Reports

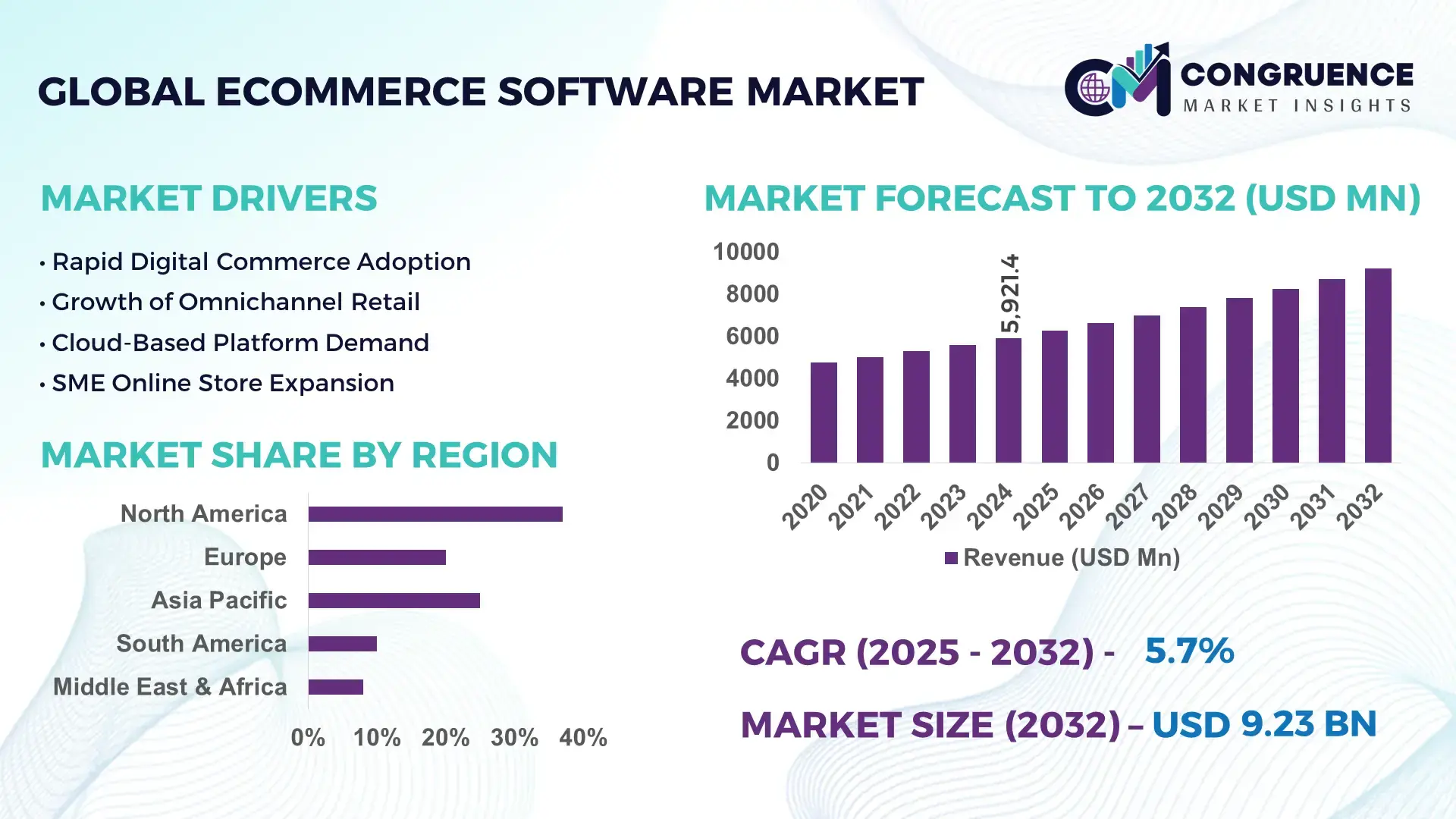

The Global eCommerce Software Market was valued at USD 5921.41 Million in 2024 and is anticipated to reach a value of USD 9226.26 Million by 2032 expanding at a CAGR of 5.7% between 2025 and 2032. Growth is driven by accelerated digital commerce adoption, omnichannel retail strategies, and continuous innovation in cloud-based commerce platforms.

The United States represents the most influential country in the global eCommerce software ecosystem, supported by advanced digital infrastructure, high enterprise IT spending, and large-scale platform development. In 2024, over 85% of U.S. enterprises with online sales used cloud-based eCommerce solutions, with SaaS deployments accounting for more than 70% of new installations. Annual private and public investment in digital commerce platforms exceeded USD 120 billion, focusing on AI-driven personalization, headless commerce architectures, and API-based integrations. The country hosts major software production hubs and supports extensive application across retail, B2B manufacturing, subscription services, and digital marketplaces, with mobile commerce transactions representing nearly 44% of total online purchases.

Market Size & Growth: Valued at USD 5921.41 Million in 2024, projected to reach USD 9226.26 Million by 2032 at a CAGR of 5.7%, driven by cloud migration and rising digital transaction volumes.

Top Growth Drivers: Cloud adoption at 68%, AI-based personalization improving conversion rates by 30%, mobile commerce penetration increasing by 42%.

Short-Term Forecast: By 2028, average eCommerce platform operating costs are expected to decline by 18% through SaaS optimization and automation.

Emerging Technologies: Headless commerce, AI-powered recommendation engines, and composable commerce frameworks.

Regional Leaders: North America projected at USD 3520 Million by 2032 with strong B2B adoption; Asia-Pacific at USD 2980 Million driven by mobile-first users; Europe at USD 2140 Million supported by cross-border digital trade.

Consumer/End-User Trends: SMEs and direct-to-consumer brands increasingly adopt modular platforms to enable faster storefront customization and omnichannel experiences.

Pilot or Case Example: In 2024, a large U.S. retailer deployed AI-driven eCommerce software, improving checkout efficiency by 27% and reducing cart abandonment by 19%.

Competitive Landscape: Shopify leads with approximately 23% share, followed by Adobe Commerce, Salesforce Commerce Cloud, BigCommerce, and SAP Commerce.

Regulatory & ESG Impact: Data protection regulations and green IT initiatives are accelerating adoption of secure, energy-efficient cloud platforms.

Investment & Funding Patterns: Over USD 35 billion invested globally between 2023–2024, with strong venture funding for AI-native and vertical-specific platforms.

Innovation & Future Outlook: Increased integration of AI agents, low-code customization, and unified commerce platforms shaping next-generation deployments.

The eCommerce software market serves key industry sectors including retail, B2B wholesale, consumer electronics, fashion, and digital services, with retail and B2B commerce together accounting for over 60% of platform deployments. Recent innovations such as headless storefronts, AI-based demand forecasting, and real-time analytics have improved scalability and customer experience. Regulatory requirements related to data privacy, digital taxation, and cross-border trade compliance continue to influence platform architecture. Regionally, Asia-Pacific shows the fastest consumption growth due to mobile commerce and super-app ecosystems, while North America focuses on enterprise-grade integrations. Looking ahead, composable commerce, embedded finance, and AI-driven automation are expected to redefine platform competitiveness and long-term market evolution.

The eCommerce Software Market holds strong strategic relevance as it underpins digital revenue generation, customer experience management, and scalable global commerce operations for enterprises across sectors. Modern platforms increasingly function as core enterprise systems, integrating inventory management, payments, CRM, analytics, and marketing automation. Cloud-native and headless commerce architectures now enable deployment cycles that are 45% faster than traditional monolithic platforms, while composable commerce delivers a 30% improvement in feature scalability compared to legacy all-in-one systems.

From a comparative benchmark perspective, AI-driven personalization engines deliver up to 25% higher conversion rates compared to rule-based recommendation standards. North America dominates in transaction volume due to high enterprise digital maturity, while Asia-Pacific leads in adoption with over 72% of online retailers operating mobile-first or super-app–integrated commerce platforms. By 2028, generative AI and automated merchandising tools are expected to reduce customer acquisition costs by nearly 20% through improved targeting and dynamic pricing.

Compliance and ESG considerations are shaping platform strategies, with firms committing to measurable sustainability goals such as a 35% reduction in data-center energy intensity by 2030 through cloud optimization and green hosting. In 2024, a U.S.-based enterprise retailer achieved a 22% reduction in checkout abandonment through AI-enabled workflow optimization and real-time fraud detection. Looking ahead, the eCommerce Software Market is positioned as a pillar of operational resilience, regulatory compliance, and sustainable digital growth across global commerce ecosystems.

The accelerating shift toward omnichannel retail and mobile commerce is a primary driver of the eCommerce Software Market. More than 60% of global online transactions now originate from mobile devices, prompting enterprises to adopt responsive, API-driven platforms capable of supporting multiple touchpoints. Businesses using unified commerce software report inventory accuracy improvements of up to 35% and order fulfillment speed gains of nearly 25%. Additionally, social commerce integrations and in-app purchasing features are expanding platform usage beyond traditional websites. Retailers adopting omnichannel eCommerce software also experience higher customer retention, with repeat purchase rates increasing by approximately 20%, reinforcing sustained platform demand across retail, B2B, and service sectors.

Data security risks and system integration complexity present notable restraints for the eCommerce Software Market. As platforms handle sensitive customer, payment, and behavioral data, enterprises face rising exposure to cyber threats, with reported eCommerce-related data breaches increasing by over 15% annually. Compliance with data protection regulations requires continuous investment in encryption, monitoring, and governance tools. Additionally, integrating eCommerce software with legacy ERP, supply chain, and CRM systems can extend deployment timelines by 30–40%, particularly for large enterprises. These challenges increase implementation costs and delay ROI realization, causing some organizations to postpone platform upgrades or limit feature adoption.

AI-driven automation presents significant opportunities within the eCommerce Software Market by enhancing efficiency, personalization, and decision-making. Automated product recommendations, dynamic pricing, and predictive inventory management can reduce stockouts by up to 28% while improving margin optimization. AI-powered chatbots and virtual assistants now handle nearly 50% of routine customer service interactions, lowering support workloads and response times. Emerging opportunities also exist in vertical-specific platforms tailored for B2B manufacturing, healthcare commerce, and subscription-based services. As enterprises seek modular solutions that adapt quickly to market changes, AI-native eCommerce platforms are increasingly positioned as strategic growth enablers.

Rising operational costs and regulatory complexity pose ongoing challenges for the eCommerce Software Market. Continuous platform upgrades, cybersecurity investments, and compliance requirements increase total cost of ownership, particularly for small and mid-sized enterprises. Regulations governing data privacy, digital taxation, and cross-border transactions require frequent system updates and localized configurations. In parallel, the cost of skilled technical talent for platform customization and maintenance has risen by more than 20% in key markets. These factors strain budgets and slow deployment cycles, making it challenging for organizations to fully leverage advanced eCommerce capabilities at scale.

• Accelerated Shift Toward Modular and Composable Commerce Architectures

The adoption of modular and composable commerce frameworks is reshaping enterprise platform strategies in the eCommerce Software market. Nearly 58% of newly deployed enterprise eCommerce platforms now use modular architectures, enabling faster feature rollouts and system customization. Organizations adopting composable stacks report implementation time reductions of up to 35% and development cost savings of around 25%. API-first designs allow independent upgrades of checkout, catalog, and payment modules, improving system resilience and reducing vendor lock-in across retail and B2B commerce environments.

• Rapid Expansion of AI-Driven Personalization and Automation Capabilities

AI integration has become a defining trend, with over 62% of eCommerce software platforms embedding machine learning for personalization, pricing, and demand forecasting. AI-powered recommendation engines improve average order value by approximately 20% and boost conversion rates by nearly 28% compared to static merchandising tools. Automated merchandising and content generation tools reduce manual catalog management effort by 40%, enabling enterprises to scale product assortments while maintaining consistent customer experiences across channels.

• Growing Emphasis on Headless and Omnichannel Platform Deployment

Headless commerce adoption continues to accelerate, with more than 46% of mid-to-large enterprises implementing decoupled front-end and back-end architectures. This approach improves page load performance by up to 30% and enables seamless integration across web, mobile, social, and in-store touchpoints. Businesses leveraging omnichannel eCommerce software report customer engagement improvements of 22% and inventory visibility gains of nearly 33%, supporting real-time fulfillment and unified customer journeys.

• Increased Focus on Security, Compliance, and Sustainable Infrastructure

Security and compliance enhancements are increasingly embedded within eCommerce software platforms as regulatory complexity rises. Around 64% of vendors now offer built-in compliance automation for data protection and cross-border transactions, reducing audit preparation time by 26%. Simultaneously, enterprises are migrating to energy-efficient cloud infrastructures, achieving data-center energy consumption reductions of up to 30%. Sustainability-focused platform optimization is becoming a standard procurement criterion, influencing long-term software adoption decisions.

The eCommerce Software Market segmentation highlights clear differentiation across platform types, application areas, and end-user adoption patterns. Enterprises increasingly select solutions based on deployment flexibility, scalability, and integration depth rather than single-function capabilities. Platform types are evolving from monolithic systems toward modular and API-driven architectures, while applications span consumer-facing retail, B2B commerce, and cross-border digital trade. End-user demand varies significantly by organization size and industry maturity, with large enterprises prioritizing omnichannel orchestration and SMEs focusing on rapid deployment and cost efficiency. Across segments, adoption is closely linked to automation levels, data analytics maturity, and the ability to support personalized digital experiences at scale.

The eCommerce Software Market by type includes SaaS-based platforms, on-premise solutions, headless commerce platforms, and composable or modular commerce systems. SaaS-based eCommerce software currently leads the segment, accounting for approximately 46% of total adoption, driven by faster deployment cycles, subscription-based pricing, and reduced infrastructure dependency. Headless commerce platforms represent around 28% of adoption, while traditional on-premise systems account for nearly 16%. However, composable commerce platforms are the fastest-growing type, expanding at an estimated CAGR of 14.2%, fueled by enterprise demand for flexibility, API-driven integrations, and independent feature scaling. The remaining niche types collectively contribute about 10%, serving highly regulated or legacy-dependent environments.

By application, the eCommerce Software Market is segmented into B2C retail commerce, B2B commerce, marketplace platforms, and subscription-based digital commerce. B2C retail applications dominate with nearly 41% share, supported by high transaction volumes, mobile shopping penetration exceeding 60%, and strong personalization requirements. B2B commerce applications follow with around 34%, reflecting increasing digitization of procurement and wholesale transactions. Marketplace platforms hold approximately 15%, while subscription commerce accounts for the remaining 10%. Subscription-based commerce is the fastest-growing application, expanding at an estimated CAGR of 12.6%, driven by recurring billing models, digital services, and D2C brand strategies.

End-user segmentation in the eCommerce Software Market includes large enterprises, small and medium-sized enterprises (SMEs), and digital-first startups. Large enterprises lead adoption with approximately 49% share, driven by omnichannel complexity, global operations, and advanced analytics requirements. SMEs account for around 33%, while startups and niche digital players represent about 18%. However, SMEs are the fastest-growing end-user group, expanding at an estimated CAGR of 13.8%, supported by SaaS affordability, no-code customization, and rapid go-live capabilities. Adoption rates among SMEs in retail and services exceed 55%, reflecting growing confidence in cloud-native platforms.

North America accounted for the largest market share at 38.6% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2025 and 2032.

North America’s leadership is supported by high enterprise digital maturity, with over 72% of medium-to-large businesses operating advanced eCommerce platforms. Europe followed with approximately 27.4% share, driven by cross-border digital trade and regulatory-aligned software demand. Asia-Pacific held nearly 24.1% share in 2024, supported by strong platform adoption among SMEs and mobile-first commerce ecosystems, while South America and the Middle East & Africa together accounted for about 9.9%. Regionally, mobile commerce transactions exceed 65% of total online purchases in Asia-Pacific, compared to 48% in North America, highlighting different consumption dynamics. Investment intensity, regulatory complexity, and platform localization needs continue to shape region-specific deployment strategies across the eCommerce Software Market.

How is enterprise-scale digital transformation redefining platform adoption patterns?

North America represents approximately 38.6% of the global eCommerce Software Market, supported by strong demand from retail, healthcare, financial services, and B2B manufacturing sectors. Over 68% of enterprises in the region operate cloud-native or hybrid eCommerce platforms integrated with ERP and CRM systems. Regulatory frameworks around data protection and digital payments have accelerated adoption of secure, compliance-ready platforms. Technological advancements such as AI-driven personalization, headless commerce, and predictive analytics are widely deployed, with nearly 60% of large retailers using AI-based merchandising tools. A prominent regional platform provider expanded its headless commerce offerings in 2024, enabling faster omnichannel rollouts across thousands of enterprise storefronts. Consumer behavior shows higher adoption of subscription commerce and complex checkout workflows, particularly in healthcare and financial services digital channels.

Why does regulatory alignment shape platform selection and customization priorities?

Europe accounts for roughly 27.4% of the eCommerce Software Market, with Germany, the UK, and France representing more than 62% of regional adoption. Strong regulatory oversight related to data privacy, consumer protection, and digital sustainability drives demand for transparent and compliant software architectures. Over 54% of enterprises prioritize explainable AI and auditable transaction workflows when selecting platforms. Adoption of emerging technologies such as composable commerce and cross-border tax automation is increasing, particularly among multinational retailers. A European-based software vendor introduced region-specific compliance automation tools in 2024, reducing cross-border checkout errors by 21%. Consumer behavior reflects high sensitivity to data usage transparency, reinforcing demand for configurable consent and localization features.

How are mobile-first ecosystems accelerating platform scalability and usage volume?

Asia-Pacific holds approximately 24.1% share of the eCommerce Software Market and ranks as the fastest-expanding regional market by adoption volume. China, India, and Japan together account for over 70% of regional platform deployments. Infrastructure investments in cloud data centers and digital payment rails support rapid scaling, with mobile transactions representing more than 65% of online commerce activity. Regional innovation hubs are driving adoption of AI chat commerce, super-app integrations, and social commerce enablement. A leading regional platform provider enhanced AI-powered live commerce tools in 2024, supporting millions of daily transactions during peak sales events. Consumer behavior is heavily influenced by mobile apps, embedded payments, and real-time engagement features.

Why is localization becoming critical for digital commerce expansion?

South America represents around 6.2% of the global eCommerce Software Market, led by Brazil and Argentina. Growing internet penetration and digital payment adoption are increasing platform demand, particularly among retail and media-driven commerce sectors. Government initiatives supporting digital trade and cross-border eCommerce have improved platform accessibility for SMEs. Infrastructure modernization, including cloud hosting and logistics digitization, is reducing deployment barriers. A regional software provider focused on multilingual storefronts and localized payment integrations in 2024, improving checkout completion rates by 18%. Consumer behavior in the region shows strong preference for localized language support, installment payments, and mobile-optimized interfaces.

How is digital modernization reshaping commerce platforms across emerging economies?

The Middle East & Africa account for approximately 3.7% of the eCommerce Software Market, with the UAE and South Africa as primary growth hubs. Demand is driven by retail diversification, construction-linked B2B commerce, and expanding digital services. Governments are promoting digital economy strategies, leading to increased adoption of cloud-based commerce platforms. Technological modernization includes mobile payment integration and AI-powered fraud prevention, with over 40% of new platforms supporting real-time risk analytics. A regional platform provider partnered with logistics firms in 2024 to improve delivery orchestration across urban centers. Consumer behavior varies widely, with strong growth in mobile commerce and cashless payment adoption in urban markets.

United States eCommerce Software Market – 32.1% share: Dominance driven by high enterprise adoption, advanced cloud infrastructure, and large-scale omnichannel platform deployments.

China eCommerce Software Market – 18.4% share: Strong position supported by massive transaction volumes, mobile-first commerce ecosystems, and widespread integration of AI-driven platform features.

The eCommerce Software market is characterized by a moderately consolidated yet highly competitive environment, with more than 120 active global and regional vendors offering platforms across SaaS, headless, and composable architectures. The market shows consolidation at the top, where the top five companies collectively account for approximately 55% of total deployments, while the remaining share is distributed among mid-sized vendors and niche specialists targeting vertical-specific or regional requirements. Competition is primarily driven by platform scalability, ecosystem depth, API extensibility, and speed of innovation rather than price alone.

Strategic initiatives such as partnerships with cloud hyperscalers, payment service providers, and logistics platforms have increased by over 30% since 2023, enabling vendors to offer end-to-end commerce ecosystems. Product launches increasingly focus on AI-powered personalization, no-code storefront customization, and real-time analytics, with more than 65% of leading vendors embedding native AI capabilities into their platforms. Mergers and acquisitions remain selective, largely aimed at expanding B2B commerce, subscription billing, and cross-border compliance capabilities. The competitive intensity is further amplified by open-source frameworks and low-code platforms, which lower entry barriers while pushing established players to continuously enhance performance, security, and omnichannel orchestration.

Shopify

Adobe Commerce

Salesforce Commerce Cloud

SAP Commerce

BigCommerce

Oracle Commerce

VTEX

WooCommerce

Magento Open Source

OpenCart

Technology innovation is a central force shaping the evolution of the eCommerce Software Market, with enterprises increasingly prioritizing platforms that deliver scalability, automation, and data-driven decision-making. Cloud-native architectures dominate current deployments, with more than 70% of new eCommerce platforms implemented on public or hybrid cloud environments to support elastic traffic handling and rapid global expansion. API-first and microservices-based designs enable modular upgrades, reducing platform downtime by up to 30% during feature enhancements and integrations.

Artificial intelligence and machine learning are now embedded across core commerce functions. AI-powered recommendation engines improve average order values by approximately 18–25%, while predictive demand forecasting tools reduce inventory stockouts by nearly 28%. Generative AI is increasingly used for automated product content creation, with enterprises reporting a 40% reduction in manual catalog management effort. Natural language processing supports conversational commerce, allowing chatbots and voice assistants to handle over 50% of routine customer inquiries.

Headless commerce technology continues to gain traction, with around 46% of mid-to-large enterprises adopting decoupled front-end frameworks to improve page load speed by up to 30% and enable seamless omnichannel experiences. Security technologies such as tokenization, real-time fraud detection, and zero-trust authentication are being integrated into platforms, reducing fraudulent transactions by 20–35%. Additionally, sustainability-focused technologies, including energy-efficient cloud hosting and workload optimization, are enabling enterprises to cut data-center energy consumption by nearly 25%, aligning digital commerce operations with long-term ESG objectives.

• In January 2023, Adobe Commerce expanded its composable development tools and AI-powered personalization features, including enhanced App Builder and API Mesh capabilities that streamline third-party integrations and reduce backend integration effort by up to 50%, enabling more dynamic and flexible commerce experiences across retail and enterprise use cases. (Adobe Business)

• In December 2024, Shopify released its Winter ’25 Edition, delivering more than 150 platform updates, including checkout improvements that boost load speeds by up to 50% and enhanced customization options for checkout blocks and cart workflows, improving operational scalability for merchants of all sizes. (Shopify)

• In September 2024, Salesforce introduced the next-generation Commerce Cloud with unified platform and AI agents, including Merchant, Buyer, and Personal Shopper autonomous agents designed to manage recommendations and order lookup tasks, advancing retailer automation and cross-channel personalization at scale. (Salesforce)

• In 2025, Salesforce launched Agentforce Commerce, a unified agentic shopping platform that enables retailers to syndicate product catalogs into consumer AI channels such as ChatGPT and offers guided shopping and order routing, supported by a reported 119% year-over-year growth in AI assistant traffic, marking a significant shift toward agent-driven digital shopping. (Salesforce)

The scope of the eCommerce Software Market Report encompasses a comprehensive examination of platform offerings, application domains, technological drivers, and end-user behaviors shaping the global digital commerce ecosystem. It includes segmentation by platform type—such as SaaS, headless, and composable commerce systems—highlighting architectural design, integration patterns, API-first strategies, and adoption across enterprise and SMB landscapes. The geographic scope spans major regions, including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed insights into market volume distribution, technology uptake, and regional digital infrastructure capabilities.

Application segmentation covers critical use cases such as B2C retail commerce, B2B commerce platforms, marketplace enablement, and subscription-based digital services, with emphasis on demand dynamics, operational workflows, and customer experience outcomes. The report also analyzes emerging and niche segments like omnichannel orchestration, cross-border commerce, social commerce integration, and mobile-first ecosystem adoption. Technology focus areas include cloud-native platforms, AI-embedded automation, headless & composable architectures, predictive analytics, and security & compliance capabilities, detailing how these technologies influence enterprise decision-making and competitive differentiation.

End-user coverage profiles adoption and usage patterns across large enterprises, small and medium enterprises, and digital-native startups, with metrics on platform penetration, feature utilization, and buyer priority shifts. The report offers evaluation of innovation trends, strategic partnerships, product roadmaps, regulatory impacts, and sustainability trends affecting procurement and platform evolution. Through a combination of qualitative insights and numerical indicators, this scope delivers a holistic view of market breadth, competitive pressures, and future trajectories for business leaders and technology strategists.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 5921.41 Million |

Market Revenue in 2032 | USD 9226.26 Million |

CAGR (2025 - 2032) | 5.7% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Shopify, Adobe Commerce, Salesforce Commerce Cloud, SAP Commerce, BigCommerce, Oracle Commerce, VTEX, WooCommerce, Magento Open Source, OpenCart |

Customization & Pricing | Available on Request (10% Customization is Free) |