Reports

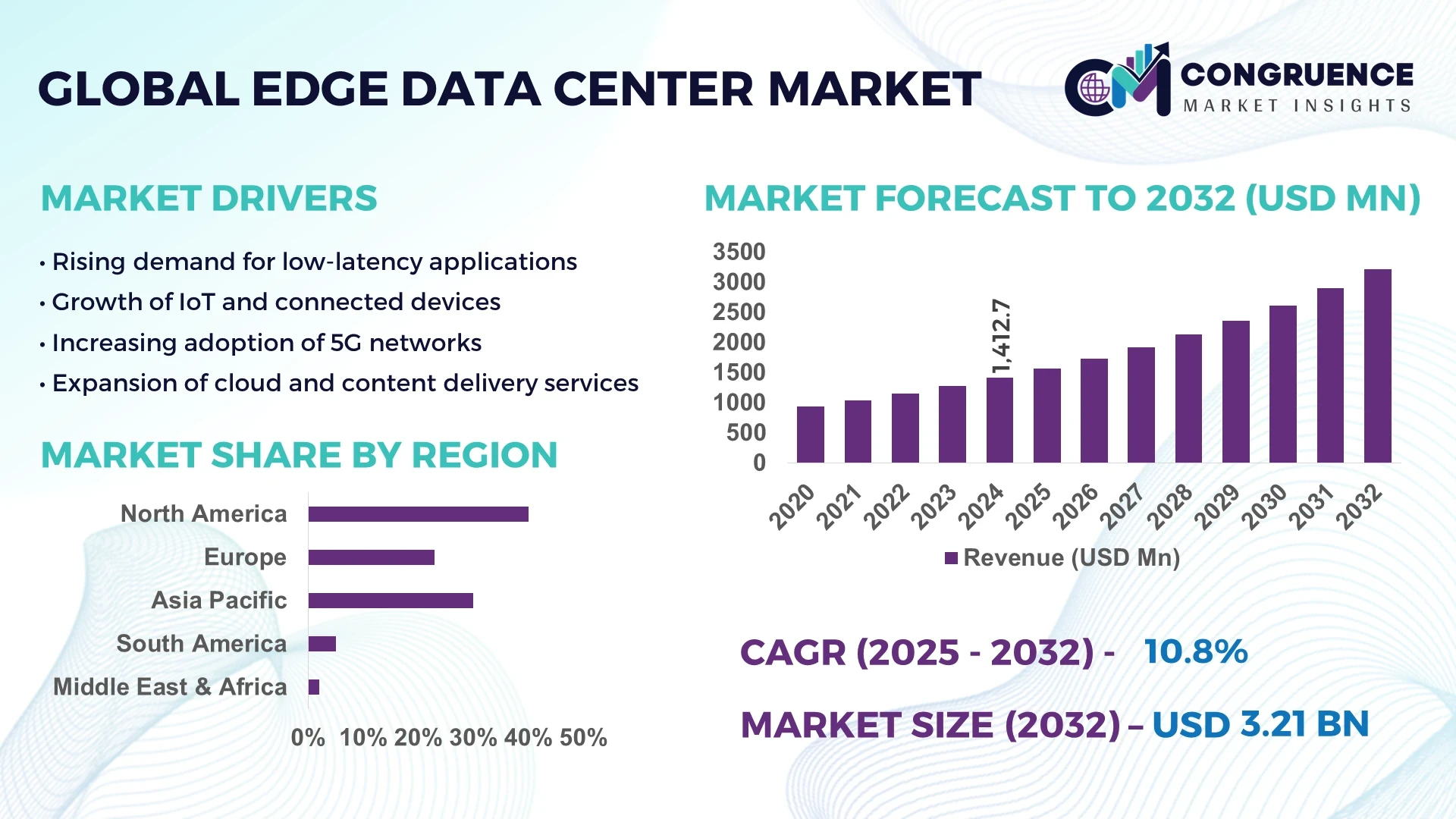

The Global Edge Data Center Market was valued at USD 1412.7 Million in 2024 and is anticipated to reach a value of USD 3208.98 Million by 2032 expanding at a CAGR of 10.8 % between 2025 and 2032.

North America, led by the United States, stands as the dominant force in this sector, with the region deploying a vast network of hyperscale micro-facilities and modular edge infrastructure. The U.S. has spearheaded initiatives to integrate energy-efficient cooling systems and advanced edge processing capabilities across industries such as telecommunications, healthcare, autonomous transportation, and smart city development.

Industry stakeholders across IT & telecom, healthcare, manufacturing, energy, BFSI, and government are collectively driving demand, with IT & telecom alone accounting for revenues measured in billions of dollars. Product innovations include modular micro data centers and AI-enhanced DCIM tools, while environmental and regulatory frameworks—such as GDPR and local energy efficiency mandates—shape design and deployment. Regional consumption varies: Asia-Pacific is surging with digital adoption and 5G rollout; Europe emphasizes data privacy; North America leverages investment and technological synergies. Emerging trends point to hybrid infrastructure strategies combining cloud and edge with sustainable operations, AI-enabled predictive maintenance, and the rise of decentralized architectures tailored to real-time processing demands and localized data sovereignty.

The Edge Data Center Market is undergoing profound transformation driven by AI-enabled optimization and advanced workload handling. AI integration is enhancing operational performance through intelligent resource allocation, predictive maintenance, and real-time process automation. Data centers are increasingly utilizing AI systems to monitor thermal conditions and optimize cooling dynamically, reducing energy waste and improving efficiency. Furthermore, AI-powered network management solutions are enhancing data traffic flow and minimizing latency, resulting in faster, more reliable service delivery at the edge.

In hyperscale and enterprise edge environments, AI-based analytics are enabling continuous assessment of performance metrics, identifying potential hardware failures before they occur and scheduling maintenance proactively. This shift toward autonomous management is reducing operational downtime and improving uptime reliability—critical for mission-critical applications like autonomous vehicles and real-time industrial control. AI is also optimizing task offloading between central and edge nodes, ensuring workloads are processed most efficiently based on latency, energy, and bandwidth considerations.

Concrete investments reflect this trend: companies like Schneider Electric and Nvidia have collaborated to introduce reference architectures capable of handling racks with up to 132 kW of load, reducing cooling energy consumption by approximately 20 % and accelerating development timelines by about 30 %, reflecting substantial gains in both efficiency and cost effectiveness. Energy demand projections highlight that AI-driven operations will significantly increase electricity needs, prompting edge facilities to adopt smarter energy distribution and renewable integration strategies to balance demand and sustainability. These developments demonstrate how AI is reshaping not only service delivery but also infrastructure design in the Edge Data Center Market.

“Enhanced AI as a Service at the Edge via Transformer Network,” a 2025 study, reports that applying a transformer-based model for offloading deep neural network inference tasks like ResNet and VGG16 to edge servers improved energy efficiency by 18 % and significantly reduced task failure rates when resources were constrained.”

The Edge Data Center Market is shaped by rapid digital transformation, the growth of 5G networks, and increasing adoption of IoT devices that demand localized data processing. Enterprises across telecom, healthcare, manufacturing, and finance are driving strong adoption of distributed computing infrastructures, emphasizing low-latency performance and data security. Investment in modular and containerized solutions is rising, enabling faster deployment and scalability. Industry focus on sustainability and energy-efficient cooling systems is accelerating innovation, as operators seek to align with environmental standards. The market is also influenced by regional regulations concerning data sovereignty, stimulating the need for localized infrastructure in both developed and emerging economies.

The rollout of 5G infrastructure is a critical driver for the Edge Data Center Market, as telecom operators and enterprises require localized processing to handle vast data traffic volumes. 5G generates high-bandwidth applications including autonomous vehicles, immersive AR/VR, and industrial IoT, all of which rely on sub-10 millisecond latency. Edge facilities strategically positioned near end users help manage these requirements effectively. Reports indicate that by 2025, global 5G connections will surpass 4.6 billion, substantially boosting demand for micro and modular data centers. This integration reduces congestion on core networks and ensures smoother service delivery, making edge deployments indispensable for digital ecosystems.

One of the significant restraints affecting the Edge Data Center Market is the high operational expenditure tied to energy use and maintenance. Edge facilities often run in distributed, smaller formats, requiring advanced cooling technologies and backup power solutions to maintain uptime. Studies highlight that data centers consume around 1–1.5 % of global electricity, with edge sites adding incremental load due to proximity deployment. This cost burden makes scaling difficult for smaller enterprises. Additionally, compliance with sustainability mandates such as carbon reduction frameworks further raises investment needs, creating barriers for widespread adoption in certain regions.

The increasing development of smart cities and widespread IoT adoption presents a substantial opportunity for the Edge Data Center Market. Governments and enterprises are investing in localized infrastructure to power real-time applications like traffic management, energy grids, and public safety systems. Forecasts suggest that the number of connected IoT devices will exceed 29 billion by 2030, intensifying the need for distributed edge processing nodes. Edge facilities reduce latency and enhance reliability for these mission-critical applications. Strategic collaborations between municipalities, telecom providers, and cloud vendors create favorable conditions for scalable deployments, unlocking new revenue streams and regional infrastructure growth.

A major challenge for the Edge Data Center Market is ensuring data security and compliance across diverse regulatory environments. Unlike centralized facilities, edge deployments are dispersed across multiple geographies, exposing them to varied jurisdictional requirements. Compliance with frameworks such as GDPR, HIPAA, or regional cybersecurity laws requires tailored solutions that add complexity and cost. Furthermore, edge sites are often located in less secure or remote environments, increasing vulnerability to breaches. Industry data shows that cyberattacks targeting distributed IT infrastructure rose by over 30 % in 2024, underlining the heightened risk. Addressing these issues requires robust encryption, zero-trust models, and continuous monitoring, all of which add operational strain.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction is gaining momentum in the Edge Data Center Market. Prefabricated units are assembled off-site and transported to deployment locations, reducing construction timelines by nearly 50 % compared to traditional builds. Automated cutting and pre-bent components ensure precision and minimize labor costs, which is increasingly valuable in Europe and North America where skilled labor shortages persist. This trend is enabling faster scalability for telecom and enterprise operators who require rapid deployment of localized infrastructure.

• Integration of Liquid Cooling Technologies: Liquid cooling solutions are emerging as a vital trend, particularly as edge facilities face growing power density challenges. Data shows that racks in edge deployments are now exceeding 40 kW, making traditional air cooling less effective. Immersion and direct-to-chip liquid cooling systems are improving energy efficiency by up to 30 %, enabling operators to meet sustainability targets. Adoption is rising in Asia-Pacific and North America, where demand for high-performance computing workloads such as AI inference and video analytics is expanding rapidly.

• Growth of Renewable-Powered Edge Sites: Sustainability concerns are driving a shift toward renewable-powered edge facilities. Operators are integrating solar panels, wind turbines, and energy storage solutions into micro data center architectures. Recent deployments in Europe indicate that renewable integration has cut operational emissions by up to 35 %. As edge data centers scale globally, reliance on renewable energy ensures compliance with carbon neutrality targets and strengthens resilience against grid fluctuations, offering both cost and environmental benefits.

• AI-Driven DCIM Adoption: AI-enabled Data Center Infrastructure Management (DCIM) tools are transforming edge operations by providing real-time monitoring and predictive analytics. Operators leveraging AI-based DCIM report up to 25 % improvements in asset utilization and significant reductions in downtime incidents. These platforms optimize workload distribution, automate thermal management, and enhance fault detection, particularly in distributed facilities. With the surge in IoT devices and 5G networks, AI-based management is becoming essential to maintain efficiency and reliability across decentralized edge infrastructures.

The Edge Data Center Market is segmented by type, application, and end-user, reflecting diverse demand across industries. Types include hyperscale edge facilities, micro data centers, and modular containerized solutions, each catering to specific deployment models. Applications span telecom, smart cities, healthcare, manufacturing, and BFSI, with each sector leveraging edge computing for latency-sensitive tasks. End-user insights highlight strong adoption by IT and telecom operators, followed by growing uptake in industrial enterprises and government agencies. Segmentation reveals how different stakeholders drive demand, with leading categories focusing on speed, scalability, and data sovereignty, while emerging segments prioritize sustainability and advanced AI integration.

Hyperscale edge data centers remain a dominant type, serving large enterprises and telecom providers that require massive processing capabilities at distributed sites. Their adoption is propelled by the surge in 5G rollouts and the demand for high-bandwidth applications such as AR/VR and AI-powered analytics. Micro data centers represent the fastest-growing segment, driven by their portability, small footprint, and ability to provide localized computing in remote or urban areas. These facilities are particularly favored in regions deploying smart infrastructure and IoT ecosystems. Modular containerized edge solutions hold a niche but valuable role, offering rapid deployment and flexibility for disaster recovery, temporary events, or military operations. While hyperscale leads in scale and processing power, micro data centers are reshaping deployment strategies by providing cost-efficient, low-latency options tailored for real-time use cases.

Telecom applications lead the Edge Data Center Market, as operators integrate edge computing to manage high volumes of mobile data traffic and ensure ultra-low latency for 5G services. The demand for faster connectivity and real-time analytics has made telecom operators the primary adopters of edge facilities. Smart cities are emerging as the fastest-growing application segment, with initiatives focusing on connected traffic systems, energy grids, and surveillance requiring distributed computing power. Healthcare is another significant contributor, utilizing edge solutions for remote patient monitoring, medical imaging, and AI-assisted diagnostics where real-time data processing is crucial. Manufacturing leverages edge facilities for predictive maintenance and automation, while BFSI institutions adopt them to enhance cybersecurity and support advanced digital banking services. These diverse applications highlight the wide-ranging relevance of edge computing across industries and the growing reliance on localized data processing.

IT and telecom companies form the leading end-user segment, driven by their heavy reliance on edge infrastructure to support 5G, cloud integration, and large-scale data traffic management. Their investments in high-performance and modular edge deployments underscore their position as primary contributors to market expansion. Industrial enterprises represent the fastest-growing end-user group, as Industry 4.0 adoption accelerates across automotive, electronics, and energy sectors. These businesses depend on edge facilities for real-time automation, robotics, and IoT-driven production optimization. Government agencies also play a crucial role, particularly in the deployment of smart city projects and secure defense communication networks. Healthcare providers, though smaller in scale, are increasingly integrating edge solutions to enhance patient care and reduce data latency in critical applications. The collective growth across end-users demonstrates how edge infrastructures are becoming indispensable for both commercial and public sector digital transformation initiatives.

North America accounted for the largest market share at 40% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 22% between 2025 and 2032.

North America’s dominance is attributed to its advanced technological infrastructure, high adoption rates of authentication solutions across sectors like banking, healthcare, and government, and stringent regulatory frameworks ensuring data security. Conversely, Asia-Pacific's rapid growth is driven by increasing digitalization, rising cyber threats, and significant investments in cybersecurity technologies, particularly in countries like China and India.

Secure Digital Transformation in North America

North America led the global authentication services market in 2024, accounting for approximately 40% of the total market share. The region's robust demand is primarily driven by the banking, financial services, and insurance (BFSI) sector, which emphasizes secure digital transactions and compliance with stringent data protection regulations. Technological advancements, such as the integration of artificial intelligence and machine learning in authentication processes, are enhancing security measures and operational efficiency. Government initiatives promoting digital identity solutions further bolster market growth, positioning North America as a leader in authentication services.

Regulatory Compliance Fuels Market Growth in Europe

Europe's authentication services market is characterized by a strong emphasis on regulatory compliance and data protection. Countries like Germany, the United Kingdom, and France are at the forefront, driven by stringent regulations such as the General Data Protection Regulation (GDPR) and the eIDAS regulation. These regulations mandate secure authentication mechanisms across various sectors, including finance, healthcare, and public services. The adoption of multi-factor authentication (MFA) and biometric solutions is increasing, aligning with the region's commitment to enhancing cybersecurity and protecting user data.

Rapid Digitalization Accelerates Authentication Services in Asia-Pacific

Asia-Pacific's authentication services market is experiencing significant growth, with countries like China, India, and Japan leading the charge. The region's rapid digitalization, coupled with increasing internet penetration and mobile device usage, is driving the demand for secure authentication solutions. The rise in cyber threats and data breaches has prompted governments and enterprises to invest heavily in advanced authentication technologies. Additionally, initiatives promoting digital identities and smart city projects are further propelling the adoption of authentication services across the region.

Emerging Markets Drive Authentication Services Growth in South America

South America's authentication services market is witnessing steady growth, primarily driven by key countries such as Brazil and Argentina. The increasing adoption of digital platforms in sectors like banking, e-commerce, and government services is fueling the demand for secure authentication solutions. Government initiatives aimed at enhancing digital infrastructure and promoting cybersecurity are contributing to market expansion. While challenges like economic instability and infrastructure limitations exist, the overall trend indicates a positive outlook for authentication services in the region.

Strategic Investments Boost Authentication Services in Middle East & Africa

The Middle East & Africa region is experiencing a growing demand for authentication services, driven by major growth countries such as the United Arab Emirates and South Africa. Key industries like oil & gas, construction, and government services are increasingly adopting secure authentication solutions to protect sensitive data and ensure compliance with international standards. Technological modernization trends, including the implementation of smart technologies and digital transformation initiatives, are further accelerating the adoption of authentication services. Local regulations and trade partnerships are also playing a pivotal role in shaping the market dynamics of the region.

United States Market Share: 35%

Reason: High production capacity and strong end-user demand in sectors like BFSI and government services.

China Market Share: 25%

Reason: Rapid digitalization and significant investments in cybersecurity technologies.

The Authentication Services market is highly competitive, featuring over 50 active global players ranging from large multinational corporations to innovative technology startups. Companies are strategically positioning themselves through product launches, partnerships, acquisitions, and collaborations to expand their footprint across key industries such as banking, healthcare, government, and enterprise IT. Innovation is a central driver of competition, with firms investing heavily in AI-based authentication, biometric verification, and passwordless login solutions to differentiate their offerings. Several market participants are focusing on enhancing cloud-based authentication services to meet growing demand for scalable and flexible solutions. Regional expansions, regulatory compliance solutions, and cybersecurity integrations further influence market dynamics. Companies are also emphasizing user experience, seamless integration, and interoperability of authentication solutions, which has become a key determinant in market positioning. The competitive landscape is continually evolving as firms leverage technology and strategic initiatives to maintain or gain market leadership.

International Business Machines Corporation (IBM)

Cisco Systems, Inc.

RSA Security LLC

Gemalto (Thales Group)

HID Global

OneLogin, Inc.

CyberArk Software Ltd.

The Authentication Services market is experiencing a significant technological transformation, driven by advancements aimed at enhancing security and user experience. One of the most notable developments is the widespread adoption of passwordless authentication methods. This approach leverages biometrics, such as facial recognition and fingerprint scanning, to authenticate users without the need for traditional passwords. These methods not only improve security by reducing the risk of password theft but also streamline the user experience by eliminating the need to remember complex passwords. Another emerging trend is the integration of behavioral biometrics into authentication systems. This technology analyzes patterns in user behavior, such as typing speed, mouse movements, and navigation habits, to create unique user profiles. By continuously monitoring these behaviors, systems can detect anomalies that may indicate fraudulent activity, providing an additional layer of security.

The rise of multi-factor authentication (MFA) is also shaping the market. MFA requires users to provide two or more verification factors—something they know (password), something they have (security token), or something they are (biometric data)—to gain access to systems. This approach significantly enhances security by adding multiple barriers against unauthorized access. Cloud-based authentication solutions are gaining traction as organizations move their operations to the cloud. These solutions offer scalability, flexibility, and centralized management, making it easier for businesses to secure access to their applications and data across various devices and platforms. The shift towards cloud services necessitates robust authentication mechanisms to protect sensitive information and ensure compliance with data protection regulations.

In October 2024, the FIDO Alliance introduced the Credential Exchange Protocol (CXP) to standardize the secure transfer of passkeys between platforms, aiming to enhance user convenience and security.

In November 2024, major tech companies, including Google, Apple, and Microsoft, expanded support for passkeys, allowing users to authenticate using biometric data or PINs, reducing reliance on traditional passwords.

In December 2024, the UK government approved the use of digital passkeys across its digital services, signaling a move towards passwordless authentication to bolster cybersecurity.

In January 2025, Microsoft announced that all new accounts would default to passkeys, eliminating the need for passwords and enhancing login efficiency and security.

The Authentication Services Market Report provides an extensive and structured overview of the market, highlighting its breadth across technologies, sectors, and regions. It examines various authentication methods, including multi-factor authentication, biometric verification such as facial and fingerprint recognition, passwordless solutions, and emerging behavioral authentication techniques. The report also details the deployment of these technologies across key industry sectors, including banking, financial services, healthcare, government, IT and telecommunications, retail, and education. Regional insights include detailed analysis of North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with data on adoption trends, volume-based market shares, and growth drivers. The report also evaluates the influence of regulatory frameworks, such as GDPR, eIDAS, and digital identity initiatives, which shape market adoption strategies and compliance requirements. Additionally, it identifies emerging trends in cloud-based authentication, AI-powered security, decentralized identity solutions, and passwordless technologies. Niche markets, such as small and medium enterprises (SMEs), smart cities, and IoT-enabled applications, are examined to highlight untapped opportunities. With detailed coverage of technologies, end-users, applications, and regional dynamics, the report equips stakeholders and business leaders with actionable insights for strategic planning, investment decisions, and technology adoption, enabling informed navigation of the evolving global authentication services landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1412.7 Million |

|

Market Revenue in 2032 |

USD 3208.98 Million |

|

CAGR (2025 - 2032) |

10.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Schneider Electric, Equinix Inc., NVIDIA Corporation, Vertiv Holdings Co, Dell Technologies, IBM Corporation, Huawei Technologies Co. Ltd., Hewlett Packard Enterprise (HPE), Cisco Systems Inc., EdgeConneX |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |