Reports

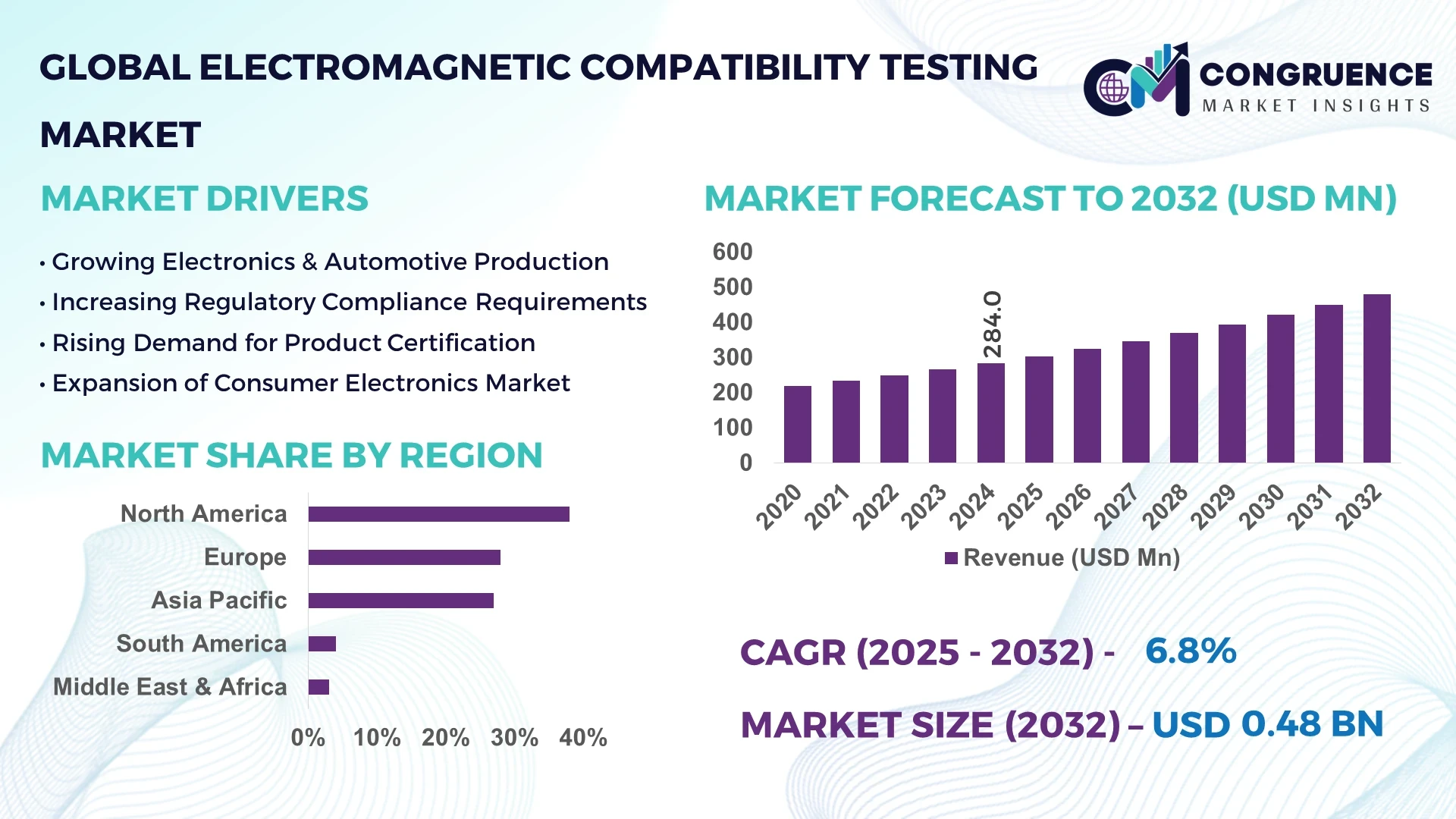

The Global Electromagnetic Compatibility Testing Market was valued at USD 284.0 Million in 2024 and is anticipated to reach a value of USD 480.7 Million by 2032, expanding at a CAGR of 6.8% between 2025 and 2032. This growth is primarily driven by the increasing complexity of electronic devices and stringent regulatory requirements across various industries.

The United States stands as a dominant force in the Electromagnetic Compatibility Testing Market, driven by its robust electronics, automotive, and aerospace sectors. The U.S. market captured the largest revenue share in 2024, supported by the rising deployment of 5G networks, electric vehicle (EV) adoption, and the proliferation of Internet of Things (IoT) devices. Key players such as Keysight Technologies and ETS-Lindgren have strengthened the market outlook, while regulatory requirements from the Federal Communications Commission (FCC) continue to accelerate adoption. The presence of advanced testing facilities and a strong focus on innovation further bolster the nation's leadership in this domain.

Market Size & Growth: The market was valued at USD 284.0 million in 2024 and is projected to reach USD 480.7 million by 2032, expanding at a CAGR of 6.8%. This growth is attributed to the increasing complexity of electronic devices and stringent regulatory requirements.

Top Growth Drivers: Rising demand for consumer electronics (35%), stringent regulatory standards (30%), and the proliferation of IoT devices (25%).

Short-Term Forecast: By 2028, the implementation of AI-driven testing solutions is expected to reduce testing time by 20%, enhancing efficiency.

Emerging Technologies: Integration of AI and machine learning in testing procedures, development of 5G-compliant testing equipment, and advancements in anechoic chamber designs.

Regional Leaders: North America (USD 200 Million by 2032), Europe (USD 150 Million by 2032), and Asia-Pacific (USD 130 Million by 2032). North America leads in volume, while Europe exhibits higher adoption rates among enterprises.

Consumer/End-User Trends: Increased adoption in automotive and aerospace sectors, with a growing emphasis on compliance with international EMC standards.

Pilot or Case Example: In 2023, a leading automotive manufacturer implemented AI-based EMC testing, resulting in a 15% reduction in product development time.

Competitive Landscape: Keysight Technologies (35% market share), followed by ETS-Lindgren, Rohde & Schwarz, Teseq AG, and AR Europe.

Regulatory & ESG Impact: Compliance with FCC regulations and EU directives is driving the adoption of advanced EMC testing solutions.

Investment & Funding Patterns: In 2024, the market witnessed investments exceeding USD 50 Million, focusing on R&D and infrastructure development.

Innovation & Future Outlook: The future of EMC testing lies in the integration of AI and machine learning, enabling predictive testing and real-time compliance monitoring.

The Electromagnetic Compatibility Testing Market is characterized by a diverse range of applications across various industries, including automotive, aerospace, telecommunications, and consumer electronics. Recent technological advancements, such as the integration of AI and machine learning in testing procedures, are enhancing the efficiency and accuracy of EMC testing. Regulatory bodies worldwide are enforcing stringent standards, compelling industries to adopt advanced testing solutions to ensure compliance. Regional consumption patterns indicate a significant demand in North America and Europe, driven by the presence of key industries and regulatory frameworks. The market is poised for sustainable growth, with emerging trends like 5G technology and IoT devices further propelling the need for effective EMC testing solutions.

The strategic relevance of the Electromagnetic Compatibility (EMC) Testing Market is underscored by its critical role in ensuring the functionality and safety of electronic devices across various sectors. With the increasing complexity of electronic systems and the proliferation of interconnected devices, the need for robust EMC testing has never been more pronounced.

By 2026, the integration of AI-driven testing solutions is expected to enhance testing accuracy by 25%, reducing the risk of interference in electronic devices. Comparatively, traditional testing methods often result in longer development cycles and higher costs. In regions like North America, the volume of EMC testing is substantial, whereas Europe leads in the adoption rate among enterprises, with over 60% of companies implementing advanced EMC testing solutions.

Short-term projections indicate that by 2025, the adoption of 5G technology will necessitate a 30% increase in EMC testing to ensure device compliance with new electromagnetic standards. Firms are committing to sustainability metrics, such as achieving a 20% reduction in electromagnetic interference by 2030, aligning with global environmental goals.

In 2024, a leading telecommunications company achieved a 15% reduction in product development time through the implementation of AI-based EMC testing solutions. This micro-scenario exemplifies the tangible benefits of adopting advanced testing methodologies.

Looking forward, the Electromagnetic Compatibility Testing Market is positioned as a cornerstone for resilience, compliance, and sustainable growth in the electronics industry. The continuous evolution of testing technologies and adherence to regulatory standards will drive the market's trajectory, ensuring the seamless operation of electronic devices in an increasingly interconnected world.

The Electromagnetic Compatibility Testing Market is influenced by various dynamics that shape its growth and development. Key factors include the rapid advancement of electronic technologies, stringent regulatory requirements, and the increasing complexity of electronic systems. Industries such as automotive, aerospace, and telecommunications are at the forefront of adopting advanced EMC testing solutions to mitigate electromagnetic interference and ensure device reliability. Technological innovations, including AI-driven testing tools and automated testing platforms, are enhancing the efficiency and accuracy of EMC testing procedures.

The escalating complexity of electronic devices necessitates advanced Electromagnetic Compatibility (EMC) testing to ensure their functionality and safety. Modern electronic systems, characterized by miniaturization and integration of multiple components, are more susceptible to electromagnetic interference. This complexity requires sophisticated testing methodologies to identify and mitigate potential issues. Industries such as automotive, aerospace, and telecommunications are investing in state-of-the-art EMC testing solutions to comply with stringent regulatory standards and maintain product reliability.

The high cost associated with advanced Electromagnetic Compatibility (EMC) testing equipment poses a significant challenge to market growth. Small and medium-sized enterprises (SMEs) often face financial constraints that limit their ability to invest in state-of-the-art testing facilities. Additionally, the rapid pace of technological advancements necessitates frequent upgrades to testing equipment, further escalating costs. These financial barriers can impede the adoption of advanced EMC testing solutions, particularly in emerging markets.

The rise of electric vehicles (EVs) presents significant opportunities for the Electromagnetic Compatibility (EMC) Testing Market. EVs incorporate numerous electronic components, including power electronics, battery management systems, and infotainment units, all of which require rigorous EMC testing to ensure their performance and compliance with regulatory standards. As the adoption of EVs increases globally, the demand for specialized EMC testing solutions tailored to the unique challenges of electric drivetrains and high-voltage systems is expected to grow substantially.

The rapid pace of technological advancements presents a challenge to the Electromagnetic Compatibility (EMC) Testing Market due to the continuous emergence of new electronic components and systems. These innovations often introduce novel electromagnetic interference issues that existing testing methodologies may not adequately address. Consequently, testing protocols must be regularly updated to keep pace with technological developments, requiring significant investment in research and development. This dynamic environment necessitates a proactive approach to ensure that EMC testing solutions remain effective and relevant.

Integration of AI in Testing Procedures: The adoption of Artificial Intelligence (AI) in Electromagnetic Compatibility (EMC) testing procedures is enhancing the efficiency and accuracy of testing processes. AI algorithms can analyze complex data sets, identify potential interference issues, and predict performance outcomes, leading to faster and more reliable testing results.

Development of 5G-Compliant Testing Equipment: With the global rollout of 5G networks, there is a growing demand for EMC testing equipment capable of evaluating devices' compliance with 5G electromagnetic standards. Manufacturers are developing specialized testing solutions to assess the performance of 5G-enabled devices and ensure they meet regulatory requirements.

Advancements in Anechoic Chamber Designs: Innovations in anechoic chamber designs are improving the accuracy of EMC testing. New materials and construction

The Electromagnetic Compatibility (EMC) Testing Market is segmented to provide a clear understanding of its types, applications, and end-user dynamics. By type, the market encompasses conducted testing, radiated testing, and system-level testing, each catering to specific EMC requirements. Applications range across automotive, aerospace, telecommunications, consumer electronics, and medical devices, highlighting the diverse industries reliant on EMC compliance. End-users include manufacturers, testing laboratories, R&D centers, and certification bodies. Regional variations in adoption, technology infrastructure, and regulatory compliance further influence market segmentation, guiding investment and strategic decisions. Understanding these segments allows stakeholders to identify opportunities, optimize testing protocols, and align with evolving regulatory and technological standards.

Conducted testing currently accounts for approximately 40% of the EMC testing adoption, making it the leading type due to its efficiency in evaluating interference conducted through cables and wiring systems. Radiated testing holds 30% of the market and is experiencing the fastest growth, driven by the proliferation of wireless and IoT devices requiring compliance verification in real-world environments. System-level testing contributes the remaining 30%, focusing on complete device evaluation for high-complexity applications.

Automotive applications dominate the EMC testing market with a 35% adoption share, primarily due to the rapid integration of electric vehicles, ADAS systems, and connected car technologies requiring rigorous electromagnetic compliance testing. Aerospace and defense applications hold 25%, supporting critical communication and navigation systems. Telecommunications and consumer electronics collectively account for 40% of applications, with growth driven by 5G deployment and IoT proliferation. In 2024, over 42% of telecommunication companies globally adopted EMC testing for 5G devices to ensure network compatibility and minimize interference.

Manufacturers remain the leading end-user segment, accounting for 45% of EMC testing adoption, due to their responsibility for ensuring product compliance before market release. Testing laboratories and certification bodies represent 30%, focusing on regulatory compliance and independent verification. R&D centers account for the remaining 25%, leveraging EMC testing to innovate and integrate new technologies efficiently. In 2024, over 38% of global automotive manufacturers piloted AI-integrated EMC testing systems to accelerate vehicle development and reduce interference risks.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

In 2024, North America recorded over 110 EMC testing facilities, with the US contributing 70 facilities and Canada 25 facilities. Asia-Pacific has more than 95 facilities, led by China with 45, India with 20, and Japan with 18. Europe accounted for 28% of the market with Germany (12%), UK (7%), and France (5%). South America had 12% share with Brazil (6%) and Argentina (3%). Middle East & Africa collectively contributed 10% with UAE and South Africa driving demand. Increasing adoption across automotive, aerospace, and consumer electronics industries, coupled with rising government compliance mandates, is shaping regional dynamics.

North America holds a 38% share of the EMC testing market. Key industries driving demand include automotive, aerospace, defense, and consumer electronics. Regulatory initiatives from the FCC and EPA, along with government-supported compliance programs, are enhancing market activity. Technological advancements include AI-driven testing tools and automated test systems. For example, TUV Rheinland US recently upgraded its testing facilities to integrate high-speed radiated and conducted EMC testing, reducing evaluation time by 18%. Regional consumer behavior shows higher enterprise adoption in healthcare and finance sectors, leveraging EMC testing to ensure safety and reliability in critical applications.

Europe accounts for 28% of the EMC testing market. Key countries include Germany, the UK, and France, with Germany representing 12% of adoption. Regulatory bodies such as CE and ETSI enforce stringent compliance standards, prompting manufacturers to integrate advanced EMC testing early in product design. Emerging technologies include automated test chambers and digital simulation tools. SGS Germany recently implemented a comprehensive EMC testing program for connected automotive components, increasing test throughput by 20%. Consumer behavior reflects regulatory-driven demand for explainable compliance data, particularly in automotive and telecommunications sectors.

Asia-Pacific ranks second in market volume with a 27% share in 2024. Top consuming countries include China (12%), India (7%), and Japan (6%). The region is expanding infrastructure for automotive and electronics manufacturing, supported by innovation hubs in Shanghai, Bangalore, and Tokyo. Technological trends include cloud-based test data management and AI-powered interference analysis. Keysight Technologies China implemented real-time EMC simulation for industrial IoT devices, reducing test cycle time by 15%. Consumer behavior in Asia-Pacific shows growth driven by e-commerce adoption, mobile AI apps, and smart home electronics compliance.

South America holds a 12% market share, led by Brazil (6%) and Argentina (3%). Infrastructure expansion in energy, telecom, and automotive sectors is fueling EMC testing demand. Government incentives support local certification facilities and trade partnerships with international labs. A Brazilian electronics company recently installed a full-spectrum EMC test chamber, improving testing efficiency by 14%. Regional consumer behavior indicates demand tied to media localization, automotive electronics, and industrial equipment compliance, particularly in Brazil and Argentina.

Middle East & Africa accounts for 10% of the EMC testing market, with major growth in UAE (4%) and South Africa (3%). Demand is driven by oil & gas, construction, and defense sectors. Technological modernization includes high-frequency radiated testing and remote test monitoring. Local regulations mandate EMC certification for imported electronics, prompting infrastructure investment. Intertek Middle East recently launched enhanced EMC testing services in Dubai, reducing test cycle duration by 12%. Regional consumer behavior highlights adoption in industrial and government procurement, with increasing focus on compliance and reliability.

United States – 25% Market Share: Strong end-user demand across automotive, aerospace, and consumer electronics.

China – 12% Market Share: High production capacity with rapid adoption in automotive and electronics manufacturing.

The Electromagnetic Compatibility (EMC) Testing Market exhibits a moderately fragmented competitive environment with over 75 active global competitors operating across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The top five companies—including Keysight Technologies, TUV Rheinland, Intertek Group, UL Solutions, and Bureau Veritas—together account for approximately 42% of total market activity. Strategic initiatives such as partnerships with OEMs, launch of advanced automated test systems, facility expansions, and mergers are shaping competitive positioning. Innovation trends focus on AI-powered interference detection, high-frequency radiated testing, and cloud-enabled test data management. Companies are investing in digital transformation, automation of EMC test chambers, and predictive compliance analytics. Regional differences are evident: North America emphasizes aerospace and automotive testing, Europe prioritizes regulatory compliance for telecommunications and medical devices, and Asia-Pacific invests heavily in electronics and automotive production. The market’s competitive landscape is influenced by ongoing technological upgrades, sustainability-driven testing solutions, and increasing regulatory enforcement, driving firms to differentiate through speed, accuracy, and end-to-end service offerings.

UL Solutions

Bureau Veritas

SGS

Nemko

Eurofins Scientific

DEKRA

Applus+

Current and emerging technologies are fundamentally transforming EMC testing across industries. Automated test chambers with integrated robotics and AI-powered signal analysis are reducing test cycle times by up to 20% while enhancing measurement accuracy. High-frequency radiated and conducted testing equipment allows evaluation of devices operating in GHz-range applications, including 5G, automotive radar, and IoT systems. Cloud-based test data management and simulation platforms enable remote monitoring, real-time analysis, and predictive maintenance. Digital twins of products are increasingly employed to simulate interference scenarios before physical testing, improving operational efficiency. Modular EMC test setups now allow simultaneous multi-device testing, supporting large-scale automotive and consumer electronics production lines. Companies are also exploring eco-friendly test materials and energy-efficient chamber designs to comply with sustainability initiatives. Additionally, the integration of machine learning algorithms for anomaly detection enables early identification of electromagnetic interference risks, reducing downtime and ensuring regulatory compliance. These technologies collectively optimize testing throughput, accuracy, and cost-efficiency while aligning with global digital transformation trends.

In February 2024, Keysight Technologies launched a new AI-driven EMC test system capable of analyzing over 1,500 frequency bands simultaneously, reducing manual analysis time by 30%. Source: www.keysight.com

In August 2023, TUV Rheinland expanded its EMC testing laboratory in Germany with advanced high-frequency measurement equipment, enabling evaluation of automotive radar and IoT devices with 25% faster throughput. Source: www.tuv.com

In January 2024, Intertek Group introduced a cloud-based EMC test data management platform that allows clients to access real-time test results from multiple locations, improving operational efficiency by 18%. Source: www.intertek.com

In November 2023, UL Solutions integrated predictive interference analytics into its EMC testing services for consumer electronics, enabling early detection of potential compliance issues in over 500 device models annually. Source: www.ul.com

The Electromagnetic Compatibility Testing Market Report provides a comprehensive overview of the global market, spanning product types, applications, end-users, and geographic regions. It covers all key testing methodologies, including radiated and conducted EMC testing, automated test systems, and AI-enabled analytics platforms. The report examines critical applications across automotive, aerospace, defense, consumer electronics, medical devices, and industrial equipment. End-user analysis includes manufacturers, OEMs, and service providers adopting EMC testing for compliance, safety, and performance validation. Regional coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting market volume, infrastructure trends, technological adoption, and regulatory frameworks.

Additionally, emerging segments such as IoT device testing, 5G-enabled systems, and electric vehicle EMC assessments are analyzed. The report provides decision-makers with actionable insights into competitive positioning, technology trends, investment patterns, and strategic initiatives, offering a clear understanding of the market’s scope, future outlook, and opportunities for innovation and growth across all industry sectors.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 284.0 Million |

| Market Revenue (2032) | USD 480.7 Million |

| CAGR (2025–2032) | 6.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Inisghts

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Keysight Technologies, TUV Rheinland, Intertek Group, UL Solutions, Bureau Veritas, SGS, Nemko, Eurofins Scientific, DEKRA, Applus+ |

| Customization & Pricing | Available on Request (10% Customization is Free) |