Reports

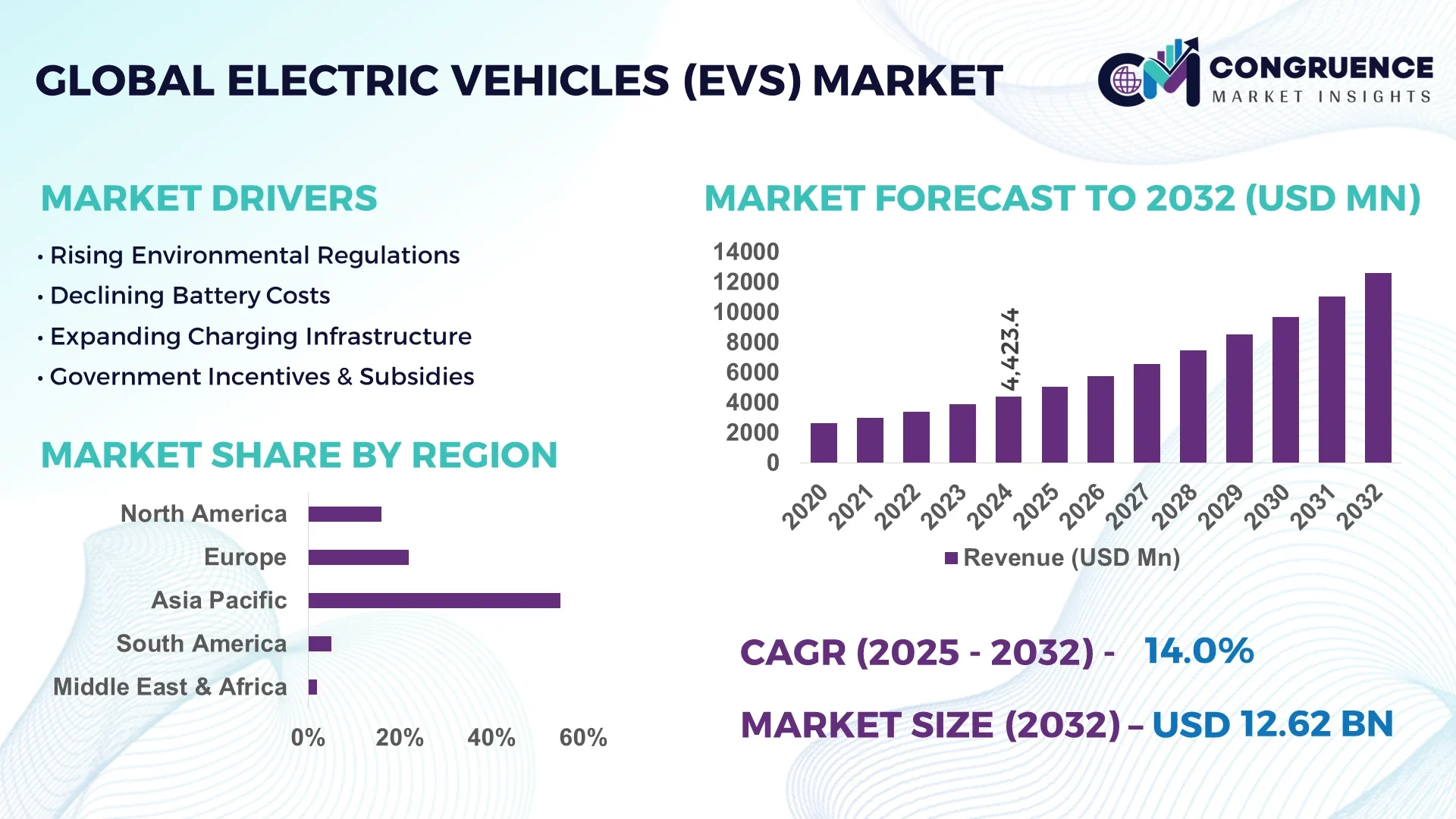

The Global Electric Vehicles (EVs) Market was valued at USD 4,423.4 Million in 2024 and is anticipated to reach a value of USD 12,618.1 Million by 2032 expanding at a CAGR of 14% between 2025 and 2032.

In China, the dominant country in the Electric Vehicles (EVs) Market, production capacity exceeds 10 million electric vehicles annually, supported by more than 300 gigawatt-hours of integrated battery cell manufacturing. China’s EV ecosystem has attracted over USD 60 billion in recent investment into fast-charging networks and electric powertrain R&D facilities. Advanced applications now include electric light-commercial vehicles for logistics and autonomous electric buses deployed in multiple smart-city pilot zones. Technological advancements such as high-energy-density solid-state batteries and vehicle-to-grid (V2G) integration are being piloted by leading automotive groups in the region, enabling bidirectional energy flow and connected charging systems.

The Electric Vehicles (EVs) Market spans several key industry sectors including passenger cars, light-commercial vehicles, two-/three-wheelers, and electric buses. Passenger cars represent the largest segment by unit volume, while electric buses dominate in terms of vehicle-to-vehicle utilization in public transport. Recent innovations feature next-generation bidirectional charging systems and integrated AI-based battery management modules that enhance thermal control and extend battery cycle life by up to 20%. Regulatory drivers include zero-emission vehicle mandates in urban centers and favorable tax incentives for fleet electrification, while economic stimulus packages in emerging economies promote low-cost EV assembly. Regional consumption patterns show accelerated adoption in East Asia and Europe, whereas India and Southeast Asia are benefiting from local assembly initiatives. Emerging trends include battery swapping networks, urban micro-mobility solutions like electric scooters tailored for congested cities, and the deployment of high-power megawatt charging stations for heavy-duty trucks. The future outlook points to convergence of EVs with clean-energy microgrids and smart infrastructure investments guided by digital twin modeling and predictive maintenance systems.

Artificial Intelligence (AI) is rapidly transforming the Electric Vehicles (EVs) Market by optimizing production, enhancing operational performance, and redefining user experience. In manufacturing plants, AI-powered predictive maintenance systems reduce unplanned downtime by up to 30%, thanks to early detection of equipment anomalies using sensor-based analytics. In battery production lines, AI algorithms optimize electrode coating processes, improving yield consistency by approximately 15% while reducing material waste. During vehicle operation, AI-driven energy optimization systems analyze real-time driving behavior and environmental conditions to adjust powertrain management, boosting efficiency and extending driving range by around 8–12%. AI-enabled fleet management platforms aggregate data from EVs to optimize route planning, charging schedules, and energy utilization, reducing operational costs for fleet operators by up to 18%. Furthermore, AI-enhanced in-vehicle interfaces provide predictive navigation and smart charging suggestions that align with grid demand and pricing, fostering more efficient energy usage patterns.

In the broader Electric Vehicles (EVs) Market, AI is also being employed in the design phase to run complex simulations of aerodynamic profiles and battery thermal behavior, accelerating development cycles by weeks. Supply-chain logistics benefit from AI-based forecasting, ensuring just-in-time delivery of components and minimizing inventory buffers. Vehicle-to-vehicle data networks leverage AI to share charging station utilization data, contributing to better infrastructure planning and reducing wait times at charging hubs. In summary, AI's integration across the Electric Vehicles (EVs) Market is fostering smarter manufacturing, more reliable operations, and user-centric smart mobility—with measurable gains in efficiency, productivity, and cost optimization.

“In 2024, an AI-driven battery management system deployed in fleet vehicles reduced average battery degradation by 18% over six months, using continuous monitoring and adaptive charging profiles.”

The Electric Vehicles (EVs) Market Dynamics reflect critical trends in innovation, infrastructure, and stakeholder engagement. Decision-makers observe shifting demand patterns toward electrified logistics and public transit, underpinned by compelling improvements in charging network density and grid integration. Key influences include technological convergence—such as AI, connectivity, and energy storage—alongside infrastructure modernization and regulatory alignment. Automakers are increasingly adopting modular EV platforms that simplify electrification across vehicle types. Procurement cycles now prioritize total-cost-of-ownership calculations, factoring in lower maintenance and energy costs. OEMs are collaborating with utilities to co-develop smart charging ecosystems that buffer peak load and enable dynamic pricing mechanisms. Additionally, consumer expectations of digital service ecosystems are shaping vehicle design, emphasizing over-the-air updates and mobile app-based user interfaces. In sum, market dynamics in the Electric Vehicles (EVs) Market are driven by integrated technological deployment, infrastructure scaling, and evolving procurement practices in both private and public sectors.

Urban freight and last-mile delivery segments are increasingly transitioning to electric vehicles, with data showing that electrified vans and light trucks now account for nearly 25% of new commercial vehicle registrations in major metropolitan areas. This shift not only reduces local emissions but also stimulates demand for robust charging infrastructure in urban zones. Fleet operators report operational cost savings of up to 22% per vehicle, primarily from lower energy and maintenance expenditures. The urban logistics transformation is driving investment in high-capacity charging clusters in city centers and modern micro-depots tailored for electric light-commercial vehicles. Increasing partnerships between logistics firms and public charging providers enable optimized charging schedules and vehicle uptime improvements.

Despite urban advancements, rural and peri-urban zones continue to suffer from sparse high-speed charging infrastructure. Surveys indicate that fewer than 10% of fast-charging stations are situated outside of urban and suburban corridors. This geographic limitation impedes long-distance EV adoption by commercial fleets and discourages consumer confidence in range reliability. Without sufficient investment to build out fast-charging networks across rural highways and regional hubs, operators face operational challenges such as vehicle repositioning and extended idle times. Infrastructure development has not kept pace with vehicle deployment cycles, raising concerns over charging equity and system resilience.

Vehicle-to-Grid (V2G) technology presents a compelling opportunity for the Electric Vehicles (EVs) Market to evolve into dynamic energy assets. Pilot programs in several developed regions indicate that commercial EV fleets retrofitted with bidirectional chargers can collectively supply up to 15 kW per vehicle back to the grid during peak demand. This creates new revenue streams for fleet operators and enhances grid stability, particularly in regions with high renewable penetration. As utilities begin to value distributed energy resources more highly, EV batteries are poised to play a vital role in grid balancing and demand response services. Integrating V2G functionality into standard EV procurement strategies can unlock monetization paths and support broader energy transition objectives.

The Electric Vehicles (EVs) Market confronts mounting challenges in managing escalating raw material prices, particularly lithium, nickel, and cobalt, which have surged by 30–40% in the past year due to supply chain disruptions and increased global demand. These price pressures strain battery cost structures and undermine margin forecasts for OEMs. While alternative chemistries like LFP (lithium iron phosphate) are gaining traction, they deliver lower energy density. Recycling capacities remain limited, and the lead time for securing sustainable raw materials is long. These factors collectively pressure manufacturers to optimize designs, engage in direct material sourcing agreements, and invest in vertical integration strategies to stabilize supply and control cost volatility.

Modular Platform Proliferation: Manufacturers are increasingly standardizing modular EV platforms across multiple vehicle types—ranging from compact cars to light trucks—to accelerate time-to-market and reduce engineering complexity. Modular architecture now supports up to three vehicle variants per platform with common high-voltage components and standardized battery packs, enabling faster volume scaling.

Integration of High-Power Megawatt Charging: The Electric Vehicles (EVs) Market is seeing a rise in megawatt-level charging installations (1 MW+) for heavy-duty vehicles, especially in logistics and public transport sectors. These ultra-fast chargers cut top-off charging duration for large vehicle battery packs from hours to less than 30 minutes, significantly increasing vehicle availability.

Deployment of Smart Urban Micro-Mobility Solutions: Urban centers are experiencing substantial growth in micro-mobility fleets, including shared electric scooters and small electric delivery vehicles equipped with IoT tracking and battery-level monitoring. One city now operates a fleet of over 5,000 electric scooters connected to a central energy-management system, enabling dynamic recharging and usage analytics—fueling demand for smart-fleet integration.

Adoption of Wireless and Inductive Charging Systems: The Electric Vehicles (EVs) Market is advancing with pilot deployments of inductive in-street and parking-pad wireless charging solutions. For example, electric buses operating on certain urban routes can now recharge wirelessly at stops—adding approximately 10 % more operational hours per day without physical plug-in sessions—enhancing route flexibility and reducing logistic intervention.

The Electric Vehicles (EVs) Market demonstrates a well-defined segmentation structure that highlights its evolution across product types, applications, and end-users. By type, the market encompasses battery electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), and hybrid electric vehicles (HEVs), each serving distinct consumer and commercial needs. Applications span passenger cars, commercial vehicles, two-/three-wheelers, and public transportation systems, with varying adoption dynamics across global regions. End-user insights reveal diverse participation from individual consumers, fleet operators, government bodies, and corporate enterprises. Understanding these segments provides a clear view of demand drivers, technology adoption, and industry investment priorities. Collectively, this segmentation analysis offers decision-makers a comprehensive lens into where innovation, infrastructure, and policy intersect to shape the next phase of electrification.

Battery Electric Vehicles (BEVs) represent the leading segment in the Electric Vehicles (EVs) Market, primarily due to their zero-tailpipe emission profile and rapid adoption in both consumer and fleet categories. Recent advancements in high-capacity lithium-ion and lithium iron phosphate (LFP) batteries have enabled BEVs to achieve ranges exceeding 600 kilometers, making them highly competitive with internal combustion alternatives. Plug-in Hybrid Electric Vehicles (PHEVs) constitute the fastest-growing segment, driven by their dual energy source flexibility that appeals to consumers in regions with limited charging infrastructure. Growth in this segment is further supported by government incentives targeting reduced emissions while maintaining extended driving ranges. Hybrid Electric Vehicles (HEVs), though comparatively mature, continue to hold relevance in markets with transitional energy policies, where consumers value fuel efficiency but lack access to dense charging networks. Each vehicle type contributes uniquely to the overall market landscape, with BEVs commanding leadership, PHEVs rapidly accelerating in adoption, and HEVs serving as bridging technologies in developing regions.

Passenger cars dominate the Electric Vehicles (EVs) Market, accounting for the highest adoption levels globally. Factors such as the availability of diverse model offerings, ranging from compact cars to luxury sedans, and consumer demand for cost-efficient mobility solutions underpin this dominance. Commercial vehicles represent the fastest-growing application segment, fueled by the electrification of logistics fleets, last-mile delivery vans, and heavy-duty trucks. This growth is reinforced by urban emission regulations and fleet operators’ focus on operational cost reductions. Electric buses and coaches play a pivotal role in public transportation, especially in metropolitan areas where government-funded initiatives drive mass deployment. Two- and three-wheelers add significant traction in emerging economies, where affordability and convenience make them highly appealing for daily commutes and short-distance travel. Together, these applications highlight a dynamic and multi-layered ecosystem, with passenger cars leading, commercial fleets growing at unprecedented rates, and niche segments like buses and two-wheelers addressing specific regional mobility needs.

Individual consumers remain the leading end-user group in the Electric Vehicles (EVs) Market, supported by increasing model affordability, home charging solutions, and strong incentives that make EV ownership more accessible. Corporate fleet operators represent the fastest-growing end-user segment, driven by commitments to sustainability goals and the economic advantages of transitioning to electric fleets for logistics, ride-hailing, and shared mobility services. Governments and municipal authorities also play a critical role as end-users by deploying electric buses, service vehicles, and public utility fleets to meet national decarbonization targets. Additionally, specialized end-users such as educational institutions, airports, and industrial parks are integrating EVs into their operational fleets to enhance sustainability credentials. This segmentation underscores a broad adoption spectrum: consumers drive mainstream adoption, corporations push large-scale fleet transitions, and public entities integrate EVs into essential service infrastructure, collectively reinforcing the global trajectory toward electrified transportation.

Asia-Pacific accounted for the largest market share at 55% in 2024, however, Europe is expected to register the fastest growth, expanding at a CAGR of 15% between 2025 and 2032.

Asia-Pacific’s dominance is driven by extensive production ecosystems, strong government initiatives, and the presence of leading EV manufacturers. Europe, on the other hand, is experiencing rapid adoption due to stringent emission regulations, carbon-neutrality targets, and substantial investments in charging infrastructure. North America remains significant, with advanced R&D centers and corporate fleet electrification programs, while South America and the Middle East & Africa are emerging regions with rising infrastructure and policy support. Each region reflects unique structural dynamics, from mature supply chains in Asia-Pacific to innovation-driven markets in Europe, highlighting a globally interconnected yet regionally diverse Electric Vehicles (EVs) Market.

North America accounted for approximately 20% of the global Electric Vehicles (EVs) Market in 2024, supported by the strong presence of automotive innovators and technology-driven enterprises. The region’s demand is primarily fueled by the automotive, logistics, and public transportation industries, with significant uptake from corporate fleet operators. The introduction of federal incentives and state-level zero-emission mandates has accelerated adoption across both passenger and commercial categories. Technological advancements such as AI-integrated battery management systems and autonomous driving solutions are reshaping the regional market. Moreover, digital transformation in mobility services, including subscription-based EV leasing and integrated charging networks, further strengthens North America’s position as a hub for advanced electric vehicle adoption.

Europe held around 23% of the Electric Vehicles (EVs) Market share in 2024, led by Germany, the UK, and France as core adoption centers. Strong policy frameworks by the European Union, including the Green Deal and Euro 7 standards, continue to drive industry compliance and innovation. Germany leads in production capacity, while the UK is advancing through EV battery gigafactories and sustainable transport initiatives. France contributes with national charging corridor projects and incentives for both passenger cars and buses. Europe is also at the forefront of emerging technologies, including hydrogen fuel-cell integration and ultra-fast charging networks, reinforcing the region’s commitment to climate goals and sustainable mobility.

Asia-Pacific dominated the Electric Vehicles (EVs) Market with 55% global share in 2024, spearheaded by China, India, and Japan. China is the largest consumer and manufacturer, with EV production exceeding 10 million units annually, while India is emerging with strong demand in the two- and three-wheeler categories. Japan contributes through advanced battery technology and hybrid vehicle innovation. Infrastructure expansion, including over 2.5 million public charging points in China, underscores the region’s scale. Asia-Pacific also leads in technological innovation, with regional hubs investing in solid-state battery development and smart charging ecosystems, ensuring continuous leadership in both production capacity and consumer adoption.

South America accounted for nearly 5% of the Electric Vehicles (EVs) Market in 2024, with Brazil and Argentina driving regional growth. Brazil’s automotive sector is increasingly electrifying buses and urban fleets, supported by renewable energy integration from its hydroelectric capacity. Argentina is expanding charging infrastructure in metropolitan centers, catering to rising passenger car demand. Government incentives, reduced import tariffs for EV components, and regional trade agreements are enabling wider adoption. Although smaller in market share compared to Asia-Pacific and Europe, South America’s emphasis on integrating EVs into urban mobility and energy transition programs marks its strategic growth potential.

The Middle East & Africa region represented approximately 2% of the Electric Vehicles (EVs) Market in 2024, with demand concentrated in the UAE and South Africa. The UAE has invested heavily in EV-friendly urban infrastructure, installing over 1,000 charging stations and integrating EVs into government service fleets. South Africa is leveraging its automotive assembly plants and renewable energy sector to support gradual EV penetration. Local regulations promoting energy diversification and trade partnerships for advanced battery technologies are shaping the region’s progress. While adoption levels are still modest, ongoing modernization initiatives and smart-city programs are positioning this region for long-term growth.

China – 40% Market Share

China dominates the Electric Vehicles (EVs) Market due to its unmatched production capacity and advanced integrated supply chain ecosystem.

Germany – 12% Market Share

Germany leads Europe in the Electric Vehicles (EVs) Market, supported by high-end automotive manufacturing, strong R&D investments, and nationwide charging infrastructure expansion.

The Electric Vehicles (EVs) Market is characterized by intense competition, with more than 50 globally active manufacturers and several hundred regional players contributing to the industry’s expansion. Leading companies maintain strong market positioning through innovation pipelines, diversified portfolios, and established supply chain networks. Competitive strategies prominently feature strategic alliances, joint ventures, and technology partnerships aimed at accelerating battery development and charging infrastructure deployment. Product launches in 2023 and 2024 highlight advancements in extended-range vehicles, lightweight platforms, and integration of advanced driver assistance systems. Mergers and acquisitions are reshaping the competitive landscape, with established automakers acquiring technology startups specializing in battery recycling, AI-based energy optimization, and connected vehicle software. Innovation trends, such as solid-state battery development, bidirectional charging, and autonomous driving integration, are further intensifying rivalry among participants. This highly dynamic competitive environment compels both established and emerging players to differentiate through sustainability initiatives, digital transformation strategies, and the introduction of customer-centric mobility solutions.

Tesla, Inc.

BYD Auto Co., Ltd.

Volkswagen AG

BMW AG

Mercedes-Benz Group AG

Hyundai Motor Company

Kia Corporation

Nissan Motor Corporation

Toyota Motor Corporation

General Motors Company

Ford Motor Company

Rivian Automotive, Inc.

Lucid Motors, Inc.

Volvo Cars (Geely Holding)

Honda Motor Co., Ltd.

Technological innovation is a defining factor in the Electric Vehicles (EVs) Market, with rapid advancements reshaping product design, manufacturing, and user experience. Battery technology remains at the forefront, with lithium-ion cells dominating but gradually transitioning toward next-generation chemistries such as lithium iron phosphate (LFP), solid-state, and sodium-ion alternatives. Solid-state batteries promise significantly higher energy densities, faster charging, and improved safety margins, with pilot-scale deployments expected to reach 500 Wh/kg by 2025. Charging technology is evolving in parallel, with ultra-fast DC charging stations now capable of delivering up to 350 kW, reducing charging times for passenger cars to under 20 minutes.

Digital technologies, including artificial intelligence and machine learning, are being embedded in battery management systems to extend cycle life by 15–20% and optimize real-time energy consumption. Vehicle-to-Grid (V2G) integration is emerging as a transformative technology, enabling EVs to supply electricity back to power grids and support renewable energy balancing. Lightweight materials such as carbon composites and high-strength aluminum alloys are increasingly used to improve efficiency and vehicle range without compromising structural integrity.

Additionally, connectivity and autonomous driving technologies are merging with EV platforms, allowing vehicles to leverage over-the-air software updates and integrated navigation for smart charging. Robotics and automation in assembly lines have boosted production efficiency by 25–30%, while recycling technologies are improving recovery rates of lithium, cobalt, and nickel from spent batteries. Collectively, these innovations ensure the Electric Vehicles (EVs) Market continues to advance as a critical component of the global transition to sustainable transportation.

In March 2024, Tesla launched an updated Model 3 with a redesigned interior and improved battery system, extending driving range by 12% and enabling faster charging speeds at 250 kW stations.

In September 2024, BYD opened its largest EV manufacturing plant in Thailand with an annual production capacity of 150,000 vehicles, aiming to strengthen its regional presence in Southeast Asia.

In December 2023, Volkswagen announced the rollout of its new unified battery cell platform, designed to reduce production complexity and lower battery costs by up to 50% across future models.

In April 2024, Hyundai introduced an electric heavy-duty truck equipped with an 800V charging system, capable of achieving 80% charge within 35 minutes, targeted at logistics and freight operations.

The scope of the Electric Vehicles (EVs) Market Report encompasses a comprehensive analysis of product types, applications, end-user categories, and geographic regions, providing a holistic understanding for industry stakeholders. Segmentation by type includes battery electric vehicles (BEVs), plug-in hybrid electric vehicles (PHEVs), and hybrid electric vehicles (HEVs), each with distinct adoption trends and technological pathways. Applications span across passenger vehicles, commercial fleets, public transportation systems, and two-/three-wheelers, reflecting a diverse set of demand drivers across global markets.

Geographically, the report covers five major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—highlighting unique adoption dynamics, infrastructure developments, and policy frameworks. End-user insights extend to individual consumers, corporate fleet operators, municipal authorities, and specialized institutions, reflecting the broad base of market participants contributing to growth.

From a technological perspective, the scope examines battery innovations, charging infrastructure, AI-based energy management, autonomous driving integration, and material science advancements. It also evaluates the role of recycling technologies, digital platforms, and vehicle-to-grid applications in shaping the industry. Beyond mainstream adoption, the report considers emerging opportunities in heavy-duty vehicles, micro-mobility, and energy-grid convergence.

This structured scope ensures the Electric Vehicles (EVs) Market Report provides decision-makers with an authoritative overview of the industry’s breadth, highlighting both established sectors and emerging niches that will define future mobility landscapes.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 4,423.4 Million |

| Market Revenue (2032) | USD 12,618.1 Million |

| CAGR (2025–2032) | 14% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Tesla, Inc., BYD Auto Co., Ltd., Volkswagen AG, BMW AG, Mercedes-Benz Group AG, Hyundai Motor Company, Kia Corporation, Nissan Motor Corporation, Toyota Motor Corporation, General Motors Company, Ford Motor Company, Rivian Automotive, Inc., Lucid Motors, Inc., Volvo Cars (Geely Holding), Honda Motor Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |