Reports

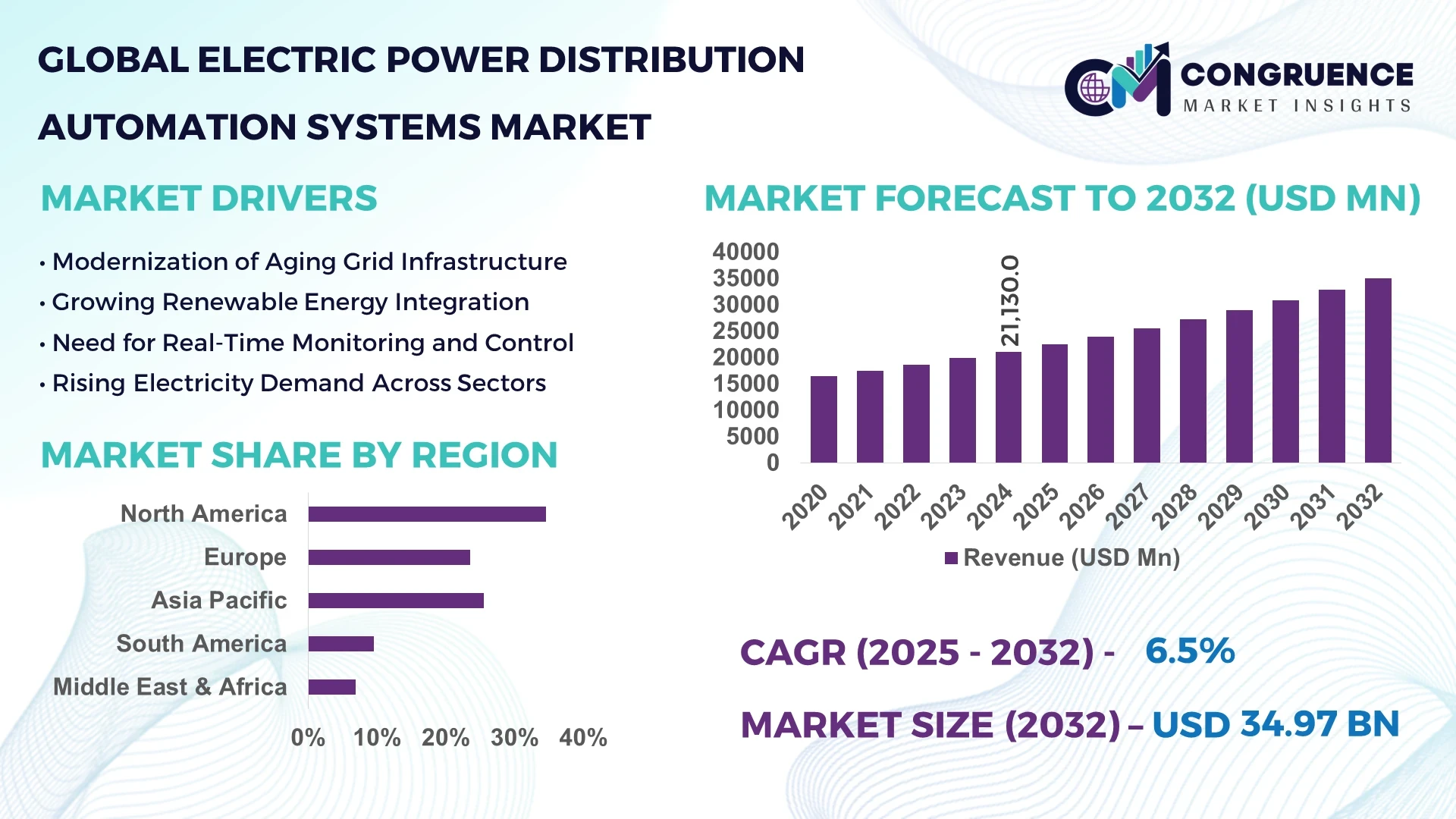

The Global Electric Power Distribution Automation Systems Market was valued at USD 21,130 million in 2024 and is anticipated to reach a value of USD 34,970.05 million by 2032, expanding at a CAGR of 6.5% between 2025 and 2032.

In the United States, the deployment of AI-driven predictive maintenance tools and dynamic line rating technologies has significantly enhanced grid reliability and efficiency, contributing to the country's leading position in the market.

The Electric Power Distribution Automation Systems market is experiencing robust growth, driven by the increasing integration of advanced technologies and the need for efficient power management. In 2024, the market witnessed substantial investments in smart grid infrastructure, with utilities adopting automation solutions to enhance operational efficiency. The implementation of intelligent electronic devices (IEDs) and supervisory control and data acquisition (SCADA) systems has enabled real-time monitoring and control of distribution networks. Additionally, the adoption of distributed energy resources (DERs) and the proliferation of electric vehicles have necessitated the modernization of distribution systems. Utilities are focusing on deploying automated feeder switches and reclosers to improve fault detection and isolation capabilities. Furthermore, the integration of renewable energy sources has led to the development of advanced distribution management systems (ADMS) to manage bidirectional power flows effectively. The market is also witnessing a shift towards cloud-based solutions for data analytics and grid optimization. Overall, the Electric Power Distribution Automation Systems market is poised for significant expansion, supported by technological advancements and the growing demand for reliable and sustainable power distribution.

Artificial Intelligence (AI) is revolutionizing the Electric Power Distribution Automation Systems market by enhancing grid reliability, efficiency, and resilience. Utilities are leveraging AI algorithms to analyze vast amounts of data from sensors, smart meters, and other grid components to predict equipment failures and optimize maintenance schedules. This predictive maintenance approach minimizes downtime and extends the lifespan of critical assets. For instance, utilities implementing AI-driven maintenance strategies have reported up to a 25% reduction in maintenance costs.

AI is also instrumental in load forecasting, enabling utilities to predict energy demand accurately and adjust supply accordingly. Machine learning models analyze historical consumption patterns and real-time data to forecast load demands, ensuring efficient energy distribution and reducing the risk of overloads. Moreover, AI facilitates the integration of renewable energy sources by managing the variability and intermittency associated with solar and wind power. Advanced analytics platforms utilize AI to balance supply and demand dynamically, maintaining grid stability. In the realm of fault detection, AI-powered systems can identify anomalies and potential faults in the distribution network swiftly, allowing for prompt corrective actions. This capability enhances the reliability of power supply and reduces the duration of outages. Additionally, AI aids in optimizing voltage regulation and reactive power management, contributing to improved power quality. The integration of AI in Electric Power Distribution Automation Systems is not only transforming operational processes but also paving the way for the development of self-healing grids that can autonomously detect and rectify issues, ensuring uninterrupted power delivery.(

"In March 2025, the Electric Power Research Institute (EPRI), in collaboration with major tech and energy companies, launched the Open Power AI Consortium. This initiative aims to develop standardized AI models and datasets tailored for the power sector to enhance grid efficiency, asset performance, and cost reduction."

The expanding deployment of smart grid infrastructure is a major growth driver for the Electric Power Distribution Automation Systems market. With over 250 million smart meters installed globally by the end of 2024, utilities are now focusing on end-to-end automation of distribution networks. The increase in distributed energy resources, particularly rooftop solar installations and small-scale wind farms, necessitates sophisticated automation systems for effective grid management. Utilities are investing in intelligent reclosers, feeder automation devices, and distributed control systems to enable remote fault detection and service restoration. These smart grids not only improve operational efficiency but also help minimize energy losses, contributing to higher utility profits and enhanced energy delivery reliability.

One of the significant restraints in the Electric Power Distribution Automation Systems market is the high initial capital investment required for implementation. From installing intelligent devices and communication infrastructure to upgrading substations with advanced control equipment, the costs involved can be prohibitive, especially for small and mid-sized utility companies. The payback period for such automation systems can extend beyond five years in many regions, which affects investment decisions in budget-constrained environments. In developing economies, where power infrastructure is often underfunded or outdated, financial constraints and regulatory hurdles further limit widespread adoption. Moreover, uncertainties regarding return on investment (ROI) and evolving technology standards can make utilities hesitant to invest.

The global transition toward clean energy sources is creating substantial opportunities in the Electric Power Distribution Automation Systems market. As solar and wind energy continue to expand, with global renewable capacity surpassing 3,700 GW by 2024, utilities are increasingly challenged with managing variable and intermittent energy inputs. This complexity is driving demand for advanced distribution management systems (ADMS), automated switches, and voltage regulators. These technologies help maintain grid stability while efficiently handling fluctuating loads and distributed generation points. As nations implement policies supporting net-zero emissions, automation systems will play a critical role in real-time energy balancing and power flow optimization, presenting lucrative market opportunities for vendors and integrators.

As Electric Power Distribution Automation Systems become more interconnected and reliant on digital communication networks, the risk of cyberattacks on power infrastructure is increasing. In 2024 alone, several utilities across Europe and Asia reported attempted breaches targeting SCADA systems and substation automation units. These attacks not only threaten service continuity but can also result in data theft and equipment damage. The complexity of securing legacy infrastructure that has been upgraded with modern digital tools presents a formidable challenge. Furthermore, a lack of standardized cybersecurity frameworks across regions leads to inconsistent protective measures, increasing system vulnerabilities. Addressing these security gaps is critical to building confidence in automation technologies and ensuring uninterrupted power delivery.

• Increased Implementation of Self-Healing Grids: One of the most prominent trends in the Electric Power Distribution Automation Systems market is the rapid deployment of self-healing grid technologies. Utilities across Asia-Pacific and North America have begun integrating sensors, fault detectors, and automated reclosers that enable real-time rerouting of electricity during outages. These systems reduce downtime and service disruption by up to 70%, enhancing grid resilience. The integration of these automated systems into legacy networks is proving essential for managing high-load urban centers and weather-related disruptions.

• Surge in Adoption of Edge Computing for Distribution Networks: Edge computing has emerged as a vital trend to support low-latency data processing in electric grid infrastructure. By bringing analytics closer to data sources, edge systems empower operators to make rapid decisions on voltage regulation, transformer load balancing, and fault isolation. Utilities in Europe and North America are increasingly investing in edge-enabled automation devices, helping them enhance system reliability and reduce dependency on centralized cloud infrastructure.

• Proliferation of IoT-Based Grid Monitoring Solutions: The incorporation of Internet of Things (IoT) technologies in distribution automation is significantly improving real-time monitoring and predictive maintenance. IoT-enabled devices, including smart sensors and actuators, are allowing operators to detect faults, measure line temperature, and identify overload conditions. By 2024, over 50% of utility companies in developed regions had deployed IoT devices for feeder and substation automation, leading to more efficient maintenance scheduling and fewer manual inspections.

• Shift Toward Cloud-Based SCADA Systems: Traditional on-premise SCADA systems are being replaced by cloud-integrated platforms that allow remote access, scalability, and improved collaboration. Utility providers are increasingly adopting cloud SCADA to centralize their operational data, streamline reporting, and lower IT infrastructure costs. In 2024, utilities in Southeast Asia and Latin America invested heavily in cloud-based control centers, boosting their real-time visualization capabilities across distributed assets and improving response times for fault recovery.

The Electric Power Distribution Automation Systems market is segmented by type, application, and end-user, each contributing uniquely to the market's structure and dynamics. Distribution automation components such as feeders, substations, and transformers are customized based on usage patterns across commercial, residential, and industrial sectors. Automation hardware and software technologies differ significantly in adoption pace, with real-time monitoring and communication interfaces becoming pivotal for reliable electricity distribution. The growing pressure on electric grids, mainly due to distributed renewable integration and rising urban energy consumption, is intensifying demand for advanced, real-time, and scalable automation systems that reduce operational complexity and enhance grid resilience.

The Electric Power Distribution Automation Systems market is segmented into Feeder Automation, Substation Automation, Consumer Automation, and Recloser Automation. Among these, Feeder Automationis currently the leading segment due to its essential role in minimizing power outages and restoring service efficiently through fault location isolation and service restoration (FLISR). Utilities across North America and Europe have increased investments in feeder automation systems, leading to enhanced operational continuity and better load management. On the other hand, Substation Automationis the fastest-growing segment as utilities modernize outdated substation infrastructure using digital relays, RTUs, and communication gateways. The surge in demand for remote monitoring, voltage regulation, and improved safety across substations is accelerating its growth. Both types are key to creating a fully intelligent and self-regulating distribution network that meets future energy demands while minimizing human intervention and manual operation inefficiencies.

Based on application, the market is divided into Fault Detection, Voltage Regulation, Communication Infrastructure, Load Balancing, and Supervisory Control and Data Acquisition (SCADA). Fault Detectionleads the application segment due to its critical role in improving grid reliability and reducing downtime. It enables operators to quickly identify, isolate, and fix distribution system faults, minimizing power disruptions for consumers. The widespread implementation of automated fault detection systems in urban networks has helped utilities enhance customer satisfaction. Meanwhile, SCADA-based applicationsare registering the fastest growth rate, particularly in emerging economies, where digital transformation initiatives are at the forefront. SCADA helps in remote asset control, enabling real-time monitoring and efficient decision-making for large-scale grids. Its rising deployment is reshaping how utility providers manage and control distributed energy systems with reduced operational risk.

The market, by end-user, is segmented into Residential, Commercial, Industrial, and Utility sectors. The Utility sectordominates the market, driven by large-scale investments in smart grid infrastructure and the modernization of national distribution networks. Utility companies manage expansive networks requiring advanced automation for outage management, demand response, and distributed generation coordination. Their direct control over infrastructure grants them early access to emerging technologies, making them primary consumers of advanced automation systems. However, the Industrial sectoris witnessing the fastest growth. Industries with critical operational continuity needs—such as manufacturing, mining, and oil & gas—are increasingly adopting automation for voltage stability, peak load management, and fault recovery. With rising energy prices and carbon footprint concerns, industrial units are prioritizing automation to ensure efficiency, safety, and compliance with environmental regulations. This shift is boosting market expansion across heavy-load industrial hubs in Asia-Pacific and the Middle East.

North America accounted for the largest market share at 34.6% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

The Electric Power Distribution Automation Systems market is experiencing robust growth across all regions, but North America leads due to early adoption of smart grid technologies, strong utility investments, and extensive infrastructure upgrades. The United States and Canada have invested heavily in feeder automation, fault location systems, and SCADA platforms. Meanwhile, Asia-Pacific is rapidly accelerating due to urbanization, electrification initiatives, and increasing adoption of IoT-based automation technologies in countries like China, India, and Japan. Europe holds a substantial share, supported by sustainable energy policies and grid modernization programs. South America and the Middle East & Africa are emerging markets with growing demand, particularly in industrial automation and remote grid management for rural electrification.

Grid Digitalization and Utility-Driven Investments Fuel Growth

North America remains the most advanced market for electric power distribution automation systems, driven by substantial investments from leading utility providers in the U.S. and Canada. In 2024, the region commanded a 34.6% share of the global market. Over 70% of urban utilities in the U.S. have integrated automated fault detection, voltage regulation devices, and reclosers across their networks. Additionally, smart meter penetration exceeded 85% across several states, allowing better integration of consumer data into distribution systems. Canadian utilities have focused on substation automation, especially in provinces with dense industrial activity. Demand response programs and the shift toward decarbonized energy sources are also driving increased deployment of self-healing grids and intelligent automation tools.

Sustainable Energy Integration Driving Automation Advancements

Europe accounted for 26.8% of the global market share in 2024, backed by strong regulatory frameworks promoting energy efficiency and grid resilience. Countries such as Germany, France, and the UK have prioritized substation automation and voltage optimization to support the high penetration of renewable energy sources. More than 60% of European utilities have integrated SCADA and digital substations to improve grid visibility and ensure seamless energy transition. The European Green Deal and national-level energy transition programs have led to increased adoption of digital reclosers, distribution transformers, and IoT-enabled sensors. Utilities in Nordic countries are also investing in automation for cold-weather reliability and grid balancing.

Rapid Electrification and Urban Growth Spur Demand

Asia-Pacific is becoming a global hotspot for electric power distribution automation, with a projected surge in adoption across developing and developed economies. In 2024, the region held a 21.4% market share and is poised for the fastest expansion. China leads the region with widespread deployment of smart substations and feeder automation systems across state-owned utility networks. India has scaled its smart grid mission, deploying fault detection systems and load balancing technologies in key urban centers. Japan and South Korea have integrated automation with renewable energy sources to support energy security and disaster resilience. The growing demand for uninterrupted power supply in high-density cities is fueling government-backed investments in digital grid infrastructure.

Modernization of Aging Grid Infrastructure Accelerates Automation

South America is witnessing steady growth in the electric power distribution automation systems market, with Brazil and Argentina spearheading regional developments. In 2024, the region accounted for 7.1% of the global market. Brazil’s investment in remote fault detection systems and SCADA has helped reduce outage response times in major cities like São Paulo and Rio de Janeiro. Argentina is focusing on voltage regulation and feeder automation to stabilize energy distribution across its vast territory. The rise of renewable energy projects, especially in Chile and Colombia, has increased the need for automation tools that can manage fluctuating energy inputs. Rural electrification projects also support adoption of automated reclosers and real-time monitoring systems.

Utility Transformation and Industrial Electrification Boost Automation

The Middle East & Africa region held an 8.1% share of the global market in 2024 and is gaining momentum due to infrastructure development and energy diversification efforts. Countries like Saudi Arabia and the UAE have integrated automation technologies in urban transmission and distribution networks to improve efficiency and reduce technical losses. Over 40% of new substation projects in the Gulf region include SCADA and digital protection systems. In Africa, South Africa and Kenya are implementing smart grid pilot programs to improve grid reliability and extend services to underserved regions. Industrial growth, particularly in mining and oil & gas, is encouraging wider use of real-time grid monitoring and automated load balancing solutions.

United States – 28.7%: Due to widespread smart grid adoption and large-scale investments in feeder and substation automation.

China – 16.4%: Driven by rapid urbanization, strong government backing, and deployment of intelligent distribution networks.

The global Electric Power Distribution Automation Systems market is characterized by intense competition among leading players, driven by rapid technological innovation, growing demand for grid modernization, and the push for smart infrastructure globally. Established companies are increasingly investing in strategic partnerships, product launches, and geographic expansion to strengthen their market position. In 2024, over 60% of market share was captured by the top 10 players, many of which offer integrated solutions combining SCADA, distribution management systems (DMS), and feeder automation.

Vendors are focusing on AI-driven analytics, cloud-enabled automation platforms, and IoT sensor integration to differentiate their offerings. For example, multiple companies have launched substation automation solutions with enhanced cybersecurity features and edge computing capabilities. Additionally, several players have expanded their footprints across Asia-Pacific and Latin America due to rising utility demand for automated systems. Mergers and acquisitions have also played a crucial role, with at least five significant deals recorded in the past two years aimed at enhancing product portfolios and technological capabilities. New entrants and regional players continue to challenge incumbents by offering low-cost, scalable, and modular automation solutions tailored for specific grid conditions.

Siemens AG

Schneider Electric

ABB Ltd

General Electric

Eaton Corporation

Schweitzer Engineering Laboratories (SEL)

Cisco Systems, Inc.

Mitsubishi Electric Corporation

Honeywell International Inc.

S&C Electric Company

Landis+Gyr

Toshiba Corporation

Oracle Corporation

Itron Inc.

Hitachi Energy

The Electric Power Distribution Automation Systems market is undergoing a significant transformation, driven by the integration of advanced technologies aimed at enhancing grid reliability, efficiency, and adaptability. One of the pivotal advancements is the implementation of digital substations, which utilize intelligent electronic devices (IEDs) and communication protocols like IEC 61850 to enable real-time monitoring and control. These digital substations facilitate faster fault detection and isolation, reducing outage durations and improving overall system resilience. Another critical technological development is the adoption of advanced metering infrastructure (AMI). AMI systems provide utilities with detailed energy consumption data, enabling demand response strategies and efficient energy distribution. For instance, in the United States, the deployment of smart meters has reached over 70% of total electric meters, significantly contributing to grid modernization efforts. Furthermore, the integration of Internet of Things (IoT) devices and sensors across the distribution network allows for continuous monitoring of equipment health and environmental conditions. This real-time data collection supports predictive maintenance strategies, minimizing unexpected equipment failures and maintenance costs.

Artificial Intelligence (AI) and machine learning algorithms are increasingly being employed to analyze vast amounts of data generated by these systems. AI-driven analytics assist in load forecasting, fault prediction, and optimization of energy flow, thereby enhancing decision-making processes within utilities. Additionally, the emergence of cloud computing and edge computing technologies offers scalable solutions for data storage and processing. These technologies enable utilities to manage and analyze data efficiently, facilitating quicker response times and improved operational efficiency. Collectively, these technological advancements are instrumental in transitioning traditional power distribution systems into intelligent, automated networks capable of meeting the evolving demands of modern energy consumption and distribution.

In August 2024, Hitachi Energy introduced the Relion REF650, an advanced multi-application protection and control relay designed to enhance flexibility and reliability in power distribution systems. This device supports evolving power quality needs across industrial and utility operations, offering a modular design and compatibility with the latest industry standards.

In May 2024, ABB signed an agreement to acquire Siemens' Wiring Accessories business in China. This strategic move aims to expand ABB's smart buildings portfolio, incorporating products such as smart home systems and leveraging a vast distributor network to strengthen its presence in the Chinese market.

In March 2024, Itron Inc. acquired Elpis Squared for $35 million. This acquisition enables Itron to integrate high-resolution, real-time "grid edge" data into planning, operations, and engineering processes, marking a significant advancement in the sector's capability to manage and optimize power distribution networks.

In January 2024, Hitachi Energy launched the SAM600 3.0, an innovative product for digital substations. The SAM600 integrates conventional instrument transformers into modern IEC 61850-9-2 process bus substation automation, protection, and control systems, facilitating safe, efficient, and extendable retrofits for existing substations.

The scope of the Electric Power Distribution Automation Systems Market Report encompasses a comprehensive analysis of key industry trends, growth drivers, technological advancements, regional insights, and competitive landscapes. These systems play a crucial role in modernizing electricity distribution networks by enhancing monitoring, control, and protection capabilities. With aging infrastructure and increasing global electricity consumption, utilities worldwide are rapidly adopting automation to improve reliability, reduce outages, and enable seamless integration of renewable energy sources.

The report provides in-depth insights into various components of distribution automation systems including advanced sensors, communication technologies, smart meters, automated feeder switches, and reclosers. It evaluates market demand across major end-users such as public utility providers, private power distribution companies, and industrial power consumers. In recent years, the proliferation of smart grid initiatives, particularly in North America, Europe, and Asia-Pacific, has fueled deployment of these systems on a large scale. For instance, more than 100 million smart meters are now operational in the United States alone.

Further, the report investigates the impact of digital technologies such as IoT, AI, and cloud-based analytics in transforming traditional power grids into intelligent distribution networks. It also covers vendor positioning, product innovation, strategic alliances, and policy frameworks that are shaping market evolution. This detailed coverage helps stakeholders understand future opportunities, address market challenges, and make informed decisions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 21130 Million |

|

Market Revenue in 2032 |

USD 34970.05 Million |

|

CAGR (2025 - 2032) |

6.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens AG, Schneider Electric, ABB Ltd, General Electric, Eaton Corporation, Schweitzer Engineering Laboratories (SEL), Cisco Systems, Inc., Mitsubishi Electric Corporation, Honeywell International Inc., S&C Electric Company, Landis+Gyr, Toshiba Corporation, Oracle Corporation, Itron Inc., Hitachi Energy |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |