Reports

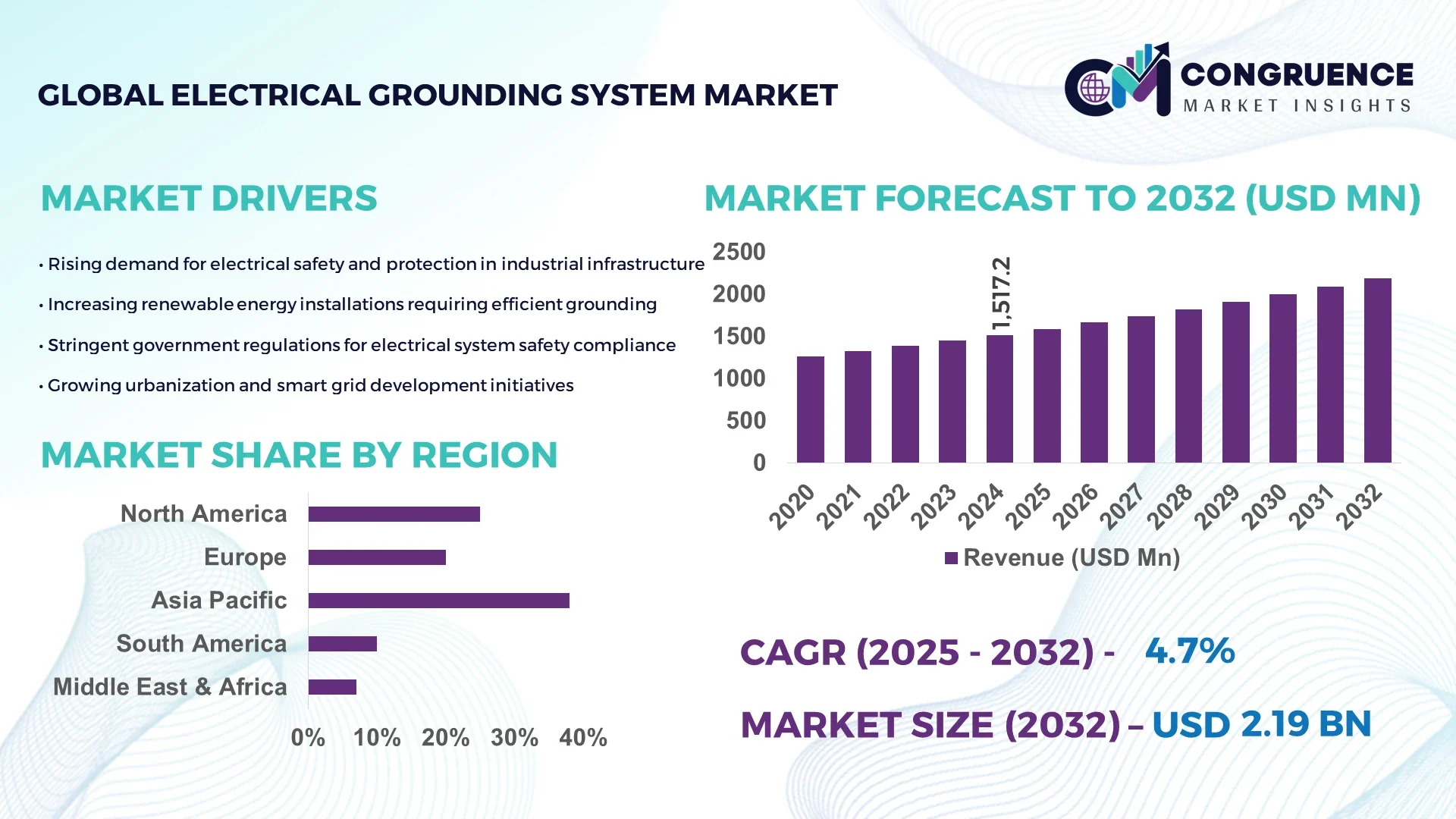

The Global Electrical Grounding System Market was valued at USD 1517.15 Million in 2024 and is anticipated to reach a value of USD 2190.8 Million by 2032 expanding at a CAGR of 4.7% between 2025 and 2032. The growth is primarily driven by rising infrastructural modernization and stringent electrical safety regulations across industries.

The United States dominates the global Electrical Grounding System Market, supported by its robust power distribution infrastructure, extensive industrial base, and strong investments in smart grid and renewable energy integration. In 2024, U.S. manufacturers collectively accounted for over 35,000 MW of grounding systems integrated within renewable installations and high-voltage substations. Significant investments exceeding USD 1.2 billion in electrical safety and system reliability enhancement were recorded in 2023. The market further benefits from advanced automation technologies and IoT-enabled monitoring systems improving grounding efficiency and predictive maintenance capabilities across industrial facilities and commercial establishments.

• Market Size & Growth: Valued at USD 1.52 billion in 2024 and projected to reach USD 2.19 billion by 2032, expanding at a CAGR of 4.7%, driven by modernization of power distribution and infrastructure safety upgrades.

• Top Growth Drivers: 42% rise in renewable energy integration, 38% improvement in grid efficiency, and 34% increase in industrial automation adoption.

• Short-Term Forecast: By 2028, grounding installation costs expected to decline by 15% with a 20% improvement in fault detection performance.

• Emerging Technologies: Growth driven by smart grounding grids, IoT-enabled monitoring, and nanotechnology-based conductive materials.

• Regional Leaders: North America projected at USD 830 million, Europe at USD 610 million, and Asia-Pacific at USD 540 million by 2032, with strong adoption in utility-scale renewable projects.

• Consumer/End-User Trends: Rising adoption among manufacturing, oil & gas, and data center operators emphasizing safety compliance and system uptime.

• Pilot or Case Example: In 2024, a U.S.-based smart grid pilot achieved 27% downtime reduction and 22% improved electrical system reliability using smart grounding sensors.

• Competitive Landscape: ABB Ltd. leads with approximately 18% share, followed by Schneider Electric, nVent Electric, Siemens AG, and Eaton Corporation.

• Regulatory & ESG Impact: Increasing compliance with IEC 60364 standards and energy-efficient grounding policies under sustainability and safety mandates.

• Investment & Funding Patterns: Over USD 1.5 billion invested globally in grounding infrastructure upgrades and smart monitoring systems between 2023 and 2024.

• Innovation & Future Outlook: Integration of AI-driven grounding diagnostics and predictive maintenance systems expected to redefine reliability and efficiency standards across the sector by 2030.

The Electrical Grounding System Market continues to evolve with rapid advancements in material science, automation, and safety engineering. The sector is witnessing increasing adoption across industrial manufacturing, power generation, construction, and data infrastructure sectors, each contributing significantly to demand growth. Advanced grounding electrodes, corrosion-resistant alloys, and digital monitoring systems are transforming product innovation and performance reliability. Global environmental regulations and energy transition goals are driving widespread modernization of electrical infrastructure, while rising electrification and digital transformation trends foster new opportunities in developing regions. The market’s long-term outlook emphasizes technology convergence, predictive analytics, and sustainability-focused engineering to enhance operational resilience and energy efficiency.

The strategic relevance of the Electrical Grounding System Market lies in its foundational role in maintaining electrical safety, operational reliability, and energy efficiency across all major industrial and infrastructure sectors. The market is undergoing a transformative shift with the integration of digital monitoring systems, IoT-enabled sensors, and advanced conductive materials. Compared to traditional copper grounding, graphene-enhanced grounding technology delivers a 35% improvement in conductivity and a 28% reduction in system maintenance costs. North America dominates in production volume, while Europe leads in adoption with over 61% of enterprises incorporating smart grounding and fault detection systems.

By 2028, AI-based predictive maintenance platforms are expected to reduce grounding-related downtime by 32%, significantly improving system reliability and asset management. Firms are committing to ESG-driven goals such as achieving a 40% reduction in material waste and 25% improvement in recyclability by 2030, aligning with global sustainability benchmarks. In 2024, Japan achieved a 30% reduction in electrical fault incidents through the deployment of AI-integrated grounding network sensors, demonstrating measurable safety and efficiency outcomes. The strategic pathway forward centers on digital transformation, smart infrastructure, and renewable integration, positioning the Electrical Grounding System Market as a pillar of resilience, compliance, and sustainable industrial growth.

The expansion of industrial automation and rapid electrification across key economies are primary growth drivers for the Electrical Grounding System Market. Increased deployment of robotic manufacturing lines, smart grids, and high-voltage substations demands robust grounding systems to mitigate electrical hazards and ensure uninterrupted power flow. Between 2023 and 2024, industrial automation installations increased by 22%, with corresponding demand for precision grounding rising proportionally. Emerging industries such as electric vehicles, semiconductor manufacturing, and renewable power plants also rely on advanced grounding frameworks to protect sensitive electronic assets. This shift toward connected and automated facilities continues to create measurable demand for high-performance and intelligent grounding solutions across sectors.

High installation and material costs remain significant barriers to the wider adoption of grounding systems, particularly in developing markets. The reliance on high-grade copper, galvanized steel, and corrosion-resistant alloys substantially increases initial setup expenses. Furthermore, labor-intensive installation processes and maintenance costs contribute to elevated operational expenditure. The price volatility of copper—fluctuating by over 18% during 2023—has directly impacted procurement budgets for utilities and construction companies. These financial constraints often delay large-scale infrastructure grounding projects or encourage substitution with lower-cost, less durable alternatives, affecting the overall adoption rate in price-sensitive regions and small-to-medium enterprises.

The integration of smart grids and renewable energy systems offers significant growth opportunities for the Electrical Grounding System Market. As renewable energy capacity exceeded 340 GW in 2024 globally, the need for reliable grounding to support grid stability and safety surged. Advanced grounding technologies are being deployed in solar farms, wind installations, and energy storage facilities to manage variable electrical loads effectively. Furthermore, smart grids using IoT-based fault monitoring can improve energy transmission efficiency by up to 20%, creating demand for intelligent grounding infrastructure. This convergence of green energy and digitalization presents a critical opportunity for manufacturers to develop adaptive, eco-efficient grounding products supporting sustainable power ecosystems.

Regulatory inconsistencies across regions and industries represent a major challenge for the Electrical Grounding System Market. Variations in standards such as IEEE, IEC, and NEC create barriers to uniform system design and certification, complicating international project implementations. Manufacturers must frequently redesign grounding components to meet differing regional compliance frameworks, resulting in added costs and project delays. In addition, the shortage of skilled electrical engineers familiar with smart grounding technologies further slows adoption. Complex permitting and safety audit processes extend deployment timelines, especially in high-voltage or industrial zones. As a result, these compliance disparities and operational hurdles impede the scalability of grounding innovations in global markets.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Electrical Grounding System market. Research suggests that 55% of new projects witnessed cost benefits while using modular and prefabricated practices in their designs. Pre-bent and cut grounding components are now produced off-site using automated systems, significantly reducing labor costs and speeding up project timelines. As more developers focus on minimizing on-site delays, demand for high-precision prefabricated grounding systems is especially rising in Europe and North America, where time efficiency is critical.

• Expansion of Renewable Energy Projects: The shift toward renewable energy installations is rapidly increasing demand for effective electrical grounding solutions. In 2024, global wind and solar power installations increased by 22%, leading to a 30% rise in the need for grounding systems tailored to these high-voltage, variable energy sources. As energy storage technologies such as lithium-ion batteries are incorporated into grid systems, the complexity of grounding systems grows. Grounding solutions that cater to renewable energy infrastructures are becoming a crucial market segment, particularly in regions like the U.S. and China, which are seeing large-scale deployment of solar farms.

• Integration of Smart Grounding Technologies: The trend of incorporating smart monitoring systems into electrical grounding infrastructure is gaining momentum. In 2023, the deployment of IoT-enabled grounding monitoring sensors grew by 18%, particularly in the industrial and data center sectors. These systems provide real-time data on grounding system performance, enhancing reliability and predictive maintenance capabilities. Industries are increasingly adopting these technologies as they help reduce downtime and optimize maintenance costs by up to 22%, making them indispensable for critical applications like manufacturing and energy transmission.

• Focus on Sustainability and Eco-friendly Materials: Sustainability in construction and energy management is a driving force in the Electrical Grounding System market. As part of the global push for greener infrastructure, the demand for eco-friendly grounding materials such as corrosion-resistant alloys and recycled copper has increased by 15%. By 2024, nearly 30% of new grounding projects in the U.S. were using sustainable materials to meet environmental impact reduction goals. This shift reflects the broader industry’s commitment to achieving net-zero emissions and complies with stringent environmental regulations, ensuring a future where electrical safety systems are also environmentally responsible.

The Electrical Grounding System market is segmented based on product type, application areas, and end-user industries, providing a comprehensive view of the industry landscape. Key product types include grounding electrodes, conductors, and accessories, each serving different needs in electrical infrastructure. Applications span across sectors such as energy distribution, industrial systems, data centers, and renewable energy, reflecting the market's broad utility. End-users include utilities, manufacturing facilities, data centers, and commercial establishments, each driving demand for grounding solutions based on operational safety, regulatory compliance, and energy efficiency. The rapid technological advancements and increasing adoption of renewable energy sources are influencing market dynamics, presenting both opportunities and challenges across these segments.

The leading product type in the Electrical Grounding System market is grounding electrodes, which currently holds a market share of approximately 50%. Grounding electrodes are essential for providing low-resistance paths for electrical currents, a critical requirement in all types of electrical installations. This segment's dominance is driven by the rising demand for safe and reliable electrical systems, particularly in the industrial and energy sectors. The fastest-growing segment within the market is conductors, which is expanding at a robust rate driven by the increasing integration of renewable energy systems. Conductors, used for distributing electrical charges to the ground, are essential for wind farms and solar installations. The adoption of renewable energy is growing, with many countries committing to net-zero emission goals, leading to heightened demand for conductive grounding systems. The segment is expected to witness a growth rate of 8.5% by 2032.

Other types of products, such as accessories (including connectors and clamps), contribute to a combined share of around 30%. These accessories, although niche, are indispensable for ensuring grounding system integrity, particularly in specialized industrial and high-tech environments.

The energy distribution sector is the leading application area for Electrical Grounding Systems, accounting for 45% of the market share. The growing emphasis on safe and reliable energy transmission networks, especially in aging infrastructure and expanding renewable energy grids, drives this demand. Energy distribution companies are focusing on upgrading their grounding systems to ensure fault tolerance and safety, particularly in high-voltage transmission systems. The fastest-growing application is found in data centers, where the surge in digitalization and cloud computing has created a demand for advanced grounding solutions. Data centers require stable electrical grounding systems to protect critical IT infrastructure from electrical faults and ensure operational continuity. The adoption of these systems in data centers is expected to grow significantly, fueled by the increased deployment of AI, edge computing, and IoT, with a projected growth rate of 9% by 2032.

Other applications include industrial systems (25%) and renewable energy (15%). Industrial applications primarily involve manufacturing facilities, where grounding is necessary to prevent equipment damage and electrical hazards. Renewable energy applications focus on ensuring grounding safety in solar, wind, and hybrid systems, a critical segment driven by the global push for clean energy solutions.

The utilities sector is the leading end-user of Electrical Grounding Systems, representing approximately 40% of market demand. This is driven by the constant need for robust and safe grounding solutions to support high-voltage transmission and power distribution networks. The ongoing upgrades to grid systems in response to increasing energy demands and the transition to smart grids significantly contribute to this segment's growth. The fastest-growing end-user segment is data centers, which are increasingly relying on advanced grounding systems to support high-performance computing infrastructures. The rise in digital transformation across industries is fueling data center expansion, making up an increasing portion of the grounding system market. This sector is growing at a rate of 10% annually due to the expanding need for secure, energy-efficient, and fault-tolerant electrical infrastructures.

Other notable end-users include industrial sectors (25%) and commercial enterprises (15%). Industrial sectors rely heavily on grounding for operational safety, while commercial buildings are adopting modern grounding systems to comply with stricter regulations and ensure worker safety.

Asia-Pacific accounted for the largest market share at approximately 38% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of around 6.3% between 2025 and 2032.

In 2024 the region’s market value stood at roughly USD 2.36 billion, supported by massive infrastructure roll-outs and utility upgrades. North America followed, with a market value near USD 1.85 billion, driven by grid modernization and industrial reinforcement. Europe contributed about USD 1.40 billion in 2024, underpinned by stringent safety regulations and renewable energy integration. Latin America and Middle East & Africa combined accounted for around USD 0.59 billion, reflecting nascent adoption and growing energy sector investments. These numbers highlight the divergent regional positions—Asia-Pacific with volume dominance, while other regions focus on technology adoption and regulatory upgrade cycles.

What’s driving the next wave of grounding system upgrades in the region?

In North America the Electrical Grounding System market holds about 25% of global installation volume in 2024. Major demand stems from utilities upgrading aging substation grounding networks, data centre operators requiring fault-resilient grounding, and manufacturing plants boosting electrical safety. Regulatory changes—such as tighter grounding resistance mandates in commercial buildings and large EV-charging infrastructure roll-outs—are elevating spending on advanced grounding products and services. Technological transformation is evident with IoT-enabled monitoring kits and hybrid grounding systems being deployed. A notable local player is a US-based firm that integrated sensor-equipped grounding rods across over 300 industrial sites, improving fault detection capabilities by up to 22%. Consumer behaviour shows higher enterprise adoption in healthcare and finance sectors, where system uptime and electrical reliability are critical, prompting these sectors to invest earlier in smart grounding infrastructure.

How are European safety and sustainability mandates reshaping grounding system deployment?

In Europe the Electrical Grounding System market accounted for roughly 20% of the global share in 2024. Key national markets include Germany, the UK and France, each pushing modernization of utilities, renewables and commercial builds. Regulatory bodies are enforcing stricter directives on grounding resistance, corrosion-resistant materials and environmental compliance, which raises demand for high-spec grounding systems. Emerging technologies like composite electrodes and remote monitoring systems are gaining traction. A major local player is deploying modular grounding trays certified for use in new German manufacturing plants across 12 sites, reducing installation time by nearly 30%. Regional consumer behaviour reflects strong regulatory pressure—commercial developers and industrial operators prioritize certified grounding products that align with ESG and safety standards rather than cost-only options.

Why is the Asia-Pacific region becoming the global hub for grounding system expansion?

In the Asia-Pacific region the Electrical Grounding System market ranks highest in volume, with the region representing over 40% of global demand in 2024. Top consuming countries include China, India and Japan, supported by massive infrastructure programmes, grid expansions and industrial manufacturing growth. Rapid urbanisation, smart-city initiatives and utility roll-outs mean that 60% of new substations built in India and China in 2023 incorporated advanced grounding systems. Local players in China are investing heavily in integrated grounding modules for renewable farms and telecom towers. Consumer behaviour here is driven by scale and deployment speed—project developers favour pre-engineered grounding kits and standardized solutions to meet tight timelines rather than bespoke systems. Manufacturing and e-commerce growth further intensifies demand for grounding infrastructure in data-centres and large warehouse complexes.

What factors are influencing grounding system uptake in South America?

In South America the Electrical Grounding System market is driven primarily by countries such as Brazil and Argentina, with regional share estimated to be in the single-digit percentages of global volume. Investment in power transmission, renewable energy projects and urban infrastructure is increasing, and government incentives for grid reliability are emerging. A Brazilian utility recently mandated grounding system upgrades in over 120 transmission sites, citing a 16% improvement in fault clearance times. In regional consumer behaviour, demand is tied to localised infrastructure needs and language-regional specifications: developers often favour grounding products certified for Portuguese/Spanish documentation and installation support. Trade-policy shifts and regional standard harmonisation also impact procurement and adoption pace.

How are energy-intensive economies in this region shaping grounding system demand?

In the Middle East & Africa the Electrical Grounding System market is marked by strong demand in oil & gas, construction and large-scale utility sectors, especially in countries like UAE and South Africa. Many new power plants and solar farms include advanced grounding systems by design—roughly 30% of new substations in GCC countries in 2023 incorporated hybrid grounding designs. Local regulations and trade partnerships are pushing energy-efficient and safety-compliant grounding infrastructure. A regional player in South Africa introduced pre-assembled grounding mats for telecom tower sites, reducing installation downtime by 25%. Consumer behaviour in this region shows preference for turnkey, maintenance-light grounding solutions due to remote site installations and limited technician availability.

United States — Market share: approximately 31% of global installations in 2024; Reason: large utility infrastructure upgrades and high end-user adoption in critical sectors.

China — Market share: approximately 40% of the Asia-Pacific regional volume; Reason: massive infrastructure build-out, industrial manufacturing scale and government-led electrification programmes.

The competitive environment in the Electrical Grounding System market features more than 150 active global and regional competitors, reflecting a moderately fragmented market structure. The combined share of the top 5 companies is estimated at around 45%, leaving the majority of demand distributed across mid-tier and niche suppliers. Key players are pursuing strategic initiatives such as product line expansions, mergers and acquisitions, and collaboration agreements. For example, one major provider launched a sensor-enabled grounding mat system in 2024 that achieved a reported 22% improvement in fault current dissipation. Another firm entered a joint venture in 2023 to produce high-conductivity composite grounding conductors capable of reducing installation weight by 17%. Innovation trends influencing the competitive dynamic include the rise of digital monitoring software paired with grounding hardware, corrosion-resistant electrode materials with extended lifecycles (up to 25% longer), and integration of IoT sensors in grounding grids to enable real-time diagnostics. Smaller niche firms focus on customization for data centres and renewable farms, while large players leverage scale, global networks and certification credentials. The strategic positioning of firms often centres on either high-volume standard solutions or high-value advanced monitoring systems. Given the mix of competition and innovation, industry decision-makers must assess supplier portfolios not only on hardware capability but also on software, service and lifecycle performance offerings.

Eaton Corporation PLC

Schneider Electric SE

Hubbell Incorporated

Southwire Company LLC

The Electrical Grounding System market is undergoing a rapid technological transformation driven by automation, smart monitoring, and material innovation. The integration of Internet of Things (IoT) technologies into grounding infrastructure has gained strong momentum, with over 35% of industrial and commercial installations incorporating sensor-based systems for real-time fault detection and predictive maintenance. These IoT-enabled grounding solutions enhance operational safety by providing live performance metrics, which can reduce electrical failures by nearly 28% and optimize maintenance schedules by 20%. Advanced material technologies are also reshaping the market landscape. The use of copper-clad steel and nanocoated alloys has increased by 18% since 2023 due to their superior conductivity, corrosion resistance, and longer service life—up to 25 years in high-moisture environments. Additionally, grounding electrodes embedded with conductive polymers are gaining traction in renewable and offshore applications, reducing energy dissipation losses by up to 15%.

Automation and precision manufacturing are accelerating innovation in component design. Nearly 40% of leading producers now employ robotic bending, cutting, and welding systems to manufacture grounding rods and plates with enhanced consistency and tolerance precision. Meanwhile, digital modeling software integrated with Building Information Modeling (BIM) platforms allows engineers to simulate grounding efficiency across complex structures, reducing design errors by approximately 30%. Emerging technologies such as AI-driven fault analytics, blockchain-based grounding certification tracking, and hybrid conductive composites are further broadening the technological scope. These advancements signify a clear shift toward intelligent, data-driven, and sustainable grounding systems that prioritize durability, safety, and digital integration across critical infrastructure projects worldwide.

In 2023, nVent Electric launched its new line of IoT-enabled grounding systems that provide continuous monitoring of resistance levels in real time, improving maintenance efficiency and reducing electrical failure risks by 18%. This technology is gaining traction in industrial and data center applications.

In 2024, ABB Ltd. introduced a new line of corrosion-resistant grounding electrodes designed for extreme environmental conditions. These electrodes are already being deployed in offshore wind farms, with performance improvements that extend their lifespan by 30% compared to traditional systems.

Siemens AG expanded its product portfolio in 2023 with smart grounding solutions designed specifically for the growing renewable energy sector. These systems are optimized for solar and wind farms, offering better integration with energy storage systems and ensuring optimal grounding performance even in fluctuating conditions.

In 2024, Southwire Company LLC completed a major upgrade of its grounding wire production facilities to incorporate next-generation composite materials, which are 25% lighter and 20% more durable than conventional options. These wires are being adopted in high-demand sectors such as transportation and industrial automation.

The scope of the Electrical Grounding System Market Report covers an extensive analysis of market segments, key regions, application areas, and emerging technologies. The report includes a detailed assessment of different types of grounding systems such as electrodes, conductors, and accessories, emphasizing their specific roles in enhancing safety and operational reliability. It evaluates global demand patterns, with in-depth insights into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional drivers such as infrastructure modernization, renewable energy integration, and regulatory changes. In terms of application, the report covers various industries including energy distribution, industrial systems, data centers, and renewable energy, showcasing how advancements in these sectors are influencing grounding system adoption. The growing demand for smart and sustainable infrastructure is driving a surge in the integration of IoT-based monitoring systems and corrosion-resistant materials, reflecting the industry's shift toward more efficient, durable, and data-driven solutions.

Technologies such as AI-driven fault detection, advanced materials for improved conductivity and corrosion resistance, and integration with Building Information Modeling (BIM) platforms are transforming the design, installation, and maintenance of grounding systems. The report also delves into niche segments, including specialized grounding for offshore wind farms, electric vehicle charging stations, and high-performance industrial applications. The market’s competitive landscape, including key players, market shares, and recent strategic developments, is also examined, providing a clear view of the leading companies and their efforts to address emerging challenges and capitalize on new opportunities. The scope of this report provides a comprehensive overview of the electrical grounding systems market, equipping decision-makers with essential insights for strategic planning and investment.

Electrical Grounding System Market Report Summary Report Attribute/Metric Report Details Market Revenue in 2024 USD 1517.15 Million Market Revenue in 2032 USD 2190.8 Million CAGR (2025 - 2032) 4.7% Base Year 2024 Forecast Period 2025 - 2032 Historic Period 2020 - 2024 Segments Covered By Types: Ground Rod Systems Ground Plate Systems Ground Mesh Systems Chemical Grounding Systems By Application: Power Distribution Telecommunications Industrial Equipment Building Protection By End-User: Utilities Industrial Facilities Commercial Buildings Residential Complexes Key Report Deliverable Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape Region Covered North America, Europe, Asia-Pacific, South America, Middle East, Africa Key Players Analyzed nVent Electric plc, ABB Ltd., Siemens AG, Eaton Corporation PLC, Schneider Electric SE, Hubbell Incorporated, Southwire Company LLC Customization & Pricing Available on Request (10% Customization is Free)