Reports

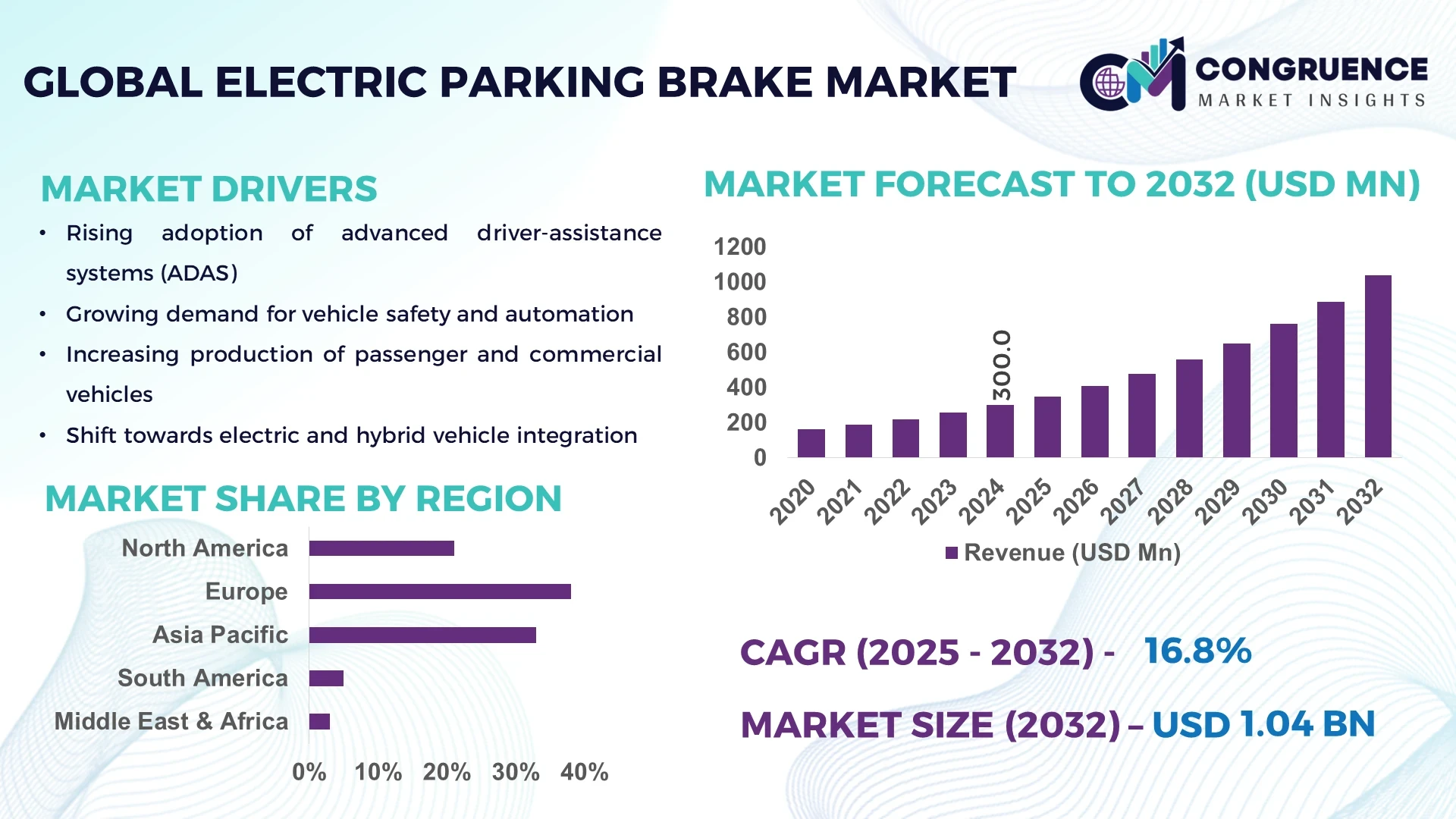

The Global Electric Parking Brake Market was valued at USD 300.0 Million in 2024 and is anticipated to reach a value of USD 1,039.1 Million by 2032 expanding at a CAGR of 16.8% between 2025 and 2032. The market growth is driven by rising adoption of advanced driver assistance systems and vehicle automation.

Germany leads in electric parking brake production with its robust automotive ecosystem, housing over 40 advanced manufacturing facilities specializing in brake system components. With an estimated annual production capacity exceeding 15 million units in 2024, Germany benefits from continuous investments in research, where nearly USD 500 million was directed toward mechatronic innovations. Automotive OEMs in the region have also incorporated next-generation brake-by-wire technology across premium vehicle segments, supported by consumer adoption levels surpassing 55% in new car registrations equipped with electric parking brakes.

Market Size & Growth: Valued at USD 300.0 Million in 2024, projected to reach USD 1,039.1 Million by 2032 at a CAGR of 16.8%; growth driven by premium vehicle automation demand.

Top Growth Drivers: 42% adoption in luxury vehicles, 36% efficiency improvement in automated braking, 28% increase in OEM integration rates.

Short-Term Forecast: By 2028, braking response efficiency expected to improve by 31% with enhanced electronic control modules.

Emerging Technologies: Integration of regenerative braking systems, AI-based safety diagnostics, and next-gen mechatronic modules.

Regional Leaders: Europe projected to reach USD 420 Million by 2032 with strong luxury car adoption; Asia-Pacific USD 380 Million with mass production efficiency; North America USD 239 Million driven by EV adoption trends.

Consumer/End-User Trends: Increasing adoption among electric vehicle buyers, with 52% citing advanced braking features as a key purchase factor.

Pilot or Case Example: In 2026, a German OEM pilot project reduced brake system downtime by 24% through integrated IoT diagnostics.

Competitive Landscape: Continental AG leads with ~19% share, followed by ZF Friedrichshafen, Aisin Seiki, Brembo, and Hyundai Mobis.

Regulatory & ESG Impact: EU regulations mandating advanced braking systems accelerated compliance adoption; firms committing to 22% emissions reduction in supply chains by 2030.

Investment & Funding Patterns: Over USD 2.4 billion invested globally in smart braking technologies since 2021, with rising venture capital interest in EV brake startups.

Innovation & Future Outlook: Development of software-defined braking platforms, integration with ADAS and autonomous driving, and predictive maintenance shaping the next decade.

The electric parking brake market is witnessing strong adoption across passenger vehicles (over 65% share), commercial fleets, and premium EVs. Recent product innovations, including lightweight actuators and integrated control modules, are reducing vehicle weight while enhancing safety compliance. Regulatory incentives in Europe and Asia Pacific, combined with rising consumer preference for advanced driver-assistance systems, are driving regional consumption. Emerging trends such as autonomous-ready braking platforms and AI-based predictive diagnostics will further accelerate global growth in the coming years.

The Electric Parking Brake Market represents a critical transformation in modern vehicle architecture, strategically aligned with global safety, automation, and sustainability imperatives. By replacing traditional mechanical systems with electronic solutions, the market delivers measurable improvements in efficiency, safety, and reliability. For instance, electronic braking modules deliver 28% faster actuation time compared to conventional hydraulic systems, ensuring improved safety and responsiveness. Regionally, Europe dominates in volume, while Asia-Pacific leads in adoption with 47% of OEMs integrating EPB systems across new EV platforms. This highlights a dual growth pathway—Europe driven by premium automotive production and Asia-Pacific supported by high-volume, cost-efficient manufacturing. By 2027, AI-enabled diagnostics are expected to cut maintenance costs by 22%, providing short-term efficiency gains and reinforcing adoption among EV manufacturers.

Firms are simultaneously aligning with ESG commitments, targeting a 30% reduction in lifecycle emissions by 2030. In 2026, a South Korean automotive leader achieved a 19% reduction in assembly line downtime through predictive EPB integration supported by Industry 4.0 practices. These micro-scenarios demonstrate the practical value of EPB adoption in real-world settings. The Electric Parking Brake Market is thus emerging as a pillar of resilience, compliance, and sustainable growth, strategically shaping the future of mobility while enhancing operational efficiency, regulatory alignment, and consumer trust in next-generation vehicles.

The Electric Parking Brake Market is influenced by evolving consumer demand for advanced vehicle safety, increasing adoption of automation, and stringent regulatory requirements mandating electronic braking integration. Market dynamics are shaped by rapid EV penetration, the growing premium vehicle segment, and OEM partnerships driving innovation. Technological advancements such as AI-based diagnostics, regenerative braking compatibility, and software-defined modules are further propelling market evolution. Additionally, supply chain investments and regional manufacturing capabilities are critical in supporting market scalability and global distribution.

The accelerating shift toward electric vehicles is driving EPB demand, with EV penetration surpassing 18% of global new car sales in 2024. EPBs are integrated seamlessly into EV platforms due to their lightweight structure and compatibility with regenerative braking systems. Increased government incentives for EVs, such as subsidies and tax credits, further enhance adoption. For instance, China produced over 9 million EVs in 2023, of which a significant proportion integrated advanced EPB systems to meet safety standards. This trend supports large-scale demand, with manufacturers aligning product design for efficient integration in EV powertrains.

Despite benefits, EPBs face challenges due to higher electronic integration costs compared to mechanical systems. Manufacturing EPB modules requires advanced sensors, actuators, and microcontrollers, which raise system prices by up to 25%. This cost barrier restricts widespread adoption in budget and mid-segment vehicles. Additionally, reliance on specialized components heightens supply chain risks. For example, semiconductor shortages in 2022 delayed EPB-equipped vehicle launches by several months, impacting OEM profitability. These cost and supply constraints hinder uniform adoption across all vehicle classes, slowing down market expansion.

The rise of autonomous vehicles offers a transformative opportunity for EPBs. Autonomous platforms require advanced braking systems capable of integration with vehicle control algorithms. EPBs align perfectly due to their electronic actuation and compatibility with ADAS features. By 2030, it is expected that over 20% of global autonomous vehicles will deploy EPB modules as standard equipment. This creates opportunities for OEMs and suppliers to design integrated braking solutions that enhance autonomous safety protocols. Moreover, partnerships with AI-driven software providers can accelerate innovation, enabling predictive braking and enhanced fail-safe mechanisms.

The EPB market faces significant challenges in navigating regulatory frameworks and achieving safety certifications across regions. Stringent compliance with UNECE, FMVSS, and ISO standards increases time-to-market and R&D costs. Variations in testing protocols between Europe, North America, and Asia complicate global deployment. For example, achieving dual certification for Europe and the U.S. can extend product launch timelines by 12–18 months. Additionally, frequent updates to automotive safety regulations demand continuous system redesign and testing. These regulatory burdens increase costs, stretch OEM resources, and pose barriers to timely commercialization.

Integration with Autonomous and ADAS Systems: In 2024, over 41% of newly launched premium vehicles featured EPBs integrated with ADAS modules, improving automated braking efficiency by 33% and enhancing vehicle safety in critical conditions.

Growth in EV Platform Adoption: EPBs are now integrated into 52% of EV models globally, with adoption expected to rise to 68% by 2027. This shift is fueled by EV production exceeding 10 million units annually and demand for compact, electronic-compatible braking systems.

Advancements in Smart Diagnostics: Manufacturers introduced EPBs with predictive maintenance capability, reducing system failures by 27% in fleet operations. AI-driven diagnostics cut repair time by 22%, supporting greater operational uptime for logistics and commercial fleets.

Expansion of Regional Manufacturing Hubs: Asia-Pacific EPB manufacturing output grew by 18% in 2024, supported by rising OEM investments. By 2030, regional production is projected to meet 45% of global EPB demand, accelerating localization and supply chain resilience.

The global electric parking brake market is segmented across types, applications, and end-user categories, each reflecting unique dynamics that shape overall industry performance. Type-based segmentation highlights the evolution from traditional cable-pull mechanisms to advanced electronic systems, with clear preferences emerging based on vehicle class and integration needs. Application analysis shows how electric parking brakes are deployed across passenger cars, commercial vehicles, and specialized mobility platforms, driven by safety regulations, premium features, and growing consumer demand for automated assistance. End-user segmentation emphasizes adoption trends across OEMs, fleet operators, and aftermarket players, with OEMs dominating due to their direct role in integrating safety innovations into mass production. Together, these segment insights provide decision-makers with a comprehensive understanding of how market demand is structured, which categories drive adoption, and where growth opportunities are accelerating across the automotive ecosystem.

In terms of type, the electric parking brake market is primarily divided into cable pull systems and electronic control systems. Electronic control systems currently account for the largest share, representing around 58% of global adoption, as they align with the automotive industry’s shift toward automation, safety compliance, and integration with electronic stability control. Cable pull systems continue to hold relevance in entry-level and mid-range vehicles, but their adoption has decreased to approximately 27%, reflecting growing replacement by advanced alternatives. The fastest-growing segment is the integrated electronic parking brake, projected to expand at a CAGR of 10.4%, driven by rising demand for premium vehicles, regulatory emphasis on safety features, and consumer preference for seamless driver assistance technologies. Other types, such as hybrid mechanisms and aftermarket retrofits, collectively account for nearly 15% of adoption, serving niche markets where cost sensitivity or vehicle design constraints persist.

Passenger vehicles dominate the application landscape for electric parking brakes, accounting for 62% of global adoption due to their integration into compact, mid-size, and luxury cars where safety and driver assistance features are prioritized. Commercial vehicles, while currently holding a 21% share, are increasingly adopting these systems as fleet operators recognize the benefits of automation, reliability, and reduced maintenance downtime. The aftermarket application segment represents around 17%, largely driven by retrofitting needs in markets with older vehicle fleets. The fastest-growing application is in commercial vehicles, projected to expand at a CAGR of 11.1%, fueled by stricter safety norms, electrification of logistics fleets, and the rising demand for cost-efficient braking solutions in urban delivery operations.

In terms of consumer adoption, 45% of new passenger cars sold in North America in 2024 featured electronic parking brakes as a standard feature, compared with just 28% in 2019, highlighting rapid mainstreaming. Similarly, surveys reveal that over 52% of fleet managers in Europe plan to integrate electronically controlled braking systems into their vehicles by 2027 to enhance safety and operational efficiency.

Among end-users, original equipment manufacturers (OEMs) dominate the market, holding a 64% share, due to their central role in embedding electric parking brakes into factory production lines and meeting both regulatory and consumer-driven demands. Aftermarket channels account for 22%, primarily serving older vehicles and regions where retrofitting offers a cost-effective upgrade. Fleet operators, though smaller in share at 14%, are emerging as the fastest-growing end-user segment, with a projected CAGR of 10.9%, driven by the need to ensure vehicle safety, reduce accident risks, and comply with tightening logistics safety regulations.

Notably, nearly 40% of global automotive OEMs reported in 2024 that electronic parking brakes are now offered as standard in at least one major vehicle line, reflecting a clear trend toward premiumization and technology-driven differentiation. In addition, over 35% of urban fleet operators in Asia-Pacific indicated plans to transition to vehicles with electronic braking systems by 2028, citing lower long-term maintenance costs and enhanced driver safety as the main motivations.

Europe accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17.5% between 2025 and 2032.

Europe maintained its lead due to Germany, France, and the UK together producing over 5.2 million vehicles annually with high integration of electronic systems. Asia-Pacific, led by China, Japan, and South Korea, exceeded 6.8 million EPB-equipped vehicle installations in 2024, reflecting surging EV production and rising adoption of premium vehicle features. North America contributed 21% of the global share, supported by technological integration in SUVs and luxury vehicles, while South America and the Middle East & Africa collectively held 8% share, showing incremental adoption trends backed by government-led automotive modernization programs.

North America accounted for 21% of the global Electric Parking Brake Market in 2024, driven by strong demand in passenger cars, SUVs, and light trucks. Key industries such as automotive manufacturing, EV adoption, and logistics fleets are driving growth. Regulatory frameworks, including NHTSA safety mandates, are accelerating electronic integration. Technological advancements such as IoT-enabled EPB modules and predictive diagnostics are becoming standard features. Local players like BorgWarner are investing in advanced brake actuation systems to improve efficiency. Consumer behavior shows higher adoption in premium and electric vehicle segments, with 58% of U.S. buyers prioritizing enhanced braking safety features in new vehicle purchases.

Europe captured 38% market share in 2024, with Germany, the UK, and France being leading contributors due to their strong premium vehicle production and integration of advanced safety systems. The European Commission’s sustainability frameworks and UNECE regulations mandate electronic braking adoption across several categories, driving demand. Adoption of emerging technologies such as AI-based diagnostics and integration with autonomous driving platforms is widespread. Local players like Continental AG continue to expand investments in smart braking solutions. Consumer behavior in this region is heavily influenced by regulatory pressure, with 64% of buyers citing compliance with safety certifications as a key decision factor for adopting advanced braking systems.

Asia-Pacific ranked as the fastest-growing region, with over 6.8 million EPB-equipped vehicles deployed in 2024. China leads consumption, followed by Japan and South Korea, supported by large-scale EV and hybrid production. Regional manufacturing hubs focus on automation, robotics, and advanced materials to reduce costs and boost efficiency. Innovation hubs in China and Japan are pioneering AI-integrated EPBs for predictive safety. Local players such as Denso are actively expanding production lines for smart braking modules. Consumer behavior is shifting rapidly, with 72% of EV buyers in China preferring vehicles equipped with advanced EPBs, highlighting strong adoption linked to e-mobility expansion.

South America held 5% of the global Electric Parking Brake Market in 2024, led by Brazil and Argentina. The regional market benefits from government incentives to modernize fleets and expand automotive safety adoption. Infrastructure growth and trade policy reforms have opened opportunities for EPB integration in passenger vehicles and light commercial fleets. Brazil’s automotive industry alone produced over 2.3 million vehicles in 2024, with an increasing proportion featuring electronic braking. Local automotive suppliers are aligning with global OEMs to provide modular EPB solutions. Consumer behavior is evolving, with rising demand tied to connected vehicle services and localized safety preferences.

The Middle East & Africa contributed 3% of the Electric Parking Brake Market in 2024, with notable growth in UAE, Saudi Arabia, and South Africa. Regional demand is driven by diversification beyond oil, with focus on automotive modernization, smart mobility, and construction equipment integration. Technological modernization trends include adoption of mechatronics and advanced braking in commercial vehicles. Regulations encouraging safety compliance and cross-border trade partnerships have supported EPB adoption. Local manufacturers in South Africa are piloting assembly of electronic braking systems for export markets. Consumer behavior highlights strong acceptance of imported vehicles with integrated safety features, particularly in premium and SUV categories.

Germany – 22% Market Share: Strong production capacity in premium automotive segments with advanced integration of EPB systems.

China – 18% Market Share: High EV manufacturing output and widespread adoption of smart electronic braking technologies across passenger and commercial vehicles.

The competitive environment for the Electric Parking Brake Market is moderately consolidated, with top players commanding a large combined presence while numerous smaller firms compete for niche and aftermarket segments. There are more than 50 active competitors operating globally, but the top five—ZF Friedrichshafen, Continental AG, Astemo Ltd., Brembo N.V., and ADVICS Co. Ltd.—together hold approximately 77-87% of market influence. Major strategic initiatives include product launches (e.g., integrated electro-hydraulic and electro-mechanical brake systems by legacy suppliers), strategic partnerships (supplier-OEM deals across Asia and Europe), and acquisitions aimed at expanding actuator or brake-by-wire technology portfolios. Innovation trends influencing competition include weight-reduction in caliper designs, integration with ADAS and vehicle electrification, modular EPB architectures, and advances in software diagnostics. Some firms are expanding into regenerative braking integration, embedding smart sensors, and enhancing reliability in actuation components. OEM contracts with high-volume vehicle models are central competitive battlegrounds, as are low-cost solutions for entry and mid-segments versus performance solutions for premium vehicles. The nature of the market is becoming more dynamic as suppliers also face pressure on cost, part count, electric vehicle compatibility, and regulatory compliance.

Brembo N.V.

ADVICS Co. Ltd.

Hyundai Mobis Co. Ltd.

Valeo

Mando Corporation

WABCO Holdings Inc.

Aisin Seiki Co. Ltd.

Dura Automotive Systems

Current and emerging technologies in electric parking brake (EPB) systems are central to maintaining competitive advantage and meeting evolving vehicle design requirements. One major technology is the electro-hydraulic caliper architecture, which combines actuator motors, hydraulics, and electronic stability control, enabling EPBs to provide consistent braking force and better integration with ADAS modules. Motor-on-caliper and actuator designs are being optimized for weight reduction, with some new actuators achieving up to 15-20% lower mass compared with conventional assemblies. Brake-by-wire systems are another advancing field: fully electronic systems with no hydraulic lines in parking brake function are being piloted in some premium models, enabling better response times and smoother integration with electronic stability or autonomous parking features.

Sensor integration, including position sensors, temperature sensors, and diagnostic feedback loops, is becoming more sophisticated. For example, EPB modules now often include sensors that detect actuator wear, cable slack, or corrosion, enabling pre-emptive maintenance and alerting systems that reduce failure rates. Software and firmware development are also key: embedded microcontrollers are being upgraded to handle more functionalities—auto-hold, hill-start assist, remote parking, and fail-safe releases. Another important technology trend is modular EPB units that are standardized across multiple vehicle platforms to reduce development cost and inventory complexity. Also, manufacturers are exploring advanced materials in actuators and friction surfaces to improve durability under harsh conditions, including high humidity or temperature extremes. Finally, integration with electrified powertrains and compatibility with high-voltage systems is essential in EVs, leading to development of EPBs capable of handling regenerative braking interplay and safety isolation.

In June 2024, Bosch introduced an integrated electro-hydraulic braking system focused on SUVs and electric vehicles, designed to address complex weight distribution and improve system stability. Source: www.prnewswire.com

In April 2025, Standard Motor Products expanded its Electronic Parking Brake Actuator program to cover millions of late-model import and domestic vehicles, adding compatibility with recent models from Ford, Jeep, Ram, Mercedes-Benz, and Subaru. Source: www.thebrakereport.com

In October 2023, Aisin Seiki launched a new compact and lightweight EPB module tailored for electric vehicles, with mass production capacity targeted for implementation in 2024.

In December 2023, Continental AG unveiled its next-generation EPB system with an integrated automatic parking function, aimed at enhancing convenience features in passenger cars.

This Report covers the Electric Parking Brake Market from multiple angles, offering comprehensive insights into product types (such as cable-pull, electro-hydraulic caliper systems, and brake-by-wire architectures), applications (passenger cars, commercial vehicles, aftermarket retrofits, EV/hybrid vehicles), and end-user segments (OEMs, fleet operators, aftermarket suppliers). Geographically, the scope spans all major global regions: North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed focus on leading countries like Germany, China, U.S., Japan, and Brazil.

Included are technological domains such as actuator design, sensor integration, embedded software/firmware, modular EPB units, integration with ADAS, and emerging brake-by-wire systems. The report also examines industry focus areas including regulatory compliance, emissions/sustainability considerations, materials innovation, production capacity expansion, and supply chain resilience. Niche segments like high-performance EPBs, retrofits for older vehicle fleets, and aftermarket replacement actuator kits are addressed. The assessment includes recent product launches, local content requirements in manufacturing, infrastructure trends supporting EV production, and consumer preferences in key markets. Decision-makers can use these scope definitions to benchmark competitive strategy, plan investment, align product roadmaps, and assess technology adoption across regions and vehicle classes.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 300.0 Million |

| Market Revenue (2032) | USD 1,039.1 Million |

| CAGR (2025–2032) | 16.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | ZF Friedrichshafen AG, Continental AG, Astemo Ltd., Brembo N.V., ADVICS Co. Ltd., Hyundai Mobis Co. Ltd., Valeo, Mando Corporation, WABCO Holdings Inc., Aisin Seiki Co. Ltd., Dura Automotive Systems |

| Customization & Pricing | Available on Request (10% Customization is Free) |