Reports

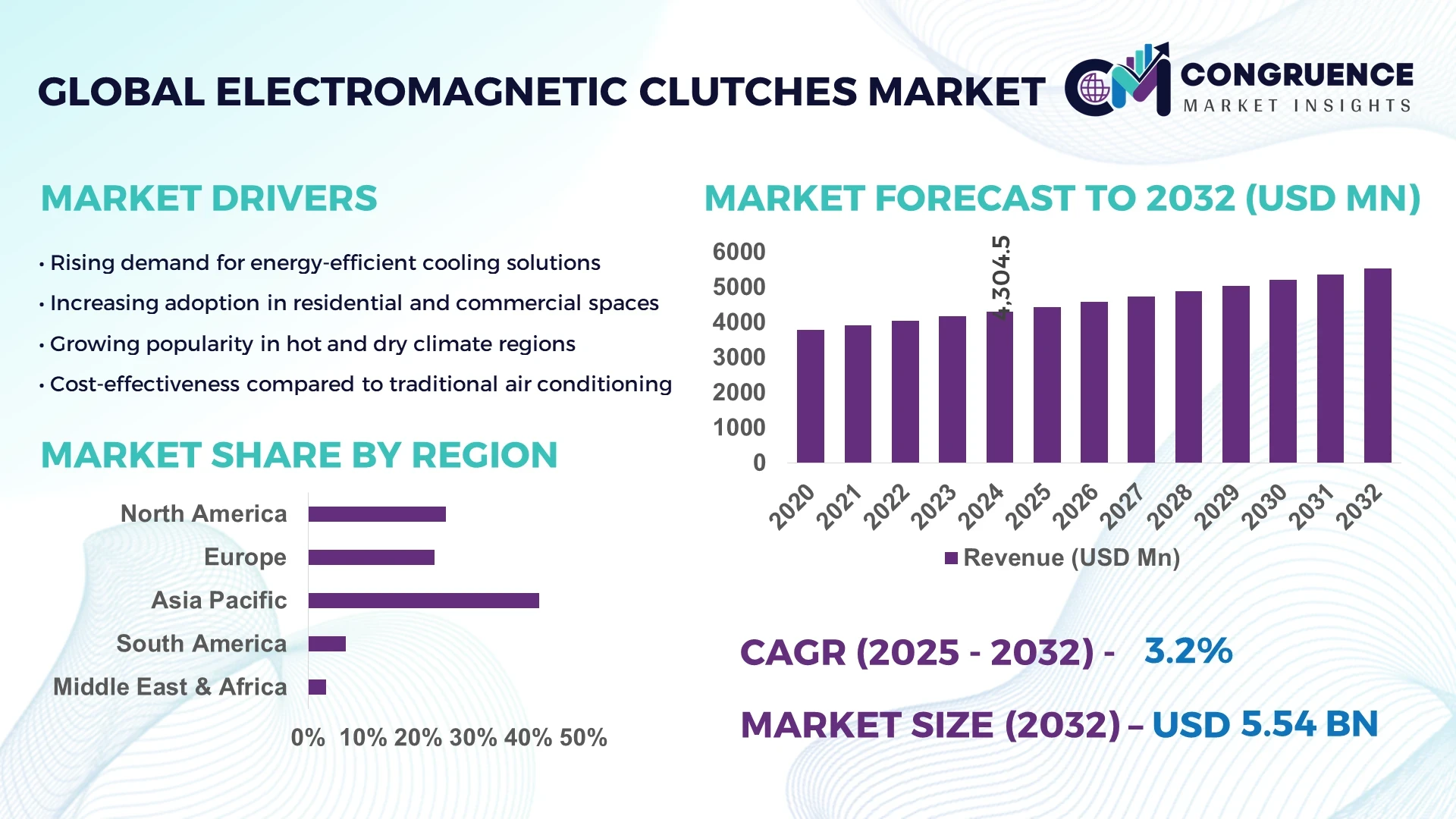

The Global Electromagnetic Clutches Market was valued at USD 4,304.47 Million in 2024 and is anticipated to reach USD 5,538.05 Million by 2032 expanding at a CAGR of 3.2% between 2025 and 2032.

China maintains a commanding position in production capacity with advanced electromagnetic clutch manufacturing facilities supported by robust investment in specialized materials and automated production lines. It demonstrates strong capabilities in producing clutch systems for automotive drivetrains, heavy industrial machinery, and high-precision automation equipment through the integration of modern thermal management technologies and intelligent control modules.

The market encompasses automotive, industrial machinery, machine tools, HVAC, and aerospace applications. Automotive demand remains a key driver with clutches deployed in drivetrain mechanisms, HVAC compressors, and engine accessories while industrial automation and robotic machinery also exhibit rising adoption. Recent innovations focus on energy-efficient clutch designs featuring enhanced torque capacity, reduced friction interfaces, and modular wet and dry clutch assemblies optimized for durability. The integration of smart sensors enables real-time monitoring of vibration, temperature, and torque data enhancing predictive maintenance and overall system efficiency. Regulatory requirements for emission reduction and energy conservation continue to accelerate adoption while economic drivers emphasize operational performance and cost optimization. Regional demand varies with Asia Pacific experiencing strong consumption due to industrial expansion whereas North America and Europe focus on advanced precision-oriented clutch platforms. Emerging developments include compact clutches for robotics and electric vehicles, embedded analytics supporting predictive maintenance, and integration into smart factory frameworks shaping the future of the Electromagnetic Clutches Market.

Artificial intelligence is transforming the Electromagnetic Clutches Market by introducing predictive intelligence, enhanced operational resilience, and faster product innovation. AI-enabled predictive maintenance leverages continuous data from torque sensors, thermal monitors, and vibration detectors to identify early signs of clutch wear and initiate proactive maintenance strategies. This approach reduces unexpected downtime, extends equipment life, and aligns with industry priorities for cost reduction and reliability.

Edge AI applications are bringing intelligence directly to clutch components by processing real-time data locally rather than relying on cloud systems. These solutions enable instant fault detection including overheating, misalignment, and torque irregularities even in environments with limited connectivity. As a result industries benefit from lower latency, improved system responsiveness, and more reliable operations under harsh conditions such as heavy vibration and high dust exposure.

Artificial intelligence is also redefining research and development by enabling simulation platforms that predict magnetic flux distribution, mechanical stress points, and heat dissipation efficiency. This capability shortens design cycles, reduces prototype requirements, and accelerates product launches. Engineers can optimize coil structures, materials, and cooling strategies through AI-assisted modeling improving both performance and cost efficiency. By combining predictive diagnostics, embedded analytics, and advanced design simulations the Electromagnetic Clutches Market is moving toward intelligent, adaptive, and high-performance solutions supporting Industry 4.0 manufacturing environments.

“In 2025 a global manufacturer introduced an AI-driven diagnostic module for electromagnetic clutches capable of detecting overheating and wear with 95 percent accuracy in under five seconds which lowered unplanned maintenance incidents by 25 percent during pilot implementation.”

The Electromagnetic Clutches Market is characterized by steady advancements in automotive systems, industrial automation, and machine tool technologies that collectively shape demand patterns. Increasing adoption of automation in sectors such as packaging, robotics, and heavy machinery is driving wider usage of electromagnetic clutches due to their precision control, high torque transfer efficiency, and reliability in variable operating conditions. The growing demand for energy-efficient equipment, coupled with stricter emission and environmental compliance requirements, further influences the market landscape. Additionally, technological innovation in clutch materials, smart sensor integration, and miniaturized designs for emerging electric vehicle applications are redefining industry standards. Regional consumption is diverse, with Asia Pacific demonstrating robust industrial uptake, while North America and Europe lead in precision-driven, sensor-enabled clutch systems.

The accelerating shift toward industrial automation is a significant driver of the Electromagnetic Clutches Market. Modern factories increasingly deploy automated machinery for processes such as assembly, material handling, and robotics, all of which require precise torque control and efficient power transmission. Electromagnetic clutches provide high responsiveness and reliability, making them integral to automation frameworks. According to industry figures, global investment in smart manufacturing technologies continues to rise annually, and clutch systems optimized with intelligent controls are seeing wider adoption. This trend strengthens demand in key sectors including automotive production lines, CNC machine tools, and packaging systems, ensuring sustained growth of the market.

The elevated cost of producing advanced electromagnetic clutches presents a restraint in the market, particularly for small and mid-sized enterprises with limited capital. High-performance clutches designed with intelligent sensors, enhanced heat dissipation mechanisms, and specialized materials significantly increase production costs. These expenses raise the upfront investment for end users and may delay adoption in cost-sensitive industries. Additionally, maintenance and replacement of sophisticated clutch systems add further expenses throughout the lifecycle. While large-scale industrial operators may absorb these costs to gain operational advantages, smaller businesses often face budget constraints, limiting overall market penetration and adoption of cutting-edge technologies.

The transition toward electric vehicles presents substantial opportunities for the Electromagnetic Clutches Market. As EVs demand compact, lightweight, and energy-efficient components, electromagnetic clutches are increasingly being designed for auxiliary systems such as HVAC compressors, battery cooling units, and drivetrain modules. With global EV production scaling rapidly, manufacturers are investing in miniaturized clutch solutions that offer high torque density and low energy consumption. Integration of predictive maintenance features and sensor-enabled diagnostics further enhances performance reliability in electric platforms. This shift aligns with government incentives and industry goals to reduce emissions, opening new growth avenues for clutch manufacturers focused on advanced automotive solutions.

One of the key challenges for the Electromagnetic Clutches Market lies in the complexity of integrating clutches into interconnected, smart manufacturing environments. Industry 4.0 demands seamless communication between machines, sensors, and control systems, requiring clutches to incorporate embedded electronics and real-time data interfaces. Developing such advanced systems increases design and engineering complexity, requiring multidisciplinary expertise in electronics, mechanics, and software. Moreover, ensuring compatibility with various industrial communication protocols and maintaining cybersecurity standards adds to implementation challenges. These factors elevate both time and cost for deployment, presenting obstacles for manufacturers striving to align clutch systems with modern smart factory requirements.

• Adoption of Modular and Prefabricated Construction: The growing adoption of modular construction methods is influencing demand for precision-driven electromagnetic clutches in automated machinery used for cutting, bending, and assembly operations. Prefabrication reduces on-site labor requirements by as much as 30% while accelerating construction timelines in sectors such as residential housing and commercial infrastructure. Europe and North America are seeing notable demand for automated equipment incorporating electromagnetic clutches, supporting efficiency in large-scale prefabrication projects.

• Integration of Smart Sensors and Predictive Maintenance: A measurable trend in the Electromagnetic Clutches Market is the widespread integration of smart sensors designed to monitor torque, temperature, and vibration. These sensors enable predictive maintenance practices that reduce unplanned downtime by up to 25% and extend the operational lifespan of clutches. Adoption is expanding across automotive production lines and industrial automation systems, where continuous monitoring ensures optimal performance and cost savings.

• Expansion in Electric Vehicle Applications: Electromagnetic clutches are increasingly incorporated into auxiliary electric vehicle systems such as HVAC compressors, drivetrain modules, and cooling systems. Global EV production growth has led to rising demand for compact, energy-efficient clutch designs that reduce power losses while maintaining torque efficiency. Lightweight designs combined with sensor-enabled diagnostics are gaining prominence, providing opportunities for manufacturers to diversify into the EV sector.

• Miniaturization for Robotics and Precision Machinery: Miniaturized electromagnetic clutches are experiencing accelerated demand in robotics and precision engineering due to their ability to deliver controlled torque in compact systems. Industrial robots, medical devices, and packaging equipment are adopting smaller clutches with high torque-to-size ratios, enabling space efficiency without compromising performance. This trend is particularly pronounced in Asia Pacific, where rapid automation in manufacturing and electronics assembly drives adoption of compact clutch solutions.

The Electromagnetic Clutches Market is segmented by type, application, and end-user categories, reflecting diverse industry needs and technology adoption trends. By type, the market includes dry, wet, and hybrid clutches with distinct performance advantages for varied operating environments. Applications span across automotive drivetrains, industrial machinery, robotics, aerospace systems, and HVAC compressors, with each segment contributing to overall market expansion. End-user insights reveal significant consumption from automotive OEMs, manufacturing firms, and aerospace operators, alongside rising adoption in energy and robotics sectors. This segmentation highlights the importance of product innovation and customization, ensuring clutch solutions align with evolving industry requirements.

Dry electromagnetic clutches represent the leading type owing to their simplicity, cost efficiency, and wide adoption across automotive and general industrial applications. They offer rapid engagement and low maintenance requirements, making them highly preferred in passenger vehicles and light industrial machinery. Wet clutches, while slightly more complex, are gaining traction as the fastest-growing type due to their ability to handle higher torque levels and superior cooling performance, particularly in heavy-duty applications and electric vehicle systems. Hybrid clutches, combining both wet and dry features, are carving a niche by offering optimized torque transmission for specialized industries such as aerospace and robotics. Other types, including compact and miniature designs, serve niche requirements in precision machinery and medical devices, highlighting the market’s adaptability to varied operating conditions.

Automotive applications dominate the Electromagnetic Clutches Market as these clutches are integral to vehicle drivetrains, HVAC compressors, and power steering systems. The demand is particularly strong in passenger and commercial vehicles, driven by growing electrification and enhanced comfort features. Industrial machinery represents the fastest-growing application segment, supported by the adoption of automation in manufacturing, robotics, and material handling equipment where clutches ensure precise torque control. Aerospace applications, though smaller in scale, continue to expand as electromagnetic clutches are utilized in actuation systems and auxiliary components requiring reliability under high-performance conditions. Additional applications in HVAC systems and marine equipment also contribute to overall market diversity, with energy efficiency and durability being primary decision factors.

Automotive manufacturers remain the leading end-user group within the Electromagnetic Clutches Market due to their large-scale consumption in drivetrains, engine accessories, and auxiliary vehicle systems. This segment is supported by continuous advancements in vehicle electrification and demand for high-efficiency clutch systems. The fastest-growing end-user segment is industrial automation, where rising investment in robotics, packaging machinery, and smart factories is accelerating the need for responsive and durable clutch solutions. Aerospace operators also play a critical role as they require high-precision clutch systems for safety-critical components. Additional end-users include marine and energy sectors, where clutches are deployed in propulsion systems and power generation equipment. Together, these diverse end-user groups highlight the extensive application versatility and strategic importance of electromagnetic clutches across global industries.

Asia-Pacific accounted for the largest market share at 42% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 3.8% between 2025 and 2032.

Asia-Pacific benefits from large-scale industrial expansion, robust automotive production, and significant investments in automation technologies. The presence of advanced manufacturing hubs in China, Japan, and India drives high consumption of electromagnetic clutches across diverse sectors including automotive, aerospace, and heavy machinery. Meanwhile, North America’s rapid digital transformation and integration of AI-driven predictive maintenance solutions in industrial systems position it as the fastest-expanding regional market.

High Adoption of Intelligent Power Transmission Solutions

North America accounted for 25% of the global Electromagnetic Clutches Market in 2024, with demand led by automotive OEMs, aerospace manufacturers, and industrial automation companies. The region’s regulatory framework encouraging energy-efficient technologies and reduced emissions has accelerated adoption of advanced clutch systems. Technological advancements such as smart clutches integrated with IoT-enabled monitoring are being widely deployed across high-performance automotive applications. Government support for automation in manufacturing further strengthens market prospects, while strong investments in defense and aerospace fuel specialized clutch demand. Digital transformation, particularly in predictive maintenance platforms, is enabling industries to optimize system performance and reliability.

Emphasis on Sustainability and Precision Engineering

Europe held a 20% market share in 2024, with Germany, the United Kingdom, and France representing the largest consumers of electromagnetic clutches. Strong focus on industrial automation and stringent EU sustainability directives have driven the adoption of energy-efficient clutch systems. Advanced machine tool manufacturing and robotics sectors continue to push demand for compact and high-torque clutches. European regulations promoting eco-friendly technologies encourage integration of clutches that support reduced energy consumption and compliance with carbon-reduction goals. The adoption of Industry 4.0 practices, including predictive analytics and smart control integration, is further shaping clutch applications in the region’s precision-oriented industries.

Industrial Expansion and Advanced Automotive Demand Driving Growth

Asia-Pacific dominated the market with 42% share in 2024, led by high consumption in China, Japan, and India. Strong infrastructure growth and robust automotive manufacturing output are central to this dominance. China is a hub for large-scale production with advanced automation technologies, while Japan focuses on robotics and high-precision engineering. India’s expanding automotive and construction equipment industries also drive strong demand. Regional innovation hubs are investing heavily in R&D for compact clutch designs suited for electric vehicles and smart manufacturing applications. The combination of industrial expansion and technology integration keeps the region at the forefront of market development.

Infrastructure Development and Energy Investments Boosting Demand

South America accounted for 6% of the global Electromagnetic Clutches Market in 2024, with Brazil and Argentina leading demand. Expanding infrastructure development projects and rising investments in renewable energy generation are contributing to adoption of electromagnetic clutches across construction and power equipment. Government initiatives to modernize transportation systems are creating additional demand for advanced clutches in automotive and industrial applications. Brazil, in particular, is driving uptake through its growing automotive and agricultural machinery sectors, while Argentina shows demand in energy infrastructure upgrades. Trade policies supporting industrial equipment imports also strengthen growth prospects in the region.

Oil & Gas Expansion and Smart Construction Driving Modernization

The Middle East & Africa represented 7% of the global Electromagnetic Clutches Market in 2024, with demand concentrated in the UAE, Saudi Arabia, and South Africa. The oil and gas industry continues to be a critical driver, requiring advanced clutches for drilling and extraction equipment. Large-scale infrastructure development projects, such as smart cities and transport hubs, are also supporting clutch adoption in construction machinery. Regional modernization strategies are accelerating integration of advanced automation technologies, while trade partnerships facilitate access to high-performance clutch components. Local regulations encouraging industrial efficiency further stimulate investment in modern clutch systems.

China – 28% market share: Strong production capacity and advanced manufacturing infrastructure drive dominance in the Electromagnetic Clutches Market.

United States – 18% market share: High demand from automotive, aerospace, and industrial automation sectors ensures continued leadership in clutch adoption.

The Electromagnetic Clutches Market is highly competitive, with over 50 active global and regional manufacturers operating across automotive, industrial automation, aerospace, and precision machinery sectors. Competition is driven by technological innovation, product customization, and expansion into emerging applications such as electric vehicles and robotics. Leading players are positioning themselves through strategic partnerships with automotive OEMs, industrial equipment suppliers, and automation integrators to secure long-term supply agreements. Product innovation is a central focus, with companies developing energy-efficient wet and dry clutches, sensor-integrated models for predictive maintenance, and compact solutions designed for lightweight machinery. Mergers and acquisitions are reshaping the competitive landscape as established firms seek to strengthen their global footprint and enhance R&D capabilities. Increasing investment in digital transformation, including AI-powered design optimization and embedded condition monitoring systems, has intensified rivalry. The market is also witnessing heightened regional competition, particularly in Asia-Pacific, where domestic manufacturers are rapidly scaling operations to challenge established international brands.

Ogura Industrial Corporation

Altra Industrial Motion

Kendrion N.V.

Ortlinghaus Group

Miki Pulley Co., Ltd.

Mitsubishi Electric Corporation

Carlyle Johnson Machine Company

Nexen Group, Inc.

Magtrol, Inc.

Thomson Industries, Inc.

Electromagnetic clutches are undergoing significant technological advancements, driven by increasing demand for high-performance solutions across automotive, aerospace, robotics, and industrial automation sectors. A major focus is on developing energy-efficient designs that optimize torque transmission while reducing power consumption. For instance, modern clutches are now being integrated with high-efficiency magnetic materials that enhance torque density without increasing size, meeting the growing need for compact machinery in electric vehicles and industrial robots. Another important trend is the incorporation of smart technologies such as embedded sensors and IoT connectivity. Sensor-based clutches allow real-time monitoring of wear, temperature, and torque, enabling predictive maintenance and minimizing downtime in critical applications. With over 60% of new industrial machinery adopting condition-monitoring systems by 2024, sensor integration is emerging as a key differentiator in the market.

Lightweight materials, such as advanced composites and aluminum alloys, are increasingly used to reduce clutch weight while maintaining structural integrity. This shift is particularly relevant in aerospace applications, where weight reduction directly contributes to fuel efficiency. Wet clutches are being engineered with advanced cooling systems to support high-speed, continuous-duty operations in demanding industries. In addition, modular clutch designs are gaining traction, offering customization flexibility for varied torque and speed requirements. Combined with digital simulation tools like finite element analysis (FEA), manufacturers are achieving more precise product development cycles, enhancing performance while lowering prototyping costs. Collectively, these technologies are reshaping the competitiveness of the electromagnetic clutches market.

• In January 2023, Ogura Industrial expanded its product line with the development of high-torque electromagnetic clutches for electric mobility applications. These clutches were engineered to deliver 15% higher torque capacity while maintaining compact dimensions, addressing the growing requirements of electric two-wheelers and compact EVs.

• In July 2023, Kendrion N.V. introduced an advanced series of electromagnetic clutches integrated with smart sensors for industrial automation systems. The launch aimed to improve real-time performance monitoring and predictive maintenance, reducing downtime by up to 20% in high-speed machinery operations.

• In March 2024, Ortlinghaus Group announced the launch of a next-generation wet-running electromagnetic clutch designed for heavy-duty industrial presses. The new clutch incorporated enhanced thermal management, enabling longer continuous-duty cycles and improved durability under extreme operational loads.

• In May 2024, Miki Pulley Co., Ltd. unveiled a compact electromagnetic clutch series tailored for robotics and precision machinery. Featuring reduced inertia and faster response times, the new line was optimized for collaborative robots and automated guided vehicles, addressing demand for high-precision torque control.

The Electromagnetic Clutches Market Report provides a comprehensive assessment of the industry across multiple dimensions, including product types, applications, technologies, and geographic regions. The scope encompasses dry, wet, and hybrid clutch types, with detailed insights into their adoption across automotive systems, industrial machinery, aerospace equipment, robotics, and energy-related applications. The analysis highlights leading as well as emerging application areas, covering both traditional uses such as automotive transmissions and industrial automation, along with fast-growing segments like electric vehicles, collaborative robots, and renewable energy systems.

From a regional perspective, the report examines market performance in North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing both established industrial economies and high-growth emerging markets. Detailed regional insights are included to illustrate production hubs, consumption patterns, and regulatory or technological influences shaping adoption. For instance, Asia-Pacific is highlighted for its manufacturing-driven demand, while Europe focuses on sustainability-oriented innovations.

The report also outlines technological progress, including IoT-enabled monitoring systems, lightweight material usage, modular clutch design, and advancements in thermal management for wet clutches. Industry-specific dynamics are included, with emphasis on automotive OEMs, aerospace companies, robotics developers, and energy infrastructure providers. By covering segmentation by type, application, end-user, and geography, the report offers decision-makers a 360-degree view of the market landscape, identifying both core areas of strength and untapped opportunities for future investment.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 4304.47 Million |

|

Market Revenue in 2032 |

USD 5538.05 Million |

|

CAGR (2025 - 2032) |

3.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Ogura Industrial Corporation, Altra Industrial Motion, Kendrion N.V., Ortlinghaus Group, Miki Pulley Co., Ltd., Mitsubishi Electric Corporation, Carlyle Johnson Machine Company, Nexen Group, Inc., Magtrol, Inc., Thomson Industries, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |