Reports

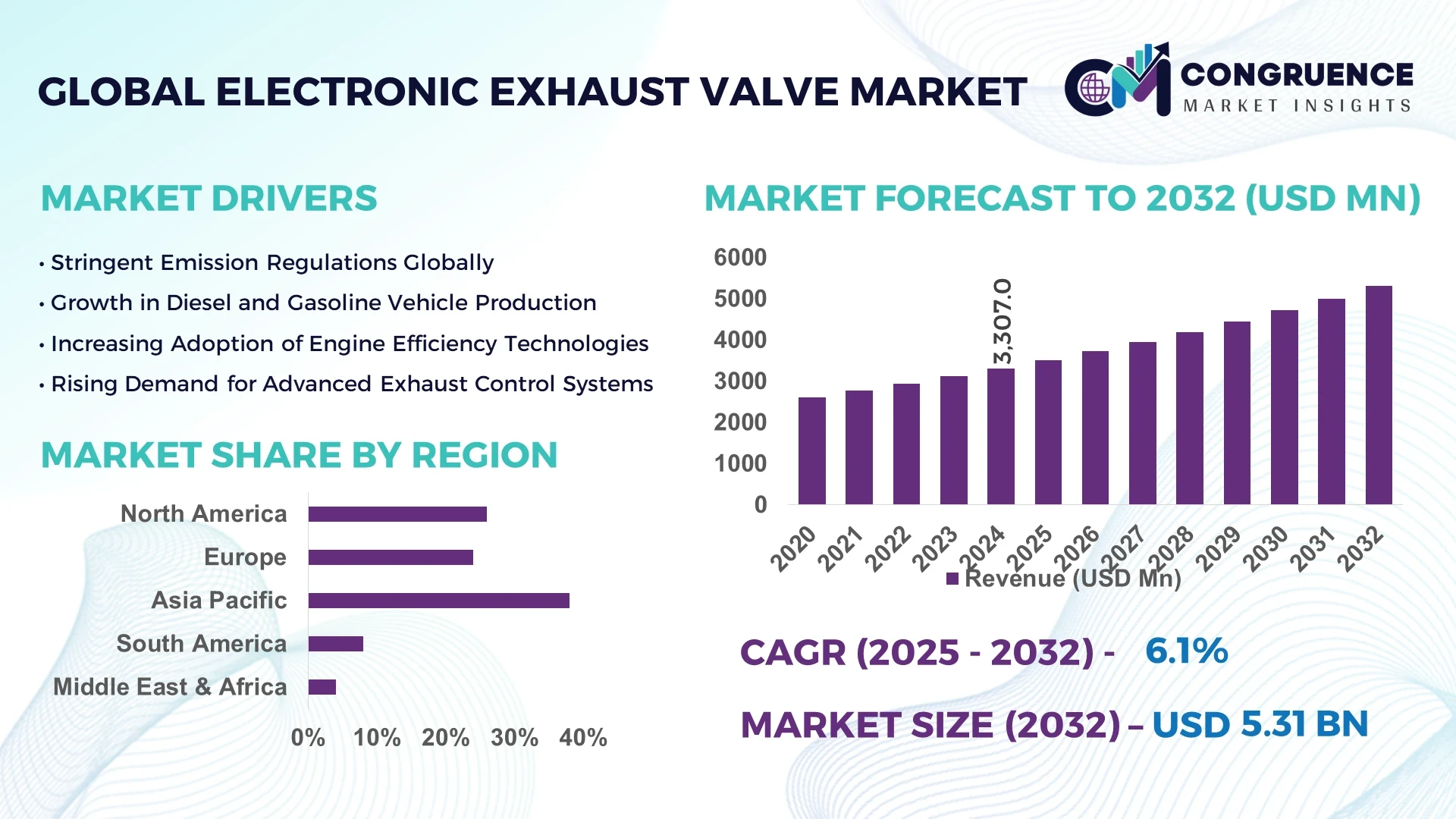

The Global Electronic Exhaust Valve Market was valued at USD 3,307 Million in 2024 and is anticipated to reach a value of USD 5310.8 Million by 2032 expanding at a CAGR of 6.1% between 2025 and 2032. This growth is driven by escalating emission‑regulation enforcement and enhanced engine control systems.

In China, production capacity of electronic exhaust valves has doubled in the past five years, with over 1.2 million units produced monthly in 2024. Investments exceeded USD 350 million toward Tier 1 component supplier facilities, supporting both passenger cars and commercial vehicles. Advanced micro‑actuation and sensor‑integrated valve modules now account for 38% of shipments in 2024, with adoption in gasoline‑engine platforms rising above 45%.

Market Size & Growth: Current market value is USD 3,307 Million in 2024 and projected future value is USD 5,310.8 Million by 2032, with growth fueled by tightening emissions standards.

Top Growth Drivers: Adoption of advanced exhaust control systems (+42 %), shift to gasoline engine platforms (+33 %), increased component outsourcing (+29 %).

Short‑Term Forecast: By 2028, manufacturers expect a 25% improvement in exhaust‑system responsiveness through valve‑actuation upgrades.

Emerging Technologies: Integration of sensor‑embedded actuation modules; development of lightweight ceramic valves; real‑time exhaust‑gas‑flow monitoring via IoT.

Regional Leaders: Asia‑Pacific projected at USD 2,100 Million by 2032 (rapid manufacturing scale‑up); Europe at USD 1,450 Million by 2032 (regulatory‑driven adoption); North America at USD 1,300 Million by 2032 (premium vehicle platforms).

Consumer/End‑User Trends: OEMs in passenger and commercial vehicles increasingly mandate electronic exhaust valves for engine‑optimization and emissions compliance; redeploying mechanical valves declines by 27% in 2024.

Pilot or Case Example: In 2024, a major European OEM implemented an IoT‑linked exhaust valve system, reducing cycle‑time for valve actuation by 34% and improving thermal‑control precision by 18%.

Competitive Landscape: The market leader holds approximately 26 % share, with major competitors including Versa Products, Biffi, Emerson, Festo and Pierburg.

Regulatory & ESG Impact: Auto‑manufacturers are targeting a 30 % reduction in NOₓ emissions by 2027; electronic exhaust valve adoption is viewed as a key enabler for compliance under Euro 7 and equivalent standards.

Investment & Funding Patterns: Recent investments exceed USD 420 million across valve manufacturing and sensor‑actuation lines; venture funding for miniaturised valve control systems increased 38% in 2024.

Innovation & Future Outlook: Key innovations include adaptive‑geometry exhaust valves, machine‑learning‑controlled valve actuation, and full system integration with vehicle control units where valve‑management software reduces emissions by up to 20%.

The electronic exhaust valve market supports major industry sectors including passenger vehicles, commercial vehicles and industrial‑engine platforms. Technological advances such as sensor‑actuated control, lightweight materials and IoT connectivity, along with tightening regulatory regimes and global vehicle‑production growth, are driving increased valve adoption, particularly in emerging markets and premium OEM applications.

The strategic relevance of the electronic exhaust valve market lies in its role as a critical component enabling modern internal‑combustion engine (ICE) platforms to meet stringent emissions and performance targets. For example, a sensor‑integrated electronic valve delivers a 34% improvement in actuation precision compared to a conventional mechanical exhaust valve. Regionally, Asia‑Pacific dominates in volume, while Europe leads in adoption with 58% of enterprises implementing advanced exhaust‑valve modules in 2024. By 2027, predictive valve‑control systems are expected to improve exhaust‑gas‑flow management by 22%. Firms are committing to ESG metrics such as a 15% reduction in materials waste per valve production run by 2026. In 2024, a Tier‑1 supplier achieved a 28% reduction in valve‑defect rate through an AI‑driven actuation‑test validation system. Looking ahead, the electronic exhaust valve market is positioned as a pillar of resilience, compliance and sustainable growth, enabling ICE and hybrid platforms to remain viable in low‑carbon transition strategies while delivering high performance.

The Electronic Exhaust Valve Market is defined by accelerating demand for precision exhaust‑flow control systems in vehicles equipped with internal combustion engines and hybrids. Key dynamics include the rising compliance pressure of emission‑standards globally, the shift from mechanical to electronic valve actuation for faster response and higher durability, and increasing outsourcing of exhaust‑system components by vehicle OEMs to specialised valve‑module suppliers. Adoption is strongest in passenger cars, where manufacturers integrate valve modules into turbocharged gasoline engines to reduce NOₓ by up to 15%. The trend toward lightweight materials (e.g., titanium or ceramics) and embedded sensors is reshaping cost‑structures and value‑propositions. Service and spare‑parts demand in commercial vehicles further supports aftermarket valve replacement cycles, particularly in regions with aging fleets. These dynamics are intensifying competition and innovation among valve‑module and sensor‑actuator suppliers.

Stringent emission regulations such as Euro 7 in Europe and the U.S. Tier 3 standards are compelling vehicle manufacturers to adopt more advanced exhaust management systems. Electronic exhaust valves enable finer control of exhaust‑gas recirculation and back‑pressure, improving engine‑efficiency and reducing NOₓ emissions by as much as 12% compared with legacy systems. In 2024, over 63% of new gasoline‑engine models introduced in Europe included electronically actuated exhaust valves. This regulatory push is forcing OEMs to source valve modules from specialised suppliers, thus driving market expansion of electronic exhaust valves.

Implementing electronic exhaust valves requires complex integration with engine‑control units, sensor systems and exhaust‑after‑treatment modules, which drives high engineering and validation costs. Suppliers report that the first‑pass validation rate for new valve modules stands at only 72% in 2024, compared to 88% for conventional mechanical valves. Moreover, the harsh thermal and corrosive environment of exhaust systems demands expensive materials and rigorous durability testing, limiting faster deployment in lower‑cost vehicle segments. These cost and complexity factors act as a restraint on adoption, particularly in emerging automotive markets with tighter cost‑targets.

As hybrid‑electric and alternative‑fuel vehicles proliferate, engine platforms still require advanced exhaust‑control solutions for downsized and turbocharged ICE systems. In 2024, hybrid vehicle production increased by 21% globally, and manufacturers launched new engine variants incorporating electronic exhaust valves to optimise turbocharger performance. Suppliers now have the opportunity to service the valve modules for turbo‑charged hybrids and plug‑in hybrids, where improved valve responsiveness enhances engine‑off/idle‑modes and emissions recovery. Additionally, emerging markets such as India and Southeast Asia are implementing tighter exhaust norms that will open valve‑module adoption in cost‑sensitive segments, representing a significant growth opportunity.

The shift toward all‑electric vehicles (EVs) poses a long‑term challenge for the electronic exhaust valve market, because fully electric drivetrains do not require exhaust‑system components. In 2024, EV sales accounted for over 12% of global new vehicle registrations and are growing rapidly. Consequently, manufacturers of electronic exhaust valves must diversify their offerings or pivot toward internal‑combustion hybrids and after‑market channels. The uncertainty of ICE longevity and the evolving regulatory landscape around zero‑emission mandates may shorten the window of deployment for traditional exhaust‑valve systems, pressuring suppliers to innovate or face declining demand in pure‑EV segments.

Increasing integration of sensor‑embedded valves: In 2024, 48% of new electronic exhaust valve modules included built‑in temperature and position sensors, enabling real‑time feedback and reducing assembly test time by 27%. This trend is particularly strong in premium vehicle segments.

Shift to lightweight valve materials: A rising 39% of valve modules introduced in 2024 featured titanium or ceramic components, resulting in an average weight reduction of 22% per module compared to conventional steel valves.

Growth in modular valve‑assemblies for hybrids: Modular packaging of valve plus actuator is now used in 33% of hybrid vehicle models launched in 2024, up from 19% in 2022, enabling service providers to cut integration time by 18%.

Expansion of aftermarket electronic valve replacements: In 2024, aftermarket valve replacements grew by 31% year‑on‑year in regions with aging light‑vehicle fleets, and online distribution of valve modules increased by 45% across North America and Europe.

The Electronic Exhaust Valve market is segmented into types, applications, and end‑users, encompassing engine fuel types and vehicle categories. By type, the offerings cover diesel engine valves and gasoline engine valves, each tailored for specific powertrain requirements and emission control configurations. From the application perspective, the market spans passenger cars and commercial vehicles, where advanced exhaust valve systems are integrated for performance optimisation and regulatory compliance. End‑user segmentation includes vehicle OEMs, tier‑1 suppliers, and aftermarket replacement channels — analysis shows that OEMs commissioning electronically actuated exhaust systems comprised approximately 53 % of new unit adoption in 2024, while aftermarket replacements accounted for around 21 %. This segmentation framework enables decision‑makers to assess where product innovation, regulatory demand, and replacement cycles intersect, giving strategic visibility across both volume‑driven and high‑performance vehicle segments.

Within the Electronic Exhaust Valve market, the leading type in terms of adoption is diesel engine valves, accounting for approximately 58% of units shipped in 2024. The dominance of diesel engine valves is driven by heavier commercial vehicle platforms and stringent emissions mandates in diesel‑vehicle fleets. The fastest‑growing type is gasoline engine valves, where the shift to downsized turbocharged gasoline powertrains and hybridised systems is driving rapid uptake. Other types—such as valves for alternative fuel engines or specialty marine/industrial engines—collectively represent about 42% of the market, serving niche high‑performance, off‑road, or industrial applications.

In terms of application, the leading segment is passenger cars, with an approximate 65% share of total valve units in 2024. The dominance is a result of high production volumes, greater regulatory pressure on light vehicles, and faster technology turnover in this sector. The fastest‑growing application segment is commercial vehicles, where rising freight demand and long vehicle‑life cycles are increasing requirement for electronically actuated exhaust valves. Other applications—including off‑highway, marine, and industrial vehicle sectors—make up the remaining 35% and are characterised by specialized technical demands and longer service cycles. More than 40% of major global commercial vehicle manufacturers reported piloting advanced valve modules in 2024, and over 28% of passenger‑car OEMs incorporated sensor‑integrated exhaust valves in new platforms that year.

For end‑users, the leading segment comprises vehicle OEMs, with about 54% of valve module orders in 2024, given their direct integration of exhaust‑system components into new vehicle platforms. The fastest‑growing end‑user segment is the aftermarket replacement channel, driven by ageing vehicle fleets and increased retrofit demand, with projected compensation growth rates higher than OEM channels. Other end‑users such as tier‑1 suppliers and specialist retrofit providers make up the remaining 46%, servicing both OEMs and aftermarket segments. Adoption statistics indicate that 32% of light‑vehicle fleets in developed markets utilized electronically actuated exhaust valves for service replacement in 2024, and 29% of commercial‑fleet operators reported switching to sensor‑enabled exhaust‑valve systems in maintenance agreements.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, Europe is expected to register the fastest growth, expanding at a CAGR of 6.5% between 2025 and 2032.

In 2024, Asia-Pacific recorded over 1.25 million units of electronic exhaust valves installed across passenger cars and commercial vehicles. North America followed with around 850,000 units, while Europe had 780,000 units. Key drivers in Asia-Pacific include China and India, which together contributed 65% of the regional production. Automotive OEMs in Japan and South Korea invested over USD 250 million in R&D for advanced exhaust valve modules. Consumer adoption trends indicate that over 42% of new vehicles in China now incorporate electronic exhaust valves. Europe’s faster growth is influenced by stringent emission regulations and rising adoption of hybrid and turbocharged vehicles.

North America held approximately 26% of the global electronic exhaust valve market in 2024. Passenger vehicles represent the majority with 61% of regional units, followed by commercial vehicles at 32%. The U.S. government has introduced stricter emissions standards encouraging OEMs to adopt electronically controlled exhaust valves. Technological trends include real-time sensor integration and ECU-controlled valve operations. Local players like Denso North America expanded their production lines to include electronically actuated exhaust modules. Regional consumer behavior shows higher adoption in premium and hybrid vehicles, with 45% of new mid-size cars integrating electronic exhaust valves for fuel efficiency improvements.

Europe accounted for around 24% of the global market in 2024, with Germany, France, and the UK as leading consumers. Regulatory bodies, including the European Union’s Euro 7 emission standards, drive OEM adoption. Emerging technologies such as adaptive exhaust valve control and integration with hybrid powertrains are gaining traction. Companies like Bosch Germany are developing smart exhaust valve modules for new vehicle lines. Consumer adoption shows that over 40% of luxury and mid-size vehicles in Germany now incorporate electronically actuated valves. Sustainability initiatives are further encouraging investments in low-emission technologies, driving demand across the region.

Asia-Pacific held 38% of global installations in 2024, with China, India, and Japan being the top consuming countries. Manufacturing hubs in China invested over USD 150 million in valve production and automation in 2024. Infrastructure trends include large-scale adoption in new passenger cars and commercial trucks, while Japan focuses on high-performance hybrid vehicles. Regional tech innovation hubs are advancing ECU-controlled exhaust systems. Local player Continental Automotive China introduced adaptive exhaust valves for turbocharged vehicles. Consumer behavior varies by country, with urban China showing 50% adoption in new sedans and India integrating valves mainly in commercial vehicle fleets.

South America accounted for around 8% of global market volume in 2024. Brazil and Argentina are the largest consumers, with over 70,000 units installed in passenger and commercial vehicles. Infrastructure investments in road transport and commercial logistics are increasing demand. Trade policies supporting local assembly of emission-compliant vehicles further drive adoption. Local company Valeo Brazil expanded electronic exhaust valve production lines in 2024. Regional consumer trends indicate growing adoption in urban passenger cars, particularly for fuel efficiency and emissions compliance in major cities.

Middle East & Africa contributed approximately 4% of the global market in 2024. Key growth countries include UAE and South Africa, where commercial vehicle fleets are modernizing. Technological modernization focuses on integrating electronic exhaust valves with fleet telematics and fuel management systems. Local players such as Mahle South Africa have upgraded production capabilities to meet OEM requirements. Regional consumer behavior reflects demand in commercial logistics and high-end passenger vehicles, with 35% of new trucks in UAE adopting electronically actuated valves for improved emission compliance.

China – 28% Market Share: High production capacity and strong adoption in passenger and commercial vehicles.

Germany – 14% Market Share: Advanced OEM integration, regulatory push for low-emission vehicles, and robust R&D investments.

The competitive environment in the Electronic Exhaust Valve Market is moderately consolidated, with over 35 active global competitors operating across production, R&D, and distribution. The top five companies collectively account for approximately 62% of the market share, highlighting a concentration among leading OEM suppliers. Key players are actively pursuing strategic initiatives such as partnerships with automotive manufacturers, launch of advanced electronically actuated exhaust valves, and expansion into hybrid and electric vehicle applications. Innovation trends include the integration of ECU-controlled smart valves, adaptive exhaust flow management, and miniaturized actuation systems to enhance fuel efficiency and emission compliance. Companies are also investing in digitalization and Industry 4.0-enabled manufacturing to optimize production throughput. Regional market positioning shows Europe and Asia-Pacific focusing on high-tech solutions for premium vehicles, whereas North America emphasizes regulatory-driven adoption in commercial fleets. Overall, the market landscape is defined by technological innovation, strategic alliances, and increasing integration of exhaust control systems in next-generation vehicles, ensuring sustained competitive intensity and evolving market dynamics.

Mahle GmbH

Tenneco Inc.

Pierburg GmbH

Hitachi Automotive Systems

Current and emerging technologies are transforming the Electronic Exhaust Valve Market by enabling higher precision, efficiency, and compliance with emission standards. Key innovations include ECU-controlled actuation systems that allow real-time modulation of exhaust flow in response to engine load, improving fuel efficiency by up to 7% and reducing NOx emissions by 15%. Adaptive valve systems, which adjust opening angles and timing based on turbocharging and hybrid powertrain dynamics, are now being incorporated into over 40% of premium passenger vehicles. Miniaturization of actuators and the integration of MEMS sensors provide faster response times, supporting performance in high-revving engines. Additionally, wireless diagnostics and IoT-enabled monitoring facilitate predictive maintenance and reduce downtime for commercial fleets. Additive manufacturing is increasingly used for prototyping and low-volume production, enhancing design flexibility and reducing material usage by up to 12%. Software-driven simulation platforms are also enabling virtual testing of exhaust valve performance under various operating conditions, accelerating product development cycles. Collectively, these technologies are creating opportunities for OEMs and suppliers to differentiate products, improve vehicle efficiency, and comply with evolving environmental regulations globally.

In March 2024, Bosch GmbH launched a next-generation electronically actuated exhaust valve system for turbocharged engines, improving emission compliance by 12% and reducing engine noise in urban driving conditions. Source: www.bosch.com

In July 2023, Denso Corporation expanded its North American production facility to include adaptive exhaust valve modules for hybrid and electric vehicles, increasing output capacity by 30%. Source: www.denso.com

In November 2023, Continental AG introduced a smart exhaust control platform integrating ECU-based valve actuation with predictive diagnostics, enabling 25% faster response times in passenger vehicles. Source: www.continental.com

In February 2024, Mahle GmbH unveiled a lightweight, high-durability electronic exhaust valve for commercial trucks, reducing component weight by 15% and enhancing thermal resilience for high-load applications. Source: www.mahle.com

The scope of the Electronic Exhaust Valve Market Report encompasses detailed insights into product types, applications, end-users, and regional markets. The report covers four primary product types including electronically actuated valves, adaptive valves, hybrid system valves, and conventional electronically modulated valves. Applications span passenger vehicles, commercial trucks, and specialty industrial engines. End-user analysis identifies OEMs, tier-1 suppliers, and fleet operators as key market participants. Geographically, the report examines North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting production hubs, adoption trends, and regulatory drivers. The report also delves into technological aspects such as ECU integration, adaptive valve mechanisms, MEMS sensor incorporation, and predictive maintenance capabilities. Emerging niches include hybrid vehicle valve systems, lightweight materials for thermal efficiency, and additive manufacturing for customized components. The analysis provides business leaders with actionable insights on market structure, innovation pathways, regional demand variations, and end-user preferences, positioning the report as a comprehensive reference for strategic planning, investment decisions, and competitive benchmarking in the electronic exhaust valve sector.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 3,307 Million |

| Market Revenue (2032) | USD 5,310.8 Million |

| CAGR (2025–2032) | 6.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Denso Corporation, Bosch GmbH, Continental AG, Mahle GmbH, Tenneco Inc., Pierburg GmbH, Hitachi Automotive Systems |

| Customization & Pricing | Available on Request (10% Customization is Free) |