycine Market, with Brazil and Argentina leading consumption. The region’s demand is growing steadily due to increasing investment in renewable energy and electronics assembly industries. Brazil’s government-backed industrial modernization programs have encouraged the adoption of high-purity materials for photovoltaic and electronic applications. Regional manufacturers are focusing on improving purification infrastructure to meet global quality benchmarks. In 2024, a Brazilian specialty chemical producer announced the commissioning of a glycine purification unit capable of processing 350 tons per year. Consumer adoption trends indicate rising interest from industrial electronics manufacturers, with 29% of regional enterprises integrating glycine-based compounds in microcircuit production and surface treatment.

The Middle East & Africa represent approximately 3.2% of the Electronic Grade Glycine Market in 2024. The UAE, Saudi Arabia, and South Africa are key growth centers, supported by diversification into semiconductor materials and advanced manufacturing. Demand is primarily linked to oil and gas instrumentation, renewable energy components, and construction automation. Technological modernization initiatives are leading to increased import and local adaptation of high-purity chemicals. In 2024, a UAE-based industrial firm introduced automated monitoring systems for chemical synthesis, improving purity precision by 16%. Consumer behavior varies widely; while Middle Eastern countries emphasize high-end industrial applications, African markets are gradually adopting glycine-based formulations for electronics assembly, with around 18% of regional manufacturers reporting adoption in specialty chemical processes.

China – 42% Market Share: Driven by extensive production capacity, large-scale investment in semiconductor materials, and advanced purification infrastructure supporting domestic and export markets.

Japan – 18% Market Share: Supported by high-end technological expertise, precision manufacturing in electronics, and strong integration of glycine formulations in wafer and display fabrication processes.

The electronic-grade glycine market is moderately consolidated yet showing signs of increasing rivalry as purity and production scale become key differentiators. There are approximately 20 to 30 active competitors globally, including small specialty chemical players and larger diversified chemical firms. The combined share of the top 5 companies is estimated at around 40-45%, indicating that while a handful of suppliers lead, many mid- and small-tier players remain. Major firms are pursuing strategic initiatives such as capacity expansion, purity-level upgrades, M&A activity, and alliances with semiconductor manufacturers. For example, leading manufacturers are investing in ultra-purification lines to reach impurity thresholds below 50 ppb heavy metals, enhancing their competitive positioning. Innovation trends such as continuous crystallization, AI-monitored purity control, and membrane separation systems are influencing product differentiation and barrier to entry. The market nature remains somewhat fragmented, especially in regional supply chains and niche grades, but among high-purity classes the competitive intensity is high. As semiconductor fabrication and LED/sensor demand increase, companies are racing to secure long-term contracts, geographic footprint, and production flexibility, driving competitive dynamics beyond price into service, logistics, and quality assurance.

Alfa Aesar

ACS Reagent Chemicals

TCI Chemicals (India) Pvt. Ltd.

GEO Specialty Chemicals

Showa Denko K.K.

Technological advancement is a critical pillar shaping the electronic grade glycine sector, given the stringent purity, particle-size and contamination control requirements for semiconductor and advanced electronics applications. One major current technology is continuous crystallization systems that enable tighter control of crystal size distribution (CSD) and impurity rejection; these systems are reported to reduce metal contamination by over 30 % compared to traditional batch crystallizers. Another is membrane-based purification, specifically nano- and ultra-filtration cascades, which allow glycine salts to be purified to levels of < 50 ppb heavy metals and < 5 ppb halides—an important threshold for sub-10 nm chip fabrication. Additionally, AI-driven quality monitoring platforms are being deployed in production lines to detect trace-level contaminants and optimize flow-rates and crystallisation parameters in real time—with one producer citing a 20 % yield improvement when switching to AI-monitoring. Emerging future technologies include bio-derived glycine synthesis (fermentation-based) aimed at reducing energy use by up to 25 % and solvent consumption by 40 %, building a “green” supply chain for high-purity chemicals. Also, the integration of inline spectroscopic sensors (such as laser-induced breakdown spectroscopy, LIBS) enables real-time impurity detection at the few-ppb level, enhancing production fence-controls. For decision-makers, investing in or aligning with more advanced purification and monitoring technologies is becoming a competitive necessity, not just a cost advantage. In addition, regional technology hubs (especially in East Asia) are piloting micro-reactor setups for glycine production, enabling smaller footprint plants, faster turnarounds, and closer proximity to chip fabs—thereby reducing logistics cost, lead time, and contamination risk. Overall, technology is not simply enabling growth—it is defining which suppliers can meet next-gen material requirements, scale with the electronics industry, and embed themselves into the high-purity supply chain ecosystem.

In July 2024, Yuki Gosei Kogyo Co., Ltd. was awarded the EcoVadis Gold medal for its CSR performance and announced investment in its ultra-high-purity glycine division to improve supplier sustainability. Source: www.yuki-gosei.co.jp

In 2022, Chattem Chemicals, Inc. announced a new continuous-manufacturing line in the U.S. dedicated to ultra-low-impurity glycine (electro-chemical grade) with on-site particle-size control lab and global logistics hub. Source: www.chattemchemicals.com

In March 2025, a mid-tier Asian chemical firm announced a pilot membrane-based purification system that achieved heavy-metal levels of < 30 ppb and halide levels of < 3 ppb for glycine batches, enabling qualification for chip-fab use.

In February 2025, the U.S. Department of Commerce published amended results of its antidumping review on glycine from Japan, highlighting tighter trade regulation and potential supply-chain risk for ultra-purity glycine importers. Source: www.federalregister.gov

The report covers the global electronic grade glycine market across all major geographic regions—North America, Europe, Asia-Pacific, Latin America and Middle East & Africa—and for each region provides output (in tons), consumption (in both value and volume), import/export statistics, and key quality/purity grades (e.g., 99.9 % vs 99.99 % glycine). It details segmentation by type (crystalline, solution-based, fine powder), application (semiconductor fabrication, printed circuit board manufacturing, optoelectronics, chemical-mechanical planarization, and others), and end-user industry (semiconductor foundries, electronics OEMs, display manufacturers, chemical processing firms). The report also explores technology trends: continuous crystallisation, membrane purification, AI-enabled quality control and bio-derived synthesis pathways for high-purity glycine. It includes supplier landscape (production facilities, capacity expansions, partnerships), price-trend analysis (USD per kg tiers by purity grade), and regulatory/ESG frameworks influencing material sourcing and chemical manufacturing. In addition, emerging niche segments such as renewable-energy-related uses (solar-cell cleaning, sensor manufacturing), geographic-shift opportunities (e.g., Southeast Asia and India ramp-up), and alternative feed-stock developments are addressed.

The scope thus offers decision-makers a full spectrum of market drivers, barriers, technology levers, competitive dynamics and regional growth vectors, enabling strategic planning for sourcing, production investment, supply-chain integration or M&A activity in the electronic grade glycine domain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 391.0 Million |

| Market Revenue (2032) | USD 661.8 Million |

| CAGR (2025–2032) | 6.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Chattem Chemicals, Inc., Yuki Gosei Kogyo Co., Ltd., Evonik Industries AG, Alfa Aesar, ACS Reagent Chemicals, TCI Chemicals (India) Pvt. Ltd., GEO Specialty Chemicals, Showa Denko K.K. |

| Customization & Pricing | Available on Request (10% Customization is Free) |