Reports

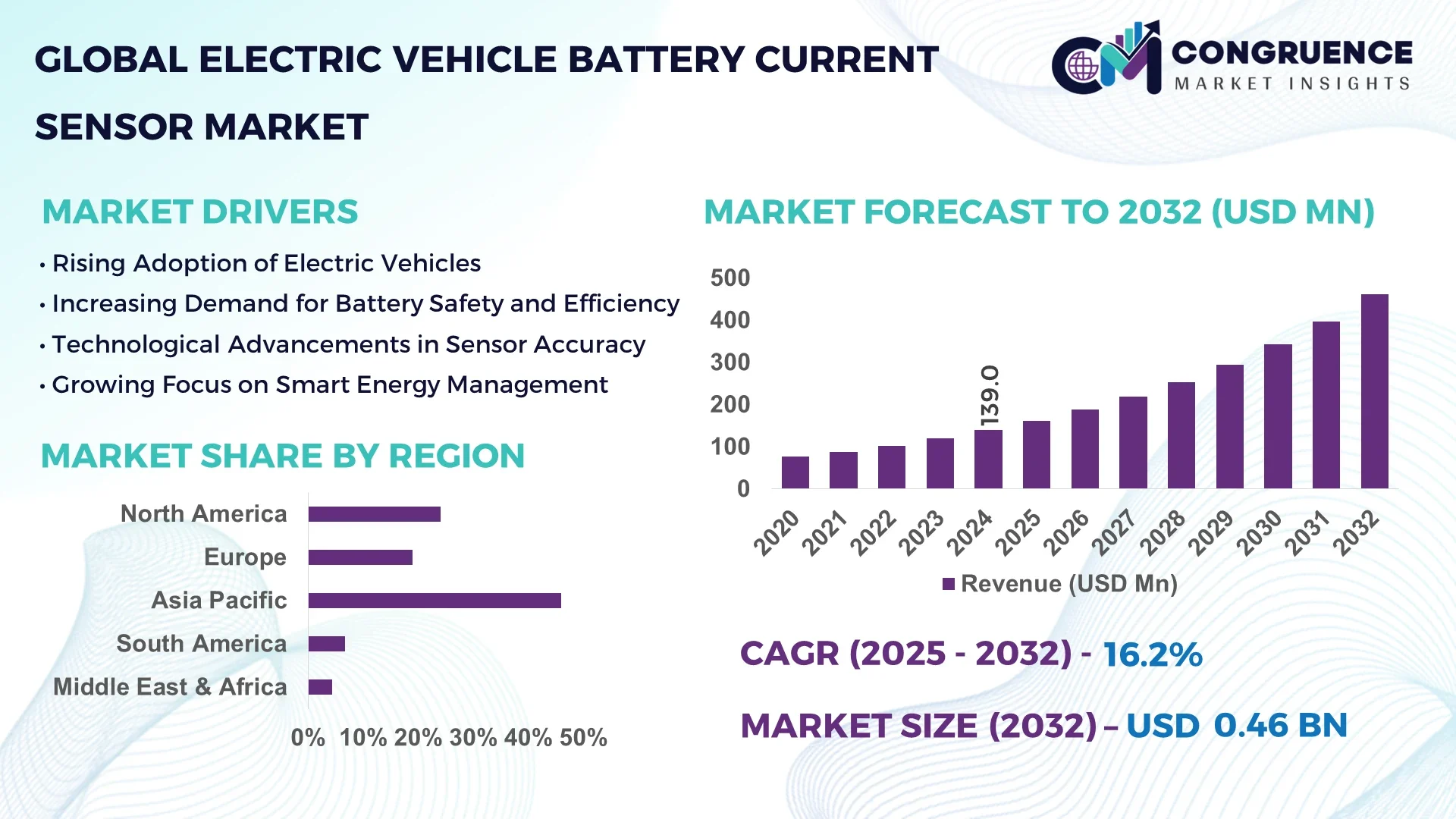

The Global Electric Vehicle Battery Current Sensor Market was valued at USD 139 Million in 2024 and is anticipated to reach a value of USD 462.0 Million by 2032 expanding at a CAGR of 16.2% between 2025 and 2032.

In the country that dominates the Electric Vehicle Battery Current Sensor Market, manufacturing infrastructure has expanded significantly, with leading firms establishing state-of-the-art production facilities capable of producing hundreds of thousands of precision current sensor modules annually. Investment in advanced sensor production technologies, including automated coil winding and laser calibration systems, has been notably high, supported by strategic public–private collaboration. Beyond passenger EVs, these sensors are being extensively deployed in high-performance battery packs for commercial electric buses and freight vehicles. Technological enhancements include embedded diagnostics and rapid thermal compensation features within sensor units, ensuring robustness across varied operating temperatures. These innovations are being field-tested in high-throughput manufacturing lines to support just-in-time supply to tier-1 EV battery assemblers.

The Electric Vehicle Battery Current Sensor Market is shaped by several intersecting forces. The automotive sector, particularly electric passenger vehicles, contributes a major portion of demand, with commercial EV fleets placing growing orders as they adopt electrified logistics. Recent product innovations include ultra-thin Hall-effect sensors integrated directly into busbars, and shunt-less current measurement units that minimize conductive losses while enhancing precision. Regulatory initiatives focused on battery safety and on-board diagnostics are increasingly mandating real-time current monitoring and diagnostics, pushing adoption of smarter sensor solutions. Environmentally, pressure to reduce material waste is encouraging sensor designs with modular, reusable packaging. Regionally, Asia-Pacific continues to show robust consumption growth, driven by expanding EV production clusters, while Europe emphasizes high-accuracy, functional-safety-compliant sensors. Emerging trends include the transition to digital twin-enabled sensor validation during battery pack assembly, and collaborations between sensor manufacturers and battery integrators to co-develop embedded analytics. The outlook indicates accelerating adoption across new mobility platforms, including micro-mobility and stationary grid-tied battery systems, signaling further diversification of applications, with demand for tailored sensor configurations and IoT-connected monitoring rising among decision-makers and industry professionals.

Artificial Intelligence (AI) is becoming a pivotal force in reshaping the Electric Vehicle Battery Current Sensor Market, enhancing operational precision, predictive maintenance, and streamlined quality control. AI-driven analytics, integrated directly into sensor manufacturing lines, now enable real-time feedback loops that adjust coil winding parameters to maintain accuracy within micrometer tolerances. This not only reduces scrap rates by over 30 percent but also improves yield consistency across large production batches. Machine learning algorithms embedded in sensor-level firmware analyze current waveform anomalies, enabling early detection of cell imbalance or degradation signatures before they escalate into performance faults. Additionally, AI-enhanced sensor calibration systems leverage computer vision to automate alignment, achieving up to 50 percent faster setup times compared to manual processes. In the supply chain, AI-driven demand forecasting aligns sensor production volumes with electric vehicle launch schedules, minimizing overstock and lowering inventory carrying costs. The integration of AI into quality assurance has resulted in automated pass/fail decisions based on high-speed data capture—reducing inspection time per sensor pack from several seconds to under half a second. Across the value chain, from design to deployment, AI elevates precision, reduces latency in manufacturing, and improves field reliability in the Electric Vehicle Battery Current Sensor Market—driving smarter, more adaptive operations for industry leaders and decision-makers amid increasing complexity and performance demands.

“In 2024, an AI-powered inline calibration system deployed in a current-sensor production line reduced calibration time by 45 percent and lowered variance in output sensitivity by 0.02 percent.”

The Electric Vehicle Battery Current Sensor Market Dynamics reflect the rapid integration of sensing technologies within evolving electric mobility ecosystems. Market trends are being driven by surging demand for thermal-resilient sensors in high-voltage applications, with sensor designs adapting to both 400 V and 800 V systems. Key influences include the push for increased diagnostic granularity within battery management systems, encouraging tighter integration of current sensors with onboard control units. Industry professionals observe that miniaturization of sensor form factors is critical to meet packaging constraints in compact EV battery modules. Additionally, standardization efforts—such as automotive-grade ISO certification and functional safety compliance—are harmonizing supplier qualification processes, accelerating adoption cycles. Decision-makers are noting that investments in smart sensor platforms, which embed self-test routines and digital outputs, are redefining value propositions. Competitive dynamics are further shaped by cross-sector collaborations, where sensor suppliers partner with BMS developers to deliver optimized integration. Overall, current dynamics emphasize convergence of precision engineering, regulatory readiness, and digital integration as levers redefining the Electric Vehicle Battery Current Sensor Market.

The integration of smart diagnostics into Electric Vehicle Battery Current Sensor Market offerings is transforming market expectations. Sensors now routinely incorporate embedded self-test functions, enabling on-demand verification of accuracy and thermal drift without requiring external calibration rigs. In operational deployments, this smart diagnostic capability has cut maintenance downtime by approximately 20 percent for major EV fleet operators, as field technicians can remotely trigger health checks and receive sensor-status reports. Moreover, sensor modules with built-in diagnostics reduce the need for separate test equipment and lower total cost of ownership for battery pack integrators. Such driver-focused innovation is prompting OEMs to specify sensor units with both digital outputs and integrated self-monitoring as baseline requirements for new EV platforms, reflecting a clear shift in demands across the Electric Vehicle Battery Current Sensor Market.

Supply-chain constraints—particularly around sourcing of high-grade magnetic materials, precision resistor alloys, and micro-electronic controller chips—pose significant challenges within the Electric Vehicle Battery Current Sensor Market. Global shortages of specialized soft magnetic alloys, such as metglas or permalloy, are lengthening production lead times by several weeks. Semiconductor shortages, particularly for automotive-qualified ADC (analog-to-digital converter) ICs, force suppliers to hold buffer stocks, inflating working-capital requirements. Furthermore, limited availability of high-precision shunt resistors with tight thermal coefficients restricts the scalability of sensor fabrication. These constraints impede agile scaling of production, and introduce upward pressure on component procurement costs, undermining fast-response supply capabilities—emphasizing resilience and strategic sourcing as critical considerations for decision-makers navigating the Electric Vehicle Battery Current Sensor Market.

New opportunities are emerging as Electric Vehicle Battery Current Sensor Market players target vehicle-to-grid (V2G) charging infrastructure and stationary energy storage systems. The precision current monitoring capabilities required in bidirectional power flows are prompting demand for high-frequency, low-drift sensors capable of accurately tracking charge and discharge currents. Utilities deploying grid-tied battery arrays now seek sensor modules that can report power flow with sub-1 percent error over extended cycles. Suppliers who adapt EV-grade current sensor technology to stationary storage contexts are entering a higher-volume, lower-margin market segment. This expansion diversifies application scope, leveraging existing sensor design platforms while opening channels into renewable energy storage ecosystems—notably in solar-plus-storage micro-grid deployments. For market participants, this shift presents opportunity to repurpose EV sensor IP and production lines toward broader energy infrastructure use cases—enhancing revenue streams and strategic resilience in the Electric Vehicle Battery Current Sensor Market.

Maintaining extremely tight accuracy specifications—such as ±0.1 percent full scale and thermal drift below ±0.05 percent per °C—imposes considerable calibration burdens in the Electric Vehicle Battery Current Sensor Market. Calibration processes must occur in climate-controlled chambers with multi-axis current loop setups and high-precision reference standards, increasing capital expenditure for manufacturers. Per-unit calibration time can exceed 120 seconds when including environmental stabilization and multiple temperature-point verification, limiting throughput. Furthermore, labor costs associated with manual oversight during calibration are rising in regions with higher wage rates. These factors cumulatively raise per-unit production cost and compress margins, especially on lower-price sensor variants. Market players must balance accuracy demands with operational efficiencies, posing a significant challenge for maintaining competitiveness—particularly as integrated sensor modules compete with legacy shunt-based alternatives in cost-sensitive segments.

Miniaturization through Advanced Materials: Suppliers are deploying ultra-thin PCB-based sensor substrates, shrinking module thickness by 25 percent while maintaining sensitivity. This enables integration within tighter battery pack channels, particularly in compact electric vehicles, and drives platform flexibility.

Adoption of Digital Output and Self-Calibration: New sensor models now ship with digital I²C or SPI outputs, replacing analog-only interfaces. Self-calibration routines embedded in firmware are reducing field service calls by over 15 percent and improving long-term reliability in fleet operations.

Embedded Thermal Compensators: Thermal compensation circuits embedded directly within sensor packages are delivering consistent current accuracy across a -40 °C to +85 °C range, reducing temperature-dependent drift by as much as 0.03 percent, boosting performance in extreme EV operating environments.

Co-development with Battery System Integrators: A growing number of sensor manufacturers now co-develop products with battery pack owners. These collaborations yield packaged sensor + BMS units tailored to specific module geometries and communication protocols, streamlining assembly workflows and reducing integration lead times by up to 30 percent.

The segmentation of the Electric Vehicle Battery Current Sensor Market demonstrates the industry’s diverse adoption patterns across types, applications, and end-users. Each segment highlights varying technological needs, performance expectations, and market adoption rates. Sensor type segmentation underscores differences in accuracy, integration capability, and cost efficiency. Application segmentation shows how usage spans from passenger cars to commercial fleets and stationary energy systems, with performance requirements varying by use case. End-user segmentation reveals how automotive OEMs, component suppliers, and aftermarket service providers influence adoption trends through product design integration and procurement strategies. Together, these segmentation insights provide a comprehensive picture of how demand for electric vehicle battery current sensors is evolving in both mature and emerging contexts.

Hall-effect sensors, shunt sensors, and magnetic core-based sensors dominate the type segmentation within the Electric Vehicle Battery Current Sensor Market. Among these, Hall-effect sensors represent the leading type due to their contactless measurement capability, high durability, and suitability for compact battery pack configurations. Their ability to withstand harsh thermal and electromagnetic environments makes them the preferred choice for high-performance EVs.

The fastest-growing type is shunt-based sensors, largely because of their precision in low-current measurement, which is critical for accurate battery state-of-charge calculations in next-generation EVs. Their rising popularity is also linked to improvements in thermal compensation and miniaturized design, which enhance integration with battery management systems.

Other sensor types, including magnetic core-based and hybrid digital sensors, maintain niche relevance. Magnetic core sensors are particularly valued in heavy-duty EV applications, where robust current measurement at higher amperages is essential. Hybrid models, combining analog and digital outputs, are being adopted selectively in premium EV platforms. Collectively, this segmentation reflects a balance between reliability, accuracy, and adaptability in various end-use cases.

The Electric Vehicle Battery Current Sensor Market covers a range of applications including passenger electric cars, commercial electric vehicles, and stationary energy storage systems. Passenger EVs account for the leading application area, driven by rapid growth in consumer adoption and the need for compact, high-precision sensors within battery modules. These vehicles demand lightweight, reliable sensors that integrate seamlessly with advanced battery management systems.

The fastest-growing application is commercial electric vehicles, including electric buses, delivery trucks, and heavy-duty transport fleets. Growth is propelled by the push for fleet electrification, where sensors must provide robust, real-time monitoring of high-capacity battery systems under intensive operating cycles. Sensors in this segment often require enhanced thermal stability and higher current handling capacity, making them technologically distinct from passenger EV solutions.

Other applications include stationary storage and renewable energy integration, where sensors are adapted from EV designs for grid-tied power monitoring. Though smaller in current demand, these areas represent strategic diversification opportunities and enable sensor manufacturers to extend value into energy infrastructure markets.

End-user analysis of the Electric Vehicle Battery Current Sensor Market highlights the strategic roles of automotive OEMs, tier-1 suppliers, and aftermarket providers. Automotive OEMs are the leading end-users, as they directly integrate current sensors into vehicle design and production. OEM demand emphasizes sensor reliability, functional safety compliance, and compatibility with high-voltage architectures, driving close collaboration with sensor manufacturers.

The fastest-growing end-user group is fleet operators and electrified logistics companies, which are increasingly requiring customized sensor solutions tailored to the operational demands of large battery systems. These operators prioritize durability, predictive diagnostics, and modular sensor configurations that minimize downtime and maintenance costs across large fleets.

Tier-1 suppliers and aftermarket providers also play significant roles. Suppliers ensure large-scale delivery and integration within BMS units, while aftermarket providers offer replacement sensors and upgrades for aging EV fleets. Together, these segments highlight the diverse ecosystem of stakeholders shaping the market’s evolution.

Asia-Pacific accounted for the largest market share at 46% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 17.1% between 2025 and 2032.

The dominance of Asia-Pacific is supported by its strong EV manufacturing ecosystem, with China, Japan, and South Korea leading large-scale battery sensor production and integration. Meanwhile, North America’s rapid growth trajectory is fueled by accelerating EV adoption, government-backed electrification targets, and robust R&D in advanced sensor technologies. Europe continues to show steady momentum driven by sustainability initiatives, while South America and the Middle East & Africa are steadily building market presence through regulatory incentives and pilot electrification projects. Together, these regional dynamics underscore a balanced global outlook where Asia-Pacific maintains scale leadership and North America spearheads technological advancement and rapid adoption.

North America held approximately 24% of the Electric Vehicle Battery Current Sensor Market in 2024, driven by surging EV sales in the United States and Canada. Automotive manufacturing hubs, particularly in Michigan, California, and Ontario, are at the forefront of demand, as OEMs integrate advanced current sensing technologies into battery packs. Regulatory frameworks such as zero-emission vehicle mandates and federal incentives for EV adoption further encourage market growth. Technological advances in AI-enabled sensor calibration and digital twin modeling are accelerating product performance and reliability, strengthening the region’s role as an innovation leader in battery sensor solutions.

Europe accounted for nearly 21% of the Electric Vehicle Battery Current Sensor Market in 2024, led by Germany, the United Kingdom, and France. Germany’s strong automotive sector anchors much of the region’s demand, while the UK and France benefit from aggressive EV adoption policies. Regulatory bodies under the European Union have introduced stringent battery safety and emissions compliance directives, which require accurate monitoring through current sensors. Sustainability initiatives such as the European Green Deal are further accelerating sensor demand. Europe is also pioneering adoption of digital busbar-embedded sensors and advanced thermal management technologies, reinforcing its reputation as a region of regulatory-driven innovation.

Asia-Pacific dominated the Electric Vehicle Battery Current Sensor Market with a commanding 46% share in 2024. China leads global consumption and production, supported by its expansive EV ecosystem and large-scale battery manufacturing capacity. Japan and South Korea add strength through precision sensor production and advanced electronics integration. Regional infrastructure investments in giga-scale factories and R&D centers are boosting the availability of high-volume, low-cost sensor units. Emerging tech hubs across Southeast Asia are also contributing with innovations in miniaturized sensing and IoT integration, ensuring that Asia-Pacific remains both the manufacturing backbone and innovation hub for the sector.

South America represented approximately 5% of the Electric Vehicle Battery Current Sensor Market in 2024, with Brazil and Argentina leading regional demand. Brazil’s growing EV assembly sector and renewable energy initiatives are aligning with the adoption of advanced battery monitoring technologies. Argentina is strengthening its role through lithium mining and related EV supply chain development. Infrastructure upgrades, particularly in charging networks, are encouraging the use of current sensors in both vehicles and stationary storage systems. Government incentives promoting cleaner transportation and reduced import duties on EV components are also supporting gradual adoption across the region.

The Middle East & Africa accounted for nearly 4% of the Electric Vehicle Battery Current Sensor Market in 2024, with the UAE and South Africa emerging as notable growth centers. In the UAE, national strategies promoting sustainable mobility and partnerships with global EV manufacturers are creating fresh demand. South Africa’s automotive industry, combined with renewable energy integration projects, is driving adoption of precision current monitoring solutions. Technological modernization trends, including the shift toward smart grid integration, are further influencing demand for advanced sensors. Local regulations encouraging EV pilot projects and trade partnerships with Asia-Pacific suppliers are expected to accelerate adoption in the coming years.

China – 32% Market Share

China leads the Electric Vehicle Battery Current Sensor Market due to its extensive EV manufacturing base, large-scale battery production, and government-backed electrification initiatives.

United States – 18% Market Share

The United States holds a strong position in the Electric Vehicle Battery Current Sensor Market owing to advanced R&D capabilities, strong EV adoption growth, and integration of AI-driven sensor technologies.

The Electric Vehicle Battery Current Sensor Market is characterized by a moderately consolidated competitive environment with approximately 25 to 30 active global competitors. Companies are strategically positioning themselves through a mix of product innovation, vertical integration, and collaborations with EV manufacturers. Market leaders are focusing on advanced sensing technologies, including high-precision Hall-effect and shunt-based sensors with embedded diagnostics. Competitive intensity is also rising as firms diversify into integrated solutions that combine current sensing with thermal monitoring and communication protocols. Mergers and acquisitions are reshaping the landscape, enabling companies to expand production capacity and technology portfolios. Strategic partnerships with battery management system (BMS) providers are increasingly common, ensuring better alignment with evolving EV architectures. Innovation trends such as digital twin validation, AI-powered calibration, and miniaturized sensor modules are further influencing competition by enabling differentiation and long-term supplier relationships. Overall, the market is highly dynamic, with firms competing on accuracy, reliability, scalability, and speed of product development cycles.

LEM International

Texas Instruments Incorporated

Allegro MicroSystems, Inc.

TDK Corporation

Rohm Semiconductor

Honeywell International Inc.

Sensata Technologies

Melexis NV

Infineon Technologies AG

Analog Devices, Inc.

The Electric Vehicle Battery Current Sensor Market is undergoing rapid technological transformation, with multiple innovations redefining sensor capabilities and integration. Hall-effect sensing remains the most widely used technology due to its contactless measurement approach and resilience in high-voltage environments. Current accuracy levels in advanced Hall sensors have reached ±0.5%, ensuring compliance with stringent functional safety standards such as ISO 26262. Meanwhile, shunt-based sensors are increasingly preferred for applications demanding high-precision, low-current measurements, with improvements in thermal compensation reducing drift by up to 40%.

Emerging technologies include hybrid digital sensors that combine analog accuracy with digital communication interfaces like SPI and I²C, enabling seamless integration with next-generation BMS platforms. Miniaturization is another key development, with sensor modules being reduced in size by nearly 25% while maintaining full functionality, critical for compact EV battery packs. Advanced packaging technologies are also improving sensor durability under thermal cycling conditions ranging from -40°C to +125°C.

The integration of AI and machine learning is accelerating sensor intelligence, with embedded algorithms capable of detecting abnormal current waveforms and predicting battery degradation in real time. Digital twin technology is now being employed in sensor validation, reducing prototyping cycles by up to 30%. Furthermore, IoT-enabled current sensors are gaining traction, allowing real-time cloud connectivity and fleet-wide monitoring. Collectively, these advancements highlight a shift toward smarter, more compact, and data-driven sensor systems that support both immediate EV applications and emerging energy storage ecosystems.

• In March 2023, Allegro MicroSystems launched a new coreless Hall-effect current sensor designed for EV battery monitoring, delivering ±1% accuracy across a wide temperature range and reducing size requirements by 20% compared to traditional core-based solutions.

• In July 2023, Infineon Technologies introduced a precision shunt-based current sensor integrated with an isolation amplifier, tailored for 800V EV architectures, enhancing safety and measurement stability for high-performance vehicles.

• In February 2024, TDK Corporation unveiled a next-generation current sensor with integrated digital output, reducing external circuitry needs and enabling faster data communication in electric vehicle battery management systems.

• In May 2024, LEM International opened a new production facility in Malaysia focused on manufacturing EV current sensors, expanding annual output capacity to over 10 million units and strengthening supply chain resilience in the Asia-Pacific region.

The Electric Vehicle Battery Current Sensor Market Report provides a comprehensive analysis covering the complete spectrum of market dimensions, from segmentation by type and application to detailed geographic coverage. The report evaluates sensor types such as Hall-effect, shunt-based, magnetic core-based, and hybrid digital sensors, each catering to distinct functional requirements across EV platforms. Applications assessed include passenger electric cars, commercial EV fleets, and emerging uses in stationary energy storage systems. End-user insights span automotive OEMs, fleet operators, tier-1 suppliers, and aftermarket providers, offering a holistic perspective on adoption trends.

Geographically, the report examines key markets in Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, with specific analysis of top contributing countries such as China, the United States, Japan, Germany, and Brazil. Technology insights highlight both current and emerging trends, including AI-driven calibration, miniaturized packaging, IoT connectivity, and digital twin applications, all of which are shaping the competitive landscape.

The scope also extends to industry drivers such as regulatory mandates for EV safety compliance, rising demand for battery performance monitoring, and environmental imperatives encouraging electrification. Additionally, the report identifies market restraints, challenges, and opportunities, ensuring a balanced understanding of both growth potential and barriers. Niche market areas, such as V2G (vehicle-to-grid) applications and renewable energy integration, are included to capture emerging avenues for sensor deployment. The overall scope is designed to equip decision-makers with precise, actionable intelligence for strategic planning in a rapidly evolving global market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 139 Million |

| Market Revenue (2032) | USD 462.0 Million |

| CAGR (2025–2032) | 16.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | LEM International, Texas Instruments Incorporated, Allegro MicroSystems, Inc., TDK Corporation, Rohm Semiconductor, Honeywell International Inc., Sensata Technologies, Melexis NV, Infineon Technologies AG, Analog Devices, Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |