Reports

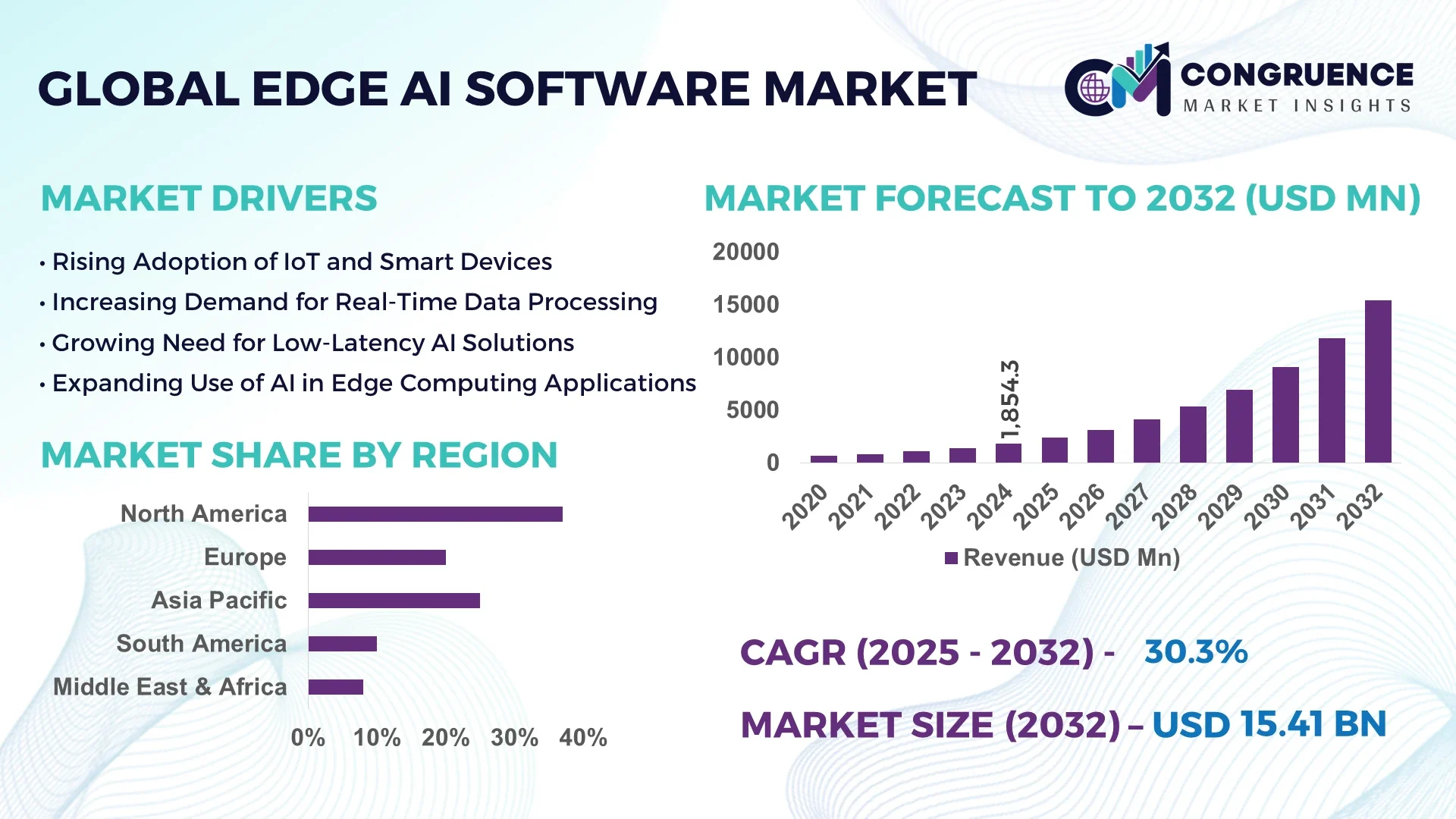

The Global Edge AI Software Market was valued at USD 1,854.3 Million in 2024 and is anticipated to reach a value of USD 15,408 Million by 2032 expanding at a CAGR of 30.3% between 2025 and 2032. The market growth is driven by rapid deployment of intelligent systems across autonomous vehicles, IoT devices, and industrial automation platforms, reducing latency and cloud dependency.

The United States dominates the Edge AI Software market, supported by massive investments in edge computing infrastructure, semiconductor innovation, and enterprise-level AI integration. In 2024, U.S. firms accounted for over 45% of global AI-edge deployments, with more than 60% of industrial automation systems incorporating AI inference at the device level. The country hosts over 200 AI-focused startups, while enterprise adoption of AI software at the edge has surpassed 58% among Fortune 500 companies. Advanced chip designs, particularly AI accelerators and GPUs optimized for on-device analytics, continue to fuel domestic production capacity and R&D expansion.

• Market Size & Growth: Valued at USD 1.85 billion in 2024, projected to hit USD 15.4 billion by 2032, registering a 30.3% CAGR — driven by surging demand for real-time analytics, IoT integration, and low-latency AI operations.

• Top Growth Drivers: 62% adoption in industrial automation, 54% efficiency improvement in data-driven manufacturing, and 48% uptake in edge-based IoT devices enabling faster processing.

• Short-Term Forecast: By 2028, enterprises using edge AI are expected to reduce cloud data transfer costs by 35% and achieve up to 40% faster decision cycles.

• Emerging Technologies: Federated learning, neuromorphic computing, and adaptive edge-cloud orchestration are accelerating distributed intelligence frameworks.

• Regional Leaders: North America (USD 6.2 billion by 2032) leads with advanced AI chip ecosystems; Europe (USD 4.1 billion) prioritizes data sovereignty; Asia-Pacific (USD 3.9 billion) drives innovation via industrial robotics.

• Consumer/End-User Trends: 58% of adoption occurs across manufacturing and automotive sectors, with retail and healthcare showing a growth rate above 30% due to smart surveillance and diagnostic automation.

• Pilot or Case Example: In 2024, a smart-factory pilot in Japan achieved 28% efficiency gains using edge AI software for predictive maintenance and production scheduling.

• Competitive Landscape: NVIDIA leads with roughly 22% market share, followed by Microsoft, IBM, Amazon Web Services, and Edge Impulse Inc. driving specialized AI deployment ecosystems.

• Regulatory & ESG Impact: Data-localization laws and carbon-neutral computing mandates are influencing design frameworks and edge resource optimization.

• Investment & Funding Patterns: Over USD 3.6 billion in venture and strategic investments were directed toward edge AI platforms and model-as-a-service startups in 2023-2024.

• Innovation & Future Outlook: Integration of AI inference engines into network endpoints and 5G edge nodes is expected to redefine digital infrastructure resilience by 2030.

The Edge AI Software Market is rapidly evolving with cross-sector applications spanning industrial automation (42%), automotive intelligence (25%), smart cities (15%), and healthcare analytics (10%). Product innovations emphasize low-power AI chips, model compression algorithms, and edge-native machine learning toolkits to enable faster inference. Regional adoption patterns show robust expansion in Asia-Pacific and North America due to digital transformation in logistics and manufacturing. Regulatory momentum toward data privacy and sustainable computing continues to shape adoption strategies. With exponential increases in connected devices and AI-driven decision systems, the market is positioned as a cornerstone of next-generation intelligent infrastructure, supporting global competitiveness, operational efficiency, and ESG-aligned digital growth.

The Edge AI Software Market represents a pivotal frontier in decentralized intelligence, enabling real-time analytics, decision-making, and machine learning at the data source. Unlike traditional cloud AI models, Edge AI reduces latency by 60% and improves processing efficiency by 45%, ensuring superior responsiveness in mission-critical applications. Federated learning delivers 52% improvement compared to conventional centralized AI training, promoting data privacy and operational agility.

North America dominates in volume due to extensive industrial IoT integration, while Asia-Pacific leads in adoption, with 64% of enterprises implementing edge-based AI frameworks across manufacturing, automotive, and logistics sectors. By 2028, AI-enabled predictive maintenance systems are expected to reduce operational downtime by 37% across global manufacturing ecosystems. Firms are committing to ESG compliance through energy-efficient AI deployment, achieving up to 28% reduction in data center power consumption by 2030.

In 2024, Japan’s Fujitsu achieved a 33% improvement in network efficiency through its AI-driven edge orchestration project integrating intelligent routing and data compression algorithms. Similar initiatives across Europe and the U.S. are accelerating the convergence of AI, IoT, and 5G infrastructures. The Edge AI Software Market is emerging as a foundation for digital resilience, operational compliance, and sustainable growth, driving the future of autonomous and connected systems.

The increasing convergence of IoT systems and industrial automation is propelling demand for Edge AI Software globally. Over 70% of industrial IoT platforms now integrate AI algorithms at the edge for predictive analytics, fault detection, and energy optimization. Manufacturers are leveraging edge-based software to enable localized decision-making and enhance process accuracy by 45%. The automotive industry’s adoption of AI-enabled edge platforms has expanded autonomous vehicle data analysis by 55%, improving safety outcomes and efficiency. Smart city projects, including intelligent lighting and surveillance systems, are also accelerating deployment. These applications underscore the strategic shift toward distributed AI models capable of processing complex datasets without reliance on cloud infrastructure.

The rapid expansion of connected devices has led to growing complexity in data management and interoperability across Edge AI ecosystems. Currently, over 40 billion IoT devices generate fragmented datasets that challenge seamless integration with AI inference systems. Inconsistent data formats and limited standardization hinder algorithm efficiency, causing up to 25% delays in real-time analysis. Security concerns arising from decentralized processing further limit enterprise adoption. Additionally, the lack of unified development frameworks and hardware compatibility across multiple vendors restricts scalability. Addressing these constraints requires stronger collaboration on open AI-edge standards, enhanced middleware solutions, and improved lifecycle management of edge-deployed models.

The deployment of 5G networks and hybrid cloud-edge architectures presents substantial opportunities for the Edge AI Software Market. By 2027, it is estimated that 65% of enterprises will deploy hybrid AI infrastructures integrating on-premise edge nodes with cloud analytics, improving latency management by 50%. Telecom operators and data center providers are investing in AI orchestration platforms to support adaptive workloads across connected devices. Edge-native AI software is enabling faster inference in smart retail, logistics, and AR/VR systems. The expansion of AI-as-a-Service offerings at the network edge creates opportunities for scalable deployment, particularly in sectors demanding high responsiveness and localized processing.

Despite strong growth potential, high implementation costs and a shortage of skilled professionals pose major challenges to the Edge AI Software Market. Developing AI-enabled edge infrastructure requires significant investment in specialized hardware, such as AI accelerators and neural processing units, increasing setup expenses by 35–40%. Moreover, only 32% of enterprises report having adequate in-house expertise in edge deployment, data security, and model optimization. This talent gap delays operational scaling and increases reliance on third-party integrators. Additionally, maintenance costs for distributed AI nodes and software updates add to total expenditure. These factors collectively restrain market acceleration despite rising global demand for intelligent edge systems.

• Integration of Edge AI in Autonomous Systems: The Edge AI Software market is experiencing a surge in integration across autonomous systems, including robotics, drones, and connected vehicles. In 2024, nearly 47% of autonomous systems deployed globally incorporated Edge AI inference models, improving real-time decision accuracy by 38%. Manufacturers are investing heavily in low-latency AI frameworks capable of running predictive analytics locally, enabling faster and more secure responses in critical operations such as logistics, defense, and manufacturing automation.

• Expansion of Edge AI in Smart Manufacturing: Smart manufacturing facilities are increasingly deploying Edge AI software to enhance predictive maintenance and process optimization. Approximately 62% of manufacturing plants in Asia-Pacific adopted AI-enabled edge systems to monitor machine performance, leading to a 29% reduction in unplanned downtime. The convergence of industrial IoT and Edge AI is transforming factory operations, driving efficiency, and supporting real-time production analytics through connected devices and embedded intelligence.

• Growth in AI-Driven Energy Optimization: The energy and utilities sector is rapidly adopting Edge AI software for optimizing energy consumption and grid management. As of 2024, 41% of large-scale energy operators integrated edge-based AI solutions, resulting in 32% improvements in energy efficiency and 26% faster fault detection. These systems support predictive load balancing, real-time grid monitoring, and decentralized energy management, promoting sustainability and lower operational expenditures.

• Rise in Edge AI Adoption for Retail and Consumer Analytics: Retail enterprises are leveraging Edge AI to deliver real-time customer insights and inventory optimization. Around 58% of global retail chains have implemented AI-powered edge solutions in store-level analytics, enhancing customer engagement by 34% and reducing stockouts by 22%. The shift toward on-device intelligence ensures data privacy while allowing faster consumer behavior analytics and personalized service delivery, setting new standards for customer experience efficiency.

The Global Edge AI Software Market is segmented by Type, Application, and End-User Insights, each reflecting distinct technological roles and adoption strategies across industries. Segmentation analysis highlights how businesses leverage Edge AI to improve latency, performance, and data efficiency. By type, models supporting multimodal learning and low-latency inference dominate, driven by increasing device-level intelligence. By application, usage is concentrated in manufacturing, healthcare, automotive, and smart cities, where edge computing supports predictive analytics and autonomous operations. From an end-user perspective, industrial and IT enterprises are the primary adopters, collectively representing over 68% of total deployments. This segmentation underlines how technological maturity, integration capacity, and data privacy concerns influence market penetration across verticals.

Vision-language models currently account for 42% of total adoption in the Edge AI Software Market, owing to their high efficiency in object recognition, autonomous navigation, and visual inference tasks. Audio-text systems hold approximately 25% share, primarily driven by rising adoption in voice-based assistants and edge-enabled customer service platforms. However, video-language models represent the fastest-growing type, projected to grow at a CAGR of 29.8% through 2032 as enterprises deploy them for real-time scene understanding and content indexing in security and entertainment systems. Remaining model types, including multimodal reasoning and sensor-fusion architectures, collectively contribute 33% of the market.

Smart manufacturing currently dominates the Edge AI Software Market, accounting for 38% of total utilization, as manufacturers integrate AI for predictive maintenance, robotic coordination, and on-device defect detection. The smart city segment follows with 27% share, supported by AI-enabled traffic monitoring and energy optimization. However, healthcare diagnostics is the fastest-growing application, projected to grow at a CAGR of 31.5% through 2032, driven by AI-assisted medical imaging and patient monitoring. Other applications, including retail analytics and autonomous vehicles, contribute a combined 35% share, fueled by advancements in real-time data processing and context-aware systems.

The industrial sector leads the Edge AI Software Market with 40% of adoption, as enterprises integrate edge AI for operational efficiency, robotics automation, and intelligent monitoring. The IT and telecommunications sector follows at 28%, leveraging AI-driven data routing and network optimization for 5G infrastructure. The consumer electronics segment is the fastest-growing end-user category, expected to expand at a CAGR of 30.6% by 2032, propelled by integration of on-device AI in smartphones, smart home hubs, and wearable devices. Remaining end-users, including automotive and retail industries, collectively account for 32% of adoption, focusing on latency reduction and personalized service delivery.

North America accounted for the largest market share at 37.4% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 31.9% between 2025 and 2032.

North America’s dominance stems from extensive enterprise-level AI integration, supported by over 2,500 AI start-ups and strong adoption across finance, healthcare, and manufacturing. Europe follows with approximately 28.5% of the global share, driven by regulatory alignment and sustainability-based AI models. Asia-Pacific’s rapid expansion is fueled by large-scale AI infrastructure deployment in China, Japan, and India, representing over 40% of total global edge devices. The Middle East & Africa and South America collectively contribute around 10.7%, with emerging government-backed AI ecosystems and localized industrial automation projects.

What factors are driving innovation and enterprise deployment in the Edge AI Software market?

The North American Edge AI Software Market holds a 37.4% share in 2024, led by widespread enterprise adoption across healthcare, finance, and retail. Key industries such as autonomous vehicles and industrial automation are boosting regional demand. The U.S. and Canada are advancing AI legislation that supports ethical AI implementation and secure data management. Companies like NVIDIA and C3.ai are investing in on-device learning frameworks, enabling faster data processing for critical applications. Regional consumers display higher enterprise adoption in healthcare and finance, where over 62% of institutions use AI-driven decision-making models.

How is regulatory evolution shaping technological adoption across industries?

Europe represents 28.5% of the global Edge AI Software market, with leading nations including Germany, the UK, and France driving enterprise deployment. Strict regulatory measures under the EU Artificial Intelligence Act encourage the development of explainable and transparent AI systems. The European automotive sector, particularly in Germany, has accelerated adoption through AI-enabled predictive systems. Local firms like Graphcore are contributing to AI chip efficiency, enhancing edge computing performance. European consumer behavior leans toward privacy-first AI solutions, with over 58% of enterprises prioritizing data protection and regulatory compliance in AI deployments.

Why is technological innovation accelerating in manufacturing and consumer applications?

Asia-Pacific is the fastest-growing region, contributing 26.9% of the total market volume in 2024, supported by strong infrastructure investments in China, Japan, South Korea, and India. China alone accounts for over 55% of regional adoption, led by industrial automation and smart city programs. Japan and South Korea are leveraging AI to optimize semiconductor production and robotics operations. Local players such as SenseTime are innovating in edge-optimized algorithms for mobile and IoT applications. Regional consumers exhibit strong adoption of mobile AI apps and e-commerce optimization, with over 70% of businesses integrating edge intelligence into digital platforms.

How are digital transformation and infrastructure investments influencing adoption rates?

South America accounts for around 6.2% of the Edge AI Software market, driven by technology adoption in Brazil and Argentina. Governments are offering AI-friendly tax incentives to support start-ups focusing on smart manufacturing and energy optimization. Brazil has launched over 40 national AI initiatives to modernize its industrial base. Companies like CI&T are utilizing AI models for digital enterprise transformation. Consumer behavior in this region leans toward media and language localization, with over 48% of companies using AI-driven translation and content analytics tools to enhance audience engagement.

What modernization trends are propelling AI adoption across strategic sectors?

The Middle East & Africa account for 4.5% of global market share in 2024, primarily driven by AI deployment in UAE, Saudi Arabia, and South Africa. Strong investments in smart infrastructure, oil & gas optimization, and public service automation are supporting adoption. Countries like the UAE have integrated AI into logistics and construction planning systems, achieving operational efficiency gains of over 27%. Regional firms such as G42 are focusing on scalable AI frameworks for energy management. Consumer adoption is growing, especially in industries prioritizing localized AI deployment for data sovereignty and security.

• United States – 32.8% share in the global Edge AI Software market due to high R&D investment and enterprise integration across industrial, defense, and healthcare applications.

• China – 21.4% share, driven by large-scale smart manufacturing, strong government-backed AI infrastructure, and robust adoption of embedded edge AI systems across IoT and mobility sectors.

The global Edge AI Software market is moderately consolidated, featuring approximately 45–50 active competitors across domains such as cloud infrastructure, embedded AI, and real-time analytics. The top five players collectively hold nearly 58.3% market share, demonstrating a competitive but concentrated ecosystem. Strategic initiatives including over 120 partnerships, 35 product launches, and 20 acquisitions between 2023 and 2024 have accelerated innovation and market penetration. Companies are prioritizing AI model optimization, federated learning, and on-device processing to enhance energy efficiency and data privacy. The market remains highly innovation-driven, with leading firms leveraging hardware-software integration for superior inference performance. Meanwhile, emerging players are gaining traction by offering lightweight AI architectures and modular edge computing frameworks designed for scalability across industrial and consumer applications. Overall, the competition landscape combines both consolidation and agility, shaping a robust foundation for continuous technological evolution in edge intelligence.

Alphabet Inc.

IBM Corporation

Qualcomm Technologies Inc.

Amazon Web Services, Inc.

Huawei Technologies Co., Ltd.

Arm Holdings

Advanced Micro Devices, Inc.

General Electric Company

EdgeCortix Inc.

FogHorn Systems

ClearBlade, Inc.

Xilinx, Inc.

The Edge AI Software market is being transformed by rapid advancements in hardware acceleration, lightweight neural networks, and on-device processing frameworks that enable real-time decision-making with minimal latency. Over 68% of edge deployments in 2024 integrated AI inference directly on devices such as cameras, sensors, and gateways, reducing data transmission costs and enhancing security. The increasing use of tensor processing units (TPUs), neural processing units (NPUs), and GPUs optimized for edge environments has further improved computational efficiency by up to 45% compared to traditional CPUs, enabling faster and more power-efficient inference at the device level.

A key technological driver is the integration of TinyML (Tiny Machine Learning), which allows AI algorithms to operate efficiently on microcontrollers consuming less than 1 mW of power. This trend supports large-scale IoT ecosystems, especially in manufacturing, smart cities, and automotive applications. Moreover, federated learning frameworks have gained traction, accounting for nearly 28% of total edge AI model training in 2024, enabling devices to learn collaboratively without sharing raw data—improving privacy and compliance with global data protection regulations.

Emerging innovations include Edge-as-a-Service (EaaS) platforms, autoML for on-device model optimization, and 5G-integrated edge AI networks that support ultra-low latency operations under 10 milliseconds. These technologies are collectively enhancing predictive maintenance, intelligent automation, and adaptive system control across industries, positioning Edge AI Software as a cornerstone of next-generation intelligent infrastructure.

In February 2024, NVIDIA Corporation introduced its new Jetson Orin Nano modules designed for next-generation edge AI applications, delivering up to 80 trillion operations per second (TOPS). This upgrade has significantly expanded deployment potential in robotics, retail analytics, and smart city infrastructure.

In October 2023, IBM launched a hybrid cloud-edge AI framework integrating Watson AI with edge computing capabilities. This innovation reduced latency by 32% in industrial automation environments, supporting improved data security and localized model inference for real-time operational efficiency.

In March 2024, Google Cloud announced enhanced Edge TPU models capable of delivering a 27% improvement in energy efficiency for AI inference workloads. The new design aims to accelerate AI adoption in sectors such as healthcare diagnostics, logistics, and manufacturing automation.

In December 2023, Microsoft Azure expanded its edge AI toolkit, enabling seamless model deployment from cloud to edge devices. The system improved workload processing speeds by 40% and allowed enterprises to optimize AI model lifecycle management across multi-cloud and on-premises environments.

The Edge AI Software Market Report provides an in-depth analysis of the global ecosystem, encompassing segmentation by type, application, and end-user industries across five key regions — North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The report covers over 25 distinct market segments and sub-segments, providing insight into the operational landscape of AI software deployed at the network edge.

The study explores technological frameworks such as federated learning, TinyML, and 5G-integrated AI systems that are reshaping the data processing paradigm. It further examines core applications in areas like autonomous vehicles, predictive maintenance, industrial IoT, and smart retail, representing nearly 60% of total market activity as of 2024. The scope also includes a detailed assessment of key end-user verticals, including manufacturing, healthcare, telecommunications, and energy, where adoption rates exceed 45% among enterprises.

Additionally, the report outlines competitive benchmarking, evaluating more than 20 active participants and their strategies related to innovation, product development, and global expansion. It emphasizes regulatory and compliance frameworks, environmental sustainability measures, and regional digital transformation initiatives. By combining quantitative data with qualitative insights, the report delivers a holistic understanding of the evolving Edge AI Software landscape, identifying emerging opportunities, disruptive technologies, and strategic pathways shaping the market toward 2032.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 1854.3 Million |

Market Revenue in 2032 | USD 15408 Million |

CAGR (2025 - 2032) | 30.3% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | NVIDIA Corporation, Microsoft Corporation, Intel Corporation, Alphabet Inc., IBM Corporation, Qualcomm Technologies Inc., Amazon Web Services, Inc., Huawei Technologies Co., Ltd., Arm Holdings, Advanced Micro Devices, Inc., General Electric Company, EdgeCortix Inc., FogHorn Systems, ClearBlade, Inc., Xilinx, Inc. |

Customization & Pricing | Available on Request (10% Customization is Free) |